After a month of very sharp rises in the yield on Treasury Inflation-Protected Securities, the trend continued Monday, with the yield on the benchmark 10-year TIPS rising to 0.11%, plus inflation, marking two trading days in a row the yield has gone positive.

That is an incredible gain of 75 basis points since May 1, when the yield stood at -0.64%. This is the first time the 10-year TIPS yield has gone positive since Dec. 15, 2011. That has been a very long, painful slog for net buyers of TIPS (buying more than mature each year).

The trend has reversed. TIPS are interesting again, for the buy-and-hold investor.

Buy and hold is my TIPS philosophy. That means buying TIPS at TreasuryDirect and holding them to maturity. There is very little risk in this strategy. You aren’t trading, you can ignore the secondary price and never consider ‘duration.’ Along with I Bond purchases, it is a very conservative way to preserve capital, for a portion of your portfolio. (And a poor way to build wealth, I must say.)

However, buyers should be choosy. I stopped buying TIPS in June 2011, a 30-year TIPS with a yield of 1.774%. Nearly two years later, last month, I got back in the game, purchasing the 10-year TIPS reissue with a yield of -0.225%.

Painful day. But for investors in TIPS mutual funds and ETFs, these are painful times. The flagship ETF, with the ticker TIP, declined $0.80 today to close at $114.64, down 0.69% on the day and down 5.9% since May 1.

Obviously, money is pouring out of TIPS funds, just as it poured in during a heady 20-month period from July 1, 2011, to April 30, 2013, when TIP increased from $105.96 to $122.15, or 13.3%.

Unlike a stock mutual fund, there are no ‘fundamentals’ to support the price of the ETF or other TIPS mutual funds. No one looks at 200-day moving averages or strange chart formations. The value of TIPS is determined by the yield to maturity, and the yield is rising. That means the price is falling, and will keep falling as long as the yield increases.

There are several factors at work here:

- Overall interest rates are rising. The nominal 10-year Treasury closed today at 2.22%, up 56 basis points since May 1.

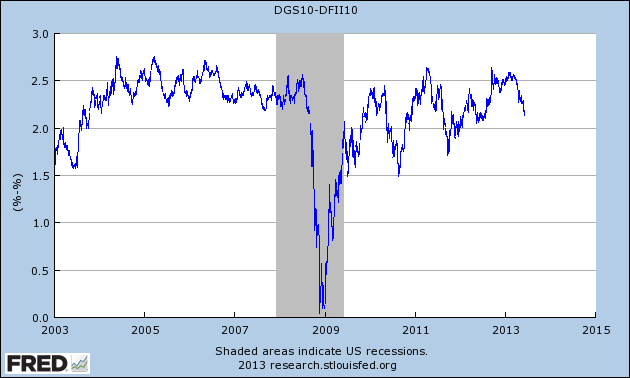

- The yield on TIPS is rising even faster – 77 basis points since May 1. That means TIPS are getting cheaper versus traditional Treasurys. Today’s 10-year inflation breakeven rate stands at 2.11%, getting close to my 2.0% ‘cheap’ marker.

- Inflation is currently muted, running just 1.1% over the last 12 months. Since TIPS offer extremely low yields, low inflation is a double whammy for TIPS holders.

- Despite the pain for traders and mutual fund investors, TIPS are a much better deal for investors today than they were 40 days ago. This chart shows just how rarely the breakeven rate drops below 2.0%:

At some point, I might get interested in TIPS mutual funds. I speculate (not with money, just my mind) that the TIP ETF is heading down to about $110 and the 10-year Treasury will hit 2.75%. At that point, a 10-year TIPS would be yielding maybe 0.55%, maybe higher, but still substantially below the 1% to 2% that TIPS investors saw in the past.

I am often wrong. Very wrong. Back in May 2011, I wrote a blog explaining why I was exiting Fidelity Inflation Protected Bond (FINPX) in favor of Vanguard Total Bond Fund. I was doing this at EXACTLY the wrong time, and to my embarrassment, this was one of my most popular blog posts of all time. It still gets viewed, every day.

Oh well, here is how that worked out:

I looked wise for about a month, then very stupid as the Federal Reserve launched QE after QE, buying Treasurys and creating money to stimulate the economy.

But my bond portfolio is more about preserving capital, along with a minimal interest-rate return. Vanguard Total Bond Fund is still one of my favorites. And here’s how it has gone since May 1:

I won’t claim to know what the future holds. I have long believed that yields on TIPS were unnaturally low, and that trend had to – and would – reserve. I think that trend has started. Let’s watch to see if I am right.

Not to worry - as testified under oath before Congress, if confirmed as Fed Chair, Warsh is going to change…