By David Enna, Tipswatch.com

Also: See my update on why this real yield was actually logical (to bond traders).

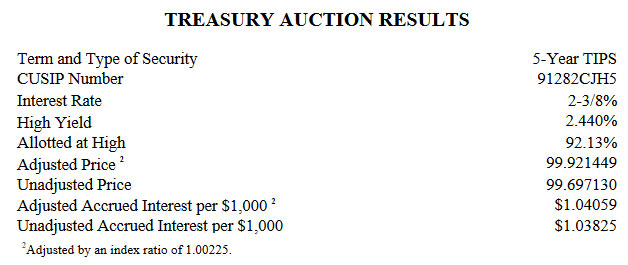

Today’s Treasury auction of $22 billion in a new 5-year Treasury Inflation-Protected Security generated a real yield to maturity of 2.440%, continuing a recent trend of mildly disappointing results for TIPS at auction.

This is CUSIP 91282CJH5, which will mature Oct. 15, 2028. At yesterday’s market close, the U.S. Treasury estimated the real yield of a full-term 5-year TIPS at 2.57%, and a TIPS with a similar term was trading all morning with a real yield in the range of 2.54% to 2.61%. So the result of 2.440% was a downside surprise, indicating fairly strong demand for this new issue.

I was expecting a real yield and coupon rate topping 2.5%. Nevertheless, this TIPS broke through some historic milestones:

- The real yield of 2.440% was the highest for any TIPS auction of this term going back to October 2008, during the heart of the U.S. financial crisis.

- The coupon rate was set at 2.375%, the highest for any 5-year TIPS since the very first TIPS auction of this term in history, which generated a coupon rate of 3.625% on July 9, 1997.

- The auction size was $22 billion, the largest for this term in history.

While the real yield came in a bit lower than expected, CUSIP 91282CJH5 measures up as a stellar investment, with a real yield 112 basis points higher than a similar auction just six months ago, on April 20.

Investment cost

Because this was an auction of a new TIPS, the coupon rate (2.375%) was set below the auctioned real yield (2.440%) and investors got CUSIP 91282CJH5 at a slight discount. The unadjusted price was 99.697130. Here is how that works out for a $10,000 investment:

- Par value: $10,000

- Inflation index on settlement date: 1.00225

- Adjusted principal: $10,022.50

- Unadjusted price: 0.99697130

- Investment cost (adjusted principal x unadjusted price): $9,992.15

- Plus, accrued interest: $10.41 (will be returned at first coupon payment)

- Total cost: $10,002.56

Inflation breakeven rate

At the auction’s close, a 5-year Treasury note was trading with a nominal yield of 4.95%, creating an inflation breakeven rate of 2.51% for this TIPS. That is about 30 basis points higher than the breakeven for recent auctions of this term. Hard to explain, but the 5-year nominal yield actually rose today a few basis points, while this TIPS auction came in 10+ basis points lower than expected.

And the bid-to-cover ratio was 2.36, indicating just average demand. But the pre-auction “when issued” measurement of expected yield was 2.42%, below the actual result. So, the when-issued number most likely indicates strong advance orders for this TIPS from big-money investors, orders that are too big for the secondary market. And therefore those buyers were willing to accept a lower real yield.

Anyone have other theories?

Final thoughts

Today’s auction adds another notch to the view that buying TIPS on the secondary market is a wise move, since you know exactly the real yield and price you will be getting. We’ve had a slew of “slightly” disappointing TIPS auctions this year.

I wasn’t a buyer because my TIPS ladder is loaded with maturities in 2028. But honestly, this real yield of 2.440% was highly desirable, even if a little disappointing. Since it is a new issue, there was no direct comparison on the secondary market.

CUSIP 91282CJH5 will be reopened at auction on Dec. 21, 2023. It will be interesting to watch yield trends over the next two months.

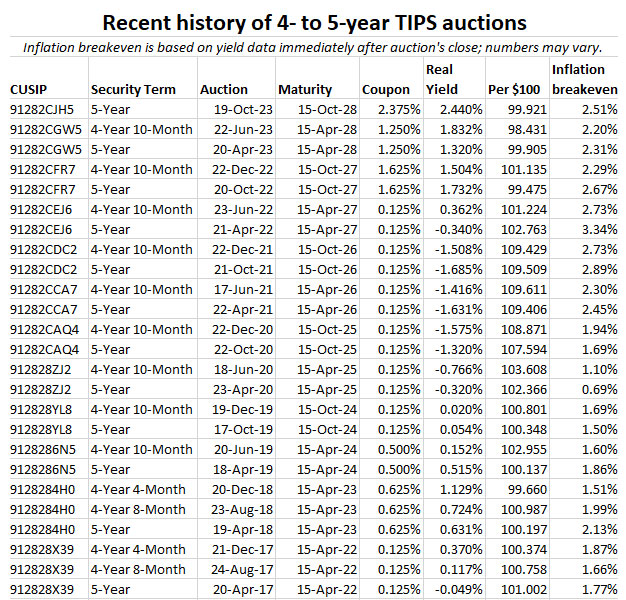

Here is the history of 4- to 5-year TIPS auctions going back to 2017. Note there is nothing on the list that even comes close to a real yield of 2.440%.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Pingback: Next week’s 5-year TIPS auction has solid appeal | Treasury Inflation-Protected Securities

Pingback: 5-year TIPS reopening auction gets real yield of 1.710%, on target for investors | Treasury Inflation-Protected Securities

Any idea why there is a large discrepancy in pricing in the secondary market for the same bond? I’m looking at Schwab

Here is the 5yr you wrote about:

US Treasury TIP 2.375% CUSIP 91282CJH5 Price 100.02900 YTM 2.369

US Treasury TIP 2.375% CUSIP 91282CJH5 Price 100.94500. YTM 2.171

This seems to be true for all bonds to varying degrees. I’m looking to buy more quantity than what is offered ifor the cheapest ask so I am concerned about the large variation and price and resultant YTM.

That’s a pretty large variance, so it can’t be because of quantity. Could be weekend oddities, since you can’t complete a purchase on the weekend. Vanguard greys out secondary TIPS on the weekend. But at this point (Saturday) is showing an ask price of 99.890 and a real yield of 2.398%.

Fidelity is showing an ask price of 100.029 and yield of 2.368%. So that top line looks more reasonable.

Wait until Monday to get a true quote, I would guess.

Upon issue today, this TIPS has an ask of 2.37% for amounts under 100k on Fidelity. So those who bought at the auction did just fine.

I think buying tips in auction is like playing a Russian roulette. Just a few weeks ago, the break even rate was close to 1.99% in the secondary market, so what happened? 50 basis point move is huge. There is a lot of chatter that the street demand for the long bond was very weak and investors are demanding a higher term premium. As David pointed out, the bid to cover ratio was average! I am stumped! At least, if you buy in secondary, you know what you’re getting. In auction, one cannot fulfill even reasonable expectation of getting real yield close to pre-auction market rate!

Not quite Russian roulette, since you might be just missing out on 10 basis points. (Not a big deal, but it still stings, I know.) In many past auctions, small-scale buyers got the benefit of getting the auction’s high yield without any spread. But now the secondary market generally has no-commission trading and reasonable “buy” yields. Plus you can buy any maturity you want.

I’m not disappointed with the slightly lower than expected real yield. I used this to “pre-pay” the gas and some other expenditures for my child’s first big game hunting season in October/November 2028. The 2 3/8% coupon is coffee money (the coupon will actually stay in TreasuryDirect in some form for some time).

Note: I use TreasuryDirect, so I can’t sell on the secondary market. I also don’t have enough money sloshing around at any one time to regret buying too much of a single security at auction. A 100 here, a few or more there, reinvest in that instead of this, make sure I have enough in I-Bonds for an emergency… a different situation (read: different point in life) than most readers of this site.

I have found this site very helpful. Thank you.

J.D., you hit on one very good reason to buy at auction: The ability to buy in increments of $100 on TreasuryDirect. Brokerages want minimum bids of $1,000 and sometimes much more.

so how do you all control your lizard brain ? (regret buying at auctions) or (regret buying on secondary) . how much basis points (loss) is regrettable ? are you on with 10year tips buying at 2% real yield now that real yield is 2.5%. (most probably not since you have lots of free time like me (to post comments))

The truth: Once I buy a TIPS with a decent real yield, I file it away and pretty much forget about it. It’s a safe investment, and while it is fun to gripe about 15 basis points, that shortfall will have zero effect on my future life.

There is so much to learn about life from Tipswatch blog – if one has the CONVICTION that TIPS is right investment instrument for them, the MINDSET of longterm investing, the MINDSET of CONTENTMENT, the MINDSET of selflessness in SERVING similar INTERESTS in the community and world at large by SHARING USEFUL KNOWLEDGE for the benefit of all, etc. This overall MINDSET helps MIND BE FREE, this is TRUE FREEDOM and one can go to greece, macedonia or stay right HERE right NOW and BE HAPPY!

Definitely Treasurydirect vs. brokerage accounts (they are all about fostering a trading MINDSET) is way to go for SET/FORGET even more so for longer term securities as daily market fluctuations won’t CATCH mind’s ATTENTION unnecessarily prompting knee-jerk REACTIONS:-)

BEING HAPPY is all about setting MIND FREE TO BE and STAYING HAPPY is about serving the HIGHEST GOOD of ALL ALIKE! David teaches with his MINDSET how to live life, invest, share selflessly and BE HAPPY on days market goes up and sun is shining and days markets go down and cloudy / windy days, above all else! This MINDSET is what I strive to CULTIVATE with practice and David is role model enough!

I’m pretty new to investing in TIPS but bought some in today’s auction in my IRA. I’m wondering why my broker has already taken the purchase cost out of my account if the bonds aren’t actually issued until 10/31. If I’ve already paid for the bonds, why do I still have to pay accrued interest on the purchase? The treasurydirect.gov site states that for a purchase made directly through them one must “Make sure enough money is in your bank account to pay for the security before the issue date for that security”, suggesting that I should still have use of my funds until 10/31. Do all brokers do this, or is it perhaps a requirement within an IRA account?

Fidelity is showing a “debit from unsettled activity” on mine, although the cash account balance hasn’t changed. Not sure if I remember correctly, but last time, I think the funds weren’t withdrawn from my settlement fund until the issue date. I don’t know what other brokers do.

Intersting, thanks Jenny. May I ask whether that’s for an IRA account?

Yes, mine’s in a rollover IRA.

Yes, that’s how Fidelity handles it.

I use Schwab, Vanguard, and Fidelity. I sell enough money market fund units on the morning of the setllement date, such as 10/31, to cover the cost of the buy/trade at the auction. However, I do get emials from them reminding that there is insufficient money to cover the trade. To the best of my understanding, no money changes hand until the settlement date.

Hmmm, my IRA’s with Etrade, and I have to sell sufficient shares of the money market fund I keep any cash in and have that settle before I can even place the order, and the cash for today’s TIPS purchase has already been taken out of the pathetic 0.01% interest rate automatic sweep bank account. Sounds like it might be time to move my IRA accounts elsewhere if that’s not some limitation of IRA accounts. Thanks!

I just looked up 7 day yield on the money market funds that I use to hold cash for the auctions:

Schwab SWVXX/SNAXX 5.2455/5.3955%

Fidelity FZDXX 5.18%

Vanguard VMRXX 5.3%

Yes, I keep my cash in VMRXX in my Etrade account, but I can’t use it to place any orders until I first sell the necessary shares of VMRXX and wait until the proceeds settle that evening into the automatic 0.01% sweep bank account. Think I better give them a call and whine tomorrow – seems like they’re basically stealing use of my funds for 16 days! I do have a non-retirement account at Fidelity and their automatic sweep account pays a decent rate and doesn’t require me to do orders to buy more shares for every dividend payment, etc. If their IRAs work the same way, sounds much better. Thanks.

TD Ameritrade deducted the funds from my account on the auction date. That surprised me too. This leave me with a negative margin account balance and TDA will take 13.25% interest until I restore a positive balance! This seems ridiculous.

I also have a non-retirement TD Ameritrade account and find their Account Balances screen pretty confusing. I know that it often shows a negative negative value under “Margin balance” while there are pending settlements but still zero under “Margin balance subject to interest” and I’ve never been charge any margin interest. Are both negative in your case?

Yes, both were negative as of this morning. Subsequently, I sold sufficient securities to cover the transaction amount. Now both margin and margin subject to interest are zero.

Weird, since I doubt those funds get transferred to Treasury until the issue/settlement date, I’m surprised that’s even legal.

On my Etrade account, this morning, unlike yesterday evening, my Balances screen does how the full purchase cost still in the insulting 0.01% rate sweep bank account, so I gather it’s still earning at least that token interest from now to the 31st. I called them nonetheless to ask about changing my sweep account to a higher yielding money market alternative described on their website but was told that it was no longer possible to change the sweep option. So I decided to transfer both accounts to Fidelity after they assured me such transactions would work the same way as in my non-retirement account with them and offered to reimburse me the account transfer fees charge by Etrade. The two customer service experiences were like night and day!

Saw this thread on Twitter.

https://x.com/beth_stanton/status/1714321628383908134?s=20

Sure, I could buy that seasonality could be a factor, and generally the April TIPS could have a higher real yield because of the “December dip” in non-seasonally adjusted inflation. Usually that is maybe 5 basis points, at the most. But this was a pretty big spread. And it might indicate that the December reopening auction could get a nice yield pop.

Hi David. Thanks for another great and timely article! I was a buyer of TIPS at auction today. Like you, was surprised and disappointed about the effective yield. But as you point out, it’s still a really nice yield compared to recent 15 years so I’m good with it.

Re: your great question as to why the yield is lower than market, I have a thought: the Fed stepped in to lower Treasury financing costs. I am a believer (and as you know I’ve written on Seeking Alpha, which you so graciously referenced elsewhere on your excellent site) that the Fed and Treasury will collaborate to repeat the 1940’s playbook of monetizing and inflating away the debt. Heck, what better setup than having former Fed head Janet Yellen as Treasury Secretary. This buyer of last resort certainly has the wherewithal to move auction rates. I googled the Fed buying TIPS and found this interesting article – “The Fed Buys More TIPS than Treasuries Issues.” It’s a bit older but perhaps still valid:

https://manhattan.institute/article/fed-buys-more-tips-than-treasury-issues#:~:text=When%20many%20economists%20advocated%20for,market%20price%20for%20inflation%20protection.

Happy TIPS investing!

Hello Ralph! I did see today, though, that the Fed bought zero of this new issue. Well, that was posted on Twitter by reliable sources. In theory, the Fed should be rolling off its TIPS investments, which simply means they don’t buy more when a set matures. There is no doubt that the Fed forced real yields deeply negative. Now, without Fed disruption, yields are climbing ever higher.

Ahh, so much for my theory! Nice sleuthing to find that nugget David.

You don’t need to depend on Twitter. Down near the bottom of the auction results in the section on amounts tendered and accepted you find a line labeled “SOMA” which stands for “The dollar amount of System Open Market Account (SOMA) bids awarded in the auction.” It was zero at this auction.

Historically, the beauty of the noncompetitive bid for individual investors was the chance to avoid the brokerage commissions and spreads in the secondary market. Some of you fellow geezers remember what our full-service brokers used to charge for a trade back in the day. Since many brokers now offer commission-free trading on secondary market Treasurys, the biggest reason to participate in the auction is gone. One still avoids the spread, but that’s peanuts for TIPS, a few basis points for the spread and a couple more for buying small lots.

Further down the press release for today’s results, one can see that the bulk of the demand was from the indirect bidders. These are big players like sovereign wealth funds, hedge funds, and others who have to use an authorized dealer or direct bidder to submit their bid. They’re likely still having to pay commissions on the secondary market. An investment bank isn’t going to buy $100m in the secondary market for you for free, Mr. Moneybags. And the spread may be peanuts to us on our small lot trades, but with $100m principal, it gets to be a big number. So the indirect bidders tend to bid aggressively at the auction to make sure their allotment gets filled. The press release says 50% of the bonds auctioned today went for 2.32% – 2.355%. The noncompetitive bidders got the best price of 2.44%.

Great information, thanks.

Hi T Lee,

FYI and just to be clear on how these “clearing bid” type auctions work, all of the successful bidders received the 2.44 % rate, even if they bid and would have accepted a lower number.

David X

Yes, thank you. I see I didn’t make that clear.

Definitely disappointing. But in the big picture of things, a few basis points here and there won’t make much of a difference. I’m glad to have bought today.

Such an educating blog. Very detailed analysis. We learnt so much from this blog about TIPS. Thank you David for helping TIPS investors make INFORMED decisions whenever they decide to buy or sell TIPS.

In a yo yo market like this with outsized interest rate movements, GET/FORGET approach is easier on the eyes when the term is 5 years or less. So this TIPS is a winner no matter what!

Secondary market issues mostly have very low coupon rates and decent amount of inflation adjustments – so it is hard to compare with today’s issue which comes with highest coupon in recent history and at par! Its like comparing apples to oranges!

I bought this most recent TIPS (91282CJH5) on Fidelity secondary market on 11/30/23 for 101.164. It was there to buy, along with the rest of the TIPS that have lower coupons and high inflation adjusted principles. I don’t know when 91282CJH5 became available on the Fidelity secondary market. It hurt to pay 101.164, but TIPS yields have been decreasing. I think my YTM was only about 2%. I don’t know if I’ll buy the next issue. I worry that I’ll buy, and then coupons for subsequent issues will increase. However, I bought this issue (91282CJH5) because I’m worried that coupon rates may have reached their peak, and may decrease in the future. I’m not going “all in” on either possibility.

What a disapointing and confusing auction today.

I was going to buy 191282cgw5 on secondary market yesterday (was trading>2.55% ) but when I saw the 2.57% real yield posted on the Treasury site last nite, I changed to an auction purchase anticipating a higher yield today.

Surprisingly, cgw5 (a little shorter duration and lower coupon of 1.25%) is still >5.5% on schwab today.

Does the higher coupon of 2 3/8% (shorter bond “duration” with earlier return of principal) and the 6 month shorter maturity expain such a difference in real yields? Given my limited sophistication, seems mispriced.

Thank you Mr. Enna for sharing your knowledge and education. Terrific site, and I look forward to every post.

Dale

In general, the real yield of a 4 1/2-year TIPS and a 5-year TIPS should be closely aligned, even if the coupon rate is different. The inflation accrual of that that GW5 TIPS isn’t high enough to be a factor either. My only though is that very large investors (like hedge funds, pension funds, etc) wanted to load up on this new issue.

Not sure how you arrived at the $10.37 figure for accrued interest under “Investment Cost” for a $10,000 purchase?

That was a quick calculation, and I think the number should be around $10.41?

Technically, it should be accrued principal $10.0225 x unadjusted interest ($1.03825) = $10.40586

I mess this one up every time. It is now fixed.

I just use the “Adjusted Accrued Interest per $1,000” figure from the Treasury Auction Results, which matches your recalculated value (rounded). Hopefully they get it right 😉

I will never buy from auction again. What a ripoff.

I’m with you. I’ll just poke around on the secondary market if I want any more TIPS.

but when you buy an older TIPS on the secondary market you could get a much higher adjusted principal and then you would be more at risk if there is deflation than if you buy at auction.

Chris. I do not buy TIPS with inflation adjusted principals that are too much greater than one, for the reasons you describe above. I do not want to incur that risk. Inflation rates less than zero seem unlikely over the next 5 years, but they are within the realm of possibility. I’m feeling rather risk averse lately.

Yes, I’m actually really fluxommed on whether to increase my duration or not. Mr. Powell and the Fed’s history of “transitory” (the word will stay in infamy) mistake gives me pause to move away from my 4-week T-Bill refresh. Perhaps David can help tell us more about how this all pans out.

I have kept my year-plus-long rollover of staggered 13- and 26-week Treasurys, and I need that as my main emergency fund. But I also have been working hard to extend duration of TIPS, out to year 2043. I have put my attention on the years 2033 and beyond, and hope to fill in 2034 in January. Was that the right decision? It would have worked better if I had waited this current surge in rates, which could now go higher or possibly fall off a cliff. But with a TIPS held to maturity, I know my return will exceed inflation.

While I look forward to David’s take, let me share my take. As we all know, a Fed interest rate increase has, more or less, an immediate impact on the short end of the yield curve. It takes a while for it to impact the long end. I believe that we are now seeing that impact on the long end. I have waited for 5% on US treasury bonds for a long long time. For the first time, I have highlighted the dates for Treasury bond auctions on the printed copy of the tresuries schedule. In short, I will be adding duration. However, if some black swan or an unexptected recession happens then all bets are off.

Be careful what you wish for. The talking heads are saying long term rates could be double digits in a few years. If that is the case, then that 5% LT bond will get crushed.

Understandable. There can be all sorts of good predictions, using perfectly rational criteria, such as David’s on this blog, but then perhaps, on the day of a TIPS auction, or the day before, the institutional bond market’s lizard brain thinks, “Ooh, it looks like inflation will tick up [or down] and there’s an entirely different–although, really now, not super-dramatic–outcome. In the secondary market you know exactly what you’re going to get before you click, or decide not to click, “Submit.”

Does is this lower your expectations for the new I-bond fixed rate to be released in November?

No, because this yield of 2.44% is 154 basis points higher than the current fixed rate of 0.9% on the I Bond. That fixed rate should be higher. I have recently focusing on a fixed rate of 1.2% as the floor. We will see.