I Bonds, a U.S. Savings Bond you can buy and hold at TreasuryDirect.gov, are currently paying a base rate of 0.0% and an inflation-adjustment rate of 1.76%, but that rate only applies to bonds purchased by April 30.

I Bonds, a U.S. Savings Bond you can buy and hold at TreasuryDirect.gov, are currently paying a base rate of 0.0% and an inflation-adjustment rate of 1.76%, but that rate only applies to bonds purchased by April 30.

On May 1, the inflation-adjustment rate will fall to 1.18%, and the base rate will continue at 0.0%.

What this means. If you buy before April 30, you can lock in the 1.76% rate for six months, then get the 1.18% rate for six months, for an annual rate of 1.47%. You can sell the I Bond after one year, but you will forfeit 3 months’ interest. You can sell after 5 years with no penalty.

I Bonds don’t seem exciting at this point, and the interest rate you’ll get in the next year is barely competitive with a 5-year Bank CD. But I highly recommend buying them, and I’d suggest buying to the $10,000 per person limit by April 30. Reasons:

- I Bonds are the best inflation-protected investment right now. You can buy a bond this week and hold it for 30 years. Although the base rate is zero, the add-on rate will ensure your holding matches the growth in inflation. Compare that with a 5-year TIPS, paying -1.33% to inflation, or a 10-year, paying -0.64%. With a TIPS, you have to go all the way out to 20 years to get positive to inflation, and that’s just 0.04%.

- Federal income taxes are deferred on I Bonds until you sell them, a big advantage over TIPS and bank CDs.

- There are no state taxes on I Bond interest, another advantage over bank CDs.

- I Bonds are completely deflation proof. Your principal grows with inflation, but can never go down with deflation. The worst you can earn is zero percent. This isn’t true of TIPS, where deflation will eat away at accrued principal.

- I Bonds are excellent for retirement savings because you can pick the maturity date. You can space out your maturities to provide steady income.

- The current value of I Bonds is much easier to track than that of TIPS. You just download the Savings Bond Wizard, enter your holdings and update the data every so often.

There are no negatives? Obviously, I am a big fan of I Bonds for their inflation protection. The return is acceptable, better than you will currently receive with 5- or 10-year TIPS. As a long-term holding, they are tax deferred and protected against inflation and deflation.

Because of the I Bond tax advantage, TIPS traditionally paid up to a 1% higher return than I Bonds. Today, that is reversed. In my opinion, this makes I Bonds a ‘gift’ from the federal government. Take the gift.

If, at some point in the future, the I Bond base rate rises above 0.0%, you can sell these 2013 I Bonds and buy the new ones (assuming you have held them more than 1 year).

Well, there is one negative … Each person can only buy $10,000 per calendar year. That means $20,000 for a couple, but you have to create separate accounts at TreasuryDirect. (You can also get paper I Bonds with your tax refund, but I am not a fan of that strategy.)

So, if you haven’t purchased $10,000 in I Bonds this year, take a look at buying before May 1 to lock in that 1.76% for six months.

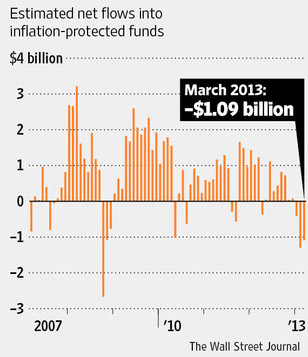

Before we get to rooting for inflation, let’s look at the article’s premise, that investors are suddenly pouring out of TIPS and into stocks, traditional Treasurys or high-yield bonds. This Wall Street Journal chart does show that TIPS mutual funds have been seeing net outflows for the last three months. These outflows have been fairly rare, and we haven’t seen three consecutive months of outflows since the financial crisis of 2008, when TIPS yields skyrocketed upward, and TIPS values plummeted.

Before we get to rooting for inflation, let’s look at the article’s premise, that investors are suddenly pouring out of TIPS and into stocks, traditional Treasurys or high-yield bonds. This Wall Street Journal chart does show that TIPS mutual funds have been seeing net outflows for the last three months. These outflows have been fairly rare, and we haven’t seen three consecutive months of outflows since the financial crisis of 2008, when TIPS yields skyrocketed upward, and TIPS values plummeted.

Thank you Fred Bloggs for this coherent analysis, without undertones of personal agendas... a rarity on the modern www. It…