By David Enna, Tipswatch.com

First off, let’s point out that the Federal Reserve has not yet lowered interest rates by a single basis point and, in fact, the federal funds rate has been stable since July 2023.

But changes are coming this week, with the Fed likely to cut short-term rates by 25 to 50 basis points, beginning a string of rate-cutting decisions that will likely stretch well into 2025. The market has been repricing longer-term Treasurys in reaction to the potential Fed moves, and in reaction to a gradually weakening U.S. economy.

Real yields (meaning yields above inflation) hit a 2024 high on April 30, with the 10-year yield on a Treasury Inflation-Protected Security topping off at 2.28%. This is the trend since then:

In the middle of that trend, on July 18, the Treasury auctioned a new 10-year TIPS, CUSIP 91282CLE9, with a real yield to maturity of 1.883%. On Thursday this week, it will stage the first reopening auction, creating a 9-year, 10-month TIPS. The auction size is $17 billion, the highest in history for a 10-year reopening.

Obviously, a lot has changed in two months. CUSIP 91282CLE9 trades on the secondary market, and closed Friday with a real yield of 1.57%, 31 basis points below the originating auction.

Is this TIPS still attractive?

It’s definitely less attractive, we have to admit. But getting a real yield above 1.50% is at least historically appealing, or maybe at least “normal.” Here is a chart of 10-year real yields over the last 14 1/2 years:

I pushed this chart back to 2010 to reflect the period just before the Federal Reserve began aggressive quantitative easing in mid 2011. In April 2010 real yields peaked at 1.70% but did not again top 1.50% until November 2018. So based on “recent history” 1.50%+ looks like an attractive real yield.

I filled out my TIPS ladder in the late summer of 2023 with TIPS yielding mostly in the 1.7% to 2.2% range. A few months later, it looked like I acted too early because yields continued climbing into October. But today I can say: “I did all right.”

And that is where investors are today, but in reverse. If you are looking to add to your TIPS holdings, should you act now to lock in 1.57% in fear of falling yields, or wait in the hopes that TIPS real yields will bounce higher in the near future? Tough question.

Pricing

The July originating auction for CUSIP 91282CLE9 set its coupon rate of 1.875%, well above today’s market real yield of 1.57%. So it is currently trading at a premium price of about 102.77. In addition, it will have an inflation index of 1.00237 on the settlement date of Sept. 30. With that information, we can estimate the investment cost of $10,000 par at the current real yield of 1.57% (which will likely change by Thursday’s auction):

- Par value: $10,000.

- Actual principal purchased: $10,000 X 1.00237 = $10,023.70

- Cost of investment: $10,023.70 x 1.0277 = $10,301.36

- + Accrued interest: About $39.32.

In summary, an investor placing a order for $10,000 par at Thursday’s auction will pay about $10,301.36 for $10,023.70 in principal and from that point on will earn accruals on principal matching U.S. inflation plus a coupon rate of 1.875%.

These numbers will change before Thursday’s auction, so this is just an estimate. CUSIP 91282CLE9 trades on the secondary market and could be purchased at any time before the auction, or after, if you see a real yield you like.

Inflation breakeven rate

With the 10-year nominal Treasury note closing Friday at 3.65%, CUSIP 91282CLE9 currently has an inflation breakeven rate of 2.08%, potentially the lowest level at auction since November 2020, in the heart of the pandemic-triggered collapse in yields. A low breakeven rate indicates that a TIPS is “cheap” versus a nominal Treasury of the same term.

Here is the trend in the 10-year inflation breakeven rate over the last 14 1/2 years, which shows the recent decline from levels nearing 3.0% in April 2022 and then 2.4% in April 2024:

Do you think inflation will average more than 2.08% over the next 10 years? If so, this TIPS is attractive versus a nominal 10-year Treasury.

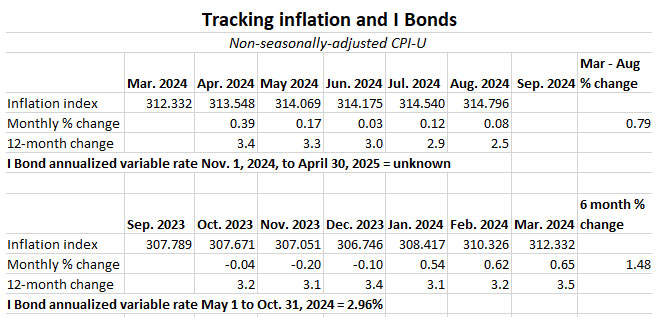

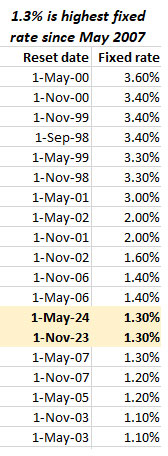

I Bond alternative

As real yields decline, the current U.S. Series I Savings Bond — with a fixed rate of 1.3% above inflation — is looking attractive. At Friday’s close, a 5-year TIPS had a real yield of 1.48%, only an 18-basis-point advantage over the I Bond. That is an extremely low spread. At the last rate reset, on May 1, the spread was 95 basis points.

I Bonds with a fixed rate of 1.3% are going to get more and more attractive if TIPS real yields continue to decline through October. The fixed rate, which is permanent, could decline for I Bonds issued after November 1, but it’s too early to make that call.

Final thoughts

There is no particular reason to buy this TIPS at auction instead of on the secondary market, unless you want to use TreasuryDirect (where the minimum purchase is just $100). You can check Bloomberg’s Current Yields page to track the yield of CUSIP 91282CLE9 in real time.

If the real yield was still in the 1.75% range, I’d be tempted to make a purchase. But I have filled the 2034 rung of my TIPS ladder (real yields of 1.81%, 1.89% and 2.04%) and I am awaiting the Jan. 23, 2025, auction of a new 10-year TIPS to mature in January 2035. Real yields seem likely to be lower by then, but I am going to wait it out.

This TIPS auction closes Thursday at 1 p.m. ET. Non-competitive bids at TreasuryDirect must be placed by noon Thursday. If you are putting an order in through a brokerage, make sure to place your order Wednesday or very early Thursday, because brokers cut off auction orders before the noon deadline.

I plan on posting the results after the auction’s close. Meanwhile, here is a history of recent 9- to 10-year TIPS auctions. Notice that less than three years ago the auctioned real yield was -1.145%, the lowest in history for this term:

—————————-

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I plan on selling some SGOV and buying before the end of the month as well. I had one I…