The Consumer Price Index for All Urban Consumers (CPI-U) increased 0.3% in June on a seasonally adjusted basis, the U.S. Bureau of Labor Statistics reported today. But over the last 12 months, overall inflation rose just 0.1%.

While higher gasoline prices (up 3.4% in the month) were a big factor in June’s increase, inflation also perked up in other sectors: Food at home, up 0.4%; shelter, up 0.3%; and transportation services, up 0.4%. Inflation was moderated by declines in apparel prices, down 0.1%, and used cars and trucks, down 0.4%.

Core inflation – which strips out food and energy – was up 0.2% in June and 1.8% over the last 12 months, indicating that inflation remains in the ‘moderate’ zone.

Holders of Treasury Inflation-Protected Securities and I Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust the principal balance of TIPS and set the future interest rate on I Bonds. In June, the CPI-U inflation index rose to 238.638, up 0.35% from May’s number.

This is significant. I Bonds purchased today carry a fixed rate of 0.0% and an annualized inflation-adjusted rate of -1.60%, resulting in a composite rate of 0.0%, the lowest it can go. But the inflation-adjusted rate will be re-set November 1, based on non-seasonally adjusted inflation from March to September. So far, from March to June, inflation has increased 1.06%, which would result in an annualized rate of 2.12%. And we have three months to go. I Bonds could be a buy in November and December.

I have updated my Tracking Inflation and I Bonds page to reflect these new numbers.

I have updated my Tracking Inflation and I Bonds page to reflect these new numbers.

The news is also better for holders of TIPS, who have seen 12-month inflation rates dip to zero or below zero since January 2015. That is turning around. Today’s 0.35% inflation number will be added to TIPS balances through August 31. That is on top of the 0.51% increase in May and 0.20% hike in April. At least the trend is finally up.

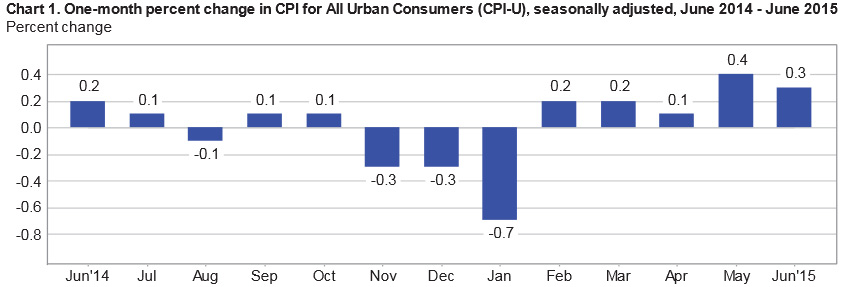

Here is the overall trend for seasonally-adjusted inflation over the last 12 months, clearly showing the upward movement, primarily caused by rising gasoline prices:

“Of course, that totally depends on how closely one’s personal inflation rate matches the CPI-U”

Actually, that is a thoroughly minor point trumpeted by the Wall St. charlatans who would rather make a big fat commission selling you something that they make a big fat commission on. There’s no money for them in TIPS, so they come up with shockingly stupid arguments against them. (What’s even more shocking is that people are taken in.) Even for me, a fairly elderly person with well-above average income, probably the worst case scenario as far as personal CPI vs official CPI, the official CPI probably has a 90% correlation with my personal CPI. Don’t get me wrong, there are a lot of good reasons why TIPS/I-Bonds might not be right for some people, but lack of correlation with CPI isn’t one of them. Suggestion: stop watching CNBC, and think for yourself. You are smarter than them.

TIPS are nothing more than a virtually riskless defensive method to preserve purchasing power. Of course, that totally depends on how closely one’s personal inflation rate matches the CPI-U.

So what? People who bought umbrellas last week expecting rain that never came also wasted their money. If it had rained, they’d look like geniuses. What really matters is ex ante. TIPS are simply nominal T-Bills/bonds that come with an insurance policy on inflation. They are nothing more than that. The insurance “premium” is the difference between the TIPS coupon and the coupon on a nominal bond of equivalent duration. All else being equal, when the inflation premium is under-priced, buy TIPS instead of nominal T-Bonds; when the premium is over-priced, buy nominals. But let’s not lose the forest for the trees. ALL Treasury obligations are grossly mis-priced today, making whatever minor mis-pricing that exists between indexed and nominal debt today seem trivial. Maybe the best strategy today is to buy neither (which I think has been your recommendation lately). Since their debut in 1997/1998, there have been only two periods when TIPS were clearly mis-priced relative to nominals, making them a screaming buy. The first time was in 1998 when, nobody knew what TIPS were; the second was in 2008, when Lehmann dumped its TIP holdings on an illiquid market. Hopefully, we will have such opportunities again. At other times, it really is a toss-up. I don’t see a rate increase by the Fed as making much difference either way. This is simply not the golden age for savers.

But MGK, inflation has been running below expectations. If you bought a TIPS with a breakeven rate of 2.0% and inflation runs at 0.1% over 12 months, that investment didn’t work out for you versus a nominal Treasury. If you bought a TIPS with a yield negative to inflation and inflation runs at 0.1%, you are getting, at best, zero return, and possibly less than zero. People who bought TIPS with negative yields were absolutely expecting inflation. And they didn’t get it. So far, anyway.

I don’t think so. Fisher equation. Nominals outperform TIPS only when inflation runs below expectations, and vice versa. The problem I think you are alluding to is that real rates are very low now, but that is as “bad” for nominals and CDs as it is for TIPS, The Fed raising nominal rates probably would raise real rates too, but the interesting question is whether that would actually be good for TIPs. Many would view raising rates now as potentially deflationary (especially if done prematurely), making nominals and CDs possibly more attractive than TIPS, not less so. But, maybe not. Back to the Fisher equation. If investors view the Feds move as deflationary ex ante, the coupon on TIPS would actually have to higher than that of nominals, to make up for the deflation adjustment. Again, a wash. Would conservative investors (TIPS, T-Bonds CDs) be better off if real rates were higher? Yes. Does that make TIPS more or less attractive relative to the other safe alternatives. No. There is no inflation “inflation bonus” for TIPS, unless the CPI rises above the ex-ante breakeven CPI. And, that’s the same “bonus” your family gets when they collect on your life insurance policy. Not much to cheer about indeed.

MGK, TIPS and I Bonds do suffer as an ‘attractive’ investment when inflation runs at zero percent or below. Nominal Treasuries are superior, since they pay a real return under those circumstances. I don’t cheer for higher inflation, but we need enough to get the Fed to begin raising short-term rates to levels at or above inflation. Then we could see a bonus to inflation with TIPS and I Bonds.

TIPS holders should be neutral about about inflation, shouldn’t they? So it’s neither good news nor bad news for TIPS holders, since purchasing power stays the same regardless of the inflation rate. If anything, they are worse off, because the higher inflation “coupon” is taxed, even though there is no real gain to the holder.