May 2, 2022 update: Treasury holds I Bond’s fixed rate at 0.0%; composite rate soars to 9.62%.

By David Enna, Tipswatch.com

Based on the March inflation report, which concluded the six-month rate setting period for the U.S. Series I Savings Bond, the inflation-adjusted variable rate of the I Bond will rise from the current annualized 7.12% to 9.62% as of the May 1 reset.

This is for all I Bonds, no matter when you purchased them. All I Bonds will get six months of the 9.62% interest rate, but the starting month for the new rate will depend on the month the I Bond was originally issued.

Here are the official inflation numbers used in this calculation:

The 7.12% variable rate was already a record high for the I Bond, which was first issued in September 1998. So the new rate of 9.62% will crash through that record high. Possibly, we may never see a rate this high again. Economists have speculated that the March inflation report will set the peak and now we will begin a gradual slide lower. But … who knows?

For a much more detailed discussion of these savings bonds, read my Q&A on I Bonds.

For reasons to use I Bonds as part of your emergency fund, read the I Bond Manifesto.

Stick with the buying strategy!

While waiting for the May 1 reset might look tempting to launch directly into the 9.62% rate, I still strongly recommend buying I Bonds before April 30, which will lock in a 7.12% rate for a full six months, followed by 9.62% for six months. That’s an annual rate of about 8.4%, and there is no other very safe investment that can match that return.

I Bonds must be held for 12 months before you can redeem them. If you redeem them before five years, you will forfeit the last three months of interest. But if you buy near the end of April 2022, you will get full credit for April and can redeem 14 months and a few days later, avoiding taking the interest penalty on the 9.62% rate.

However, I always recommend buying I Bonds every year up to the purchase cap of $10,000 per person per year and holding them until you actually need the money. People who have been buying I Bonds for years — like many of my readers — are very happy right now, collecting an annual rate of 8.4%, plus any fixed rate attached to the original purchase.

Will the I Bonds’s fixed rate rise on May 1?

I still say “no,” but conditions are getting better for a fixed rate higher than the current 0.0%. The real yield of a 10-year TIPS has now “surged” to -0.12%, an impressive rise of 85 basis points since the beginning of the year. But until it gets to at least 0.25%, I think it’s unlikely the Treasury will increase the I Bond’s fixed rate. We might see the rate rise in November, which would be available to grab when the calendar resets in January.

My advice: Don’t be waiting for a higher fixed rate that might never come, and miss out on the chance to make $840 on a $10,000 investment in one year. Invest up to the cap before May 1.

The March inflation report

Once again, this was a stunner.

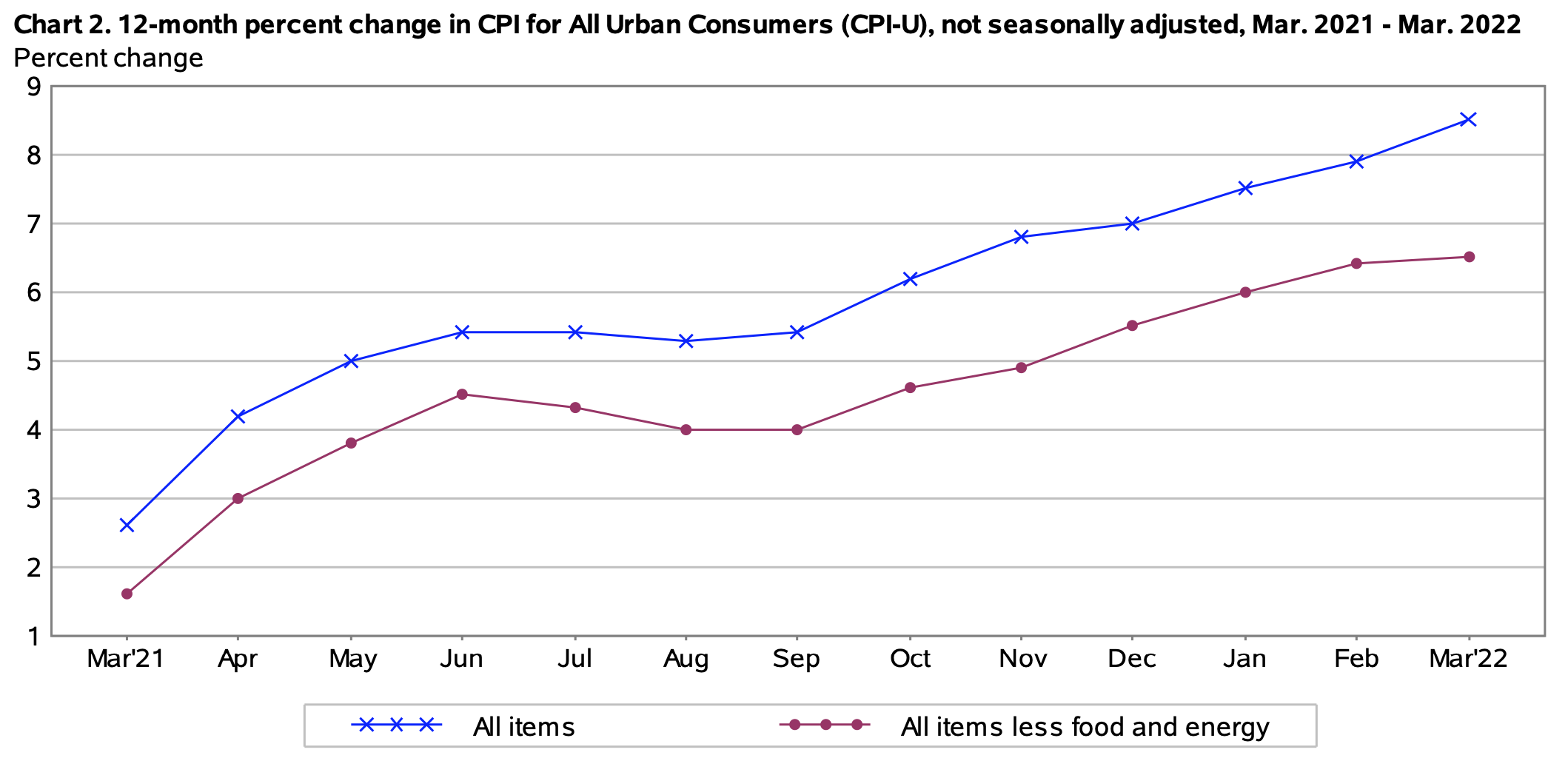

The Consumer Price Index for All Urban Consumers increased 1.2% in March on a seasonally adjusted basis, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all-items index increased 8.5%.

Both the March and year-over-year number were higher than the consensus forecast, which has happened repeated for the last six months. However, core inflation — which removes food and energy — came in lower than expectations for the month (at 0.3%) and year-over-year (at 6.5%, the highest level for core inflation since August 1982.)

So economists might view this report as a “mixed bag,” but American consumers are seeing nothing positive about it. The year-over-year number of 8.5% was the largest 12-month increase since the period ending December 1981. Inflation is surging across almost all areas of the U.S. economy:

- Gasoline prices rose 18.3% in March and accounted for over half of the all items monthly increase, the BLS said.

- Food prices rose 1% for the second month in a row and are now 8.8% higher over the last year. That’s the highest annual level since December 1981.

- Especially painful: the costs of food-at-home increased 2.0% in March.

- The costs of shelter rose 0.5% for the month and are up 5.0% over the year. It seems likely that we will continue to see higher costs in this area as rents are adjusted higher.

- The index for airline fares rose 10.7% in March.

- One area with declining prices was used cars and trucks, down 3.8% but still up 35.3% over the last year.

Here is the overall trend for annual all-items and core inflation over the last year, showing the steady rise higher since September 2021. Many inflation-watchers believe inflation now will begin gradually declining, possibly to a rate of 4% to 5% by the end of the year. But the war in Ukraine has created huge volatility in fuel and food prices:

What this means for TIPS

Investors in Treasury Inflation-Protected Securities are also interested in non-seasonally adjusted inflation, which is used to adjust the principal balances of all TIPS. The March inflation report means that TIPS principal balances will rise 1.34% in May, after rising 0.91% in April. Here are the new May Inflation Indexes for all TIPS.

This year’s incredible surge in inflation demonstrates the value of placing (and keeping) a portion of your investment portfolio into inflation protection, provided by TIPS and I Bonds. When inflation surges unexpectedly, these investment become valuable insurance against losses.

For a more detailed look at TIPS, read my Q&A on TIPS.

What this means for future interest rates

As many of you know, I am writing this in the mid-afternoon in Catania, Sicily, near the end of a three-week holiday. I haven’t been tracking the Federal Reserve’s pronouncements, but obviously the Fed seems highly motivated to get interest rates higher to slow the pace of inflation. This report should add fire to the motivation.

On the positive side for the Fed, core inflation was slightly lower than expectations. But that could be caused simply by consumer spending shifting to higher food and fuel costs, leaving less disposable income. There is no evidence that inflation will suddenly plummet, so the Fed needs to stay on this course. It could take years, unless the economy slips into a deep recession.

At some point, the real yields provided by TIPS should become competitive with I Bonds and eventually surpass the I Bond’s fixed rate, even if the fixed rate rises later this year. It will be good to see TIPS back as an attractive inflation-fighting investment.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Pingback: This Savings Bond Now Pays Nearly 7% — Should You Buy? - TheFinanceMagazine

Pingback: 7 Streams of Earnings Past a Wage - English Jobs Reviews

Why wouldn’t my older i-bonds (those purchased between June 2022 and October 2022) reset to the new 9.62% interest rate but my newer one purchased November 2022 did? I understand my new i-bonds purchased December 2021 onward staying at 7.12%. Is there a ‘glitch” in the Treasury Direct website?

Sorry, but I can’t answer specifically based on these June and October 2022 dates, which must be a typo. What year did you mean? What specific months did you make the purchases? If you bought in June, new rates take effect in June and December. If you bought in December, new rates take effect in December and June. A purchase in November gets the new rates in November and May.

Pingback: This government bond now pays 9.62% – should you buy it?

Pingback: This government bond now yields 9.62% – is it worth buying?

Pingback: This Government Bond Now Pays 9.62%

Treasury direct indicated you can access your account and purchase ibonds 24/7. However it fails to say that purchases made after business close are processed the next day. So I just lost out on the ~7% interest rate before May. Because my after hour purchase on April 29th was redirected to May 2nd. If they had been more clearer I had purchased them before business close. Bummer.

Yes, you absolutely need one full business day after your order to complete your purchase. I was recommending making the purchase on Wednesday, April 27, to be safe. However, you will get a May-dated I Bond, paying an annualized 9.62% for the first six months. That is very good, and this remains a good investment. Don’t fret it.

I feel the new rate is kinda a good news bad news thing. Killer rate but everything is more expensive. Of course we don’t control what’s going on so might as well take advantage of what we can while the opportunities exist. Can’t even imagine what the SS COLA is gonna be this year. IMHO this isn’t “transitory” but may be like the period we had in the mid to late 70s. I can’t even imagine mortgage rates doubling or tripling from what they are now. If you didn’t live that period of time, look it up. Brutal.

Social Security uses CPI-W to set the Social Security increase. The March inflation report showed that CPI-W was up 9.4% over the last 12 months, higher than CPI-U. But the formula only uses the average of 3rd quarter inflation versus last year’s average for the same months. A lot can happen in the next few months.

I also failed to account for the one business day.

Pingback: April 2022 Better of the Internet - Bonisa

Pingback: 3 Financial Dates and Deadlines in May 2022

Thank you , David. Very helpful. I’m following you now. I doubt inflation is going to abate soon, but in the meantime, this is a great place to park some money.

Thank you for your article on I bonds. It answered a number ofp questions I had. I would like to ask about gifting I bonds. I see you have stated that interest lock in rate and the date the bond starts earning interest begins with the purchased date not the date you actually gift it. When does the bonds purchase price go against the yearly maximum investment of $10k? Example: If my I buy 10k for myself in April 2022 and also buy 3 x 10k gift I bonds, one for each of my daughters. But they have each also purchased 10k I bonds this year. If I wait till next year to transfer them out of my account to each of them will that be OK and go against their 2023 limits for I bond purchases? This way they will still be getting the advatange of the current rates? It would also already be 12 months active and tech could be cashed in?

I guess my question is no matter when I purchase a gift I bond it starts earning interest at that point. I can then transfer/gift it into their account anytime after that up to its 30 yr? That I bond only goes against their total allowed I bond investment the year I transfer/gift it into their account?

Is this correct?

. I can invest for the future of my daughters as well my widf and I could each gift one to each other to transfer the following year when rates are very likely to be lower or possibly the fixed rate might have increased and we could reinvest depending on the landscape.

Obviously given the rates currently it seems a great opportunity to invest idle cash into these bonds

Sorry for the lengthy post. I have not bothered with treasury bonds so my knowledge is lacking. Treasury direct is a bit lacking in details. It took some reading before I saw tech I could invest 15k per yr by using $5k of my tax return into a paper I bond. They are not clear on this but in one place I could find.

I am not an expert on the “gift box” technique and didn’t even know about it until this year’s I Bond rage. (I’ve been writing about I Bonds for 11 years.) But as I understand it, from everything I have read, your assumptions are correct: Buy the I Bonds for recipients (they must have a Social Security number) this year and then deposit them in the gift box. They begin earning interest immediately, and that purchase does not count against your yearly limit. I Bonds in the gift box are no longer “yours,” they belong to the designated recipient. At the time of the delivery, the recipient needs to have a TreasuryDirect account. When you grant the I Bonds to the recipient, then that amount will count against their $10,000 limit for the year they received the I Bonds. This is how I understand it works and haven’t seen anybody with problems (so far) using this technique.

The potential negatives are 1) in the future the I Bond’s fixed rate could increase, and maybe that rate would be more attractive, and 2) TIPS in the future could be more attractive than I Bonds.

TheFinanceBuff.com has the best explanation of this technique that I’ve seen: https://thefinancebuff.com/buy-i-bonds-as-gift.html

TreasuryDirect has this helpful .pdf that won’t quite answer your specific questions, unfortunately: https://www.treasurydirect.gov/instit/savbond/otc/HowtobuygiftsavingsbondsinTreasuryDirecttipsheet.pdf

Thank you for such a complete answer and for your advice and possible concerns.

My thoughts are, given I known the rates I will get for the next 12 months 7.12% & 9.62% Inflation @ 0.0% fixed. I know I have a healthy return for that 12 month period. I am only chancing a fixed rate increase my last 6 months (first half of 2023) over this 12 month period which seems minimal. I doubt we would see the fixed rates anywhere near the highs of 1999/2000. (At least for another couple years!?!)

If that fixed rate does increase say Jan 2023 as its a calendar year reset , our family can all purchase I-bonds plus even add a gift bond each. As long as I do not exceed the $16k gift exmept limit per family member no issues. As Jan is the reset and I can wait till April again to see what the second half of 2023 rates will be. Then I can choose what to do. Transfer the gifts and cash out. Then gift purchase more prior to April deadline or if fixed increases yet again wait and purchase post deadline. If there is no increase in fixed I can just purchase more if inflation rate for year looks better than other safe investments If not I can transfer the accrued gifts bonds and we can go from there.

Looking over what inflation rates were at times fixed rates were up inflation rate will have to tank to under 2% to fit inside the trend from what I can derive from the history charts on Treasury Direct https://www.treasurydirect.gov/indiv/research/indepth/ibonds/res_ibonds_iratesandterms.htm#fixed

Then again if our current leaders of this Gov continue to run us headlong into a rerun of the Carter years…………. Something that can only be ended with a massive ression. But then again if I-bonds were around during that period can you imagine the fixed rates we could have locked in not to mention near 20% inflation.

Although I don’t use the gift box strategy, I can’t argue that using right now, before May 1, makes a lot of sense. If the fixed rate rises next year (seems likely in November 2022 or May 2023) you can hold off on granting the I Bond to the recipient and then purchase more, either as a current grant or another to place in the gift box. A higher fixed rate is not going to make up for the sensational one-year return you will be getting in the first 12 months.

Great! Thank you for your opinion as regardless of your strategic use is still far more informed than mine.

Again I appreciate the advice and your work and effort on keeping your website up to help people such as myself.

Cheers,

With markets what they are. With inflation. With Russian incursions (again) into independent Ukraine and of course with Covid weariness – i Bonds are one of the few shining stars.

Hello,

New reader/investor here.

QUESTION

If I purchase I Bonds as a gift & hold, will this lock in the current rate? Clarity on gift giving.

Thank you.

Yes. The interest starts accruing from issue date and not gifting date.

Hey David, do savings bonds ACTUALLY begin earning interest the first month after the purchase date, or is the four month delay before the earnings kick in still in effect?

Yes they begin earning interest in the month of purchase. But TreasuryDirect will not show the last three months of interest until you reach five years.

Thanks! Enjoy your vacay!!!

Thank you for this clarification. Few people seem to understand this anomaly of not seeing the 3 months. Why the Treasury makes this so complicated is a mystery.

What is difference between I bond and TIPS

I was very happy the last few years with my 3% fixed rate I-bonds I bought in the early 2000s. I am happier now that I will be getting 12.62% for the next six months. This is tempered by the whopping tax I will have to pay the irs on the interest at maturity. At least I won’t have to pay the state anything.

Thank you for your post, this is helpful. For someone who is trying to pay down debt on a home equity line of credit (HELOC), would you consider actually borrowing more against that HELOC to fund an I-bond purchase in April? The rate on the HELOC is variable and currently 3.0%, and will likely be going up as the Fed increases rates.

It might make sense by the numbers, but I personally wouldn’t borrow money to invest elsewhere. The HELOC rate might rise to 5.5% to 6% this year? So the numbers would work? Might depend on how fast you could pay it off.

Thank you for your thoughts. I agree, I think it might make sense by the numbers, as long as the HELOC rate stays below about 6 or 7%. Borrowing money to invest elsewhere can certainly be risky, but this particular potential investment in I-Bonds appears to be the closest option to a guaranteed return, as opposite to equity risk or even corporate bond default risk. I guess the US Treasury could default, but since they US has taxing authority, I would think it’s reasonable to expect I-Bonds to be risk-free.

I love our IBonds, especially now receiving a 10.34 rate. We use them as emergency money but also our travel funds to make our retirement fun and easy. Half in dividend paying stocks and the other other half in IBonds has been a great combo, especially on a small budget. Totally recommend I Bonds!!!

Pingback: I Bond’s variable rate will rise to 9.62% with the May reset - The web development company Lzo Media - Senior Backend Developer

Ciao David! Please eat some Guanciale for me. I miss Italia.

I want to be greedy. Have already bought this years max. What’s your position on using the giftbox feature at TreasuryDirect to get in on the current high interest rates? I’ve been buying iBonds for wife and me for over a decade but never have done the gift purchases. Thinking about buying 10k as gift for wife and vice versa. Then could deliver next year or even hold off if rates are still high.

Only downside I can think of is if the fixed rate is raised. But with the high interest rates would it make a material difference?

Enjoy the rest of your trip!

We did it. If the fixed rate increases, we will buy gifts again and deliver them in 2024.

From the TreasuryDirect site:

Bonds you buy for yourself and bonds you receive as gifts or via transfers count toward the limit. Two exceptions:

If a bond is transferred to you due to the death of the original owner, the amount doesn’t count toward your limit

If you own a paper bond issued before 2008, you can convert it to an electronic bond in your account in TreasuryDirect regardless of the amount of the bond. (The annual limit before 2008 was greater than today’s limit of $10,000.)

So you can’t buy the max as a gift to your wife and vice versa and still buy an additiona $10,000 for yourself.

Notice that it says I Bonds you purchase for yourself and those you receive as gifts. So you can buy $10,000 for yourself and $10,000 as a gift for someone else in the same year. However, the person receiving the $10,000 gift (now or in the future) will have the gift count against their purchase cap, and will therefore not be able to buy more I Bonds that year.

Thank you for putting together such an informative site. In the above article, you state: “While waiting for the May 1 reset might look tempting to launch directly into the 9.62% rate, I still strongly recommend buying I Bonds before April 30, which will lock in a 7.12% rate for a full six months, followed by 9.62% for six months”. I’m trying to understand the logic here – are you predicting that the next applicable rate change, November 1st, will be <7.12% annualized?

Enjoy the remainder of your trip!

No, I don’t really have any idea what inflation from March to September will run. I “suspect” it will be lower than 3.56%, which would equal the 7.12% variable rate, but who knows? My contention is that you should take the 7.12% rate for a full six months (by buying in April) and then get the 9.62% rate for the next six months. After that, you will get any variable rate that follows in November. The current rate is too attractive to pass up, since you will also get all future rates for six months.

By purchasing I bonds in April, investors are guaranteed six months at 7.12% and another six months north of 9%. Let’s say the November 2022 I bond rate ends up even higher than the upcoming May 2022 rate (hopefully not the case, as it would mean inflation is nowhere under control). But if it were higher, bonds purchased in April 2022 would still earn the (hypothetically) higher November 2022 rate for six months starting in April 2023.

By purchasing in the month before new rates take effect, you’re essentially locking in the previous 6-month rate while guaranteeing you’ll earn the new rate six months after that. This way you’ll always know the interest rate of your bonds 11-12 months into the future instead of just 6 months at a time.

The only drawback to purchasing now vs. May is that the fixed rate on I bonds is still zero. While it could be higher in May, it’s wiser to lock in an 8.4% interest rate for a year rather than 9.6% for six months followed by an undetermined rate.

Excellent analysis, Justin. Keep in mind that a fixed rate of 0.2% only adds $20 a year to a $10,000 investment. That 7.12% rate will earn $356 in six months, a huge advantage even with a 0.0% fixed rate.

I can’t speak for David E, but I think the logic here is independent of what the following six-month window will be.

7.12% for six months, capitalizing the interest, and then 9.62% for six months will give a guaranteed 8.54% APY. That obliterates any other safe investment out there. The risk-free rate is often approximated by 3-month treasuries, which are sitting at…0.69%. A 1-yr treasury? Just 1.71%.

That 8.54% APY comes with many benefits not seen in many forms of safe investments–no state/local taxes, the ability to hold onto the bond for up to 30 yr but can sell as early as just 1 yr, and the federal taxes are deferred until you do cash them in. Honestly, as long as one can tolerate the 1-yr lockout on these, they’re probably a good fit for almost anyone, even if just for an emergency fund.

About the only situation I can think of where one might want to wait until next month (operating under the assumption that the new fixed rate will be 0%, which is extremely likely) would be a situation where the money WILL DEFINITELY be withdrawn in April-May 2023 and one doesn’t want to lose 2-3 months’ interest at 9.62%. However, I think running the numbers on that would show that the extra 1 month of interest (April 2022) would still outweigh the penalty net-net. And if the next 6-month window is, in fact, higher than 7.12%, most people will just continue holding onto the I Bonds because of the above advantages.

Thank you, Scott. Excellent, sensible analysis.

The 7.12% variable rate was already a record high for the I Bond, which was first issued in September 1998.

My calcs show show 7.49% starting in May 2020 for six months. Is that incorrect?

The inflation rate history is here: https://treasurydirect.gov/indiv/research/indepth/ibonds/res_ibonds_iratesandterms.htm#comb

This is a record. I’m not sure how you came up with that calculation,

Not sure how you are getting that number. The six-month inflation rate for the May 2020 reset was only 0.53%, so the variable rate was only 1.06% at the May 2020 reset.

the may 2000 fixed rate = 3.60%

the may 2000 inflation rate = 1.91%

the caculated composite rate at that time was = 7.49%

the above was what i was trying to say, your article mentioned 7.12%.

Ok, now I understand. My article referred to the highest “variable” rate in history. The 7.49% rate you are quoting is the initial “composite” rate for the May 2000 I Bond reset. That I Bond will now be paying about 13.2% for six months.

To have backed the truck up back then! (Although being younger, that money was better placed in stocks.)

Interestingly, a 50/50 US/International stock portfolio rebalanced quarterly would have had an inflation-adjusted CAGR of just 3.50% from May 2000 through March 2022 (modeled with Portfolio Visualizer using the mutual funds VTSMX/VGTSX). A 3.60% real interest rate compounded every six months has an inflation-adjusted APY/CAGR of 3.63%. So yes, even over ~22 yr, those I Bonds beat out a balanced global stock portfolio at a tiny fraction of the risk!

I think all of us, myself included, tend to suffer from recency bias and somewhat forget that the last ~13 yr of great stock performance were preceded by a horrible 9-10 yr. Many people will point out, correctly, that US stocks have far outperformed international stocks during those 22 yr, but no one in 2000 could have predicted that (and international was ahead even 13 yr into that window!)