By David Enna, Tipswatch.com

U.S. inflation surged 0.6% in March, the Bureau of Labor Statistics reported today, and provided the final piece of data to determine the new variable rate for U.S. Series I Savings Bonds: a whopping 3.54%, annualized, for purchases after April 30 and eventually for all I Bonds.

The I Bond’s new variable rate is based on a six-month inflation rate, in this case from September 2020 to March 2021. Non-seasonally adjusted inflation increased 1.77% over that period, which translates to a new six-month variable rate of 3.54%, annualized, for all I Bonds. That is a huge increase over the current rate of 1.68%.

May 3 Update: I Bond’s fixed rate holds at 0.0%; composite rate soars to 3.54%

April 15 Update: I Bond dilemma: Buy in April, buy in May, or wait until later?

In today’s report, the BLS set the March inflation index at 264.877, an increase of 0.71% over the February number. It’s been a strange six months, with non-seasonally adjusted inflation rising only 0.06% in the first three months, then surging 1.69% in the last three months.

Here are the relevant numbers (you can see historical data on this page, which I update monthly):

What this means

Obviously, we are going to see intense investor interest in I Bonds over the next few months, with the new composite interest rate — combined with a 0.0% fixed rate — likely to be 3.54% (annualized) for six months. That is the highest rate reset since May 2011, when the inflation-adjusted variable rate surged to 4.6%.

For current I Bonds. If you already bought your I Bond allocation in 2021 (as I did in January), you will be earning 1.68% for six months and then 3.54% for six months, for a one-year rate of 2.61%, triple the current earnings of any other very safe one-year investment.

Investments in I Bonds are limited to $10,000 per person per calendar year, along with the possibility of purchasing $5,000 in paper I Bonds in lieu of a federal income tax refund.

All I Bonds, no matter when they were purchased, will get the 3.54% variable rate for six months. When that rate kicks in depends on the month you purchased the I Bond. Remember, when you purchase an I Bond, you always get the current composite rate for six months, before the next reset takes effect. Here is that schedule:

| Issue month of your bond | New rates take effect |

|---|---|

| January | January 1 / July 1 |

| February | February 1 / August 1 |

| March | March 1 / September 1 |

| April | April 1 / October 1 |

| May | May 1 / November 1 |

| June | June 1 / December 1 |

| July | July 1 / January 1 |

| August | August 1 / February 1 |

| September | September 1 / March 1 |

| October | October 1 / April 1 |

| November | November 1 / May 1 |

| December | December 1 / June 1 |

Purchases after May 1. If you wait until May 1 to purchase I Bonds, you can be assured of earning 3.54% for six months, and then a-yet-to-be determined rate for six months. But the worst you could do is 1.77% over the year, even if the next variable rate resets to 0.0%.

I suspect a lot of investors who haven’t yet purchased I Bonds in 2021 will now wait until after May 1, locking in that higher variable rate for the first six months.

Let’s remember the reason we invested in I Bonds: To protect against unexpectedly high inflation. In March 2021, we got exactly that. I will be writing more on this topic in a few days after I let today’s news settle in.

The March inflation report

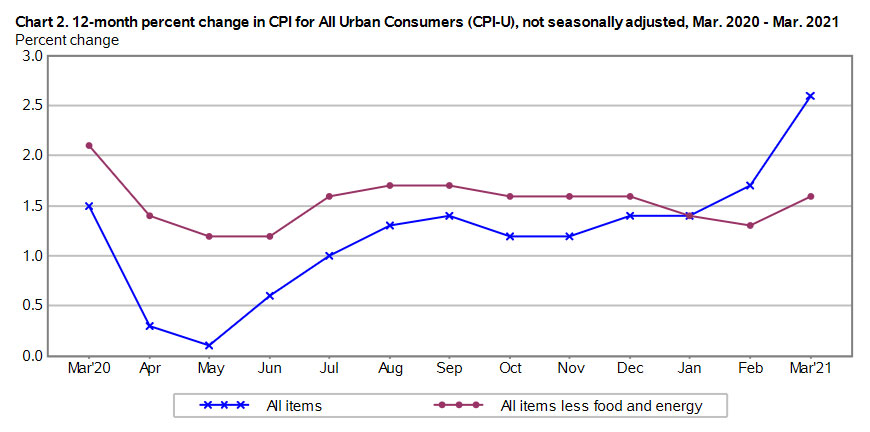

The Consumer Price Index for All Urban Consumers increased 0.6% in March on a seasonally adjusted basis, the BLS reported. This 1-month increase was the largest rise since a 0.6% increase in August 2012. Over the last 12 months, the all-items index increased 2.6%.

Economists were expecting higher inflation in March, based on very weak numbers in pandemic-stricken March 2020. But actual inflation for the all-items index was higher than the consensus, for both the month and year-over year.

Core inflation, which removes food and energy, came in at 0.3% for the month, also higher than the consensus estimate. The year-over-year number for core inflation matched the target of 1.6%.

The BLS noted that higher gasoline prices again were a key factor in March’s inflation increase, rising 9.1% for the month and accounting for nearly half of the seasonally adjusted increase in the all-items index. Other items of interest:

- Food prices increased a moderate 0.1% in the month, but are up 3.5% over the last year.

- The costs of shelter increased 0.3%, but are up only 1.7% over the year. (Rents have been held down by eviction moratoriums and other measures, which may end soon.)

- Prices for used cars and trucks increased 0.5% and are up 9.4% over the year.

- Apparel prices fell 0.3% and are down 2.5% over the year.

- The motor vehicle insurance index increased for the third consecutive month, rising 3.3 percent in March.

- The index for medical care services rose 0.1% for the month and is up 2.7% for the year.

Here is the overall trend for both all-items and core inflation over the last year, showing the dramatic rise in all-items inflation (primarily caused by rising gas prices) and the relatively stable path for core inflation:

What this means for TIPS

As with I Bonds, non-seasonally adjusted inflation is the key number for Treasury Inflation-Protected Securities, setting future adjustments of principal balances for TIPS. March’s increase of 0.71% in non-seasonally adjusted inflation means that principal balances for all TIPS will rise 0.71% in May, following a 0.55% increase in March.

Here are the new May Inflation Indexes for all TIPS.

What this means for future interest rates

The Federal Reserve certainly saw this coming: U.S. inflation was going to surge in the spring of 2021 when compared to the very weak numbers of spring 2020, when much of the economy was shut down. I don’t think today’s report alone will have any effect on the Fed’s policy. It will need to see many months of surging inflation to change course.

So for now, expect the Fed to continue holding short-term interest rates near zero, and to continue its current program of bond-buying, with any tapering or increases that could jolt the market.

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

David…

Thanks for your great articles on IBonds. I was fortunate to purchase $60,000 worth back in 2001 for a 3.0 fixed rate. It seems like a great investment even today as a method of inflation protection. Why did the Treasury decide to limit purchases to $10,000 per person years ago?

I bought some of those early I Bonds, too, but I didn’t go all in with $30,000 (credit card purchases were allowed, too). That $30,000 limit was dropped to $5,000 in January 2008, and then raised to the current limit of $10,000 in January 2012. So we have gone nine years without an increase.

David

Appropriate to say overthink, and yes, I don’t want to overcomplicate decision-making. However, I purchased my 2021 bond early in the year. With penalties, on net, if you redeem it and buy Spring allotment does it produce better yield–or if its even allowed? It’s not big money but it’s only a 15-20 minute effort.

Thanks

Brad

First of all, if you bought your allotment in 2021, you are done for the year. You can’t buy more. And really, truly … you wouldn’t want to do it anyway, unless the fixed rate somehow jumps above 0.0%. You will be getting that 3.54% variable rate for a full six months. For example, I bought my full allotment in January, so I will get 1.68% for six months and then beginning in July I will get the 3.54% rate, which will apply for six months to all I Bonds in existence, since none have yet reached full maturity.

I am hearing a lot of economists and analysts of the opinion that this current inflation will be relatively short term and there is still little threat of long term year over year inflation at these levels. In light of that and the fact that the chance of even a .1% fixed term component is almost nil, I am thinking of buying my allotment or at least half at 1.68%. This is still an attractive rate at least in recent memory and I am not really that concerned whether I get the 3.54% now or in 6 months.

Does this thinking make sense?

I will be writing about this later this week, and if you are considering this a long-term investment, I don’t think it matters much. A few months ago, 1.68% annualized looked very attractive, and now … geez … that 3.54% is tempting. You will get it if you buy now, or buy later. I Bond investors are famous for “over-thinking” (me included, obviously) but the main point is to buy up to the limit every year.

On the other hand, if you consider this short-term money, to be redeemed a year out, then maybe waiting toward the end of May makes sense. I need to dive into the numbers.

One quick point: If you buy $10,000 of I Bonds in April or May, you will earn $177 for a six-month period at 3.54%. That is equal to 17+ years of 0.1% fixed rate.

You say “Economists were expecting higher inflation in March, based on very weak numbers in pandemic-stricken March 2020.” Actually current inflation is independent of past numbers. It is simply a reflection of supply and demand for products. In other words, there is no such thing as supply and demand for inflation. One cannot have pent-up demand for inflation. This may be a subtle point, but inflation is not a commodity.

The current CPI raised my 3.0% fixed rate I-bonds to 6.54% overall yield. Not bad for a zero risk tax-deferred investment, and considering the best 5 year CDs are currently paying .60%. Back in the day we could buy $30,000 in a year. Treasury saw this could be a problem for them (as it is now) and reduced the maximum to $10,000 a year ($5,000 more if you want to play around with your IRS return, which I don’t want to).

I-bonds have an archaic structure, e.g. getting a full month’s interest if you buy or sell the last day of the month. It’s like when in the old days you could open a bank accournt for $10 on the tenth of the month and earn from first, and get 5%. Try that nowadays. My guess is Treasury would like to get rid of I-bonds altogether, but they are stuck with this “economic inefficiency”, which we should all try to exploit to the maximum.

One reason you can be sure Treasury will not change its fixed rate in May from 0% will be the increased demand for I-bonds over the next few months. If they could do so legally, they would probably make the fixed-rate negative. Also they probably want to appear to be in lock-step with the Fed. My guess is the current CPI is not a blip, and we will see increasing inflation this year unless Covid cases start rising again.

I always enjoy your articles.

That is a stunner! While we love to get higher interest payments, no one loves to pay more for goods and services or to borrow money. Curious how long the Fed can keep the federal funds rate so low.

My theory is that the Fed will begin “signaling” that it is considering higher short-term interest rates or any tapering in its bond purchases. That signaling will go on for at least two months before it happens. It takes at least two months of “market-soothing” by the Fed to set the way for a rate increase. When it cuts rates, it does it with no warning, over a weekend, even.

David, any thoughts on the fixed rate reset on May 1?

My feeling is that there is less than a 0.1% chance that the Treasury will increase the fixed rate on May 1. I Bonds will already be very attractive and the real yield will be substantially higher than that of TIPS. But, “the Treasury does weird things” at times, so the chance is not zero, but very close to zero.