Buy in April to lock in the 1.2% fixed rate? Or buy in May to start with a higher composite rate?

April 30 update: I Bond gets a new fixed rate of 1.10%, composite rate of 3.98%

By David Enna, Tipswatch.com

Long-time investors in U.S. Series I Savings Bonds know there are a few weeks a year when conditions are ideal for making a decision: Purchase now or purchase later?

With Thursday’s release of the March 2025 inflation report, we have entered one of these “buying seasons,” which will continue through the end of April. But before we get to the details, let’s look at some basics of this investment:

An I Bond is a Treasury security that earns interest based on combining a fixed rate and an inflation-adjusted rate.

- The inflation-adjusted rate (often called the variable rate) changes each six months to reflect the running rate of inflation. That annualized rate is currently set at 1.90% and will increase to 2.86% after May 1. All I Bonds will eventually get the 2.86% variable rate, with the start date depending on the original month of purchase.

- The fixed rate will never change. So if you bought an I Bond in 2014 with a fixed rate of 0.2%, it will continue to have a 0.2% fixed rate for the life of the bond. Purchases through April 29, 2025, have a permanent fixed rate of 1.2%.

- The composite rate is a combination of these two rates, currently 3.11% annualized for a full six months for any bond purchased through April 2025.

The variable rate

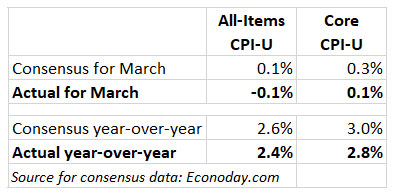

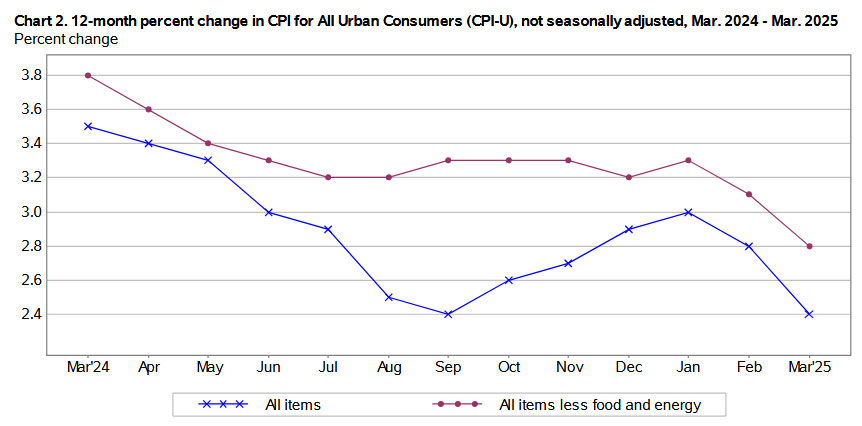

Here is where we have certainty. The March CPI report provided the final number needed to set the I Bond’s new variable rate. Inflation ran at 1.43% from October 2024 to March 2025. Double that number and you get the new variable rate, 2.86%, up from the current 1.90%.

The new variable rate, 2.86%, is a big jump from the current rate of 1.90%. It makes an I Bond purchase in May more attractive, but remember that the variable rate changes every six months. All I Bonds, including those purchased in April, will get this new variable rate for six months.

The fixed rate

Here is where we lack certainty, except for one thing: If you purchase an I Bond in April, you will lock in the 1.20% fixed rate for the life of the I Bond, up to 30 years. We don’t know for sure how the Treasury will reset that fixed rate on May 1, which will apply to purchases from May to October.

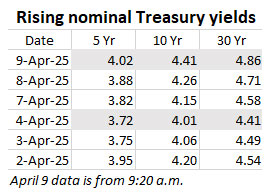

The Treasury has no announced formula for setting the I Bond’s fixed rate, but I Bond watchers have settled on a forecasting tool that seems to work: Apply a ratio of 0.65 to the average 5-year TIPS real yield over the preceding six months. This formula has worked without fail at least since 2017.

On Friday I updated my 5-year real yield data from the date of the last reset on November 1, 2024, to Thursday’s close. The data predict the I Bond’s fixed rate will fall to 1.10% at the May 1 reset:

The I Bond’s fixed rate is always set to the one-tenth decimal point and that means the result of the 0.65 ratio calculation has to be rounded, which results in a projection of 1.10%. With only 12 market days remaining to the reset, that level is likely to stick.

However … We have a new administration running the Treasury Department at a time of some fairly dramatic employee reductions. There is no way to be sure what formula, if any, the Treasury will use to set the new fixed rate. I think it will be 1.10%, but this is not certain.

The composite rate

If you purchase I Bonds in April, you have one year of certainty: You will earn a composite rate of 3.11% for six months and then 4.08% for six months. Combine the rates and you get to a annual compounded rate of 3.64%. According to Bogleheads genius #Cruncher, a $10,000 investment will grow to $10,364 in one year (ignoring the 3-month interest penalty for redemptions before 5 years.)

Obviously, 3.64% isn’t going to make you wealthy over the next year, but I Bonds are more about protecting wealth than building wealth. An I Bond purchased in April is going to earn 1.2% above official U.S. inflation for as long as you hold it.

Purchasing in May opens a couple of unknown variables: 1) we don’t know for certain what the new fixed rate will be, and 2) we don’t know what will happen with inflation over the next six months. But it is certainly possible that a purchase in May will end up with a higher one-year return than a purchase in April, if inflation continues at a brisk pace.

Keep in mind that the difference between a 1.20% fixed rate and 1.10% (if that is the new fixed rate) is only 10 basis points, which equals just $10 of annual interest on $10,000 of principal. Not life changing.

Conclusion. I have been recommending buying in April (and I completed my purchases for 2025 in March). I’d still recommend April, but this decision is a bit of a toss-up and most likely both April or May purchases will work out well. If you want certainty, buy near the end of April (no later than April 28). If you want to wait it out, then buy in late May or …

What about October?

I Bond purchases are limited to $10,000 per person per year unless you add to your holdings through gift-box, trusts, or business-owner strategies. Some people like to spread I Bond purchases over the year, for example $5,000 in April and then $5,000 in October, or possibly even in November at the next reset.

The next “buying season” will open Oct. 15 with the release of the September inflation report, when we will know the next I Bond variable rate. And what about the fixed rate? I have been saying I know with 100% certainty that the November fixed rate will fall into the range of 0.0% to 4.0%. In other words … who knows? We have entered a year of wild financial possibilities.

One important thing to remember is that the November rate decision will be available for purchase in January 2026 when the purchase cap resets.

Are I Bonds that attractive?

With short-term T-bill rates still topping 4%, many investors are shunning I Bonds because of the potentially lower nominal return plus the three-month interest penalty for redemptions within five years. Some thoughts:

- We just went through a phase of inflation hitting 40-year highs, and higher prices could be returning in 2025 as we enter a turbulent era. Inflation protection, for part of your portfolio, looks like a wise choice.

- Eventually, the Federal Reserve would like to resume cutting short-term interest rates and then the T-bill returns will begin falling. But, yes, the future of rate cuts is unclear. T-bills remain attractive.

- I Bonds, if held for 5 years, create an inflation-protected store of cash you can use for future needs, with no penalty for redemption except for federal taxes on the interest.

Is this a short-term investment? I Bonds aren’t a good choice for money you will need in the next one or two years. You can get a 1-year T-bill paying about 3.9%. That nominal yield will beat the return of an I Bond after the three-month interest penalty is applied. I Bonds are best viewed as a longer-term, cash-equivalent investment.

Thoughts

I am a long-time advocate for investing in I Bonds, which create a tax-deferred, totally safe, inflation-protected investment with a flexible maturity date. If inflation heats up again as it did in 2022, you will sleep better at night with a treasure chest of I Bonds.

Again, this investment is not designed to make you rich. It is designed to protect a portion of your nest egg against inflation. April or May? It may not matter much, but I still stand behind I Bonds as an investment in 2025.

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Hi, and thanks for the nice synopsis of the upcoming auction expectations. I will be a buyer since I need…