The US Treasury announced this morning that it will reopen CUSIP 912828H45, creating a 9-Year 10-Month Treasury Inflation-Protected Security with a coupon rate of 0.250%.

This TIPS initially auctioned on Jan. 22 with a real yield (after inflation) to maturity of 0.315%. Here’s what we can say about next week’s auction, knowing that things can change in a week:

- This TIPS is trading this morning with a real yield of 0.34%, according to Bloomberg’s Current Yields chart. That means it is trading at a discounted price of about $99.10 per $100 of value.

- It closed yesterday with a real yield of 0.367% and a price of about $98.90 per $100, according to the Wall Street Journal’s Closing Prices chart.

- The US Treasury estimates a full-term 10-year TIPS would have yielded 0.39% at the close yesterday.

One interesting side note to this TIPS is that it currently carries a March 31 inflation index of 0.98686, meaning that it has no accrued inflation. In fact, buyers at the January auction have seen their principal balance decline by about 1.4%. This TIPS won’t rise to par until we see inflation rise in non-seasonally adjusted CPI-U. In return, I would expect buyers to expect a higher yield to compensate for the deflationary trend.

10-year inflation breakeven rate. At yesterday’s close, a 10-year nominal Treasury was yielding 2.11%, and that creates a 10-year inflation breakeven rate of 1.72%, which is low by historic standards, and indicates this TIPS is a good buy versus a nominal Treasury. If inflation averages more than 1.72% over 10 years, this TIPS will outperform a nominal Treasury.

Is a real yield of 0.35% too low? Personally, I’d say ‘yes’ and I have no interest in this issue as an investor. I’d get more interested as real yields rise to about 1%, which is perfectly possible over the next year (or … not.) However, if you need to fill a 2025 spot on a long-term TIPS ladder, this one could serve the purpose. But note that it will be reopened again in May.

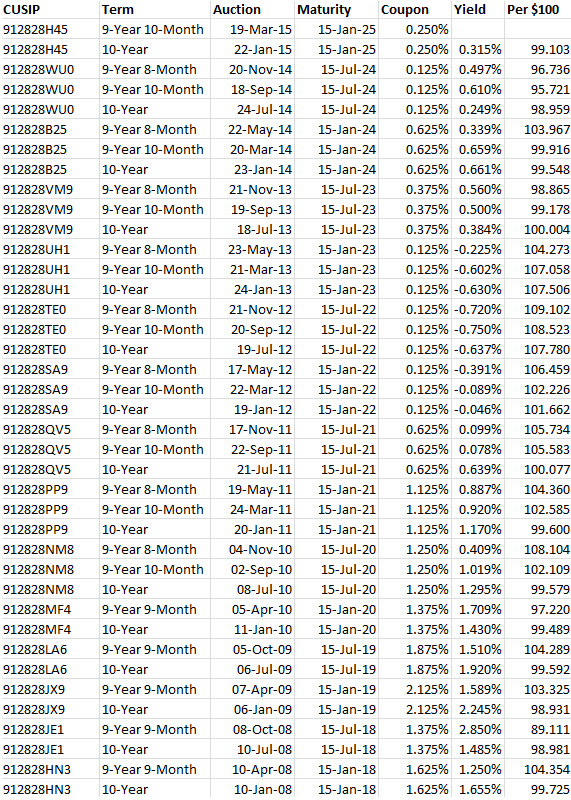

As recently as September 2014, we saw a 10-year TIPS reopening auction go off at a yield of 0.61%, much more attractive than the result that looks likely next week. Here is a history of all 9- to 10-year TIPS auctions since 2008:

In today’s case, this looks about right — 0.39% yesterday for a full-term 10-year, versus 0.35% mid-morning on a day when TIPS yields were declining. This TIPS ended up closing at 0.358% and the Treasury stuck with 0.39% as the full-term number. I tend to trust the Treasury number as a piece of evidence to consider.

Any thoughts on why there is frequently such a huge disparity between the Daily Treasury Real Yield Curve Rates at treasury.gov and the Bloomberg data for actual trades? I realize there may be a slight difference because the Treasury’s are computed on a theoretical basis versus (no spread) but there is still quite a difference.