The Treasury will announce later this morning that it will be offering a new 5-year Treasury Inflation-Protected Security at auction on Thursday, April 23. This will be CUSIP 912828K33. Update: Here is the announcement.

The market for 4- to 5-year TIPS has changed dramatically since the Treasury’s last auction of this term, on Dec. 18, 2014, when a a 4-year, 4-month TIPS auctioned with a yield of 0.395%, highest in 4 1/2 years.

Today we are looking at a yield in the range of -0.26%, a decline of 65 basis points since December. But that’s still well above the record low of -1.496% for the auction of a 4-year, 4-month TIPS on Dec. 20, 2012.

Because the lowest-possible coupon rate for this TIPS is 0.125%, buyers will likely be paying up at next Thursday’s auction, somewhere around $101.92 for $100 of value to produce a yield to maturity of -0.26%. (A lot can change in a week, of course.)

Inflation breakeven rate. With the 5-year Treasury currently yielding about 1.33%, this sets up an inflation breakeven rate of 1.59% for this TIPS, meaning that it will outperform a 5-year nominal Treasury if inflation averages more than 1.59% over the next 5 years. Inflation has been running at 0.0% over the last 12 months.

Alternatives. The 5-year term sets up good comparisons with other ultra-safe investments. For example, you can buy an I Bond today and be assured that you will earn at least the inflation rate over the next five years. That return will be 0.26% better than the return of this TIPS, and so an I Bond – as weak as it seems right now – is a better investment.

Another alternative is 5-year insured bank CDs, which pay 2.00% to 2.25% right now at several banks. The 2.25% return sets up an inflation breakeven rate of 2.51% for this TIPS. If you don’t believe inflation will average higher than 2.51% over the next 5 years, the bank CD is a better investment.

Why buy it? I like the 5-year term, and I was a buyer last December when the yield hit a favorable 0.395%. But next Thursday’s auction will be interesting mainly to big-money investors like central banks, pension funds and hedge funds — where small-dollar alternatives make no sense. I suspect many small investors will pass and look for better alternatives.

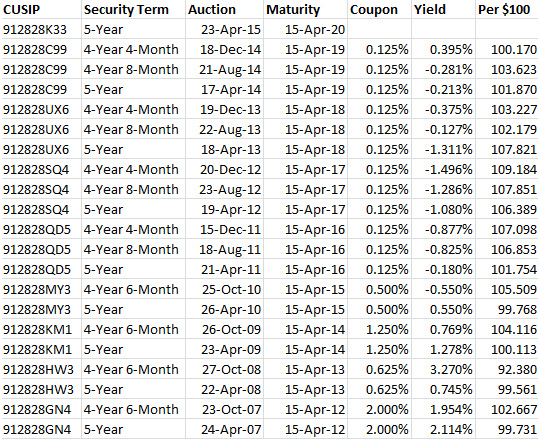

Here is the history of all 4- to 5-year TIPS auctions since 2007:

Len, foreign central banks are in the group called ‘indirect bidders’ and can make up about half the demand the demand for TIPS at auction. The Treasury site says this:

An “Indirect Bidder” is referred to on the auction results press release as customers placing competitive bids through a direct submitter, including Foreign and International Monetary Authorities placing bids through the Federal Reserve Bank of New York.

Still, since central banks in Europe and Asia are busy buying up their own bonds in quantitative easing programs, so you’d think there would be less demand for TIPS and yields would be rising. But they are still very attractive when compared to ultra-low yields on European bonds.

We may differ on some points, but as usual your analysis is always useful. Some might consider splitting their investment between CDs and 5 year TIPs in proportion to their outlook for inflation. I recall reading this is how some of the “big guns” approach it. Wasn’t aware foreign banks were large investors in TIPS. Any source?

Thank you for the analysis