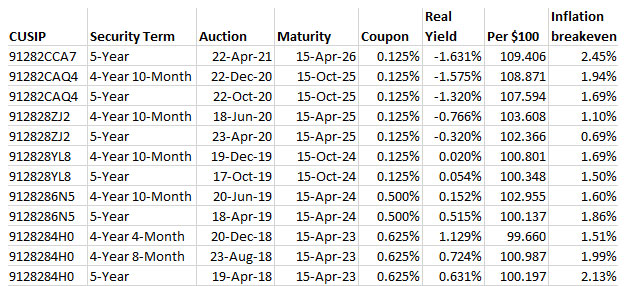

The Treasury’s offering of $18 billion in a new 5-year Treasury Inflation-Protected Security — CUSIP 91282CCA7 — auctioned today with a real yield to maturity of -1.631%, the lowest real yield at auction for any TIPS in history.

But here’s the surprise: The yield was a bit higher than expected, and it seemed to indicate lukewarm demand for this 5-year offering. The bid to cover ratio was 2.5, a decent number but well below recent auctions of this term.

A TIPS is an investment that pays a coupon rate well below that of other Treasury investments of the same term. But with a TIPS, the principal balance adjusts each month (usually up, but sometimes down) to match the current U.S. inflation rate. So the “real yield to maturity” of a TIPS indicates how much an investor will earn above inflation.

In this case, CUSIP 91282CCA7 got a coupon rate of 0.125%, the lowest the Treasury will allow for any TIPS. And that means investors had to pay a sizable premium to collect that 0.125% coupon for 5 years, plus future inflation accruals to principal. Investors paid an adjusted price of about $109.41 for about $100.32 of value, after accrued inflation and interest are added in. This TIPS will have an inflation index of 1.00273 on the settlement date of April 30.

The Treasury’s estimate of the real yield of a full-term 5-year TIPS ended Wednesday at -1.72%, about 9 basis points below today’s result. A four-year, 6-month TIPS is currently trading on the secondary market with a real yield of -1.87%, also much lower that today’s auction result.

Nevertheless, CUSIP 91282CCA7 got the lowest auctioned real yield for any TIPS in history, surpassing the -1.575% result generated by a 4-year, 10-month TIPS reopening on Dec. 22, 2020.

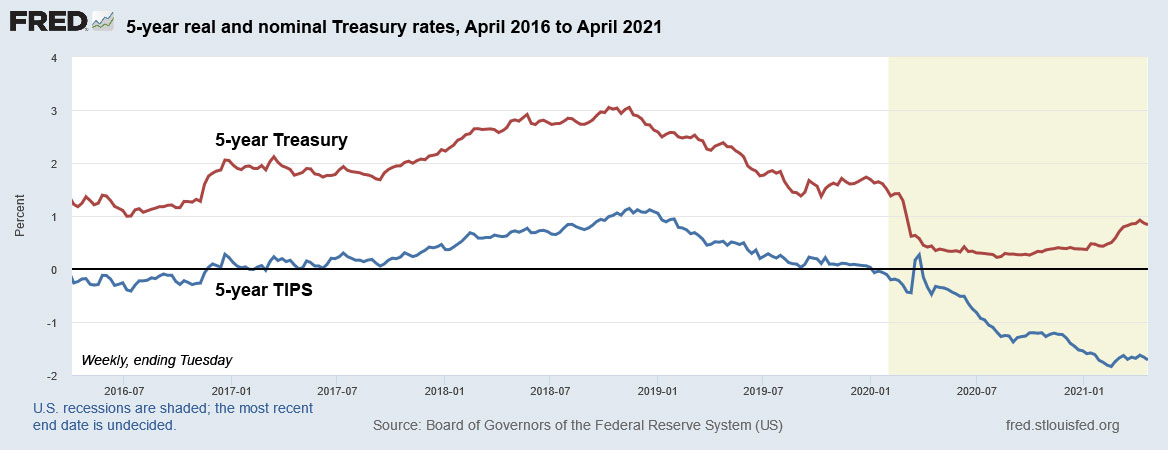

Here is the trend over the last five years for the real yield of a 5-year TIPS versus the nominal yield of the 5-year Treasury note, showing how the two yields have been moving in different directions in recent months, with the nominal Treasury yield moving higher and the real yield of a TIPS moving deeply below zero.

Negative real yields are not rare for TIPS, especially for the 5-year maturity. We’ve seen them often ever since the Federal Reserve began aggressive quantitative easing programs in 2011. But today offered a first: the lowest real yield for any TIPS of any maturity at auction.

Inflation breakeven rate

With a nominal 5-year Treasury trading at 0.82% at the auction close, this new TIPS gets an 5-year inflation breakeven rate of 2.45%, a bit below the number that looked likely as trading began today. But 2.45% is still higher than the result for any recent auction for any 4- to 5-year TIPS. In fact, since 2013, only two TIPS auctions of this term have generated a breakeven rate higher than 2.0%.

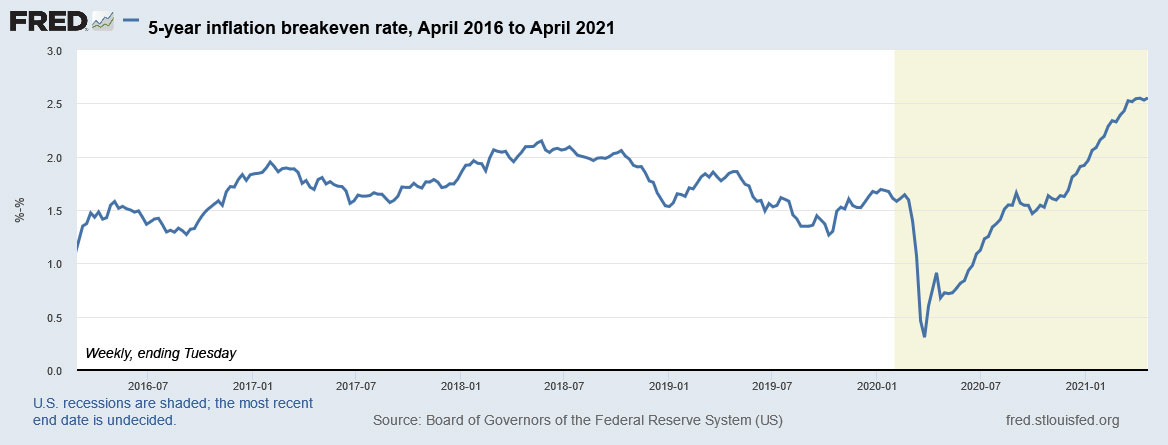

Here is the trend in the 5-year inflation breakeven rate over the last 5 years, showing the immense move higher since March 2020, when the Federal Reserve and U.S. Congress began aggressive programs to stimulate the U.S. economy, with the accepted side effect of driving inflation higher:

When the inflation breakeven rate rises, TIPS get more expensive versus a nominal Treasury. Before today’s auction closed at 1 p.m. EDT, a breakeven rate of as high as 2.7% looked possible. That might have sent some investors scurrying for cover.

Reaction to the auction

Based on the 4-year, 6-month TIPS trading on the secondary market with a real yield of -1.87%, I was expecting a real yield to maturity of -1.70% or lower for this TIPS. I can understand a shorter-term TIPS getting a lower real yield right now, because investors are pricing in higher inflation for the next year, but not necessarily for the longer term.

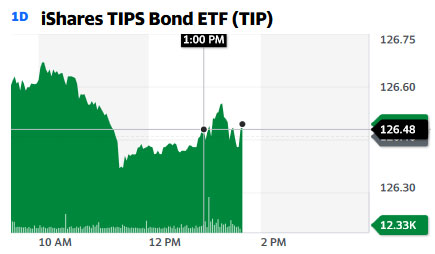

The TIP ETF — which holds the full range of maturities of TIPS — had been trading higher this morning, and seemed unbothered by the auction result, which closed at 1 p.m. EDT. This looks like the market saw the result … and yawned.

Investors at today’s auction should welcome the higher-than-expected real yield, even if it was a record low. And keep in mind that their holding will get a 0.71% boost in principal in May, reflecting non-seasonally adjusted inflation for March 2021.

This TIPS will be reopened at auction in June, and then the Treasury will offer a new 5-year TIPS in October. Here are auction results over the last three years:

The U.S. Treasury will offer $18 billion in a new five-year Treasury Inflation-Protected Security at auction on Thursday, April 22. This is CUSIP 91282CCA7, and its coupon rate and real yield to maturity will be set by the auction results.

I’ve been eyeing this offering for a few months, figuring it would be worth a look for investment. In a time of low yields, a 5-year TIPS becomes more appealing just because … the term is only five years, the lowest the Treasury offers for a TIPS.

But as Thursday’s auction approaches, this new TIPS isn’t looking appealing.

A TIPS is an investment that pays a coupon rate well below that of other Treasury investments of the same term. But with a TIPS, the principal balance adjusts each month (usually up, but sometimes down) to match the current U.S. inflation rate. So the “real yield to maturity” of a TIPS indicates how much an investor will earn above inflation.

Coupon rate. Although it will be set by the auction, this TIPS will get a coupon rate of 0.125%, the lowest the Treasury will go for any TIPS. That’s a 100% certainty.

Real yield to maturity. As of Friday’s market close, the Treasury was estimating the real yield to maturity of a 5-year TIPS at -1.73%, meaning an investor would be willing to receive a return that trails official U.S. inflation by 1.73% over the next five years. This would be the lowest real yield for any 4- to 5-year TIPS auction in history, surpassing the record -1.57% of the last auction of this term on Dec. 22, 2020.

Cost of the investment. Because the real yield looks likely to be about 186 basis points below the coupon rate, investors will have to pay a fairly lofty premium to receive the 0.125% coupon rate, plus future inflation adjustments. The adjusted cost should be somewhere around $109.30 for about $100.27 of value, after accrued inflation is added in. This TIPS will carry an inflation index of 1.00273 on the settlement date of April 30.

So in other words, investors are going to pay a premium of about 9% above par for this TIPS, and then will receive coupon interest of 0.125% plus accruals to principal matching inflation over 5 years.

One positive factor in this equation is that the May inflation accrual will add 0.71% to the value of this TIPS, matching the rate of non-seasonally adjusted inflation in March 2021. Big-money investors know this, and it will be factored into Thursday’s auctioned price.

Here is the trend in the 5-year real yield over the last five years, showing the deep decline that began as the COVID-19 pandemic erupted in March 2020, forcing extraordinary measures by the Federal Reserve and Congress to stimulate the U.S. economy:

Negative real yields are not rare for TIPS, especially for the 5-year maturity. We’ve seen them often ever since the Federal Reserve began aggressive quantitative easing programs in 2011. But we’ve never seen a TIPS of any maturity auction with a real yield as low as -1.73%.

Remember that a negative real yield doesn’t necessarily mean that a TIPS won’t have a positive nominal yield or that it is a bad investment. The investment has to be viewed against the overall interest rate environment and current expectations for future inflation. So that brings us to …

5-year inflation breakeven rate

With a 5-year Treasury note currently trading with a nominal yield of 0.84%, this TIPS would get a 5-year inflation breakeven rate of 2.57% if the auction results in a real yield of -1.73%. That would not be a record high for a 5-year TIPS, but it is very high.

Essentially, this breakeven rate means that inflation will have to average higher than 2.57% over the next five years for this TIPS to out-perform a traditional, nominal Treasury. U.S. inflation is currently running at 2.6%, so that looks OK. But five-year inflation averages haven’t exceeded 2.5% for any period ending in April since 2004 to 2009, when inflation averaged 2.6%.

The inflation breakeven rate is determined by market sentiment, comparing a Treasury’s nominal yield to the real yield of a TIPS of the same term. This measurement has been notorious in recent years for overestimating inflation. Here is a look at the 5-year inflation breakeven rate going all the way back to 2003, showing that a rate above 2.5% is a rarity:

I’ve highlighted two very high rates of the past:

On March 18, 2005, the 5-year inflation breakeven rate reached 2.92%. In the next five years, inflation averaged 2.4%. It overestimated inflation by 50 basis points a year.

On July 3, 2008, the 5-year inflation breakeven rate was 2.72%. In the next five years, inflation averaged 1.2%. It overestimated inflation by 150 basis points a year.

A high inflation breakeven rate indicates that a TIPS is a pricey investment versus a nominal Treasury of the same term. I consider 2.57% high. TIPS at these levels are expensive.

Here is a simple example of what this means: The 5-year Treasury note started 2021 with a nominal yield of 0.36% and now is yielding 0.84%, a gain of 48 basis points. A 5-year TIPS started the year with a real yield of -1.62% and now is yielding -1.73%, a decline of 11 basis points. The value equation has shifted toward nominal yields.

I’ve been tracking how TIPS have performed against nominal Treasurys over the last decade, and the results have been rather grim, as shown in this chart:

Of course, it’s possible we have entered a “new era,” with Federal Reserve and government stimulus pushing floods of easy money into the economy, spurring a new inflationary age. I do think that is possible. It’s definitely a reason to maintain a position in inflation-protected investments.

The math says: Invest in I Bonds

You can purchase a U.S. Series I Savings Bond today and get a fixed rate of 0.0%, which means its real yield is 0.0% and your investment will very closely match future U.S. inflation for as long as you hold the I Bond. That is a 173-basis-point advantage over a 5-year TIPS, and it means that an I Bond has a huge advantage as an investment, beyond the facts that it offers tax-deferred earnings, a flexible maturity and better deflation protection.

Yes, I Bonds have a purchase limit of $10,000 per person per calendar year. But the point is: Invest in I Bonds before you invest in TIPS in 2021. After you reach the cap, then consider a TIPS. And what about a 5-year Treasury or a 5-year bank CD? Here is how those investments compare, under varying inflation scenarios:

In every possible scenario where inflation averages higher than 1% a year, an I Bond will out-perform a 5-year TIPS, 5-year Treasury note or 5-year bank CD.

For the TIPS, out-performance against the nominal Treasury and bank CD only begins once the U.S. inflation rate averages 2.57%.

Honestly, the 5-year nominal Treasury at 0.84% and 5-year bank CD at 0.80% appear to be ridiculously unappealing. In that light, the 5-year TIPS — with its insurance against unexpectedly high inflation — looks much more appealing.

So is a 5-year TIPS yielding -1.73% a horrible investment? No, it isn’t. But unless inflation surges in the next five years, it could provide nominal returns well under 1% a year. And while an investor is guaranteed to receive full par value at maturity, that 9% premium you’d pay on Thursday isn’t part of par value and isn’t guaranteed to be returned at maturity.

Auction facts

Thursday’s auction closes for non-competitive bids (meaning those through TreasuryDirect or your brokerage) a noon EDT, and will finalize at 1 p.m. I will be posting the results soon after the auction closes.

Despite my qualms about this issue, I’m expecting demand to be fairly high, given the recent trend driving real yields lower, indicating investor demand.

Here’s a history of recent 4- to 5-year TIPS auctions, showing the current record low yield of -1.575% at the last auction on Dec. 22, 2020.

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

The March inflation report, released April 13, is going to create a lot of interest in U.S. Series I Savings Bonds, because the bond’s inflation-adjusted variable rate – for purchases from May to October — will increase to 3.54% from the current 1.68%.

All I Bonds will eventually get that 3.54% rate, annualized, for six months, on top of an I Bond’s fixed rate. But the new rate will raise a question for new investors in I Bonds: Should you buy before May 1, or after May 1? Or does it even matter? Before we get into that issue, let’s start with some basics, since I am assuming many new investors will now be researching I Bonds.

An I Bond is a U.S. Treasury security that earns a composite rate of interest based on combining a fixed rate and an inflation rate.

The fixed rate will never change. So if you bought an I Bond in 2014 with a fixed rate of 0.2%, it will continue to have a 0.2% fixed rate for the life of the bond. Purchases through April 30, 2021, will have a fixed rate of 0.0%. The fixed rate will be reset on May 3, 2021, but it is highly likely to remain at 0.0%. The fixed rate is equivalent to an I Bond’s “real return,” meaning its return above inflation.

The inflation rate changes each six months to reflect the running rate of non-seasonally adjusted U.S. inflation. Basically, the semiannual inflation rate is doubled to create what I call the I Bond’s “inflation-adjusted variable rate.” That rate is currently set at 1.68% annualized. It will adjust again on May 3, 2021, to 3.54% for I Bonds purchased from May to October. Over time, all I Bonds will get the 3.54% annualized rate for six months (on top of any existing fixed rate); but exactly when the new rate rolls out depends on the month of your initial investment.

Here is the formula the Treasury used to determine the I Bond’s current composite rate of 1.68%, drawn from the TreasuryDirect site:

The composite rate for I bonds issued from November 2020 through April 2021, is 1.68%

Here’s how we set that composite rate:

Fixed rate

0.00%

Semiannual inflation rate

0.84%

Composite rate = [fixed rate + (2 x semiannual inflation rate) + (fixed rate x semiannual inflation rate)]

[0.0000 + (2 x 0.0084) + (0.0000 x 0.0084)]

Composite rate

[0.0000 + 0.0168 + 0.0000000]

Composite rate

0.0168000

Composite rate

0.0168

Composite rate

1.68%

Key facts about I Bonds

An I Bond is a very safe, Treasury-backed investment that will at least track official U.S. inflation. The value of an I Bond can never decline. In a time of severe deflation, an I Bond might return 0.0% for six months, but its accumulated value will never decline. I Bond earnings compound tax-deferred for federal taxes until they are redeemed. Earnings are free of state income taxes.

The Treasury limits I Bond purchases in electronic form at TreasuryDirect to $10,000 per person per calendar year, plus allows an additional $5,000 in paper I Bonds in lieu of a federal income tax refund.

An I Bond must be held for one year, and after that, can be redeemed with a three-month interest penalty. After five years, there is no penalty for redemption. The I Bond will continue paying interest until its full maturity in 30 years. An I Bond can be purchased near the last day of a month and gain credit for a full month of ownership. That effectively shortens the initial lock-down holding period to 11 months.

I Bonds are an investment for capital preservation, not capital growth. You won’t get rich buying I Bonds, but you will be able to protect a portion of your portfolio against unexpectedly high inflation in the future.

Is there any chance the fixed rate will rise May 3?

Because of the $10,000-a-year purchase limit, there are two key strategies for investing in I Bonds: 1) Buy them every year to build up a sizable cache of inflation-protected money, and 2) Aim to get the highest fixed rate possible, because the fixed rate is permanent for the life of the bond.

I Bond investors — yes, me, too — are pretty passionate about getting the highest fixed rate possible. Right now the fixed rate is 0.0%, but a very attractive inflation-adjusted rate (3.54%) is about to kick in. Even the current rate of 1.68% is attractive versus very low interest rates across all safe investments.

The Treasury will reset the fixed rate on May 3 (because May 1 is a Saturday) and then again on Nov. 1. Is there any chance it will climb higher? I’d say with 99.8% certainty that the fixed rate will remain at 0.0% for the May reset. Why not 100%? Because at times, “the Treasury does weird things.”

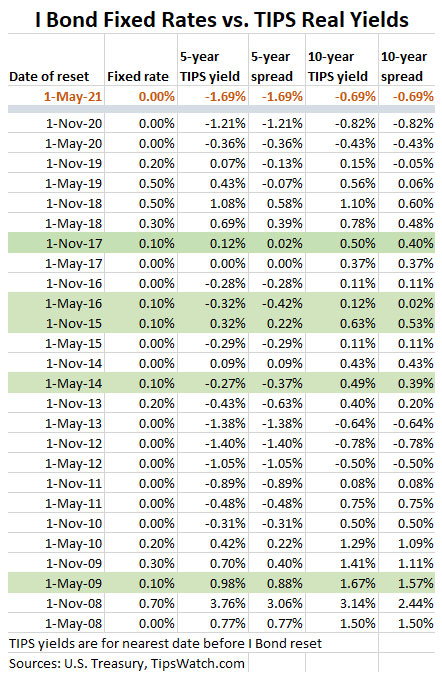

This chart shows all the fixed-rate resets back to May 2008, comparing the new rate with then-current real yields for 5-year and 10-year Treasury Inflation-Protected Securities. The top line compares TIPS yields at the market close on April 13, 2021. I’ve highlighted all instances when the fixed rate was set at 0.1%, slightly higher than it is today.

In today’s Treasury market, an I Bond has a 69-basis point advantage over a 10-year TIPS. But in every case where the Treasury set the I Bond’s fixed rate to 0.1%, the 10-year TIPS had a positive real yield, and at least a small yield spread higher than the I Bond’s fixed rate. So my conclusion is that the Treasury has no reason to raise the I Bond’s fixed rate; the bond already has a substantial yield advantage over a TIPS.

Now, the Treasury could throw us a curve ball and decide it wants to promote I Bonds for small-scale savers, and therefore set a 0.1% or 0.2% fixed rate. I’d be very surprised, and I don’t see that coming.

My conclusion. The fixed rate is going to remain at 0.0% in the May reset. The November reset is too far out for me to judge, but I’d expect it also to remain at 0.0%. And remember, any fixed rate increase in November would also be available to investors in January, when the purchase-limit clock resets.

Buy in April, or in May, or later?

Since the fixed rate is highly likely to remain at 0.0%, it should be irrelevant to this investment decision, unless you decide to wait until October to purchase I Bonds, to see if a higher fixed rate looks likely Nov. 1. By waiting until October, you’d still be able to capture the 3.54% inflation-adjusted rate for a full six months. So that is a viable option, if you believe there’s a chance that the fixed rate will increase in November.

But keep in mind, if you are investing $10,000 in an I Bond, the difference between a 0.0% fixed rate and a 0.1% fixed rate is $10 a year. In this article I am going to focus on the decision to invest in April versus May.

No matter the decision you make, an I Bond is going to be a very attractive addition to your asset allocation dedicated to “safety.” As shown in this chart, a 1-year Treasury bill is currently yielding 0.06% and best-in-nation 1-year bank CDs are yielding 0.60%. An I Bond — purchased in April or May — is going to easily outperform those metrics.

Is this a long-term investment?

I’m defining a long-term investment as a holding period of five or more years, avoiding the three-month interest penalty. We know that an I Bond with a 0.0% fixed rate will very closely match official U.S. inflation out into the future, but if you purchase an I Bond in April, you will know exactly what you will earn over the next 12 months.

Buy in April. That April-issued I Bond will earn 1.68%, annualized, for the first six months, and then 3.54%. annualized, for the next six months, for an overall first-year yield of 2.61%, more than four times the yield of best-in-nation bank CDs.

Buy in May. What if you invest in May? You would earn 3.54% annualized for the first six months, and then an undetermined rate for the next six months. Even if inflation runs at 0.0% for the next six months, you would still get a return of 1.77% for the year, nearly triple the yield of a 1-year bank CD.

I’ve modeled out other inflation-adjusted rate scenarios for the second six months, ranging from 0.5% to 3.0% for the March to September period. (Remember that the inflation-adjusted rate is double the actual-six month inflation rate; so an inflation rate of 0.84% equals an inflation-adjusted variable rate of 1.68%). So if inflation runs higher than 0.84% from March to September, purchasing in May will yield a higher return than purchasing in April.

Conclusion. There probably won’t be a lot of difference. If you believe inflation is likely to run hot from March to September, purchase your I Bonds in May. If you think inflation will cool off during that period, purchase in April. I suspect a lot of new investors will wait until May to start off with that 3.54% rate, and I can’t argue with that.

Is this a short-term investment?

As I noted above, an investor can shorten the I Bond’s 1-year holding period by purchasing late in a month and then redeeming early in that same month a year later, effectively creating an 11-month investment. But this strategy comes with a cost: The loss of the last three months of interest.

Buy in late April. In the 11-month scenario, an investor in I Bonds in April would earn 1.68% the first six months, then half of the 3.54% for the second six months (because of losing three months interest). This works out to an overall yield of 1.73% for the year, which again easily beats any very-safe one-year alternative.

Buy in late May. In this same scenario, an investor in I Bonds in May would earn 3.54% in the first six months and an undetermined yield in the second six months. Again, I’ve presented inflation-adjusted variable rate scenarios ranging from 0.0% to 3.0%, and one thing is very clear: Investing in May will out-perform investing in April in every scenario.

Even if the inflation-adjusted variable rate drops to 0.0% for the second six months, the investor would get a return of 1.77% — and the three-month penalty would be zero, because no interest was earned in the last six months. The Buy-In-May scenarios outperform Buy-in-April scenarios in every case.

Conclusion. If you are looking to invest in an I Bond as a safe place to store cash as an 11-month investment, wait until near the end of May 2021 to invest, then redeem early in May 2022.

The big picture

The financial market of April 2021 is difficult for investors seeking safety. If you are holding $10,000 in a brokerage firm’s cash or money market account, you will probably earn less than $5 of interest this year. Your monthly statement probably shows “30 cents interest.” An I Bond is a very safe investment with a flexible maturity, and that same $10,000 in invested in an I Bond could generate $250 or more in the next year, and then continue tracking official U.S. inflation.

I know, small potatoes. I’ve seen some investors chuckling in the Bogleheads forum over the obsession of I Bond investors to chase $10 to $20 in additional annual interest. But if you are holding cash for future use, you really want a return that at least matches official U.S. inflation. And I Bonds will do that, no matter if you buy them in April, in May, or later in 2021.

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

U.S. inflation surged 0.6% in March, the Bureau of Labor Statistics reported today, and provided the final piece of data to determine the new variable rate for U.S. Series I Savings Bonds: a whopping 3.54%, annualized, for purchases after April 30 and eventually for all I Bonds.

The I Bond’s new variable rate is based on a six-month inflation rate, in this case from September 2020 to March 2021. Non-seasonally adjusted inflation increased 1.77% over that period, which translates to a new six-month variable rate of 3.54%, annualized, for all I Bonds. That is a huge increase over the current rate of 1.68%.

In today’s report, the BLS set the March inflation index at 264.877, an increase of 0.71% over the February number. It’s been a strange six months, with non-seasonally adjusted inflation rising only 0.06% in the first three months, then surging 1.69% in the last three months.

Here are the relevant numbers (you can see historical data on this page, which I update monthly):

What this means

Obviously, we are going to see intense investor interest in I Bonds over the next few months, with the new composite interest rate — combined with a 0.0% fixed rate — likely to be 3.54% (annualized) for six months. That is the highest rate reset since May 2011, when the inflation-adjusted variable rate surged to 4.6%.

For current I Bonds. If you already bought your I Bond allocation in 2021 (as I did in January), you will be earning 1.68% for six months and then 3.54% for six months, for a one-year rate of 2.61%, triple the current earnings of any other very safe one-year investment.

Investments in I Bonds are limited to $10,000 per person per calendar year, along with the possibility of purchasing $5,000 in paper I Bonds in lieu of a federal income tax refund.

All I Bonds, no matter when they were purchased, will get the 3.54% variable rate for six months. When that rate kicks in depends on the month you purchased the I Bond. Remember, when you purchase an I Bond, you always get the current composite rate for six months, before the next reset takes effect. Here is that schedule:

Issue month of your bond

New rates take effect

January

January 1 / July 1

February

February 1 / August 1

March

March 1 / September 1

April

April 1 / October 1

May

May 1 / November 1

June

June 1 / December 1

July

July 1 / January 1

August

August 1 / February 1

September

September 1 / March 1

October

October 1 / April 1

November

November 1 / May 1

December

December 1 / June 1

Purchases after May 1. If you wait until May 1 to purchase I Bonds, you can be assured of earning 3.54% for six months, and then a-yet-to-be determined rate for six months. But the worst you could do is 1.77% over the year, even if the next variable rate resets to 0.0%.

I suspect a lot of investors who haven’t yet purchased I Bonds in 2021 will now wait until after May 1, locking in that higher variable rate for the first six months.

Let’s remember the reason we invested in I Bonds: To protect against unexpectedly high inflation. In March 2021, we got exactly that. I will be writing more on this topic in a few days after I let today’s news settle in.

The March inflation report

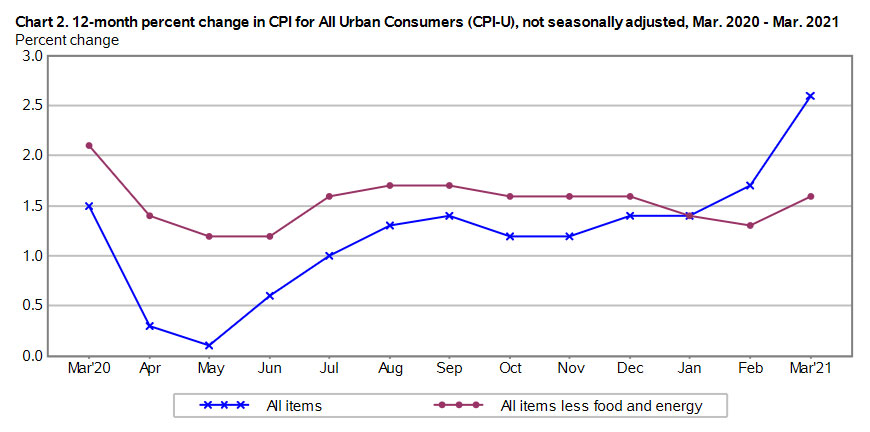

The Consumer Price Index for All Urban Consumers increased 0.6% in March on a seasonally adjusted basis, the BLS reported. This 1-month increase was the largest rise since a 0.6% increase in August 2012. Over the last 12 months, the all-items index increased 2.6%.

Economists were expecting higher inflation in March, based on very weak numbers in pandemic-stricken March 2020. But actual inflation for the all-items index was higher than the consensus, for both the month and year-over year.

Core inflation, which removes food and energy, came in at 0.3% for the month, also higher than the consensus estimate. The year-over-year number for core inflation matched the target of 1.6%.

The BLS noted that higher gasoline prices again were a key factor in March’s inflation increase, rising 9.1% for the month and accounting for nearly half of the seasonally adjusted increase in the all-items index. Other items of interest:

Food prices increased a moderate 0.1% in the month, but are up 3.5% over the last year.

The costs of shelter increased 0.3%, but are up only 1.7% over the year. (Rents have been held down by eviction moratoriums and other measures, which may end soon.)

Prices for used cars and trucks increased 0.5% and are up 9.4% over the year.

Apparel prices fell 0.3% and are down 2.5% over the year.

The motor vehicle insurance index increased for the third consecutive month, rising 3.3 percent in March.

The index for medical care services rose 0.1% for the month and is up 2.7% for the year.

Here is the overall trend for both all-items and core inflation over the last year, showing the dramatic rise in all-items inflation (primarily caused by rising gas prices) and the relatively stable path for core inflation:

What this means for TIPS

As with I Bonds, non-seasonally adjusted inflation is the key number for Treasury Inflation-Protected Securities, setting future adjustments of principal balances for TIPS. March’s increase of 0.71% in non-seasonally adjusted inflation means that principal balances for all TIPS will rise 0.71% in May, following a 0.55% increase in March.

The Federal Reserve certainly saw this coming: U.S. inflation was going to surge in the spring of 2021 when compared to the very weak numbers of spring 2020, when much of the economy was shut down. I don’t think today’s report alone will have any effect on the Fed’s policy. It will need to see many months of surging inflation to change course.

So for now, expect the Fed to continue holding short-term interest rates near zero, and to continue its current program of bond-buying, with any tapering or increases that could jolt the market.

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

One of the most important inflation reports of the year is coming up Tuesday at 8:30 a.m., when the Bureau of Labor Statistics releases its March inflation report. That report carries a lot of weight, because:

It will set the I Bond’s new inflation-adjusted variable rate, which looks likely to rise to 2.5% or higher (annualized), maybe even 2.8% or higher. That rate — which will go into effect for newly purchased I Bonds on May 1 and eventually for all I Bonds — is based on official U.S. inflation from September 2020 to March 2021. Through February, inflation had increased 1.05%, which translates to an I Bond variable rate of 2.10%. If non-seasonably adjusted inflation comes in at — let’s say a conservative 0.3% — The I Bond’s variable rate would rise to 2.7%, versus the current 1.68%.

The consensus estimate for seasonally adjusted all-items inflation in March is 0.5%, following a rise of 0.4% in February. That would likely push year-over-year U.S. inflation up to about 2.5%, the highest rate since January 2020.

Core inflation, which strips out food and energy, is projected to increase 0.2% for the month, pushing the year-over-year number up to 1.6%, from last month’s 1.3%. If core inflation comes in higher than 0.2%, it will be signalling a stronger inflationary trend.

None of this is surprising. Remember that inflation in March 2021 is being measured against inflation in pandemic-stricken March 2020, which declined 0.2% that month and declined again 0.7% in April 2020. So it’s been looking likely that we would see a surge in U.S. inflation in spring 2021, reflecting the effects of a year of government stimulus and economic recovery.

This is the theme of a report issued last week by the investment firm PIMCO, “Dealing With an Inflation Head Fake,” written by Joachim Fels and Andrew Balls. Their premise is that although the U.S. and global economies will be recovering strongly this year, the jump in inflation will be temporary. From the report:

Investors should be prepared for an inflation “head fake” and look to maintain portfolio flexibility and liquidity to be able to respond to events in what is likely to be a difficult and volatile investment environment. …

While there is a lot of potential for medium-term economic scarring, there is likely to be a strong cyclical boom this year. … As a consequence, following a 3.5% contraction in 2020, we now forecast world GDP growth (at current exchange rates) in excess of 6% in 2021, up from 5% previously. …

Over the next several months, a combination of base effects, recent increases in energy prices, and price adjustments in sectors where activity ramps up is likely to push year-over-year inflation rates significantly higher. However, we forecast that much of this rise will reverse later this year.

Here is PIMCO’s outlook for U.S. inflation through 2022, showing an increase to 3.5% in all-items inflation in coming months, before both all-times and core inflation begin settling down to about 2.0% year over year:

Will this be a ‘head fake’?

I don’t claim to know. Inflation is incredibly hard to predict beyond a month or two into the future, and even then, something unexpected can happen, such as a hurricane ripping through Texas and knocking out oil refineries.

Inflation has remained stubbornly low over the last decade, much lower than the bond market or economic experts predicted. The result is that U.S. policymakers and market-makers are complacent about inflation: Even though they can see it rising, they aren’t concerned.

For a perspective on the wanderings of U.S. inflation, take a look at this historical chart of monthly year-over-year inflation, going back to 1948:

It is true that U.S. inflation has been relatively mild for decades, all the way back to October 1990, when it hit 6.4%. A true “head fake” happened in July 2008, when inflation soared briefly to 5.6% before plummeting to -2.1% a year later in July 2009. That steep drop, however, came during the century’s worst economic recession.

So, where are we headed?

Here are some thoughts from inflation watcher Michael Ashton, who writes on inflation in his E-piphany blog:

There is a growing list of categories of prices which are seeing abnormal price pressures. … There has become an acute shortage of semiconductor chips, which has impacted automobile production (and will that increase prices for what is available?). There is a shortage of shipping containers, causing widespread increases in freight costs affecting a wide variety of goods. Packaging materials, which are also a part of the price of a great many goods, are also shooting higher in price. Worker shortages at various skill levels were reported in the most-recent Beige Book. There is a shortage of Uber and Lyft drivers.

Importantly, we should add to these shortages a growing shortage of housing. The inventory of homes available for sale just hit an all-time low … And, as a result, the increase in the median sales price of existing homes just reached an all-time high spread over core CPI. …

But it might also be the case that the current rapid escalation of home prices is the market’s attempt to get the real value of the housing stock to reflect the rapidly increasing value of the money stock. If that’s the case, then it also suggests that median wages probably will eventually follow.

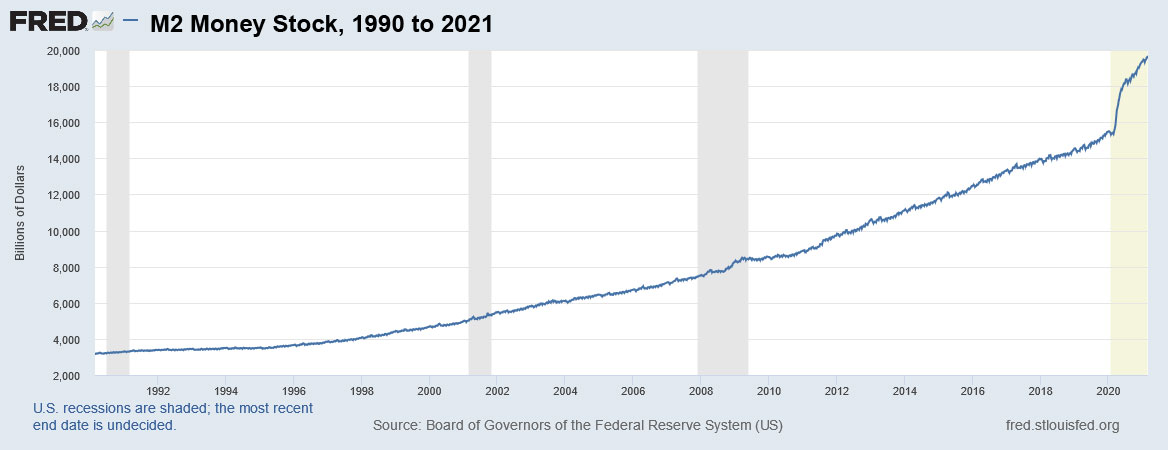

Consider this about the U.S. money supply: the M2 money stock measurement has increased about 26% over the last year, from about $15.5 trillion in January 2020 to $19.6 trillion in March 2021. That’s a sharp difference from the trend we’ve seen during all the years of relatively mind inflation since 1990:

Maybe money supply doesn’t matter, and doesn’t influence inflation. But this chart is strong evidence we have entered a “new era.” On the flip side of this, the value of the U.S. dollar has declined about 7% over the the last year, as shown in this chart:

Increasing consumer demand, supply shortages, possible labor shortages, a soaring money supply, a weaker U.S. dollar: These factors all will contribute to rising inflation over the short term. Will that trend last beyond 2021 or just be a “head fake”?

I don’t know the answer, but think staying prepared for inflation is a wise investment move.

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

It would be my pleasure to accommodate you However, the URL for 20 year TIPS at CNBC pulls up no…