Julie Andrews in “The Sound of Music.” 1965, 20th Century-Fox. Much of the filming was done around Salzburg, Austria. I just re-watched it. Fantastic.

By David Enna, Tipswatch.com

Here we go again. Yes, I am traveling again for the next three weeks through the European Alps: Switzerland, France, Italy and Austria.

Much of the time I will be in mountain cities or villages, and may not have strong Internet connections. (But this is Europe, so maybe?) I will attempt to keep up with financial news and reading & answering your comments, but no promises. My article updates will be spotty and ill-timed, I expect.

This will be a fairly busy time for news, especially with potential decisions coming on one U.S. presidential candidacy and one vice presidential choice. And it’s a fine time to view simmering political chaos in Europe.

What’s ahead?

Thursday, July 11. The Bureau of Labor Statistics will release the June inflation report at 8:30 a.m. EDT, or 2:30 p.m. CEST in Geneva, which is on Central European Summer Time. This is about the time I will be arriving in Geneva, so this report will be delayed, along with the effects of impending jet lag.

The consensus of economists is for fairly mild monthly inflation for June, with the annual inflation rate falling from the current 3.3% to 3.1%. But core inflation is expected to tick higher, from 3.4% to 3.5%.

The June inflation report is especially interesting because it sets a baseline for the upcoming increase in the Social Security COLA, which is based on the average of July to September readings in the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). I may try to provide a projection of next year’s increase, but that’s a complicated task. It may have to wait until after I return.

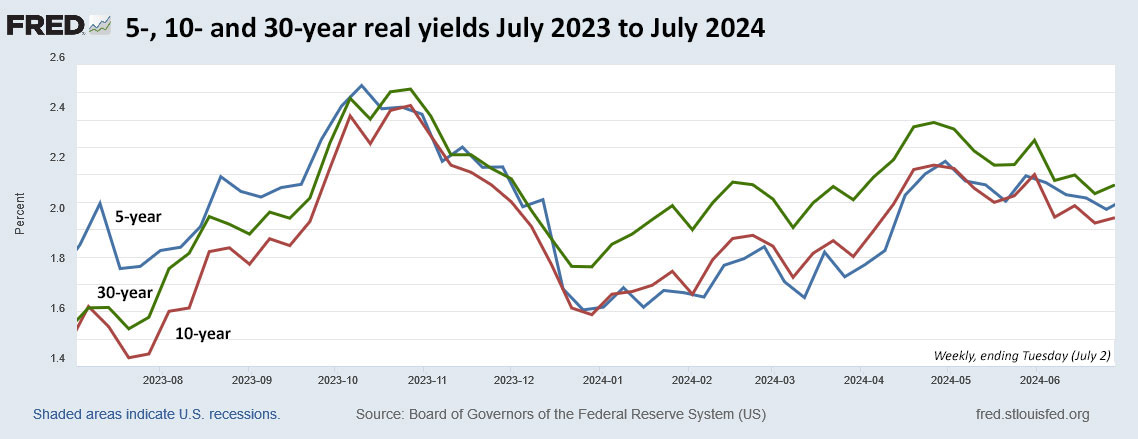

Sunday, July 14. I am planning to post a preview article on the auction of a new 10-year Treasury Inflation-Protected Security, scheduled for Thursday, July 18. Real yields have been quite volatile recently, especially in the aftermath of the June 27 presidential debate. But things have settled down, and real yields have been moving lower. The market closed Friday, July 5, with the 10-year real yield at 2.00%, down 16 basis points for the week.

Thursday, July 18. The 10-year TIPS auction closes at 6 p.m. CEST in Biella, Italy, where I will be on that date. There is a good chance my schedule will be complicated at that hour, so I will post the auction results when I can.

Sunday, July 21. I will post a TIPS vs. Nominals article on the 10-year TIPS that is maturing on July 15. This TIPS, which I own, has continued the streak of TIPS out-performance.

At this point, that is all I can see, but something always comes up when I am on vacation.

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Any long-time reader of this site knows I try very hard to avoid political discussions and I discourage political rants in the comments section. This is a site about inflation protection and investing with a focus on safety.

Thursday night’s presidential debate was difficult to watch, no matter your political persuasion. Did we get actual policy discussions? No. The solvency of the Social Security system was raised by the moderators, but we got in essence, nothing of substance from the two debaters.

But I was interested to see a report Friday from Bloomberg that combined inflation and inflation protection into the debate analysis. This was the headline, and you can read the article free on Yahoo! Finance: “Barclays Says Buy Inflation Protection to Prepare for Trump Win.”

It is based on a research report from Barclays Plc. From the Bloomberg report:

With former president Donald Trump appearing more likely to unseat Joe Biden in the Nov. 5 election, the market should “be pricing in a considerable risk of higher-than-target inflation in the coming years, and this is from a starting point of our thinking they already offered structural value,” Barclays strategists Michael Pond and Jonathan Hill said in a note.

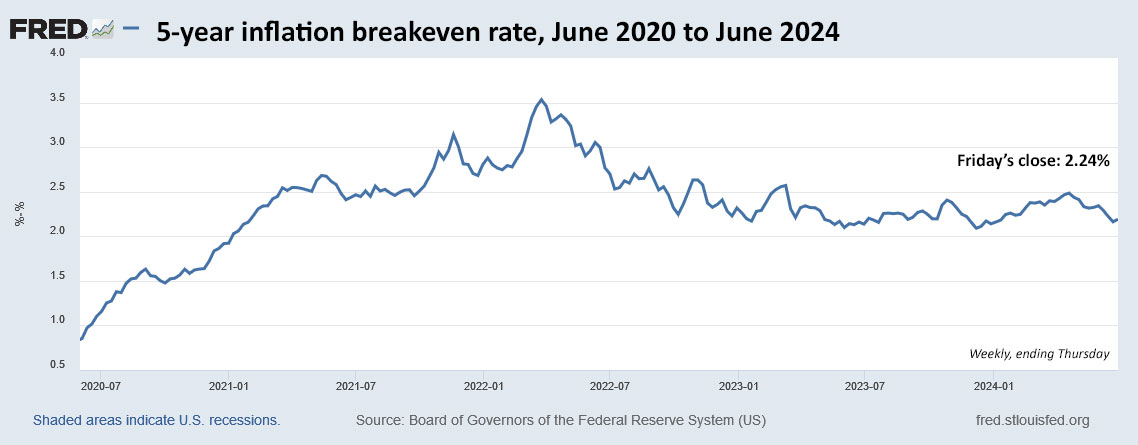

The simple trade, they wrote, is a wager that five-year Treasury inflation-protected securities, or TIPS, will outperform regular five-year Treasuries, leading to a wider yield spread between the two. That breakeven rate — representing the market-implied expectation for the average inflation rate of the consumer price index over the life of the securities — will widen to 2.5% from about 2.25% currently, Barclays projects.

Click on image for larger version.

The reasoning

The authors point to former President Trump’s proposed 10% tariffs on all imports, and likely even higher tariffs for imports from China. In addition, his plan for an aggressive effort to deport illegal immigrants could trigger labor shortages and wage inflation. He has also proposed across-the-board tax cuts, which would add to the U.S. deficit and potentially stimulate consumer spending.

(I)f the odds in the coming months continue to favor a second Trump term, “we would expect them to be embedded in the market via higher breakevens as the November elections approach,” Pond and Hill wrote.

A similar analysis was recently laid out in a letter published by 16 prominent economists, all Nobel Prize winners. They wrote, “The outcome of this election will have economic repercussions for years, and possibly decades, to come.” You can read that here.

You can read a detailed analysis of import tariffs imposed by Trump and continued by Biden in this report from TaxFoundation.org. From that report:

As of March 2024, the trade war tariffs have generated more than $233 billion of higher taxes collected for the US government from US consumers. Of that total, $89 billion, or about 38 percent, was collected during the Trump administration, while the remaining $144 billion, or about 62 percent, has been collected during the Biden administration.

Along the same lines, noted bond investor Bill Gross recently told the Financial Times that he believes a Trump victory would be “more bearish” and “disruptive” for the bond markets than the re-election of Biden.

“Trump is the more bearish of the candidates simply because his programs advocate continued tax cuts and more expensive things,” Gross said, although he noted that Biden’s presidency had also been responsible for trillions of dollars of deficit spending.

My analysis

I have been saying for several months that inflation breakeven rates seem overly optimistic, making an investment in a Treasury Inflation-Protected Security (current 5-year real yield of 2.09%) more attractive than its matching nominal Treasury (4.33%). And history is on my side. Inflation over the last 5 years, ending in May, has averaged 4.2%. And that is why we have seen a string of favorable returns from 5-year TIPS over the last several years:

I would add the possibility of Republicans controlling both houses of Congress and the presidency, which could — ironically — tamp down GOP efforts to control the federal deficit. Having a divided Congress can help control government spending and at least force compromises on policy.

In addition, Trump would likely name a new chairman of the Federal Reserve, potentially with a much more investor-friendly policy. In his first term, Trump consistently pushed the Fed to lower interest rates, and that would likely continue.

Both Trump ($2.2 trillion stimulus package) and Biden ($1.9 trillion) deserve blame for the recent surge to a 40-year high in U.S. inflation, along with Congress for approving massive deficits and the Federal Reserve for keeping interest rates too low for too long and then failing to end bond-buying quantitative easing.

The fact is, I believe that no matter which candidate is elected, we will see higher-than-expected inflation over the next four years.

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Comments on this article are now closed.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Just about every week, I get a comment or question from readers worried about the dangers of buying a Treasury Inflation-Protected Security on the secondary market with a high (or even not-so-high) inflation index.

Why is that a potential problem? Because TIPS come with a deflation-fighting guarantee: At maturity, you cannot receive less than par value, even if the nation goes through a prolonged period of deflation. Buying a TIPS with a high inflation index means part of your investment is not guaranteed to be returned at maturity.

Here is what I think: It’s possible a period of low or negative inflation could mean your TIPS investments are going to under-perform nominal Treasurys. But, under most circumstances, you are highly unlikely to lose money on that investment if held to maturity.

Some things to consider:

It has never happened. TIPS have been issued since 1997 in 5-, 10-, 20- and 30-year maturities (the 20-year was discontinued in 2009). Over that time, no TIPS has matured with an inflation index of less than 1.000, meaning par value. So the “deflation guarantee” has never been triggered for a TIPS purchased at auction.

Inflation is the norm. Since 1971, the lowest average annual inflation for any 5-year period was 1.4%, for the 5 years ending in both 2017 and 2018. For 10-year periods, the lowest was 1.6%, for the years ending in 2017. For a 30-year period, the lowest was 2.2%, for the years ending in 2020.

So if you are buying a TIPS on the secondary market with a high inflation index and 5 years remaining to maturity, you can be fairly confident you won’t be struck by a 5 year period of deflation, eating away at your original investment.

The deflation risk is more pronounced if you buy a TIPS with a very short period (meaning months) remaining to maturity. The longer the term, the lower the potential risk.

Long-term deflation is rare. The United States has not recorded a single year of December-to-December deflation in 70 years. The last deflationary year was 1954, when prices declined by 0.7%. The lowest since then was 2008, when inflation increased 0.1.%

In this chart, I have recorded 1) at the top, deflationary years going back to 1929 along with corresponding Gross Domestic Product changes in each of those years, and 2) at the bottom, the years with positive inflation but negative GDP rates.

The most devastating period of deflation came in the Great Depression years of 1930 to 1933, when prices fell a cumulative 24% from January 1930 to December 1933. That decline was matched by a similar drop in GDP.

But since 1954, inflation continued to increase even when GDP growth was negative, resulting in some classic years of stagflation in 1974, 1975 and 1980. Since the 1980s, the Federal Reserve has taken a greater role in trying to tamp down recessions, possibly easing the effects of economic downturns and holding inflation higher.

In the Great Recession years of late 2007 to mid 2009, inflation continued climbing: rising 0.1% in 2008 and 2.7% in 2009, despite negative GDP growth in 2009.

And in the brief COVID recession of 2020, inflation still managed to climb 1.4% even as the economy faltered. The next year, in 2021, annual inflation rose to 7.0%.

Short-term deflation is a risk

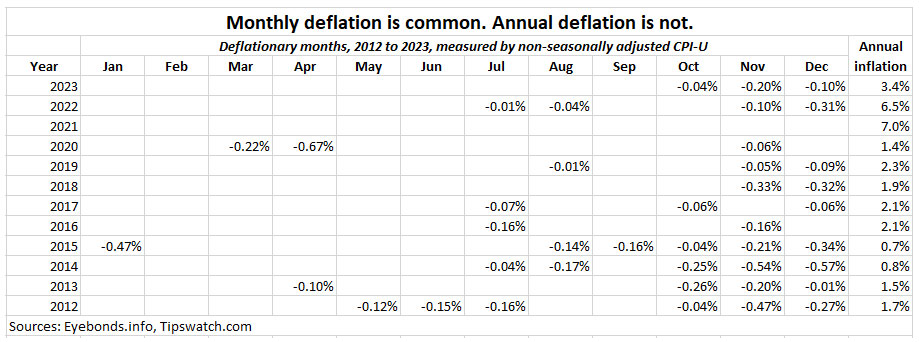

As I noted, the shorter the time to maturity, the more a TIPS is at risk of deflation because TIPS inflation accruals are based on non-seasonally adjusted inflation, which often dips into deflation in the later months of the year.

This chart shows month-over-month declines in non-seasonally adjusted inflation, going back to 2012. Note that minor deflation is common in nearly every November and December, and is fairly common in July, August and October. But also note that the annual inflation rate for every year is positive, overcoming the late-year swoons.

Click on image for larger version.

So if you are looking to buy a TIPS maturing in April 2025, with just a few months remaining, realize that the TIPS is likely to be hit by deflation in at least two or three of the remaining months. Its final inflation index will be set by inflation in February 2025.

The market knows what’s likely ahead for the April 2025 TIPS, and its real yield is currently higher (3.576%) than that of a similar 5-year TIPS that will mature in October 2025 (2.739%). In other words, deflation presents more of a risk for the April TIPS than it does for the October TIPS, and the market has adjusted prices to reflect that.

Is the October 2025 TIPS (with an inflation index of 1.207) safer than the April 2025 TIPS (inflation index of 1.212). Who knows? Because both are short-term investments, they both have some deflation risk. The April issue has a bit more risk and is priced accordingly. More on this here.

I Bonds have an advantage

U.S. Series I Savings Bonds pay out a composite interest rate based on a permanent fixed rate (currently 1.3%) and a six-month variable rate (currently 2.96%). No matter what happens with the variable rate, the I Bond’s composite rate can never go below 0.0% and the principal can never decline. So I Bonds have rock-solid protection against deflation.

In addition, while TIPS lose principal during spells of deflation, the I Bond never loses value. When inflation starts rising again, the TIPS has to make up lost ground. The I Bond starts increasing from where it left off, a nice advantage over TIPS.

But, on the flip side, the I Bond’s fixed rate of 1.3% (equivalent to its real yield) is well below the 2.0%+ real yields currently found on all TIPS maturities.

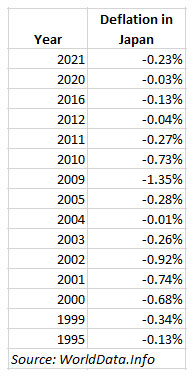

Worst case scenario: Japan

I can’t claim to understand anything about Japan’s complex economy, but I know that both inflation and interest rates have been very low for more than two decades in that country. This is from the World Economic Forum:

Between 1960 and the late 1980s, Japan’s economic growth was double that of the US. But in 1989, there was a stock market crash and a banking crisis in Japan. Inflation in Japan has remained low ever since, and turned into deflation in the 2000s, and again during the pandemic.

After two decades of extremely accommodative monetary policy, Japan is now moving to bring interest rates out of the ultra-low (or negative) range. Annual inflation rose to 2.8% in May 2024, considered a positive trend.

In Japan, rising inflation is considered a positive, which isn’t true in the United States. It’s hard to say if this is an omen for the U.S., or just a singular problem for Japan.

Final thoughts

If you want to build a ladder of TIPS stretching out 20 to 30 years, you are going to have to accept buying additional principal that is not protected against deflation. The TIPS maturing in February 2040 has an inflation index of 1.448, meaning the investor will be buying about 45% of additional principal. Is that actually risky? Sure, there is a very slight possibility of deflation striking across the next 16 years. But not enough to worry about, in my opinion.

If you have been holding any long-term TIPS for many years, they all have inflation accruals that aren’t protected against deflation. I could be wrong, but I don’t think the deflation risk is high enough to abandon these investments.

For example, I own CUSIP 912810FH6 in a taxable account at TreasuryDirect, a long-ago 30-year TIPS purchase that will mature April 15, 2029. It has a coupon rate of 3.875% and an inflation index of 1.90508, meaning it has accrued principal 90.5% above par value.

Do I lose sleep at night worrying about deflation eating away at my principal? No. This TIPS is a great asset. (But today, if I were looking on the secondary market for a TIPS maturing in April 2029, I would not buy this one. I’d prefer the April 2029 TIPS that just had a reopening auction with a much lower inflation index.)

Accepting some deflation risk is part of investing in TIPS. That risk, as I have noted, is fairly minor in most scenarios.

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

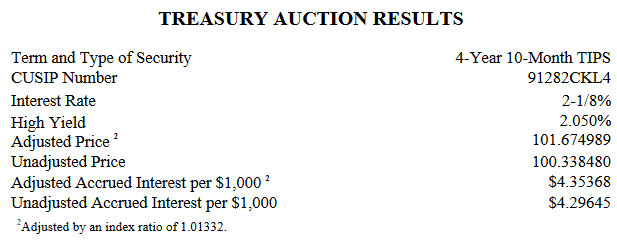

The Treasury’s offering of $21 billion in a reopened 5-year Treasury Inflation-Protected Security — CUSIP 91282CKL4 — generated a real yield to maturity of 2.050%, slightly lower than expected.

The auction appears to have been met with decent demand. The “when-issued” prediction used by bond traders was set at 2.070% right before the auction’s close. In addition, the bid-to-cover ratio of 2.52 was in the solid range.

The yield came in below the April 18 originating auction‘s real yield of 2.242%, which set the coupon rate for this TIPS at 2.125%. However, this was only the third TIPS auction of this term to get a real yield higher than 2.0% since October 2008. There have been 50 auctions of 4- to 5-year TIPS since October 2008, so today’s result is significant.

This TIPS trades on the secondary market and earlier Thursday morning it was trading with a real yield of 2.08%. The auction result of 2.050% indicates demand was strong. Apparently, inflation protection still has some appeal.

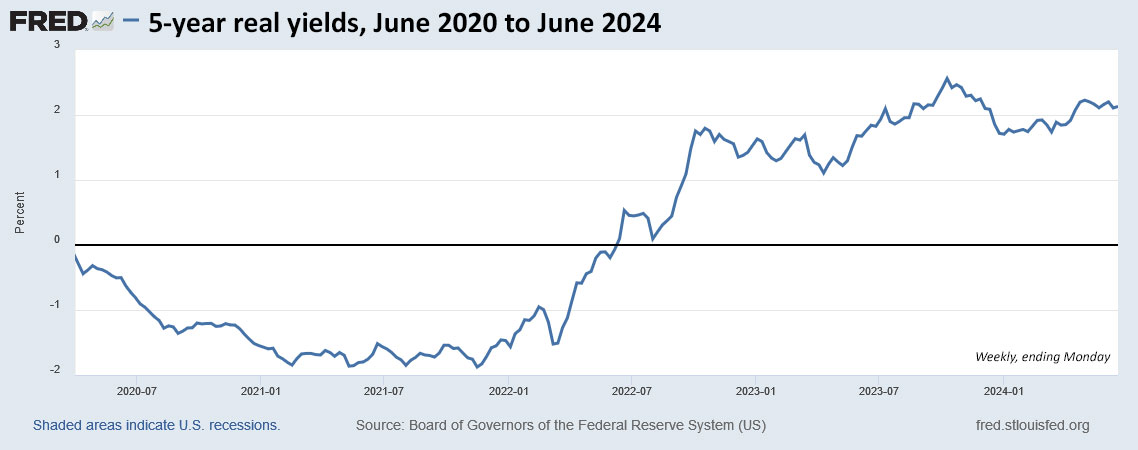

Here is the trend in the 5-year real yield over the last four years:

Click on image for larger version

Pricing

Because the real yield came in below the existing coupon rate of 2.125%, today’s investors had to pay a small premium at this auction. The unadjusted price was 100.338480. In addition, CUSIP 91282CKL4 will have an inflation index of 1.01332 on the settlement date of June 28.

This is how the pricing works out for a $10,000 par investment at today’s auction:

Par value: $10,000

Principal on settlement date: $10,000 x 1.01332 = $10,133.20

Cost of investment: $10,133.20 x 1.00338480 = $10,167.50

+ $43.54 of accrued interest, which will be returned at the first coupon payment.

In summary, an investor purchasing $10,000 par at this auction paid $10,167.50 for $10,133.20 of principal, and will now receive accruals matching inflation plus a coupon rate of 2.125% until maturity on April 15, 2029.

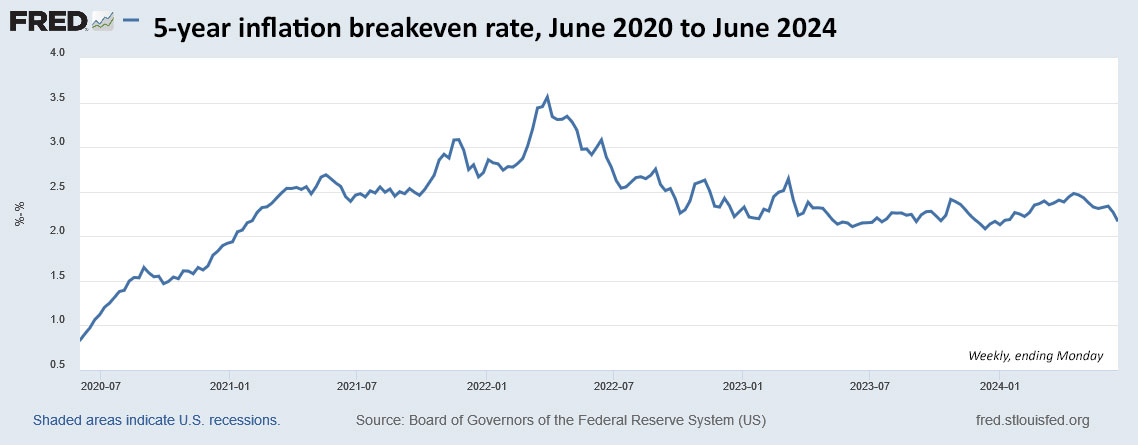

Inflation breakeven rate

In my preview article for this auction, I noted that the market was setting a 5-year inflation breakeven rate of 2.12%, which seems low given current inflation trends. But this auction narrowed the gap, a bit. With a 5-year nominal Treasury trading at 4.28% at the auction’s close, this TIPS gets an inflation breakeven rate of 2.23%.

That means it will outperform the nominal Treasury if inflation averages more than 2.23% over the next 4 years, 10 months. Seems like a reasonable bet.

Here is the trend in the 5-year inflation breakeven rate in the last four years:

Click on image for larger version.

Thoughts

There was nothing really out-of-the ordinary about this auction. The 5-year real yield closed Tuesday at 2.07%, pretty close to the result. A real yield of more than 2.0% is a solid investment, in my opinion. If you were a buyer, this looks good.

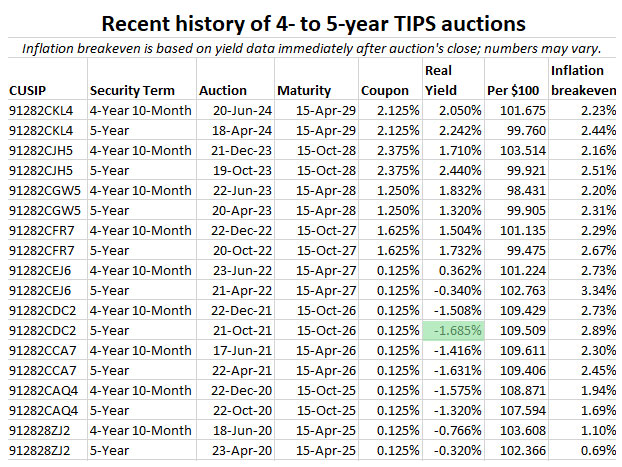

How good? Here is a history of TIPS auctions of this 4- to 5-year term, highlighting the lowest real yield in history, -1.685%, in an auction in October 2021. Since then, in less than three years, real yields have risen 373 basis points.

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Do you believe inflation will average more than 2.12% over the next 5 years?

By David Enna, Tipswatch.com

The U.S. Treasury on Thursday will offer $21 billion in a reopened 5-year Treasury Inflation-Protected Security, CUSIP 91282CKL4.

The result will be a 4-year, 10-month TIPS with a coupon rate of 2.125%, which was set by the originating auction on April 18, 2024. The auction size of $21 billion is the largest for any 5-year TIPS reopening in history, up from $20 billion in December 2023 and $19 billion a year ago in June 2023.

I was a buyer at that originating auction, which generated a real yield to maturity of 2.242%, the 2nd highest at auction in 15 years for any 4- to 5-year TIPS. As of Friday, CUSIP 91282CKL4 was trading on the secondary market with a slightly lower real yield of 2.12%.

What makes this auction interesting is the sudden shakeup of both real and nominal yields, triggered by a soft inflation report released Wednesday. That report caused speculation the Federal Reserve would cut interest rates several times in 2024, but then the Fed tamped down the euphoria with a prediction of “one … or maybe two” rate cuts this year, depending on the data it sees. This set off a shakeup in bond yields:

Nominal. On Monday, the 5-year nominal Treasury note closed with a yield of 4.48%, which fell to 4.22% by Friday, a drop of 20 basis points.

Real. The 5-year TIPS real yield closed Monday at 2.21% and fell to 2.11% at Friday’s close, a drop of only 10 basis points.

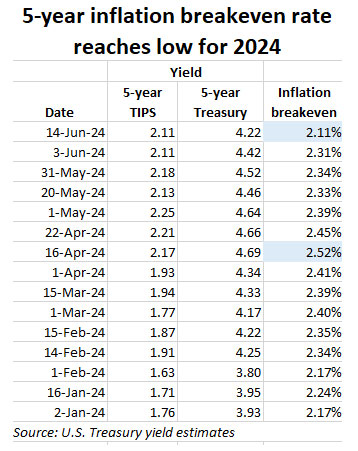

The difference means the 5-year inflation breakeven rate — a measure of future inflation expectations — fell by 10 basis points in a week. And in fact, the breakeven rate of 2.11% hit a low for 2024. I heard a commentator on Bloomberg this week mention the “collapse in breakevens” as a significant event. I wrote about this wild yield trend back on June 9: Read that here.

A lower inflation breakeven rate indicates a TIPS is “cheaper” as an investment versus the nominal Treasury of the same term. Here is the trend in the 5-year inflation breakeven rate so far in 2024:

Rate estimates are for full-term TIPS.

In just two months, expectations for inflation over the next five years have fallen 41 basis points. That is a remarkable move lower, and potentially makes the 5-year TIPS an attractive investment when measured against a nominal Treasury.

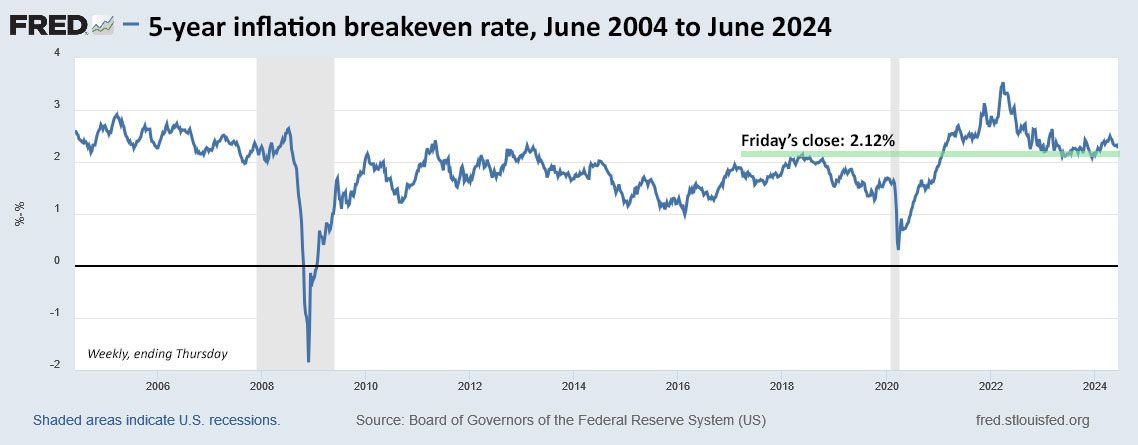

Here is a 20-year look at the 5-year inflation breakeven rate, showing that 2.12% is in a historically high range, but well below recent trends. In my opinion, the risk of under-performance for this 5-year TIPS (versus a nominal Treasury) is small.

The real yield

CUSIP 91282CKL4 trades on the secondary market, and you can track its real yield on Bloomberg’s Current Yields page, which updates in real time. It closed Friday at 2.12%, just slightly below the coupon rate of 2.125%. Here is the trend in 5-year real yields over the last 20 years:

A lot can change this week, especially with the high volatility we’ve seen in the last month. Just based on reasonable inflation expectations, it seems like the yield should be more in the range of 1.95% to 2.00%. That’s not a prediction, just an observation.

Pricing

Bloomberg shows a price very close to par value, 100.02, given that the current real yield is close to the coupon rate of 2.125%. This TIPS will have an inflation index of 1.01332 on the settlement date of June 28. So that leads to this estimate of the potential cost of $10,000 par at auction:

Par value: $10,000

Principal purchased: $10,000 x 1.01332 = $10,133.20

Cost of investment = $10,133.20 x 1.0002 = $10,135,23

+ about $43.54 of accrued interest.

This calculation is an estimate and is highly likely to change in the next week.

Thoughts

It will be interesting to see if the real yield of this TIPS holds above 2.0% over the next week. It could be that bond-market turmoil left real yields a bit out of sorts on Friday. Or … investors really have decided that inflation could average less than 2.12% over the next 4 years, 10 months. If yields hold, this TIPS is attractive versus the nominal Treasury.

Last week, you could find best-in-nation 5-year bank CDs yielding 4.50%, which moves the inflation breakeven rate up to 2.38%, a more reasonable number. But we could see those bank CD rates fall if the downward Treasury yield trend continues.

I won’t be a buyer because I already own this TIPS and the 2029 rung of my TIPS ladder is fully stocked. If you are considering a purchase, watch Bloomberg’s Current Yields page during the week. The 5-year quote there is for CUSIP 91282CKL4. (And of course you can buy this TIPS at any time on the secondary market.)

This TIPS auction closes Thursday at 1 p.m. EDT. Non-competitive bids at TreasuryDirect must be placed by noon Thursday. If you are putting an order in through a brokerage, make sure to place your order Wednesday or very early Thursday, because brokers cut off auction orders before the noon deadline.

I will be posting the auction results soon after the close on Thursday. Here is a history of auction results for this term over the last 7 years:

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

It definitely caused at least a small reduction in six-month inflation. What's amazing is if the United States didn't attack…