By David Enna, Tipswatch.com

One of the most important inflation reports of the year is coming up Tuesday at 8:30 a.m., when the Bureau of Labor Statistics releases its March inflation report. That report carries a lot of weight, because:

- It will set the I Bond’s new inflation-adjusted variable rate, which looks likely to rise to 2.5% or higher (annualized), maybe even 2.8% or higher. That rate — which will go into effect for newly purchased I Bonds on May 1 and eventually for all I Bonds — is based on official U.S. inflation from September 2020 to March 2021. Through February, inflation had increased 1.05%, which translates to an I Bond variable rate of 2.10%. If non-seasonably adjusted inflation comes in at — let’s say a conservative 0.3% — The I Bond’s variable rate would rise to 2.7%, versus the current 1.68%.

- The consensus estimate for seasonally adjusted all-items inflation in March is 0.5%, following a rise of 0.4% in February. That would likely push year-over-year U.S. inflation up to about 2.5%, the highest rate since January 2020.

- Core inflation, which strips out food and energy, is projected to increase 0.2% for the month, pushing the year-over-year number up to 1.6%, from last month’s 1.3%. If core inflation comes in higher than 0.2%, it will be signalling a stronger inflationary trend.

None of this is surprising. Remember that inflation in March 2021 is being measured against inflation in pandemic-stricken March 2020, which declined 0.2% that month and declined again 0.7% in April 2020. So it’s been looking likely that we would see a surge in U.S. inflation in spring 2021, reflecting the effects of a year of government stimulus and economic recovery.

This is the theme of a report issued last week by the investment firm PIMCO, “Dealing With an Inflation Head Fake,” written by Joachim Fels and Andrew Balls. Their premise is that although the U.S. and global economies will be recovering strongly this year, the jump in inflation will be temporary. From the report:

Investors should be prepared for an inflation “head fake” and look to maintain portfolio flexibility and liquidity to be able to respond to events in what is likely to be a difficult and volatile investment environment. …

While there is a lot of potential for medium-term economic scarring, there is likely to be a strong cyclical boom this year. … As a consequence, following a 3.5% contraction in 2020, we now forecast world GDP growth (at current exchange rates) in excess of 6% in 2021, up from 5% previously. …

Over the next several months, a combination of base effects, recent increases in energy prices, and price adjustments in sectors where activity ramps up is likely to push year-over-year inflation rates significantly higher. However, we forecast that much of this rise will reverse later this year.

Here is PIMCO’s outlook for U.S. inflation through 2022, showing an increase to 3.5% in all-items inflation in coming months, before both all-times and core inflation begin settling down to about 2.0% year over year:

Will this be a ‘head fake’?

I don’t claim to know. Inflation is incredibly hard to predict beyond a month or two into the future, and even then, something unexpected can happen, such as a hurricane ripping through Texas and knocking out oil refineries.

Inflation has remained stubbornly low over the last decade, much lower than the bond market or economic experts predicted. The result is that U.S. policymakers and market-makers are complacent about inflation: Even though they can see it rising, they aren’t concerned.

For a perspective on the wanderings of U.S. inflation, take a look at this historical chart of monthly year-over-year inflation, going back to 1948:

It is true that U.S. inflation has been relatively mild for decades, all the way back to October 1990, when it hit 6.4%. A true “head fake” happened in July 2008, when inflation soared briefly to 5.6% before plummeting to -2.1% a year later in July 2009. That steep drop, however, came during the century’s worst economic recession.

So, where are we headed?

Here are some thoughts from inflation watcher Michael Ashton, who writes on inflation in his E-piphany blog:

There is a growing list of categories of prices which are seeing abnormal price pressures. … There has become an acute shortage of semiconductor chips, which has impacted automobile production (and will that increase prices for what is available?). There is a shortage of shipping containers, causing widespread increases in freight costs affecting a wide variety of goods. Packaging materials, which are also a part of the price of a great many goods, are also shooting higher in price. Worker shortages at various skill levels were reported in the most-recent Beige Book. There is a shortage of Uber and Lyft drivers.

Importantly, we should add to these shortages a growing shortage of housing. The inventory of homes available for sale just hit an all-time low … And, as a result, the increase in the median sales price of existing homes just reached an all-time high spread over core CPI. …

But it might also be the case that the current rapid escalation of home prices is the market’s attempt to get the real value of the housing stock to reflect the rapidly increasing value of the money stock. If that’s the case, then it also suggests that median wages probably will eventually follow.

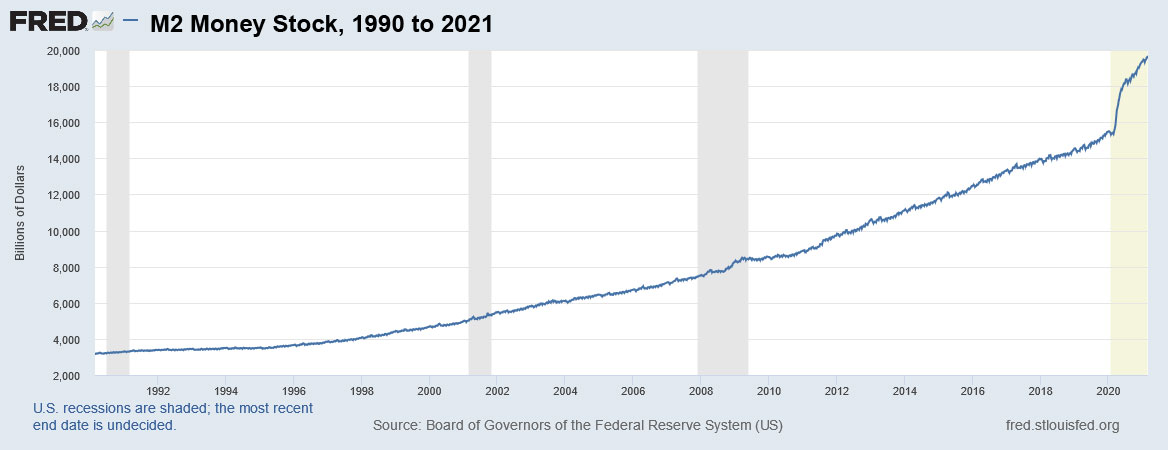

Consider this about the U.S. money supply: the M2 money stock measurement has increased about 26% over the last year, from about $15.5 trillion in January 2020 to $19.6 trillion in March 2021. That’s a sharp difference from the trend we’ve seen during all the years of relatively mind inflation since 1990:

Maybe money supply doesn’t matter, and doesn’t influence inflation. But this chart is strong evidence we have entered a “new era.” On the flip side of this, the value of the U.S. dollar has declined about 7% over the the last year, as shown in this chart:

Increasing consumer demand, supply shortages, possible labor shortages, a soaring money supply, a weaker U.S. dollar: These factors all will contribute to rising inflation over the short term. Will that trend last beyond 2021 or just be a “head fake”?

I don’t know the answer, but think staying prepared for inflation is a wise investment move.

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Housing will be particularly interesting to watch. There is very substantial pent-up demand from even before the pandemic. Building material prices have risen dramatically, and regulatory regimes have added substantial costs to new construction (eg NY scaffolding law). If Biden eggs on this trifecta of price stimulants by providing first-time homebuyers with those promised $15k down payments, it’s hard to see how housing prices don’t go parabolic. Just one man’s opinion here.

Thanks for the analysis on inflation always appreciate your opinion. I am going in on the I bonds after April. The “I’s” have it over any CD that I can see.