When inflation rises to the highest level in 31 years, that is significant.

By David Enna, Tipswatch.com

Attention, Federal Reserve: This 2021 surge in U.S. inflation is no longer looking “transitory.” It’s looking dangerous.

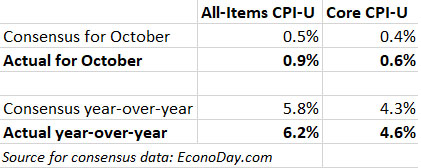

The Consumer Price Index for All Urban Consumers (CPI-U) increased 0.9% in October on a seasonally adjusted basis, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all-items index increased 6.2%, a three-decade high. Those results were well above economist expectations for an increase of 0.5% for the month and 5.8% year-over-year.

The annual increase of 6.2% was the largest, the BLS said, since the period ending November 1990, nearly 31 years ago. It noted that the surge in prices was “broad based,” hitting diverse areas like food, medical care, new and used cars, household furnishings and shelter.

Core inflation, which removes food and energy, rose 0.6% in October and 4.6% year of year. Those results also greatly exceeded consensus estimates of 0.4% for the month and 4.3% for the year.

As is usually the case when inflation surges, gasoline prices were a key cause. Gas prices were up 6.1% in October and are now up 49.6% in the last year. Even more troubling is the cost of food: The index for “food at home” increased 1.0% in October, and is now up 5.4% over the last year. The index for meats, poultry, fish, and eggs continued to rise sharply, increasing 1.7% following a 2.2% increase in September. The index for beef rose 3.1% over the month. Over the last decade, increases in food prices have remained relatively moderate. That is no longer the case.

The surge in prices was widespread across the economy:

- Natural gas prices increased 6.6% for the month, the largest monthly increase since March 2014.

- The index for new vehicles rose 1.4% in October and 9.8% year over year.

- Costs for used cars and trucks rose 2.5% in the month, restarting an upward trend after two months of declines.

- Shelter costs rose 0.5% for the month are are now up 3.5% year over year.

- The medical care index rose 0.5% for the month, the largest monthly increase since May 2020.

- One positive note: The index for alcoholic beverages decreased 0.2% for the month.

Here is the trend over the last year for both all-items and core inflation, showing a new surge higher in October after a few months of stability at an already high rate of inflation. The chart demonstrates that monthly inflation numbers are likely to continue very high through March 2022 because of low baseline numbers from early in 2021.

What this means for TIPS and I Bonds

Investors in Treasury Inflation-Protected Securities and Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances on TIPS and set future interest rates on I Bonds. For October, the BLS set the inflation index at 276.589, an increase of 0.83% over the September number.

For TIPS. The October inflation report means that principal balances for all TIPS will rise 0.83% in December, following increases of 0.21% in October and 0.27% in November. For the year ending in December, TIPS balances will have increased 6.2% to match inflation. Here are the December inflation indexes for all TIPS.

For I Bonds. The October report is the first in a six-month period (October to March) that will determine the I Bond’s new inflation-adjusted variable rate, which will be reset May 1, 2022. After just a month, inflation has increased 0.83%, which translates to a variable rate of 1.66%. The current variable rate is 7.12%, based on inflation from April to September 2021.

Here are the relevant numbers:

What this means for future interest rates

In the very short term, I don’t expect the Federal Reserve to take any step to increase its federal funds rate. That is still probably 12 to 18 months away. But in the face of this current inflationary surge, the Fed needs to keep tapping the brakes on its bond-buying quantitative easing. So far this morning, stock market futures are mildly lower, indicating that this inflationary news isn’t scaring off investors.

The Fed says it has the “tools” to calm runaway inflation, but does it have the courage and political will to use those tools, which would involve sending short-term interest rates much higher? This action would also greatly increase the U.S. government’s borrowing costs at a time of massive deficits.

From this morning’s Wall Street Journal report:

“Federal Reserve officials are closely watching inflation measures to gauge whether the recent jump in prices will be temporary or lasting. One such factor is consumer expectations of future inflation, which can prove self-fulfilling as households are more likely to demand higher wages and accept higher prices in anticipation of higher future price growth. … Consumers’ median inflation expectation for three years from now stayed at 4.2% in October, the same as in September, according to a survey by the New York Fed. That level is the highest since the survey began in 2013.”

I do think that people shopping for groceries and seeing prices rising more than 5% over the last year are well aware of this inflationary threat. At least for now, inflation is becoming part of the U.S. economic equation. The Fed knows this.

I’ll end with this commentary from inflation guru Michael Ashton, author of the E-piphany blog:

“Seriously, this month’s report – while expected, at some level – turns my stomach. We have learned these lessons, painfully, long ago: you can’t spend in an out-of-control fashion and you can’t print the money that you’re spending. That’s fiscal policy 101 and monetary policy 101. Flunk them all, I say. … “

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Should have stated was speaking to married filing jointly vs single taxpayer.

There are certainly wiser than I people who follow TipsWatch, and I’d appreciate feedback on a couple of thoughts often on my mind pertaining to personal finance, which I’d rather not post on site like Bogleheads forum:

– Having read plenty of articles over the years from folks like Pfau, Kitces about annuities for retires in need of additional income stream (retires without pension, decent 401K, IRA assets), I’m perplexed why they think an immediate annuity (or DIA version of same) may be one good solution.

To my thinking, giving a lump sum payment to insurance company(s) to pay one back a very low payout in age of near zero interest rates, and most importantly no inflation adjustment seems unwise as a wise alternate income stream. The return for ones large lump sum appears mediocre choice. Granted the DIA version may make slightly better sense if one does not have enough assets in their IRS(s) to go with a QLAC.

– The other financial thing on my mind is how on earth can our government think that tax exemptions for single vs couple is necessarily fair. A couple can plan grocery, gas and many other essential expenses so as to economize much easier than can a single person in many instances, yet couples get double the tax exemption. Of course couples can also purchase double the value of ibonds every year, and couples can often more affordably deal with capital gains taxes from sales of assets, as even though they get twice the exemption, sometimes only one of the spouses actually works for wages.

Acquaintances have dismissed my concerns with comments such as “life is not fair, get over it.”

I’ve long perceived a marriage bias built into US tax code that favors couples over singles. Thoughts?

I’m not an expert on annuities (and I’ve never used them), so here’s my uninformed opinion: I can see the sense of a very simple income annuity with reasonable fees. But I’d be more comfortable with it as an add-on and not have it wipe out all my retirement savings. Here is a decent article: https://www.spokesman.com/stories/2021/nov/14/carla-fried-enjoy-more-retirement-spending-less-st/

The problem right now is that because of ultra-low interest rates, annuity payouts are low and they aren’t adjusted for inflation. So an investor would probably want to “dollar cost average” into annuities, buying them in stages and hoping interest rates will rise in the future.

Yes, the tax code does give an implicit break to married people, because in practice 2 married people can live more cheaply than 2 single people living separately. For couples with large amounts of tax-deferred savings, the RMD burden on the surviving spouse can be tough, because of being shifted to filing single. Overall, though, the rate structure seems fair (but I am married and biased).

I have been buying and accumulating I Bonds because I thought the situation we are now in was very possible. However, despite the jeers from those who said their returns in stocks were way over I bonds, I still really didn’t want this hyperinflation to actually happen. And now that it’s here I am concerned that the US Government will order all the I Bonds to be redeemed.

Rob, I don’t think I Bonds would ever be recalled. Highly unlikely. I agree with you about inflation: We prepared for this buy investing in inflation protection, but no one should ever “cheer” for higher inflation. It is an acid that will eat away at our life savings.

I meant to type “Medicare pat B increase for 2022.” Whew boy, wonder about my cognitive thinking at times.

Am very much aware many complain about cost of living, and I’m guilty of this. Anyone note the Medicare part B increase for 2020? The government gives and takes. Have read increase in part B is due in large part to increased use of Medicare and the approval of expensive Alzheimer’s drug that many say doesn’t really help very many suffering with Alzheimer’s. A reasonable person can assume medical expenses will continue to soar. I continue to be upset about my perception of how the American tax.Medicare system is more unfair to single retirees of very modest MAGI. I’m grateful ibond holders get a bone in this age of abysmal bond/savings account interest, though one bright place (current ibond return) hardly makes up for government keeping rate around zero to keep all their massive spending debt interest lower, Then again, what do I really know except that single retired tax filers appear to me to be at a decide disadvantage to married retired tax filers in most circumstance. My wife died in 2001. On that depressing note, happy holidays to all of you!

FYI, I have an article posting Sunday morning on the Medicare premium increases .

I’ll pass on the opportunity to bash Joe Biden and his advisors here. I have saved one of David’s posts from a few months ago demonstrating the ten year TIPS underperforming a nominal alternative over the same time period. The lesson to me is that predicting the future is a hazardous venture. Thanks David.

Hi David – I was reading about how some financial advisers are adjusting clients’ portfolios because of inflation. One said he was moving money to “taxable and municipal TIPS.” Do you know what these are?

Taxable TIPS would be TIPS held in a taxable account, like one at TreasuryDirect. I’ve never heard of municipal TIPS, however.

Financial advisors. Those that make predictions only keep their jobs because most forget their misses. Barron’s Roundtable is a great source of humor.

Len, I read the Barron’s Roundtable issue for a decade and eventually gave up. Complete waste of time.

Thank you for another timely update. Winter inflation may continue to run hot with energy prices remaining high.

I do remember the late 1970s and early 1980s. It was rough but we somehow survived. Of course, back then, there was less ‘stuff’ to buy and we concentrated on the basics of food, utilities and transportation. Lots of folks where I lived did a lot of bicycling, walking and carpooling. Not many were able to afford one person per car with poor wages and lack of jobs.

It’s very disturbing. I fear for young families and young working professionals, who are most affected on the price increases in winter time heating oil and gas costs, and food increases. They too would be disproportionately hit hard when the FED does raise interest rates, and their loan servicing costs go up. Being in their prime wage earning years, they may push back, thereby spiraling the wages upwards even more. This could create a schism demographically, and some real social unrest.