Yes, there is a slim chance we could see a higher fixed rate in 2022. But next year’s investors may still want to invest in I Bonds before May 1, to lock in the current 7.12% variable rate for six months.

By David Enna, Tipswatch.com

See my April 24 update on this topic: Let’s handicap the I Bond’s fixed-rate equation

The Federal Reserve last month began tapering its bond buying stimulus program, and hinted that it might begin raising short-term interest rates in 2022, well ahead of the expected schedule. The reason? Dangerously high inflation continues to entangle itself into the U.S. economy.

Federal Reserve Chairman Jerome Powell made clear this week in testimony to Congress that inflation has been stronger than the Fed expected, and is running at a pace (an annual rate of 6.2%) that cannot be maintained. Among his comments:

“It’s difficult to predict the persistence and effects of supply constraints, but it now appears that factors pushing inflation upward will linger well into next year. …

“Generally the higher prices we’re seeing are related to the supply and demand’s imbalances that can be traced directly back to the pandemic and the reopening of the economy. But it’s also the case that price increases have spread much more broadly in the recent few months across the economy, and I think the risk of higher inflation has increased. …

“Inflation has run well above 2% for long enough that if you look back a few years, inflation averages 2%. … So I think the word transitory has different meanings to different people. To many, it carries a sense of short lived. We tend to use it to mean that it won’t leave a permanent mark in the form of higher inflation. I think it’s probably a good time to retire that word and try to explain more clearly what we mean.”

Powell’s admission that our current surge in inflation won’t be short-lived is a key concession, after months of claims the inflationary surge would be “transitory.” The result of this concession should be reflected in Fed policy: 1) quantitative easing through bond buying should be scaled back quickly, and 2) short-term interest rates should begin to rise by mid-year in 2022. Both of these actions, however, could roil the stock and bond markets, as we have seen in the last week.

Eventually, both real and nominal interest rates should begin rising, ending nearly two years of absurdly low rates, at a time when inflation has surged to a 30-year high. Finally, will investors see a reasonable return on safe investments? That’s my hope.

That brings us to the question: If the Fed truly does begin changing course (despite the likely stock market turmoil that will result) when is the Treasury likely to begin lifting the fixed rate of the U.S. Series I Bond above 0.0%, where it has remained since May 2020?

The all-important fixed rate

Even though newly issued Series I Savings Bonds currently have a fixed rate of 0.0%, they remain the most attractive very safe investment in the world. Because of the I Bond’s inflation-adjusted variable rate, investors buying I Bonds in December will earn 7.12% annualized interest for six months … and at least 3.56% over the next year (probably much higher, but that’s the worse-case scenario). Compare that to the current yield of a 1-year Treasury: 0.26%.

At this point, I Bonds don’t need a higher fixed rate to be attractive. Consider this: An investor buying the $10,000 per person per year limit in December would earn $356 in interest in the first six months. That is the equivalent of more than 17 years of interest from a fixed rate of 0.2%. For this reason, it will be almost impossible to justify not buying your 2022 allocation of I Bonds before May 1, even if you think the fixed rate will tick higher on May 1. You’ll want to lock in that 7.12% for six months.

But for investors looking to hold I Bonds as a long-term investment, a higher fixed rate is always attractive. The higher, the better.

After the Federal Reserve begins pushing short-term interest rates higher (possibly in mid 2022), what are the chances we will see a higher fixed rate for the I Bond? Let’s take a look back at the Fed’s last “tightening” period, which began with hints of tapering in 2013, followed by a tapering launch in January 2014 and then finally, in December 2015, actual increases in the the Federal Funds rate.

It’s surprising to remember that the I Bond’s fixed rate rose to 0.2% in November 2013, more than two years before the Fed began raising short-term interest rates.

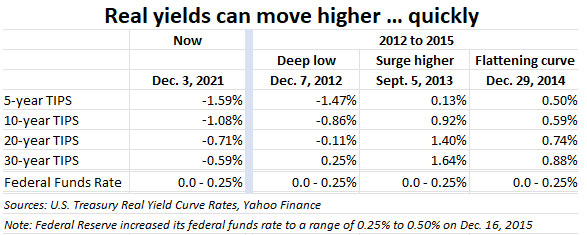

Based on this “past performance,” we can surmise that maybe the Federal Funds rate has little to do with real yields in general, or the I Bond’s fixed rate in particular. And that is true. Real yields (meaning yields above inflation, or currently, below inflation) are much more a factor of market sentiment. I contend that the I Bond’s fixed rate generally tracks 50 to 60 basis points below the real yield of a 10-year TIPS. At this point, a 10-year TIPS has a real yield of -1.08%, meaning the I Bond currently has a yield advantage of 108 basis points. Under these circumstances, there is very little chance the Treasury would raise the I Bond’s fixed rate above 0.0%.

So, for the I Bond’s fixed rate to rise, 10-year real yields are going to have to climb dramatically higher, probably at least 125 basis points from today’s level. But, that isn’t really possible in 2022, is it? Actually, it is possible, as demonstrated dramatically in the Fed’s last tightening period beginning in 2013:

Note that the 10-year real yield rose a remarkable 181 basis points in the period from December 2012 to September 2013, even though the Federal Reserve 1) hadn’t even started tapering its bond purchases and 2) was still more than two years away from its first increases in short-term interest rates.

This next chart compares rate trends for the I Bond’s fixed rate, the Federal Funds rate and the 10-year real yield over the last 10 years (click on the image if you want to see a larger version):

Note that in most cases through the decade, 10-year real yields rose and fell before the Fed took action to raise or cut short-term interest rates, and the I Bond’s fixed rate rose and fell as a lagging indicator of 10-year real yields. This makes sense because the I Bond’s fixed rate is changed only twice a year: On May 1 and November 1. The Treasury makes that rate decision based on rate trends for weeks or months leading up to the reset.

When the 10-year real yield surged higher throughout 2013, the Treasury reacted with a 0.2% fixed rate in November 2013. When the 10-year real yield started slipping lower in 2016, the Treasury returned the I Bond’s fixed rate to 0.0% through November 2017. After the 10-year real yield surged to a multi-year high in late 2018, I Bonds got a fixed rate of 0.5% for a year.

A higher fixed rate is possible in 2022

To be clear, the Treasury has no announced formula for setting the I Bond’s fixed rate, and everything you just read is informed speculation. The Treasury sometimes does weird things.

To get to a higher fixed rate, it’s going to take a mighty surge in real yields, but the example of 2013 shows that this kind of surge is possible when the Fed takes away the easy money punch bowl. The difference this time, however, is that the Fed has stated clearly that it will begin scaling back its bond buying, and real yields have barely budged. The 10-year real yield — now at -1.08% — remains close to its 2021 low of -1.19%, set on Aug. 30.

My guess is that the I Bond’s fixed rate will remain in a range of 0.0% to 0.2% through 2022. Will the fixed rate rise at or before the November 1 reset? I’d put the odds at about 15%, and that would take a giant move higher in real yields. But hey, I could be wrong.

Final thought: Can you really pass up 7.12% for six months?

Timing your I Bond investments in 2022 will take some serious thought. Will you wait it out for the chance of a higher fixed rate? I think a lot of I Bond investors will be tempted to do that. Or will you simply take the bird in the hand — a 7.12% return for six months? It will be there for the taking in January, when a new $10,000 per person purchase cap sets in.

My opinion: Waiting until mid April 2022 to make an I Bond purchase will make sense, because by then you will know the I Bond’s next variable rate, and there’s always the slim possibility that real yields will rise by 100+ basis points. But realistically, waiting until May and beyond probably won’t make sense, because as I noted earlier, the six-month return on 7.12% will be equal to more than 17 years of a 0.2% fixed rate.

Of course, the variable rate reset on May 1 could be near 7.12% or even surpass it. But remember, when you invest in an I Bond, you get the current variable rate for a full six months, and then all future variable rates will follow for six months each. Buying before May 1 looks like the logical choice.

I’ll be writing more on this topic early next year.

More on I Bonds:

- I Bond Manifesto: Why inflation-linked savings bonds can work as part of your emergency fund

- Nov. 1 update: I Bond’s fixed rate holds at 0.0%; composite rate soars to 7.12%

- I Bond podcast: U.S. Savings Bonds for a risk-free, stellar return

- I Bonds vs. TIPS: What’s the best bet for inflation protection?

- Seeking Yield And Safety? The Best Choice Is U.S. Savings Bonds

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Pingback: Let’s handicap the I Bond’s fixed-rate equation | Treasury Inflation-Protected Securities

So David,

Back in November 2021 I opened an account for me and the wife 10K each. Than in January I did another 10K each. 40k getting 7.12 for even 6 months is like 1400 bucks way better than anything anyone can get there hands on. So my question is why wait to deposit the money since you are getting the 7.12 starting from day 1. If you wait 3 months your losing out at that rate and 3 months worth of interest right? And when my bonds reset won’t I be getting the higher rate for the following 6 months. That’s if the raise the rate or lower if the lower the rate. Thank You

I Bonds are a unique investment because no matter when you purchase them, you get a full six months of the current interest rate before the rate resets. So if you buy anytime before May 1, you will get the full six months of 7.12%. If this is a long-term investment, it won’t make any difference, your return will be the same. After the first six months, you will be getting the next variable rate, whatever that is, and it will keep resetting every six months after that.

I know there is a fixed rate of 0 now; and then it’s paying the 7% rate based on inflation. If the Fed raises interest rates how does that affect those two figures.

Rick, the next variable rate depends on inflation from September 2021 to March 2022. The Fed is trying to tamp down inflation, but probably won’t have much effect by March. After that, I do expect inflation to begin lessening, but probably to an annual rate of 3.5% to 4% for 2022. That’s just a guess.

The fixed rate could rise after real yields rise above zero, but so far they remain well below zero … -0.73% for a 10-year TIPS. My theory is that would need to rise nearly 100 basis points, to about 0.25%, to even raise the possibility of a higher fixed rate. Seems unlikely at the May reset, “possible” at the November reset. Anything can happen, though.

I didn’t ask that too well but you managed to answer it, thanks….

Hello,

I am wondering if there is a grace period when purchasing the maximum amount of i-bonds each year. I set up an account on treasury direct with the plan to buy $10,000 in i-bonds for my husband, myself and two kids in december 2021. Then I was planning to buy the same max. amount again in jan. 2022..However there was a technical problem in linking my bank account to treas. direct and I wasn’t able to make the 2021 deadline. I made the max purchase for 2022 the first week of january. Is there a way to still buy the maximum amount for 2021 or is it too late?

Thanks in advance.

I’ve heard other people say this happened to them, because of the last-days rush to open TreasuryDirect accounts. You could try calling TreasuryDirect at 844-284-2676 or emailing TreasuryDirect to explain your situation. https://www.treasurydirect.gov/WF/WebFeedback?site=td01&subject=peori

Thank you. FYI, I called them this morning and waited on hold for about a half hour…They finally answered and said there’s no grace period and no way to retroactively go back and buy i-bonds for 2021. Said the long hold time is due to high interest in i-bonds. Thanks for your help.

Hello David. Thank you again for your web site and thoughts. The second graph you posted above would also argue that perhaps in 2022, assuming the federal funds rates increase, TIPS yields may finally move out of negative territory, correct? Of course, who knows anything for sure.

Yes,it’s possible. (I’m going to post something on this Sunday.) The 10-year real yield has moved 30 basis points higher in a week. The bond market is finally reacting to the upcoming Fed actions. It will be interesting to see how quickly yields could rise. And if real yields to climb above zero, then TIPS again become competitive with I Bonds.

Do you have any guesstimates on the range of what the next inflation rate will be in May?

When will we have a better sense of what it is? March/April?

I bought my first I bond over the summer and have cash just lying around, so I’m debating if I invest it by end of January, or if I should wait til April. It’s probably splitting hairs, but do you have any thoughts?

The I Bond’s next inflation-adjusted rate will be set with the CPI report for March, which comes out April 12. I am going to be writing a guide to buying I Bonds in 2022 in early January. Right now, I am thinking buying in January would be fine. Buying in April would be fine. But I’d be leaning toward buying before the rate reset on May 1.

Has anyone any information about buying extra I-bonds as gifts(Between you and the spouse) to hold for longer periods of time? Front loading is the term I believe. I read we could buy well above the $10k limit($100k or more) as a gift to your spouse and hold it in the gift queue(my term) for extended times(years) until you move the money over in as a gift to each other in 10K(plus interests) limit in future years as your yearly allotment. The 10k gift keeps earning interest while in this holding queue. It does lock up the funds, but if true feels like we would be buying a bond ladder that you could use for year 20k(plus interest) retirement income. This front load may not make make sense at zero fixed rate, but if the fixed rate does go up. This option of buying and holding in the gift queue could mean a way of loading up on bonds with fixed rate composites and distributing to each other in future times. May make great sense. As long as it is legal?

Steven, yes, I have seen these discussions in the Bogleheads forum, dating back to 2020: https://www.bogleheads.org/forum/viewtopic.php?f=1&t=306297. The discussion seems to be indicating “this is allowed,” but the Treasury has not clearly weighed in. If it works, you can buy your $10,000 limit in a year, and then buy more $10,000 allocations assigned to a different person. Each $10,000 purchase has to be made separately and has to be assigned to a person with a TreasuryDirect account. Once you put it in the gift box, the I Bond is no longer yours, but it does begin earning interest. You can only move $10,000 a year to your assigned giftee, and that amount would fill their I Bond purchase limit in the year the gift was given.

There’s no huge advantage in doing this right now, since you could do it all the way through April and still capture the 7.12% interest for six months. The strategy would backfire, sort of, if the fixed rate rises substantially in the future, because you would be gifting I Bonds with a 0.0% fixed rate.

I suspect the Treasury didn’t intend to allow the gift purchase program to be used this way, but its rules do suggest it is allowed.

Hi David,

Thanks for the info on I bonds. I had purchased via payroll bonds in 2000-2004 for a home purchase, my wife and I saved many 20K in that time. I have some left and looked up one from 2001, $50 face value, maturity is 4/2031, the calculator showed it is almost worth, $170. What is the historic return on the bonds, can’t find any info online. Now rates are. Higher again will build up our emergency fund and diversify from bank savings and cash away from stock/ bond investment accounts. I also like idea of short term savings w/ Treasury direct I bonds. I will subscribe.

Thanks

Mark

Hello Mark, It looks like you have an I Bond issued in April 2001, and that is a very good thing to have. If that was the origin date, that I Bond has a fixed rate of 3.4% and is currently paying 7% interest through March, and then will begin paying 10.5% interest for six months beginning in April. The current value of $1,000 of that I Bond is now $3,107. Hang on to those until maturity. You can do this calculation on TreasuryDirect’s Savings Bond Calculator: https://treasurydirect.gov/BC/SBCPrice

I would really appreciate your advice on what fixed income products one should invest in after the $10K I bond limit, any products with the same simplicity, albeit lower (not marginal) returns?

This is tough. For an emergency fund, I’d just combine a Treasury money market fund (earning near zero) with online bank savings accounts (earning 0.60%) and maybe some 1-year bank CDs if yields start rising. I wrote awhile back about T-Mobile Money, which offers FDIC-insured savings accounts (with a debit card) paying 1%. I use that, and you don’t have to be a T-Mobile customer. https://tipswatch.com/2021/06/01/t-mobile-money-a-weird-but-insured-way-to-earn-1-on-your-cash/

My core bond fund is Vanguard’s Total Bond, the ETF is BND. It will take a hit eventually, but it is solid and conservative. For inflation protection, I prefer Vanguard’s short-term TIPS fund, VTIP, but that does have some downside risk, maybe up to 5% to 6% if short-term real yields rise quickly.

Remember: I’m just a financial journalist, not an adviser.

“maybe some 1-year bank CDs if yields start rising.”

What yield would get you interested in a 1 year CD? 1%? 2%?

At least 1%, which I can get at T-Mobile Money. So maybe a bit more. When 5-year CDs return to 3%, I’d be interested.

Thanks so much! I literally just discovered your site and am very impressed by the amount of knowledge you have, and now how quick you are to respond.

Would you be interested in T-Bills too, at a certain yield? I know next to nothing about them and their pluses and minuses, having only discovered CDs back in 2018 and I bonds this year.

Also, I read another post here about not being so quick to sell I bonds with 0% fixed rates, and I confess beforehand I was thinking of immediately selling my I bond (0% fixed rate) when the rate went below 1%, but maybe I’ll just come back here and ask for advice instead!!

FYI, DepositAccounts.com just posted an excellent summary of best bank account interest rates: https://www.depositaccounts.com/blog/bank-accounts-survey/

About that summary of best bank account savings rates:

The pack of savings accounts that pay .05 is long, so Marcus shows 0.6% return for savings account holders, though a little more attention shows 0.6% is only for Marcus account holders who are also AARP members. I’d certainly not pay for AARP membership to earn 0.1% more interest on a Marcus savings account (;

Meant to type “The pack of savings accounts that pay .5% is long..”

do you see any relationship between the 6 month T bill rate and the I bond fixed rate, considering these rates each adjust at the same time interval?

Not a lot of relationship, in my opinion. A continuous rise in the nominal 6-month Tbill rate will often cause 5-year TIPS to get a higher real yield, and so that could have some effect on the Treasury’s fixed-rate decision. But often when short-term rates are rising quickly, longer term rates stabilize and even fall, flattening the yield curve. In times of quickly rising short-term rates, a 5-year TIPS often becomes attractive versus an I Bond.

First off, as always, thank you for another great article! Last week on Squawk Box they had a segment on IBonds. Becky was actually funny saying she was unfamiliar but immediately bought after learning about them.

I’m curious if your opinion on buying in January vs May in hopes of a higher fixed rate would change based on the following: Been buying max purchase for wife and I past 7 years. And Have no intention of redeeming early with previous/future purchases.

Since we are benefiting with the 7 years of previous purchases earning the current +7% possibly it makes sense to wait for the slim chance?

I Bonds getting mentioned on Squawk Box is a major achievement! On the I Bond purchase, I would be OK with buying in January if an investor has cash ready to go. Otherwise, it makes sense to wait until after April 12, when the March inflation report comes out and we will know the next inflation-adjusted rate. If real yields are still negative in mid-April, the fixed rate will be staying at 0.0%, so buy in April. Buying before May 1 is going to look best in almost all scenarios.

Maybe you can help me with this question. I want to put my Ibonds as well as my Wifes into our trust. I contacted treasury direct by phone. The gentlemen said to open a new acct in the Trusts name. After it is set up I could move our Ibonds from our acct to the Trust. I asked then if I would be able to only buy $10,000 in Ibonds each year since the trust is in my SS number. He said no in fact I could buy $10,000 in my old acct and my wife could as well and then move them over to the trust with the 5511 form. He also said the trust could also buy $10,000 as well which would allow me to add a total of $30,000 I bonds into the trust each year. i really questioned him about it and he was very sure that this was correct and legal. What is your thoughts? Thanks SV

I am not at all experienced with the workings of a trust and TreasuryDirect. Other readers may be able to advise you. It seems logical that you could buy $10,000 in each individual account and $10,000 in the trust. Other readers do that. Harry Sit at TheFinanceBuff.com has a good article on this: https://thefinancebuff.com/buy-more-i-bonds-treasury-direct-trust.html

He notes: “You’ll get a stern warning if you buy the maximum in both accounts and transfer from one account to the other in the same year. So if you’re buying the maximum in both a personal account and a trust account, you should just keep your personal account and your trust account separate.”

Interesting. The gentleman at Treasury Direct said I could buy 10,000 in my personal acct 10,000 in my wifes acct. fill out form 5511 have it transfered over to the trust and have the trust buy 10,000 as well. Easy peasy. I don’t want to do anything illegal that is why I am asking. The FinanceBuff’s view is not the same as his any ideas where to get the definitive answer. Thanks SV

Since TreasuryDirect guided you on this, I would keep notes on that discussion and try out your strategy. Often, a “stern warning” from TreasuryDirect does not mean you need to reverse the purchase.

I have purchased 10K (as did my wife). I then purchased 10k as a gift and transferred it into her account. Seemingly (and up till now) with no problem.

Why not hedge your bet and buy $5K in January and then wait until April to decide whether the buy $5K in April at the current (7.12%) rate or in May (at the new fixed and variable rate)? Presumably, if they raise the fixed rate to, say, 0.2%, then they will lower the variable rate by that amount, which means that the new variable rate on bonds bought before May will be 0.2% lower. Moreover, since the fixed rate applies for the life of the bond, you would always get 0.2% more when they lower the fixed rate back to 0.0%

I can’t argue with splitting your purchase, as long as you get to the max purchase in 2022, assuming you can afford it. A couple things: 1) Buying in January or April is essentially the same thing. Your return will be the same, but buying in January gives you a head start if you are looking to redeem early, after 1 year or before 5 years. 2) The fixed rate and variable rate are independent, so raising the fixed rate won’t affect the variable rate, but it will raise the overall “composite” rate. 3) The life of the bond is 30 years, but remember that the 7.12% interest in the first six months is equivalent to 17+ years of a 0.2% fixed rate. Plus, the $356 earned in the first six months will continue to compound with inflation, growing each year.

I am thinking that inflation from September to March may run close to the 3.56% of the last rate-setting period, meaning May’s new variable rate will be close to the current 7.12%, and the composite rate could be higher if the fixed rate gets raised in May. Then people will agonize over the decision: Buy before May, or after May?

I have a specific tips, tax 1099 related question: my tips investments (laddered like you have recommended) all have reset months of July & October. Does that mean the 1099 that I receive from Treasury Direct will reflect the current principal values/phantom value increases that I have now (as of October 15, 2021) (assuming no new purchases this month) or will it reset as of 12/31/21 and increase again for purposes of reporting the principal increases due to inflation for tax year 2021? Just doing some tax planning etc. Love your newsletters and twitter account too. Just Thanks.

This is a great question, and even though I face that dreaded 1099-OID every year, I don’t know the answer. I looked at my statement for last year and it does show values through Dec 31, so I am assuming the Treasury reports the full year of inflation accruals.

This page in TreasuryDirect has some information: https://www.treasurydirect.gov/indiv/research/indepth/tips/res_tips_tax.htm