By David Enna, Tipswatch.com

The U.S. Treasury on Thursday (Feb. 18, 2021) will auction $9 billion in a new 30-year TIPS, CUSIP 912810SV1. The coupon rate and real yield to maturity will be set by the auction results, but a couple things are nearly certain: 1) The coupon rate will be set at a record-low 0.125%, and 2) the real yield to maturity is likely to be negative to inflation.

Because my style of investing in TIPS is to buy and hold them to maturity, a 30-year TIPS has zero appeal for me. I have invested in them in the past, with maturities in 2029 (3.875% coupon rate) and 2041 (2.125% coupon rate). Those remain outstanding investments, but now that the new-issue maturity date has stretched out beyond my likely lifespan — 2051 — and real yields have dropped to negative levels, a 30-year TIPS doesn’t interest me.

A TIPS is an investment that pays a coupon rate well below that of other Treasury investments of the same term. But with a TIPS, the principal balance adjusts each month (usually up, but sometimes down) to match the current U.S. inflation rate. So, the “real yield to maturity” of a TIPS indicates how much an investor will earn above (or below) inflation.

The U.S. Treasury is currently estimating the real yield of a full-term 30-year TIPS at -0.16%, which means an investor is willing to accept a return 0.16% less than official U.S. inflation over the next 30 years. That yield estimate has actually been rising recently, coming off a 2021 low of -0.39% on Jan. 4.

The lowest auctioned real yield for any 29- to 30-year TIPS was set last year, on Aug. 20, when a 29-year, 6-month TIPS got a real yield of -0.272%. That is the only auction of this term to ever get a negative real yield.

If Thursday’s auction result sets the real yield in the negative range, the Treasury will set the coupon rate of this TIPS at 0.125%, and investors will have to pay a premium, probably about $108.50 (or more) for $100 of par value in this TIPS.

To summarize, then, an investor interested in purchasing $10,000 of this TIPS will have to make an initial investment of about $10,850, and then will receive about $12.50 in interest payments a year, rising with inflation. The principal balance will also rise with inflation, for 30 years. The accrued principal (which is taxable in the current year it is accrued) can’t be touched until the TIPS matures or is sold. This is the reason a TIPS of this term, with this low a yield, should only be purchased in a tax deferred account.

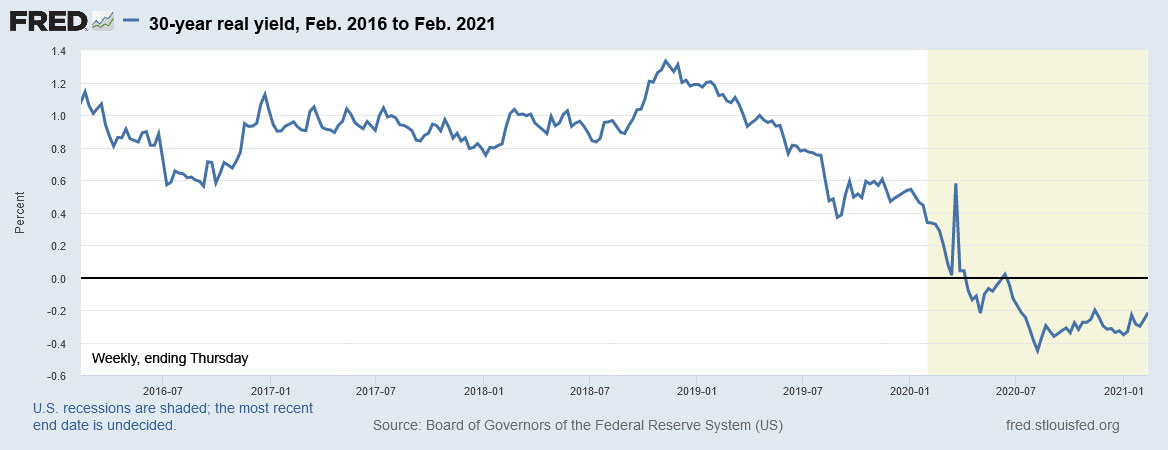

Here is the trend over the last 5 years in the 30-year real yield, showing the dramatic drop in after-inflation returns since early 2019, and the dip into negative yields after the Federal Reserve began its bond-buying stimulus program in March:

30-year TIPS as trading investment

Because 30-year Treasurys (bonds or TIPS) are so volatile, many investors find them appealing for short-term trades. For example, a new 30-year TIPS issued a year ago, on Feb. 20, 2020, got a real yield of just 0.261% and a coupon rate of 0.250%, both of which look unattractive. But that TIPS — which auctioned with an adjusted price of about $99.64 — is now trading on the secondary market at $112.46, a gain of 12.5% in a year.

A small swing in yield for a 30-year Treasury can generate a large gain or loss in the short term. Traders just need to understand the risk. It’s not my thing. I have no opinion.

30-year inflation breakeven rate

With a 30-year Treasury bond trading with a nominal yield of 2.01%, this TIPS would get an inflation breakeven rate of 2.17% if it auctions with a real yield of -0.16%. That would be the highest breakeven rate for any auction of this term since October 2013, but breakevens were also near this level in 2018. A higher inflation breakeven rate indicates that a TIPS is becoming more “expensive” versus a nominal Treasury of the same term.

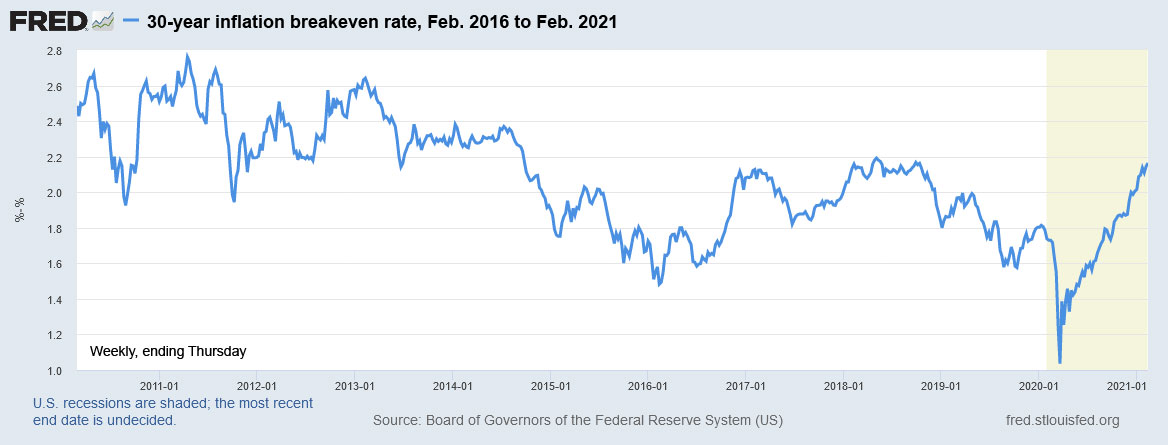

Here is the trend in the 30-year inflation breakeven rate over the last 5 years, showing the very strong rise in inflation expectations since the worst days of the pandemic in March 2020:

The obvious alternative: U.S. Series I Savings Bonds

Another Treasury issue, the U.S. Series I Savings Bond, also adjusts to official U.S. inflation but currently has a real yield of 0.0%, which is 16 basis points higher than a 30-year TIPS. (That spread is equal to nearly 5% in current value.) But the I Bond has other significant advantages: 1) a flexible maturity date of 1 year with a small penalty, or 5 to 30 years with no penalty, 2) tax-deferred interest payments, and 3) much better protection against future deflation.

When a 30-year TIPS has a negative real yield, the I Bond is a superior investment. Purchases are limited, however, to $10,000 per person per calendar year.

The Feb. 18 auction

Noncompetitive bids (like those made at a brokerage or Treasury Direct) close at noon on Feb. 18, and the auction ends at 1 p.m. I will be posting the results Thursday after the close.

Here’s a history of recent TIPS auctions of this term:

Auction morning update: The Treasury’s estimate of the 30-year TIPS real yield closed at -0.11% on Wednesday, up 5 basis points since Friday. The 30-year inflation breakeven rate held at 2.17%. This auction closes at 1 p.m. EST.

The lowest the Treasury will go on the coupon rate for a TIPS is 0.125%. So, when the real yield goes negative, the coupon rate is automatically set to 0.125%.

David

Thank you for your kind efforts. Your knowledge and friendly introduction to buying TIPS is very welcomed.

But………I am a 75 year old retired English Major who is struggling bravely to understand the concepts and wisely hold on to my money. I bought TIPS in my lucrative working past by just calling my broker and never looking at the confirmation. Now, on my own with only David Swensen’s “Unconventional Investor” to guide me, I bought 60m at the January 21st 10 year auction and then panicked when I saw the confirmation. Paid 67,000…over a 10% premium..coupons add up to $600, negative real yield yada yada…it was terrifying. Sold them the next day and somehow made $450.

So……………..can you direct me, maybe to a prior post, to where I can get my William Wordsworth head around these notions. Or…..might I ask you some questions in my language to try and prepare myself for my next attempt.

Yours in concept..

Peter … Yes, these negative real yields make purchasing TIPS at auction a wild adventure. In my preview articles, I try to lay out the premium costs you may pay at each auction. In the preview for that Jan. 21 auction, I noted: “A real yield that low will mean investors will be paying more than a 11% premium over par value for that coupon rate of 0.125%.” https://tipswatch.com/2021/01/16/up-next-new-10-year-tips-will-auction-jan-21/

In that auction, you were getting a coupon rate of 0.125%, plus adjustments to principle that would match inflation for 10 years. However, the auctioned real yield to maturity was -0.987%. Just for a rough estimate, how much would that cost? Take the 0.987% and add the 0.125% coupon rate, which equals 1.112%. Multiply that by 10 for the 10-year term, and you get an estimated premium (over par) cost of 11.1%. So buying $10,000 of that TIPS at auction was going to cost you $11,210, by the rough estimate. The actual adjusted cost was about $111.64 for about $100.005 of value, when accrued interest was added in.

Is this a horrible deal? No, it is just the cost of getting a coupon rate of 0.125% plus future inflation when the real yield auctions at -0.987%, which was the lowest ever for a TIPS of this term.

You lucked out after your purchase because real yields continued declining and you were able to exit with a gain.

So in the future, when you look to buy TIPS, make sure to recognize the cost above par you will pay if you are accepting a negative real yield.

thank you for the clarity….the math on what you wind up paying makes sense to me now and I see how you can learn the estimated/probable real yield from the Treasury Resource Center….last notion…how were you so sure going in that .125 was going to be the coupon rate?

Always enjoy reading your reports. Thanks for keeping us informed.