The 2011 crisis led to an S&P downgrade of U.S. debt. This year could be worse.

By David Enna, Tipswatch.com

When I launched this website back in April 2011, I figured I had chosen one of the most placid and unexciting corners of the investing world: inflation-protected investments. Boring. Staid.

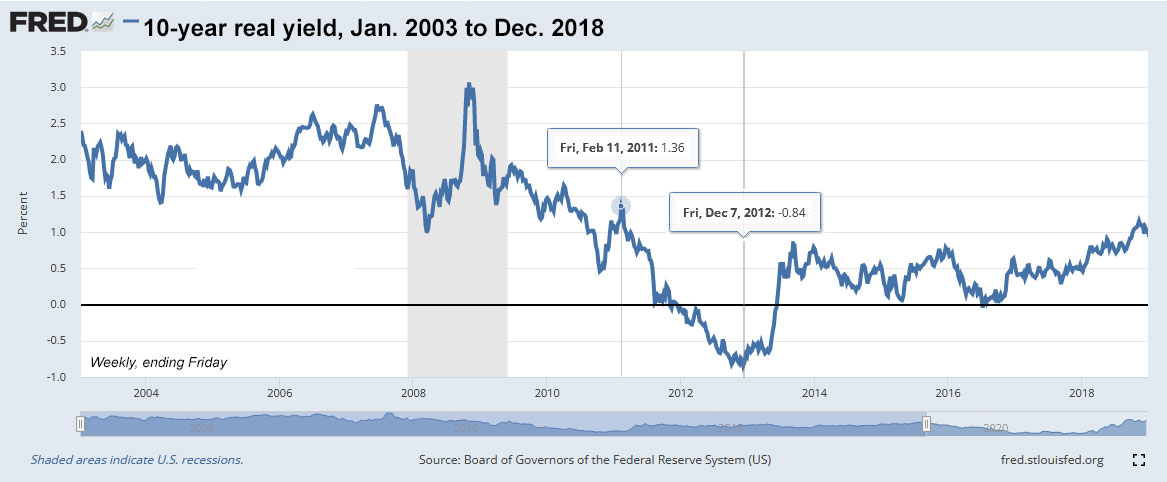

In the days leading up to my first post — on April 10, 2011 — real yields on a 5-year TIPS had started to slip below zero. That was a milestone, and a bit of a shock. But the 10-year TIPS was still yielding a solid 0.96% above inflation.

All of that was about to change. By the end of 2011, the 5-year real yield had plummeted to -0.76% and the 10-year also broke into the negative, at -0.07%. This chart shows the amazing drop in TIPS yields over the course of 2011 and through the entire year of 2012:

In the middle of 2011, something shifted, but why?

Debt-limit crisis of 2011: A monumental event

Back in late 2011, I was quick to blame Federal Reserve manipulation of the Treasury market for the pathetically low yields on TIPS. One of the episodes of quantitative easing had to be behind this sudden shift, right? Wrong.

- QE1 began in November 2008

- A second phase of QE1 began in March 2009

- QE2 began in November 2010

So in the years leading up to 2011-2012, real yields were declining but gradually. Something else happened exactly in late July to early August 2011: A crisis over increasing the U.S. government’s debt limit, the exact crisis we are rolling toward in 2023. A government in crisis; Congressional negotiations heading nowhere. Here are some headlines from that time, which we could see repeated this summer:

- July 22: Obama again presses GOP to move on taxes in debt deal

- July 24: Debt-ceiling standoff grinds on

- July 25: Obama says debt deal must include revenues

- July 26: GOP leaders seek to build support for Boehner debt plan

- July 27: An ‘altar call’ as Boehner pushes GOP for votes

- July 28: House delays vote on Boehner debt plan

- July 29: Obama blasts Boehner debt-ceiling bill, calls for bipartisan deal

- July 29: Amid crisis, TIP ETF hits an all-time high

- July 31: Parties agree to debt-ceiling deal, pending votes in Congress

- Aug. 1: U.S. leaders strike debt deal to avoid default

- Aug. 6: S&P downgrades U.S. credit rating

Yes, on Aug. 6, 2011, for the first time in history, Standard and Poors lowered its rating on U.S. debt from AAA to AA+, with a negative outlook.

Market reaction

Global stock markets declined on August 8, 2011, following the S&P announcement. All three major U.S. stock indexes declined 5% to 7% percent in one day. However, U.S. Treasurys, which had been the subject of the downgrade, actually rose in price and the dollar gained in value. The flight to safety was on.

This chart compares the performance of the TIP ETF, the long-term Treasury ETF (TLT) and the S&P 500 (SPY). It shows how the market earthquake struck precisely in mid 2011 and hit Treasuries (positively) and stocks (negatively):

Fear was the trigger: The stock market dropped and Treasurys soared. The Federal Reserved stepped in – one month later – to begin Operation Twist, selling short-term debt and using the money to buy longer-term debt. The intent was to flatten the yield curve (a problem that does not need fixing in 2023).

One last chart shows the massive moves in Treasurys and the stock market in a single month, August 2011:

What is truly remarkable is that Treasury investments thrived amid this debt crisis and the downgrade from Standard and Poors. Fear was the driving force, and U.S. Treasurys were again shown to be the world’s premier “safety-first” investment.

2023: ‘This time is different’

Here we are, in March 2023, rolling toward the exact crisis we saw in 2011. Just like then, we have a Democratic president and a divided Congress (in 2011, by the way, Vice President Joe Biden was serving as the Senate President). But this isn’t a deja vu event. Things are quite different:

- A divided Republican party. I am trying to avoid making this about politics, but it’s clear that about 20 House Republicans will attempt to block any attempt to raise the debt ceiling, right to the brink of disaster.

- A no-compromise Democratic Party. Democratic leaders are strongly opposed to cuts in spending for social programs, including Social Security and Medicare. Most Democrats are refusing to even discuss spending cuts. A compromise will be very difficult to achieve in 2023.

- Where’s the middle ground? It’s going to take middle-of-the-road Republicans and Democrats to break from party pressure to reach a debt-limit agreement. In 2011, a lot of people were talking compromise. In 2023, you can hear crickets.

- A hamstrung Federal Reserve. U.S. inflation is likely to continue running well above the Fed’s target of 2% all summer. The Fed has limited ability to step in to support the bond or stock markets, even if disaster looms.

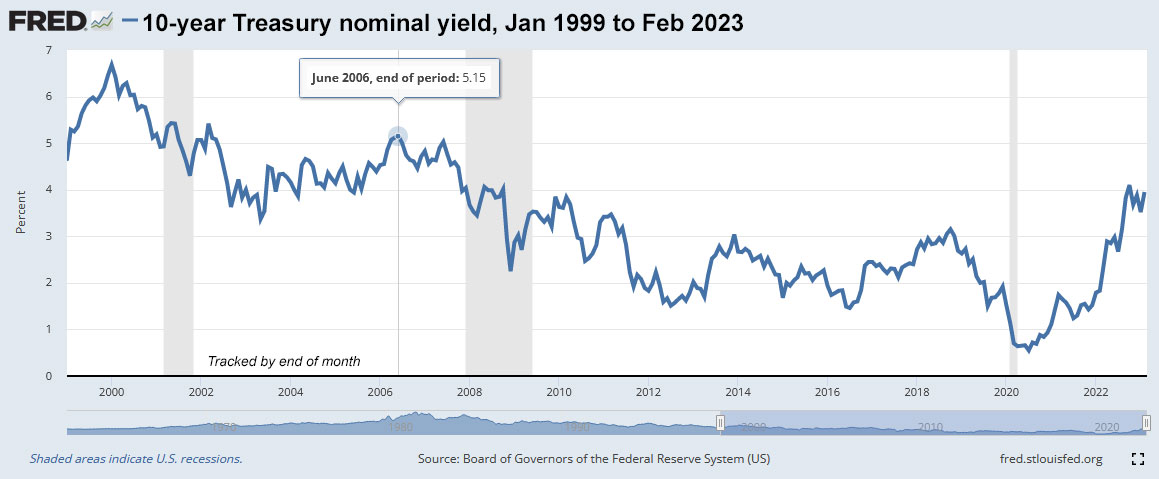

- A volatile Treasury market. In June 2011, the 10-year note was yielding 2.96%, very close to what it was a year earlier, 3.29%. Today, the 10-year is at 3.97%, up 211 basis points from one year earlier. This market is now more unpredictable and less steady than it was in 2011.

- A weakening economy. As interest rates continue to climb, many economists have been sounding the alarm about a looming recession. In 2011, the U.S. stock market was able to recover fairly quickly from the debt crisis, with the S&P 500 posting a total return of 16% in 2012 and 32% in 2013. There’s a lot more risk in 2023 with stocks still at fairly high valuations and the economy on a tightrope.

On the positive side, Biden has skills at negotiating a Congressional compromise. Eventually, both sides will probably have to “give” — a little.

Also interesting: Current Fed President Jay Powell played a key role is settling the 2011 debt crisis. At the time, Powell was a former Treasury official who was working for $1 a year as a visiting scholar at the Bipartisan Policy Center. Powell used his influence to help settle the issue, as CNN note in a recent article.

NPR’s Planet Money did a podcast recently on Powell’s role in 2011. Give it a listen:

Worst-case scenarios

A lot of readers have been asking me what will happen if the debt-ceiling negotiations fail and the U.S. government goes into debt-lock. My answer is: I don’t know. Will I Bonds continue to be issued? Will the United States continue paying interest on its debt? Will the U.S. pay out maturing Treasurys? Will Social Security payments get slashed? I don’t know.

The most probable outcome, in my opinion, is that we will come to the brink of debt disaster — and maybe even take a quick leap off the cliff — before Congress settles the issue by kicking the can down the road. Maybe Democrats will need to bend on some future spending cuts. Maybe Republicans will have to silence the ultra-hawks.

The Brookings Institution earlier this year issued a paper titled, “How worried should we be if the debt ceiling isn’t lifted?” It starts off with a bang:

“Once again, the debt ceiling is in the news and a cause for concern. If the debt ceiling binds, and the U.S. Treasury does not have the ability to pay its obligations, the negative economic effects would quickly mount and risk triggering a deep recession.”

In speculating on how a debt-lock could be handled, the authors note that the U.S. government created a contingency plan in 2011 at the height of the crisis:

“Under the plan, there would be no default on Treasury securities. Treasury would continue to pay interest on those Treasury securities as it comes due. And, as securities mature, Treasury would pay that principal by auctioning new securities for the same amount (and thus not increasing the overall stock of debt held by the public). Treasury would delay payments for all other obligations until it had at least enough cash to pay a full day’s obligations. In other words, it will delay payments to agencies, contractors, Social Security beneficiaries, and Medicare providers rather than attempting to pick and choose which payments to make that are due on a given day.”

You can read the full contingency plan here.

The Brookings paper also speculates on the level of non-interest spending cuts needed if the government goes into debt-lock:

“If the debt limit binds, and the Treasury were to make interest payments, then other outlays will have to be cut in an average month by about 20%.”

And it continues with this grim scenario:

“If the impasse were to drag on, market conditions would likely worsen with each passing day. Concerns about a default would grow with mounting legal and political pressures as Treasury security holders were prioritized above others to whom the federal government had obligations.

“In a worst-case scenario, at some point Treasury would be forced to delay a payment of interest or principal on U.S. debt. Such an outright default on Treasury securities would very likely result in severe disruption to the Treasury securities market with acute spillovers to other financial markets and to the cost and availability of credit to households and businesses. Those developments could undermine the reputation of the Treasury market as the safest and most liquid in the world. “

This Brookings scenario seems to indicate that Treasurys (and savings bonds) would continue to pay interest and continue to be issued in at least scaled-back form. All other government spending would be at risk. It’s highly likely we would see severe disruptions in the stock and bond markets.

Final thoughts

I am going to move forward trusting that a solution (although a temporary one) will be found for 2023’s version of the debt-ceiling crisis. But this is going to get ugly. Fasten your seat belts.

Note: Comments are welcome, but keep them constructive. No political flame-throwing will be allowed. However, politics is the issue today; so just keep comments on the topic and focused on solutions.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

In a professional setting in an estate planning law firm, the boss specifically told everyone to Never rely on AI…