By David Enna, Tipswatch.com

I am writing this after an evening out in Biella, Italy, and while struggling with rather weak Internet. So this is going to be brief.

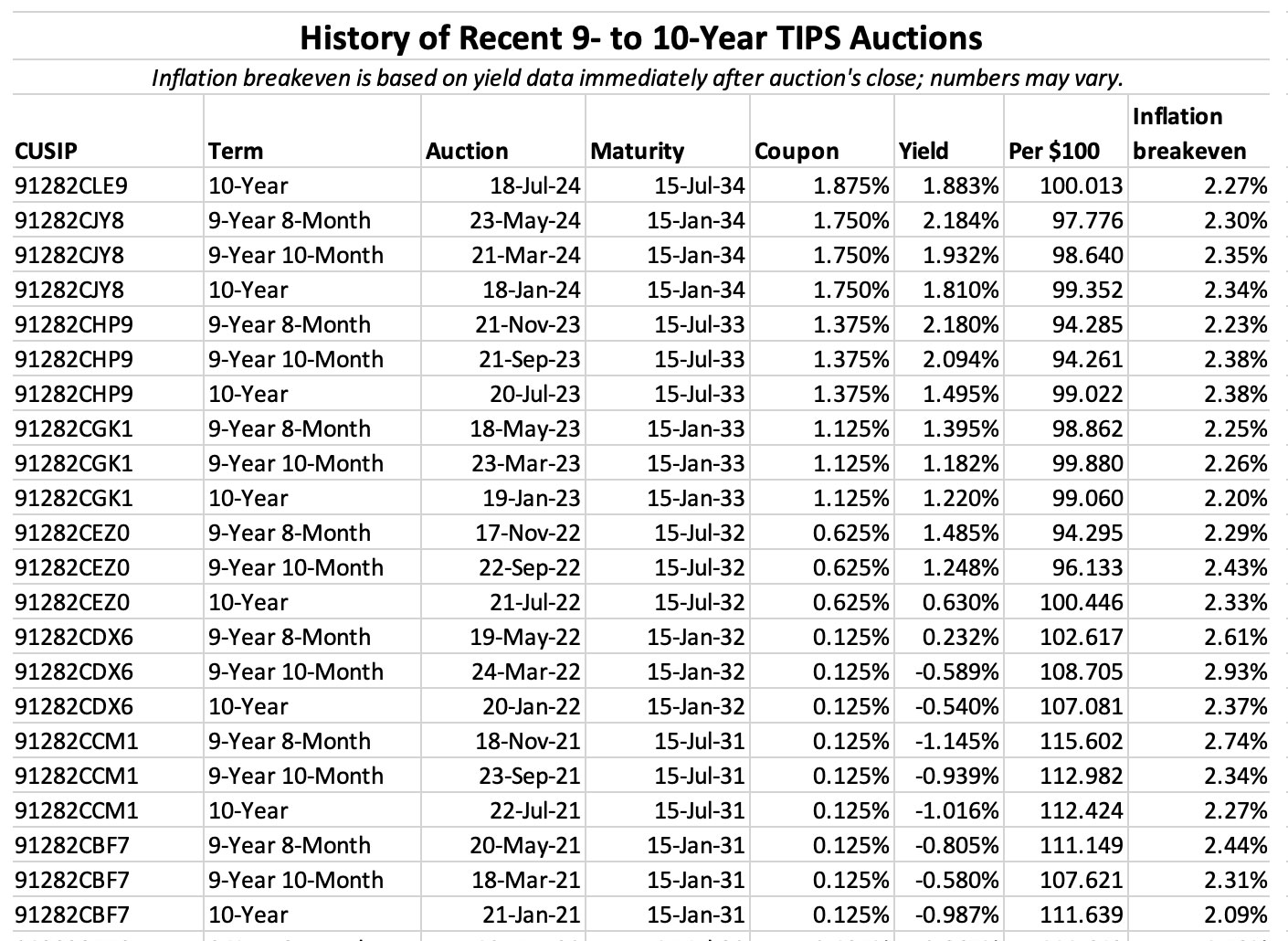

The U.S. Treasury’s auction of $19 billion of a new 10-year Treasury Inflation-Protected Security, CUSIP 91282CLE9, generated a real yield to maturity of 1.883%. The coupon rate was set at 1.875%, the highest for this term since July 2009. That was 88 auctions ago for this term of TIPS.

While the coupon rate set a milestone, the real yield to maturity was below the last two auctions of this term, which hit a multi-year high of 2.184% in a reopening auction on May 23, 2024. That was CUSIP 91282CJY8, which was trading Thursday morning with a real yield to maturity of about 1.91%, a bit higher than this auction result.

The “when issued” prediction for this new TIPS, set just before the auction’s close, was for a real yield of 1.865%. The auction came in a bit higher at 1.883%, which indicates slightly weak demand. The bid-to-cover ratio was 2.38, slightly higher than recent auctions of this term.

So … all things considered … this looks like a routine auction. No surprises.

Pricing

This TIPS will have an inflation index of 1.00086 on the settlement date of July 31. It auctioned at an unadjusted price of 99.926982. Those two factors combine to create an adjusted price of 100.012919.

So an investor purchasing $10,000 par value of this TIPS will be receiving $10,008.60 in principal on the settlement date, at a cost of about $10,001.29, plus about $8.16 of accrued interest, which will be returned at the first coupon payment in January.

This TIPS auctioned at a total cost very close to par value, which is the amount guaranteed to be returned at maturity, even after a severe period of deflation. (That is comforting, but a very, very minor issue.)

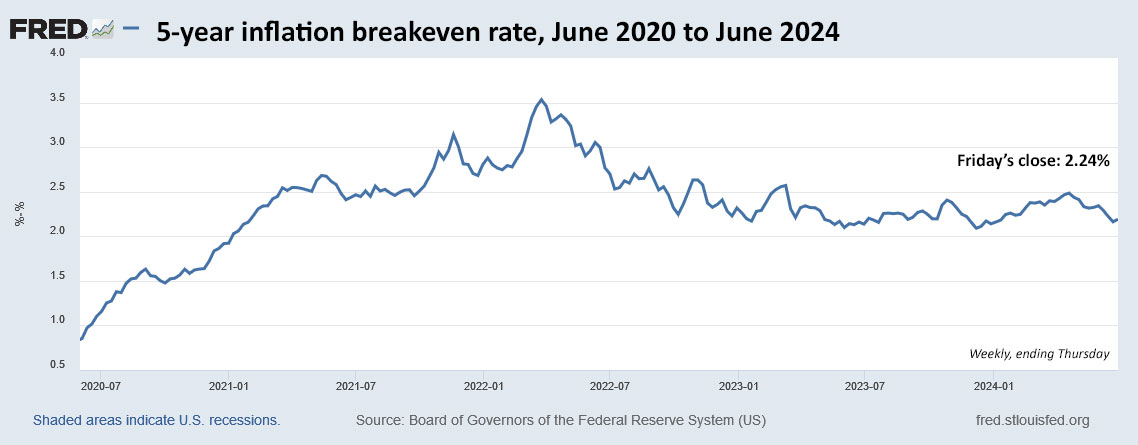

Inflation breakeven rate

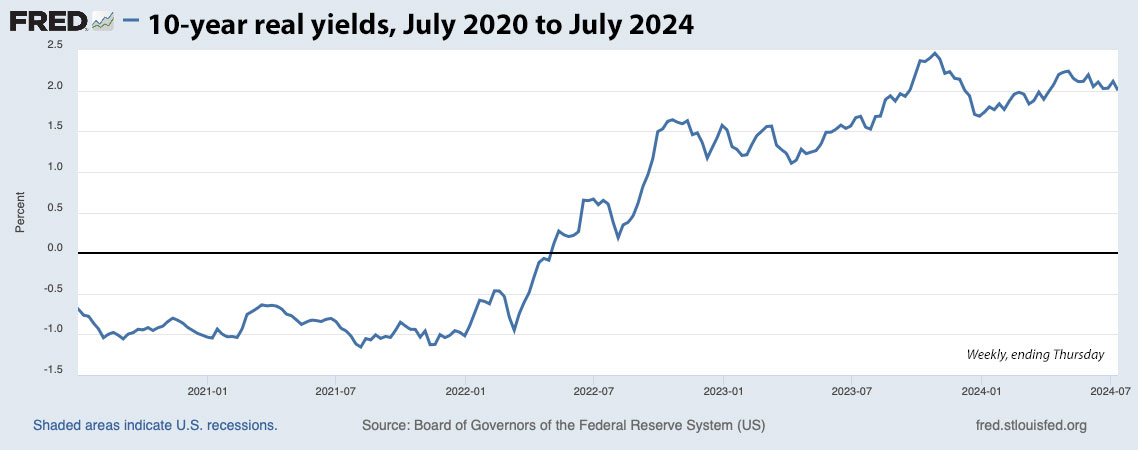

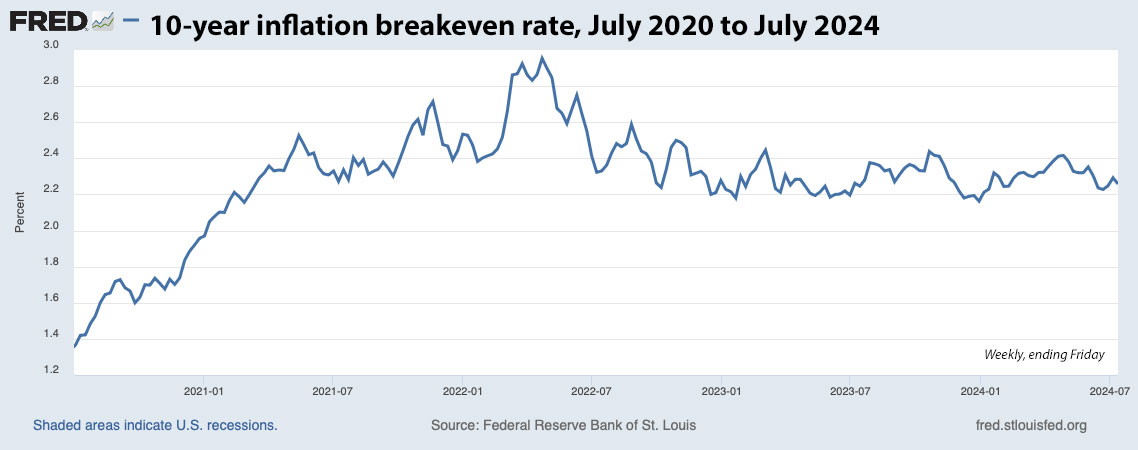

With a 10-year Treasury yielding 4.18% at the auction’s close, CUSIP 91282CLE9 gets an inflation breakeven rate of 2.27%, lower than the last four auctions of this term. This means the new TIPS will out-perform a similar Treasury note if inflation averages more than 2.27% over the next 10 years.

Here is a history of TIPS auctions of this term over the last three years:

—————————-

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

2.5% to 2.7%+ Real yield above inflation on 20 to 30-year TIP bonds.