By David Enna, Tipswatch.com

Back in the fall of 2020, when I was still writing for SeekingAlpha, I was getting a lot of questions about a new ETF with a tongue-twisting title: the Quadratic Interest Rate Volatility and Inflation Hedge ETF. Fortunately, everyone knew this fund by its ticker: IVOL.

The ETF’s creator, Nancy Davis of Quadratic Capital, was hailed as an innovator for this fund. Barron’s named her one of its top 200 Women in Finance in March 2020. But for me, IVOL was never particularly attractive. It was very new, with just a year of trading history. It was a fixed-income fund with a 1% expense ratio and a complex hedging strategy I couldn’t understand.

But … the interesting thing about IVOL is that it holds about 85% of its assets in SCHP, Schwab’s U.S. TIPS ETF, my favorite full-maturity-spectrum TIPS fund. On top of that, it overlays hedging strategies that seek to benefit from interest rate volatility. Quadratic’s information on the fund includes this summary of its strategy:

IVOL is a fixed income ETF that seeks to hedge relative interest rate movements, whether these movements arise from falling short-term interest rates or rising long-term interest rates, and to benefit from market stress when fixed income volatility increases, while providing the potential for enhanced, inflation-protected income.

Since IVOL launched in May 2019, we’ve certainly had a lot of interest rate volatility, but not in the way IVOL was targeting. Short-term interest rates have surged dramatically higher, while long-term rates have stabilized well below short-term rates, resulting in an inverted yield curve. So the performance of IVOL has suffered.

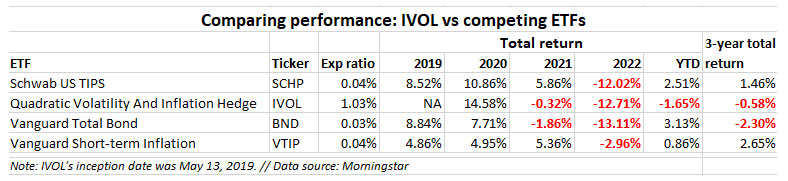

Remember, IVOL holds 85% of its assets in SCHP, but has an expense ratio about 25x higher than SCHP, 1% versus 0.04%. Here is a comparison of the total return for IVOL over the last three years versus SCHP, the total bond market ETF (BND) and Vanguard’s short-term TIPS ETF (VTIP).

From the chart, it is easy to see why IVOL, a shiny new invention, was such a hot fund in 2020, when it trounced the performance of similar investments, nearly doubling the return of the total bond market, 14.6% versus 7.7%. It benefited from having hedged positions that gained from falling short-term interest rates. The yield on a 13-week Treasury fell from 1.54% on Jan. 2, 2020, to 0.09% on Dec. 31.

In 2021, as both short- and long-term interest rates stabilized at very low levels, IVOL under-performed its two TIPS fund competitors by a wide margin. In 2022, when interest rates across all maturities surged strongly higher, all of these funds did poorly with the exception of the shorter-duration VTIP.

In summary, over the last three years, IVOL has out-performed the overall bond market, while under-performing the overall TIPS market. So I conclude that it has failed, so far, in its goal to provide “enhanced, inflation-protected income.” As a high-expense bond fund, I’d give it a B rating. But as a high-expense TIPS funds, it gets a C-.

A trial investment?

In September 2020 I decided to make small investments ($5,000) in both SCHP and IVOL and then track the results over time, with dividends being reinvested. But when I went to purchase IVOL, Vanguard informed me that its trading volume was too small for dividend reinvestments. I threw out that story idea and pretty much forgot about IVOL: too new, too small, too complex, and too expensive.

IVOL today

Nancy Davis still pops up often on Bloomberg and CNBC as a financial expert, and that makes sense because she has a lot of insight into the bond market. Here is a recent CNBC interview where she expresses a view I agree with: That we should see a less-inverted yield curve going forward:

A Forbes article this week took a look at IVOL, noting its celebrated launch in 2019 but mediocre performance since late in 2021. Here is a chart from the article, which is behind the Forbes paywall but also appears on MSN.com here:

The author, Brandon Kochkodin, has a certain way with words. Just take a look:

While others were asking whether inflation was dead, Davis was pitching her firm’s Interest Rate Volatility & Inflation Hedge ETF (IVOL). IVOL is a chimera, a lion with a goat’s head sticking out of its back. Most of its assets are held in a bond ETF that any mom or pop can buy. The rest of the money goes to options bets that are off limits to even many professional asset managers because of the sophisticated ways they offer investors of losing their shirts. It’s the options, however, that make IVOL unique and what could, if inflation expectations rise sharply and quickly enough, provide a windfall.

Davis’ timing couldn’t have been more perfect. By 2021, fretting about inflation moved from the fringe to the frontline. IVOL’s assets under management soared to more than $3.5 billion …

Nearly four years after raising the curtains … IVOL is in a rut.

Now, after attracting $3.5 billion in assets under management during its surge of popularity two years ago, IVOL today has total assets of $929.1 million. It’s daily volume is about 426,339 shares, compared with 2.47 million for SCHP and 3.46 million for VTIP.

I was wary of IVOL back in 2020, but that is my nature: I am wary of every new-fangled idea I can’t quite understand. The expense ratio of 1% turned me off. The complexity turned me off. The newness and small trading volume turned me off. That was 4 strikes, and I was out.

In coming months, if the yield curve does indeed begin widening back to normal, IVOL should do better. But it still doesn’t interest me.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

what are the advantages and disadvantages to own a 0-5 year maturity tips etf or a 15 years plus tips etf?

For the shorter-term TIPS fund, the advantage is less volatility. A fund like VTIP tends to track inflation well but won’t have large swings up or down as real yields change. For the longer-term TIPS funds, you *should* get a higher real yield (not true right now), plus greater volatility. So potentially these longer-term funds can give you capital gains, if you want to trade them. But also capital losses, if yields start rising.

i own individual tips and i bonds. i was thinking about getting a tips etf or tips mutual fund. when you get a tax form 1099 for them do they list oid? or just interest and capital gains distributions?

These funds pay out the inflation adjustment, so there is no 1099-OID, it is all considered interest.

Hi David,

Thank you for the article.

What are your thoughts on STIP v. VTIP? The two ETFs seem similar, but STIP has a slightly lower expense ratio.

Will there be advantages to owning TIPS ETFs vs. owning TIPS purchased in the auction or secondary market besides being able to buy smaller dollar amounts than $1000 from a broker? I intend to purchase and hold the investment in an IRA rather than from Treasury Direct.

With a maturity date of 4/15/27, yield to worst at 1.342% still a decent purchase?

Thank you in advance for your reply.

I own VTIP in a tax-deferred account, the only TIPS fund i own at this point. I sell some shares to fund my purchases of individual TIPS. VTIP has an expense ratio of 0.03%; STIP has the same expense ratio. These are very similar funds and both are fine.

Hi David,

I’d like to pick your brain regarding EE bonds. The question is whether to buy 10k bonds now or wait until May for the rate to reset. (By the way, thanks for the excellent post about making this same decision for I-bonds. That was very helpful.)

I am looking at EE bonds right now as a HYSA (after 1 year lock-in period) to stash emergency funds that will consistently give me 2.10% interest. If I don’t touch those funds for 20 years, I get the 3.55% rate when the bond doubles in value. If I have to redeem them before 20 years, oh well, I still get 2.10%. The HYSAs are paying 4% right now, but who knows what they’ll pay in 5 years. I already got 10k EE-bonds in December 2022. Now I’m wondering if I should make this year’s purchase by April or wait for the reset.

Is there any rough indicator to look at to predict what the EE-bond rates would be (like the 10Y-TIPS yields for I-bonds) ?

Should I get them now at 2.10% or wait for potentially slightly higher rate ? Would they ever set the rates above 3.55% ?

Thanks & regards,

EE confused

There is no way to know or predict what the EE fixed rate will be. It was 0.1% from November 2015 to October 2022 and no higher than 1.4% all the way back to May 2008. So the 2.1% fixed rate looks good. Back at the Nov 1 2022 reset the 10-year Treasury note was yielding 4.07% and now it is down to 3.55%. The trend doesn’t look good (right now) for a higher fixed rate. Things can change, of course.