For the first time in 2 years, a 10-year TIPS auctioned with a real yield positive to inflation and a price discounted to par value.

By David Enna, Tipswatch.com

Here I am, vacationing in the beautiful city of Prague, and the financial world is seemingly falling apart. Earlier this morning it appeared stocks were plunging again, and my soon-to-be-completed investment in a 10-year TIPS reopening looked pretty punk.

The Treasury auctioned $14 billion in CUSIP 91282CDX6 today, creating a 9-year, 8 month Treasury Inflation-Protected Security.

All morning, according to the Bloomberg Current Yields page, CUSIP 91282CDX6 was trading with a real yield to maturity of 0.09%, about 16 basis points lower than looked likely on Tuesday. It wasn’t even hanging above the coupon rate of 0.125%, which would have meant it would auction at a discount to par.

So I went to dinner with friends (an excellent roast duck with red and white sauerkraut and dumplings … and pilsner beer, of course) and figured this wasn’t going to be pretty, with demand seemingly soaring for TIPS as stocks plummeted. When I got back to my hotel room in central Prague, I found a surprise …

The auction, which closed at 1 p.m. EDT, got a real yield to maturity of 0.232%, a very high result based on where this same TIPS was trading just a hour before the auction closed. The bid-to-cover ratio was 2.24, a very low number that indicates investor demand was weak. Conclusion: We have entered a new era for Treasury auctions, with the Federal Reserve no longer bolstering demand (and lowering yields) by aggressively buying up supply.

This was the first TIPS auction of this term to get a positive real yield in more than two years. And it was also the first 9- to 10-year TIPS auction to sell at a discount to par value in two years. I was hoping to see that result (since I was a buyer at this auction) and … whew … it happened.

Investors paid an unadjusted price of about $98.98 for $100 of par value. Because of accrued inflation, the adjusted price was higher, about $102.62 for $103.67 of value, after accrued inflation is added in. This TIPS will have an inflation index of 1.03672 on the settlement date of May 31.

It’s not spectacular, but very welcome news for TIPS investors. Keep in mind that this TIPS, with a real yield of 0.232%, could out-perform the highly coveted U.S. Series I Bond, with a real yield of 0.0%. (Because of the I Bond’s better deflation protection, though, the I Bond will still probably end up with a slight edge.)

Inflation breakeven rate

I’m going to have to “ballpark” this one, since I was eating roast duck when this auction was closing. When I returned around 8 p.m., the 10-year nominal Treasury was yielding 2.84%, creating an inflation breakeven rate of 2.61% for this reopened TIPS. While this number is fairly high, it is 32 basis points lower than the number generated when this same TIPS was reopened in March.

That means this TIPS will out-perform a nominal Treasury if inflation averages more than 2.61% over the next 9 years, 8 months. Looks good to me.

Reaction to the auction

As I would expect, the auction result caused TIPS yields to rise, and that caused the price of the TIP ETF to move lower immediately after the auction close, but not dramatically. The TIP ETF has lost about a half-percentage-point of value on the day, so far. But it still has a positive 5-day trend, in reaction to overall market volatility.

It looks like the market is OK with this auction result, even though it continues a six-month trend of TIPS auctions coming in with higher-than-market real yields.

I am pleased to see this result because TIPS investors deserve yields that are positive to the rate of official U.S. inflation. Investors who have flooded into I Bonds now have a legitimate option after reaching the $10,000 per-person cap on I Bond purchases. TIPS are a little more complicated, but a high-quality, safe investment if held to maturity.

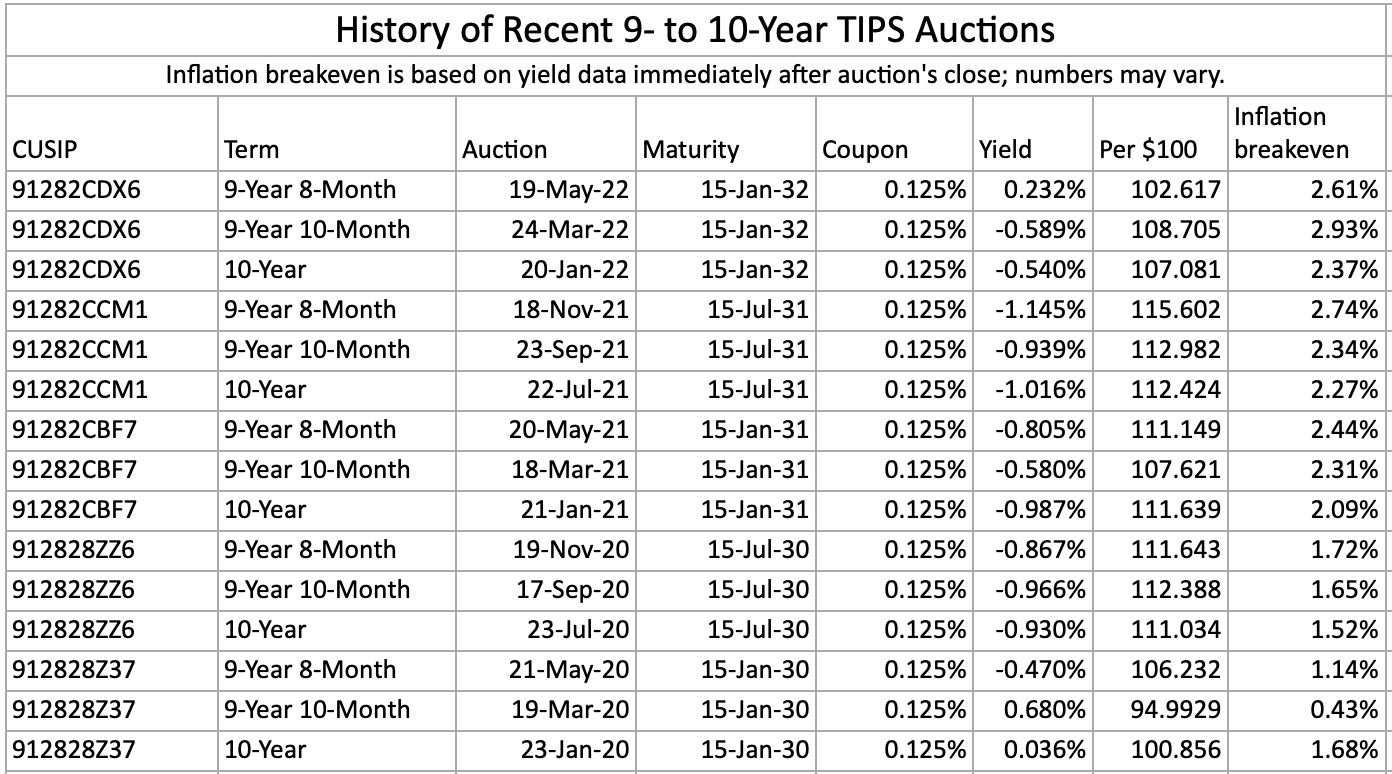

This auction closes the books on CUSIP 91282CDX6. The Treasury will auction a new 10-year TIPS on July 21. Here’s a chart of recent 9- to 10-year TIPS auctions, showing how today’s result broke a 12-auction string with below-inflation yields:

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

OK, I’m very confused. Regarding Buffalo’s purchase on May 20., his purchase price was $98.9821, which means $989.821 per bond. But instead he has to pay $1,026.20 per bond. Because? I like to buy below par. I don’t want to buy below par and end up paying above par. Regarding the .232% yield: Do I add that to the 8.6% inflation rate for a yield of .00232 + .086 = .08832 or 8.832% yield? What actual phantom interest per bond will Buffalo get every six months? Meanwhile, will VTIP drop in price with every .75 or .5 rate hike by the Federal Reserve? Or are the declines tied to TIPS auctions or both? By the way, why put VTIP in your IRA? VTIP pays you actual interest and is free from state taxes. Another one to look at is STIP.

Sorry for all the questions.

Paula Metz

OK, I should have read the treasury direct TIPS FAQs before I posted. I forgot that TIPS principal increases by an index amount as inflation rises (CPI-U). So one can calculate that monthly and the .232% yield accrues yearly in in semiannual installments of .00116 x 1,000 = $1.16 per bond. Correct? Thanks. I still think VTIP is easier except for the NAV going down.

TIPS pricing often causes confusion, especially at reopening auctions or when the real yield to maturity is negative. There is an “unadjusted” price, which is the price the investor paid for par value. In this auction, the unadjusted price was $98.98 for $100 of par value. The TIPS sold at a discount because the real yield was higher than the coupon rate. BUT … because this was a reopening auction, there was an inflation index of 1.03672 on the settlement date of May 31. So that meant investors were paying for an extra 3% of principal, so the adjusted price was about $102.62 for $103.67 of value. Still a discount, see?

Once you purchase a TIP, it pays a coupon rate (in this case 0.125%) and the par value is adjusted for inflation every day. So this TIPS would be earning interest equal to inflation + 0.125% for its term.The 0.125% interest is calculated on the accrued principal and is paid out twice a year. The principal grows with inflation until the TIPS is sold or matures.

Pingback: 10-year TIPS reopening public sale will get an actual yield of 0.232%, a powerful outcome for traders - NewsICAN

Dave, can you explain the reasoning of being overjoyed of .232% on your TIPS vs a 9.62% current 6-month rate on an I bond? I must be missing something.

Well, on the TIPS it is 0.232% ABOVE inflation and the I Bond will only match inflation. They both adjust with inflation. The I Bond’s high interest rate is caused by high inflation six months in the past.

Hi David, I’d prefer VTIP but only have VIPIX available as an option in my 401K. Do you have a perspective on allocating to it at this point in the interest rate cycle?

VIPIX is a very good TIPS fund, expense ratio is only 0.07%. Some of the risk has already been tapped out this year; the fund has a total return of -5.8% year to date. It’s getting more attractive as real yields rise. Just understand there is still some downside risk that could wipe out or exceed the inflation adjustments.

Hi really enjoy your comments on all the Treasury Products. Have one good question is how much would you consider to invest in Short Term ETF’s like VTIP? Also with rapid inflation and almost certain more corrections in market what are the best alternatives if you don’t need income for 5 years. thanks again

Bob

Hi Bob, I have a fairly large holding in VTIP in a retirement account. Because of its short duration it is less volatile, but still adjusts for inflation. It has a total return of -0.39% year to date. If rates keep rising, 5-year Treasurys will be worth a look.

This was my first-ever auction purchase. My confirmation from Fidelity this morning says I bought at a price of 98.9821. How do I calculate exactly how much will be withdrawn from my Fidelity account at settlement? The Fidelity interface (maybe all interfaces?) says 1 bond is equal to $1000 face value. Do I multiply the 98.9821 by $10 for each bond I purchased, for a total of $989.82/bond? Or does the $102.62 you referenced in your post come into play instead, and each bond will result in $1026.20 debited from my account at settlement? Thanks for the help.

Yes, that sounds right. With the inflation accrual you will be getting about $1,037 of value on May 31.

Hello, David! Thank you for your email and the analysis. I participated in this auction and am pleasantly surprised with the result as you were. Plan to participate in the July 10 year TIP auction as well. Waiting for 5-year TIPs to turn a positive yield, although it might not happen soon.

Thanks for the update. So is the ‘worst case scenario’ at maturity (deflation the entire holding period) a 3% nominal loss?

The worst case would be a nominal loss of about 2.6% since you bought at a discount. That is extremely unlikely to happen.

I was a buyer in this auction as well and was very pleased with the results. I actually hadn’t bought TIPs since two years ago, because I didn’t want that negative really yield. I bought about 40% of my yearly allocation and if real yields continue to be positive, will buy again at the next ten year and five year auctions. Thanks so much for your excellent articles. I have been a reader for many many years now.

Maybe there’s hope yet for the 5 year TIPS auction in June.

I’m even a little tempted by the 10 year TIPS auction in July.

However, at my age 10 years is getting to where 50% of my age cohort are already dead!

I was talking to a brokerage firm rep today and the poor girl asked me what my “time horizon” was.

My response was “yesterday”.

The young people just don’t get “senior gallows humor”.

Your duck diner was similar to the Kaczka duszona z kapusta that I’m used to.

Eating that sort of stuff, I guess that you’re not too worried about your own time horizon.

I was thrilled with this result. I have been incrementally laddering for 4 years now, and it was wonderful to see 0.232%.I made my July purchase now (early), and perhaps I’ll make my planned November purchase in July.