Both all-items and core inflation came in below expectations.

By David Enna, Tipswatch.com

The Federal Reserve, which is set to provide future rate predictions this afternoon, got a bit of good news this morning from the May inflation report. Inflation came in below expectations, across the board.

The Consumer Price Index for All Urban Consumers was unchanged in May on a seasonally adjusted basis, the U.S. Bureau of Labor Statistics reported. Over the last 12 months, the all-items index increased 3.3%. Both of these numbers came in lower than the expectations for 0.1% monthly and 3.4% annual.

Core inflation, which removes food and energy, also fell below expectations, rising 0.2% for the month and 3.4% year-over-year. Annual core inflation, while still too high, has now fallen from 5.3% in May 2023 to 3.4% in May 2024, a very encouraging trend.

The BLS pointed to two key factors in the May report: Gasoline prices fell 3.6% for the month and are now up 2.2% year-over-year. That was offset by a continuing increase in shelter costs, up 0.4% for the month and 5.4% year-over-year. More data from the report:

- The costs of food at home were unchanged in May and are up only 1.0% for the year.

- The medical care index rose 0.5% in May after rising 0.4% in April.

- Costs of prescription drugs rose 2.1% for the month.

- Airline fares fell 3.6% in May and are down 5.9% for the year.

- Costs for used cars and trucks rose 0.6% but are down 9.3% year over year.

- Costs for new vehicles fell 0.5% and are down 0.8% for the year.

- Apparel costs fell 0.3% for the month.

- Costs of motor vehicle insurance fell a meager 0.1% for the month, but are up 20.3% for the year.

Here is the one-year trend for annual all-items and core inflation, showing how core inflation has finally begun falling from levels near 4.0%:

What this means for TIPS and I Bonds

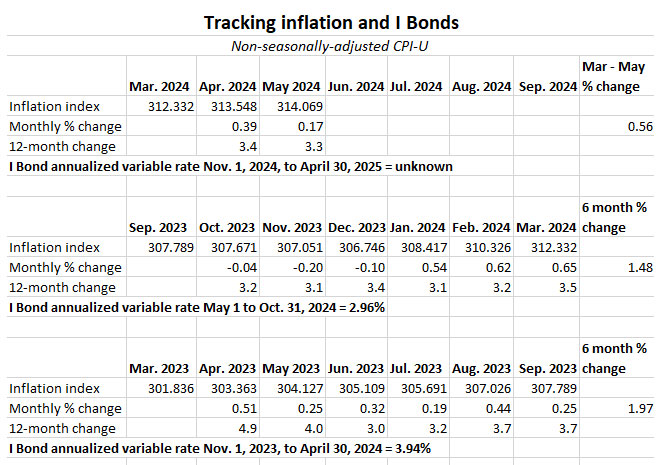

Investors in Treasury Inflation-Protected Securities and U.S. Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances on TIPS and set future interest rates for I Bonds. For May, the BLS set the inflation index at 314.069, an increase of 0.17% over the April number.

For TIPS. The May CPI index will reset principal balances for all TIPS higher by 0.17% in July, after rising 0.39% in June. Keep in mind that non-seasonal inflation tends to run higher than headline CPI from January to June, and then lower at the end of the year. Eventually, over a year, the numbers balance out.

Here are the new July Inflation Indexes for all TIPS.

For I Bonds. The May report is the second in a six-month string that will set the I Bond’s new inflation-adjusted variable rate, which will be reset on November 1 and eventually roll into effect for all I Bonds. At this point, after two months, inflation has increased 0.56%. It is too early to draw any conclusions, but note that in 2023 March to May inflation increased 0.76%.

Here are the relevant data:

What this means for future interest rates

Obviously, the Federal Reserve can breathe a sigh of relief, with inflation coming in below market expectations and annual core inflation falling 20 basis points. This is good news in the battle against U.S. inflation.

Does this mean we will get a rate cut this afternoon? That is highly unlikely, but here is Bloomberg’s headline this morning: “US CPI Report Opens Door to Multiple 2024 Fed Rate Cuts“. Selected quotes from the article:

The good news on inflation extended to the so-called “supercore” measure of core services less housing. On a monthly basis, the measure was negative (-0.04%) for the first time since late 2021.

The expectation at this point in markets will be that the Fed later today projects two rate cuts for 2024. If we only get one, that could see a negative reaction in Treasuries and stocks.

“A 0.2% monthly core CPI reading should be the base case for the balance of the year, especially as it looks more and more like the long-awaited slowdown in shelter costs will hit as soon as the next report.” (quote from Omair Sharif of Inflation Insights)

We are seeing an immediate effect on the markets, with the S&P 500 trading up about 1% this morning in the premarket, just minutes from the opening. Real yields have taken a sharp dip lower, with the 5-year falling from 2.16% at yesterday’s close to 2.08% this morning. The 10-year is at 2.05%, down from yesterday’s 2.12%.

Of course, we have seen a lot of head-fakes on U.S. inflation over the last four years. This time, the trend does look positive, but the Fed knows the battle must continue. Expect rate cuts to come at a measured, cautious pace.

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

It definitely caused at least a small reduction in six-month inflation. What's amazing is if the United States didn't attack…