Since May 1 of this year, we have seen a pretty-much unprecedented rise in Treasury yields, almost blindingly quick as the Federal Reserve began to slowly back away (verbally, not in action) from its bond-buying stimulus program.

- On May 1, the 10-year nominal Treasury yielded 1.66%. Today it stands at 2.82%, a rise of 116 basis points

- On May 1, a 10-year Treasury Inflation Protected-Security was yielding -0.64% and now is yielding 0.69%, an even higher rise of 133 basis points.

Can this continue? Can TIPS and Treasury yields rise another 100, 200 or even 250 basis points over the next year or two? The answer is yes, they can. I’d suggest an increase of nearly 200 basis points in the nominal 10-year Treasury looks probable if the economy continues to improve and Fed backs off from bond-buying, which holds yields down.

My thinking comes from looking at traditional Treasury rates and their spread over inflation, as shown in this chart for inflation and rates back to 1990:

| Date | 10-year Treasury | Inflation rate that year | Spread over inflation | 10-year TIPS yield |

| 1-Aug-90 | 8.29 | 4.7 | 3.59 | NA |

| 1-Aug-91 | 8.20 | 4.7 | 3.50 | NA |

| 1-Aug-92 | 6.72 | 3.1 | 3.62 | NA |

| 1-Aug-93 | 5.85 | 3.0 | 2.85 | NA |

| 1-Aug-94 | 7.13 | 2.5 | 4.63 | NA |

| 1-Aug-95 | 6.50 | 3.0 | 3.50 | NA |

| 1-Aug-96 | 6.65 | 2.8 | 3.85 | NA |

| 1-Aug-97 | 6.20 | 2.3 | 3.90 | 3.65 |

| 1-Aug-98 | 5.46 | 1.7 | 3.76 | 3.65 |

| 1-Aug-99 | 5.92 | 2.0 | 3.92 | 4.04 |

| 1-Aug-00 | 6.00 | 3.7 | 2.30 | 4.03 |

| 1-Aug-01 | 5.11 | 3.3 | 1.81 | 3.50 |

| 1-Aug-02 | 4.33 | 1.1 | 3.23 | 3.10 |

| 1-Aug-03 | 4.44 | 2.1 | 2.34 | 2.40 |

| 1-Aug-04 | 4.48 | 3.3 | 1.18 | 2.00 |

| 1-Aug-05 | 4.32 | 2.5 | 1.82 | 1.95 |

| 1-Aug-06 | 4.99 | 4.3 | 0.69 | 2.40 |

| 1-Aug-07 | 4.76 | 2.7 | 2.06 | 2.44 |

| 1-Aug-08 | 3.97 | 5.0 | -1.03 | 1.63 |

| 1-Aug-09 | 3.66 | -1.4 | 5.06 | 1.78 |

| 1-Aug-10 | 2.99 | 1.1 | 1.89 | 1.13 |

| 1-Aug-11 | 2.77 | 3.6 | -0.83 | 1.09 |

| 1-Aug-12 | 1.56 | 1.7 | -0.14 | -0.07 |

| 1-Aug-13 | 2.74 | 1.8 | 0.94 | 0.38 |

| Average | 5.12 | 2.7 | 2.42 | 2.30 |

| Median | 5.05 | 2.8 | 2.60 | 2.40 |

So, some assumptions:

- Inflation. As the economy improves, inflation will return to its-more-less historic rate of 2.5% a year. I am being generous here, it could be higher. The Federal Reserve is practically guaranteeing that inflation will be above 2%, not capped there, but above 2% no matter what.

- Spread over inflation. Historically, a 10-year Treasury pays a yield about 2.5% above inflation. Obviously, that can vary widely from year to year, and has even dipped into the negative range in recent years.

- 10-year Treasury. The current rate of U.S. inflation is 1.8%, so even if you apply a 2% spread over inflation, you get a 10-year Treasury yield of 3.8%, 100 basis points higher than it is today. If inflation rises to 2.5% and the spread rises to 2.5%, you get a 10-year Treasury yield of 5%, 218 basis points higher than today. This is entirely possible, as the numbers show.

- 10-year TIPS. Since being introduced in 1997, the 10-year TIPS has had an average inflation breakeven rate of 2.04%. In recent years it has been riding between 2.0% and 2.5%, and is currently at 2.13%.

- Projecting the TIPS yield. Using the average breakeven rate (which is pretty low, in my opinion), a 10-year nominal Treasury paying 3.8% results in a 10-year TIPS yield of 1.76%, a rise of 107 basis points. A Treasury paying 5% results in a 10-year TIPS yield of 2.96%, a rise of 227 basis points.

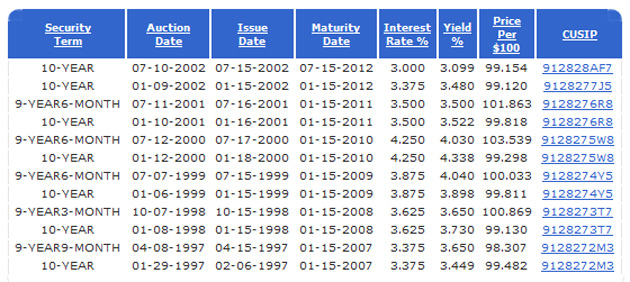

Improbable? Sure the high end of that TIPS yield looks unlikely. But a 10-year TIPS paying 2.96% would not be an anomaly. In fact, every 9- or 10-year TIPS auction from 1997 to July 2002 had a yield higher than 2.96%:

It’s interesting to note how consistent those yields are, across a period of time that including a booming economy (late 1990s) to a savage stock market collapse (early 2000s). I would argue that these yields were the norm, not an anomaly. Instead, the ultra-low, artificially manipulated rates of 2011 to early 2013 were the anomaly, and that anomaly is now returning to the norm.

What it means. Nothing is certain. The economy could nose-dive, war could erupt in the Mideast, China could collapse. That would send TIPS yields plummeting. I am comfortable making small investments in TIPS at these current rates, to add to a portfolio.

But if the economy continues to improve, and the Federal Reserve halts bond-buying, we are looking at inflation of 2.5% a year and TIPS and Treasury rates at least 100 basis points higher.

Pingback: What would ‘normal’ TIPS yields look like? | Treasury Inflation-Protected Securities

Pingback: TIPS mutal funds got a reality check in 2013, more trouble to come? | Treasury Inflation-Protected Securities

Dave,

I’ll take advantage of your “Nothing is certain.”.

The past is certain, so folks should see it soundly shown:

http://patrick.net/forum/?p=1223928

Ed

Correct, even my big chart showed an August 1997 rate. Anyway, I subbed out that lower chart and thanks for the alert.

Dave,

10 yr TIPS began earlier, as I recall.