5-year real yields are declining. What does it mean for TIPS and I Bonds?

By David Enna, Tipswatch.com

April 11, 2025, update: Welcome to the I Bond ‘buying season’

April 10, 2025, update: I Bond’s variable rate will rise to 2.86% on May 1

April 3, 2025, update: My I Bond fixed-rate projection just fell to 1.10%

I’ve just returned from 3+ weeks in very southern South America — much of the time with limited internet access — and gosh, you folks have been busy.

Tariffs on. Tariffs off. Stock market down, up, then down. Treasury yields all over the place. Although I could monitor news some of the time, I am a bit lost about what’s been happening.

During that time away, I had three interview requests from separate Wall Street Journal reporters, plus NPR and Bottom Line. Something was triggering interest. At least twice during the trip, I noticed the 5-year real yield had fallen midday to 1.30%, down from 1.74% when I left on February 10. Things have stabilized a bit, but volatility is obviously a key market factor in March 2025.

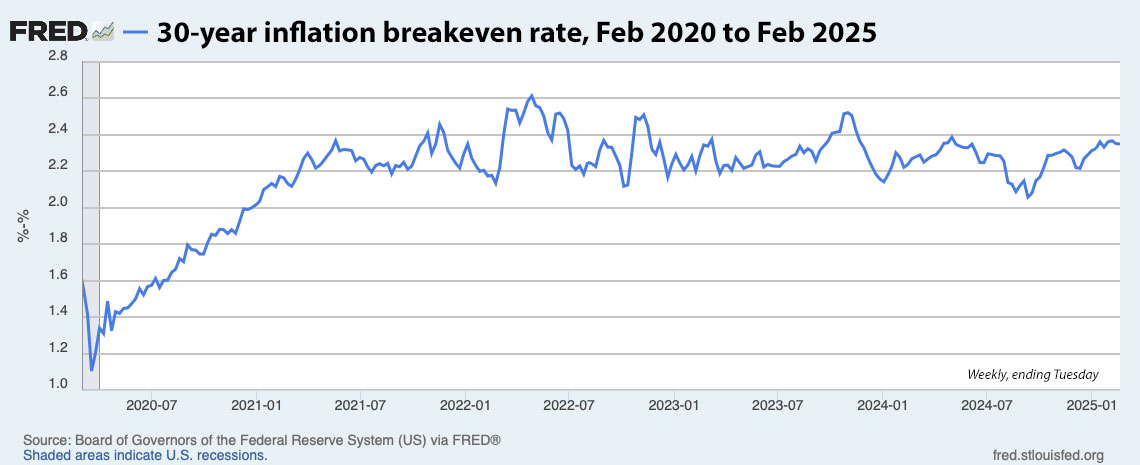

In this brief time, the real yield of a 5-year Treasury Inflation-Protected Security has fallen much farther than the yield of the 10-year TIPS. Note in this one-year chart how the two yields tracked closely until October 2024, and then have widened dramatically:

The gap between the current 5-year real yield (1.57%) and the 10-year (1.99%) has been partially caused by higher inflation expectations over the next 5 years, now at 2.57%, compared with the 10-year inflation expectation at 2.35%. For a long period of 2024, the 10-year inflation breakeven rate was running higher than the 5-year.

Markets are concerned about future inflation, and that increases demand for TIPS, which in turn lowers yields. From a Bloomberg article this week:

But rising inflation is a real possibility now even if many investors are bracing for rate cuts, said Nicolas Trindade, who runs a number of funds at AXA Investment Managers. He expects volatility to increase amid the unpredictable economic strategy.

“The main risk for 2025 is a sharp resurgence in US inflation on the back of tariffs, tax cuts and immigration restrictions that could lead the Fed to open the door to hiking interest rates again,” he said. “The market is definitely not priced for that.”

This comparison of the real yields is important now for several reasons:

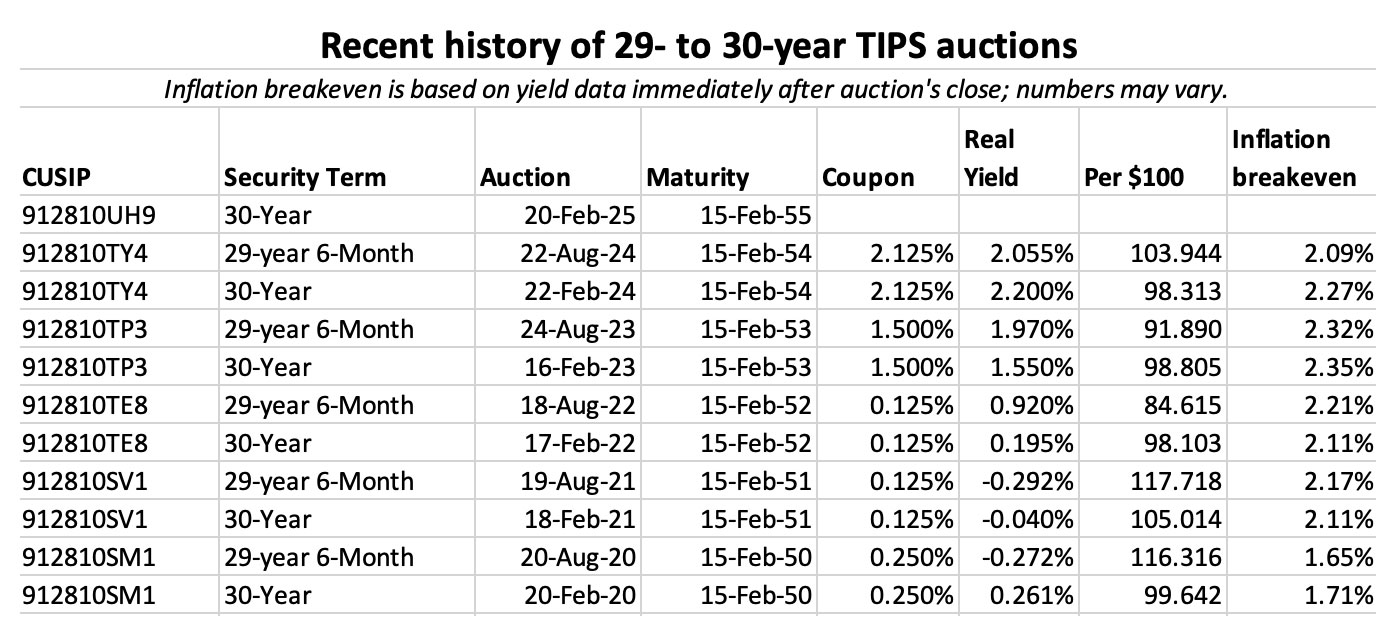

- On March 20, the Treasury will reopen a 10-year TIPS at auction. The real yield at this point would be 1.99%, a decline from 2.243% at the originating auction on Jan. 23. That’s down about 25 basis points.

- Then, on April 17, a new 5-year TIPS will be issued at auction. At this point the real yield looks likely to be about 55 basis points lower than the 2.121% set in the last auction of this term, a reopening on Dec. 19, 2024.

- And two weeks after that auction, the Treasury will reset the I Bond’s fixed interest rate for purchases from May to October 2025. My analysis of data through March 7 indicates the new fixed rate could hold at 1.20%, or potentially drop to 1.10%.

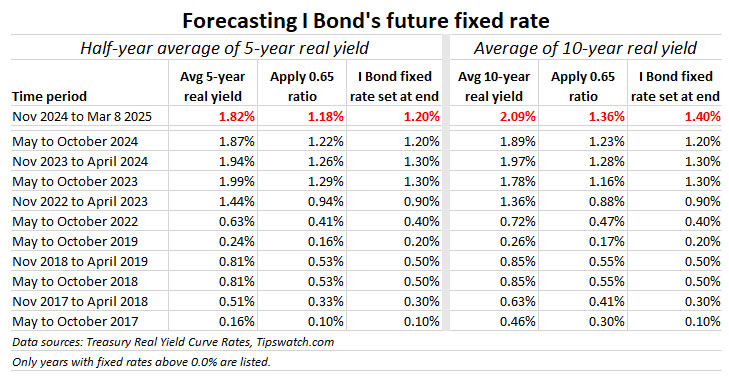

The 5-year real yield is key

The Treasury has never revealed a formula for setting the I Bond’s fixed rate, but it has stated it looks at real yield trends over time. TreasuryDirect has provided this cryptic information:

The Secretary of the Treasury, or the Secretary’s designee, determines the fixed rate. The rate is based on market rates that have been adjusted to account for the value of components unique to savings bonds. These include the early redemption put option, tax deferral feature, deferred purchase feature, and Treasury’s administrative costs.

I Bond watchers have observed that over the last decade one formula has accurately predicted the Treasury’s fixed rate decision: Apply a ratio of 0.65 to the average 5-year real yield over the preceding six months. This formula has worked without fail at least since 2017.

So now I am going to use that formula to look at how recent declining real yields could affect the Treasury’s May 1 decision. Here are the data:

I include the 10-year TIPS data in this chart simply as a back-check, but it is interesting to note that 10-year real yields would point to a higher fixed rate of 1.40%. (The fixed rate is always rounded to the one-tenth decimal.) But … ignore that. The 10-year real yield hasn’t been a reliable indicator of the rate reset.

At this point, as of March 7, 2025, the average real yield of a 5-year TIPS since November 1, 2024, has been 1.82%, much higher than the current rate of 1.57%. Applying a ratio of 0.65 to 1.82% gets you to 1.18%, which rounds to 1.20%, same as the current fixed rate.

So, yes, the fixed rate could hold at 1.20%.

But what if the 5-year real yield stays around this 1.57% level through April, or goes lower? If that happens, the I Bond’s fixed rate is likely to decline to 1.10%, at least. There are 57 market days remaining until late April. If you add in 57 days at 1.57%, the real yield average drops to 1.132%, which would round to 1.10%.

So, yes, the fixed rate could drop to 1.10%.

What we don’t know

The Trump administration could decide to ditch the long-standing formula for setting the I Bond’s fixed rate. That is certainly possible. Remember, there is no set formula required by law. Keep that in mind.

Or, maybe it could eliminate the savings bond program entirely, cutting off all new issues? Highly improbable, I’d say.

Also, real yields have been highly volatile over the last month and may continue to rise and fall unpredictably. We’ll have more certainty by mid-April.

Also read: A great mystery: I Bond buying guide for 2025

Suggested strategy: Wait

Maybe you haven’t noticed, but I Bonds are getting more and more attractive as the 5-year TIPS yield declines. An I Bond can be redeemed after 5 years with no penalty, so it is directly comparable to a 5-year TIPS, but has advantages of tax deferral, better deflation protection and no market fluctuations.

An I Bond with a fixed rate of 1.20% is more attractive than a TIPS with a real yield of 1.30% or 1.40%, in my opinion. So if TIPS yields continue declining, I Bonds with a fixed rate of 1.20% — or even 1.10% — will remain attractive.

My opinion: The best strategy for investing in I Bonds in 2025 is to wait at least until April 10, when the March inflation report will be released. Then you will know for certain what the new variable rate will be (probably higher than the current 1.90%) and have a better idea of the potential fixed-rate reset.

I am thinking an investment near the end of April will make the most sense. There is no harm in waiting. But if the fixed rate looks likely to rise, May would be the better choice. I will have more to say on this topic in mid-April.

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

This is my thinking as well. I wish I had purchased more I-Bonds at the 1.3% fixed rate but even…