This report is going to roil financial markets.

By David Enna, Tipswatch.com

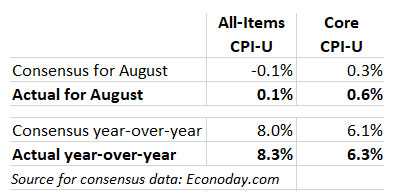

Surprises, surprises. Financial markets, which had been rallying over the last week on expectations of falling prices, got an inflation reality check today: Seasonally adjusted U.S. inflation rose 0.1% in August, and 8.3% over the last year, the Bureau of Labor Statistics reported.

Economists had been expecting inflation to decline for the month, based on plummeting gasoline prices, which were down 10.6% for the month. Instead, both the monthly and year-over-year numbers came in higher than expectations. Core inflation, which removes food and energy, also greatly surpassed expectations, coming in at 0.6% for the month (versus an expected 0.3%) and 6.3% for the year (versus 6.1%).

My two-word analysis: “Not good.”

The BLS noted that increases in the shelter, food, and medical care indexes were the largest of “many” contributors to the all-items increase, overwhelming the deep decline in gasoline prices. Some key data from the report:

- Food prices rose 0.8% for the month (the smallest monthly increase this year) and are now up a painful 11.4% year over year. Prices for all six major grocery store indexes increased.

- The food at home index has increased 13.5% over the last 12 months, the largest one-year increase since March 1979.

- Shelter costs increased 0.7% for the month and are up 6.2% year over year. The rent index rose 0.7% for the month.

- Costs of medical care services were up 0.8% for the month and 5.6% for the year.

- The index for household furnishings increased 1.0% in August after rising 0.6% in July.

- Apparel costs were up a moderate 0.2% and 5.1% for the year.

- The index for airline fares decreased 4.6% after falling 7.8% in July.

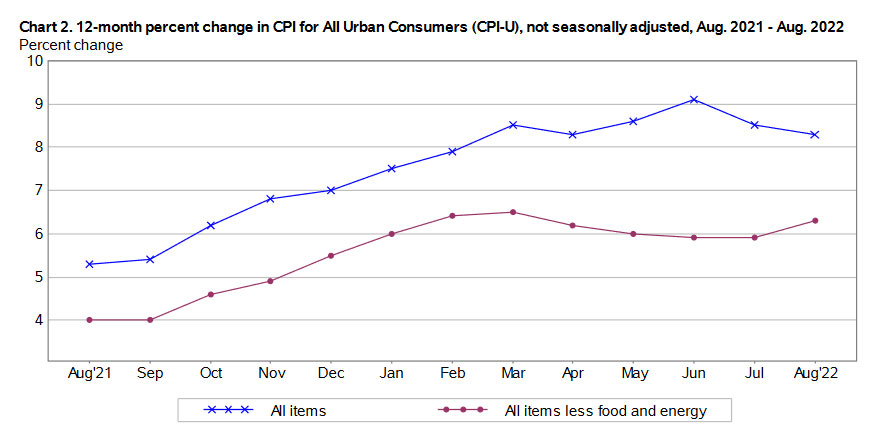

Here is the trend in annual all-items and core inflation over the last year, showing the slight rise in core inflation even as falling gasoline prices have caused all-items inflation to fall from the June peak of 9.1%.

What this means for TIPS and I Bonds

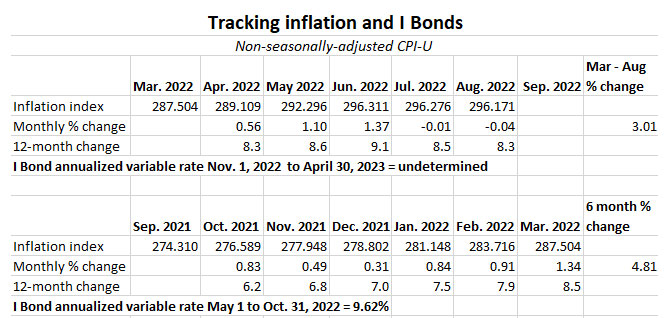

Investors in Treasury Inflation-Protected Securities and U.S. Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances for TIPS and set future interest rates for I Bonds. For August, the BLS set the inflation index at 296.171, a decline of 0.04% from July’s 296.276. The BLS called this “unchanged.”

For TIPS. The August report means that principal balances for all TIPS will decrease 0.04% in October, after falling 0.01% in September. However, year-over-year balances will have increased 8.3% by the end of October. Here are the new October Inflation Indexes for all TIPS.

For I Bonds. The August report is the fifth in a six-month series that will set the I Bond’s new variable rate, which will begin rolling out November 1 for all I Bonds. As of August, inflation has run at a rate of 3.01%, which would translate to an I Bond variable rate of 6.02%, lower than the current rate of 9.62%. However, one month remains. Oil prices seem to have stabilized this month, so it’s possible we will see a higher number. Here are relevant data:

You can see historic data back to 2012 on my Inflation and I Bonds page.

What this means for Social Security COLA

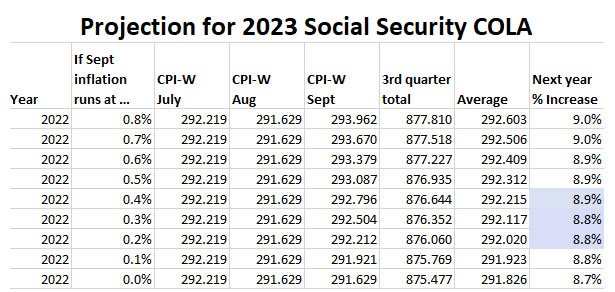

The August inflation report is the second of three — for July to September — that will set the Social Security Administration’s cost of living adjustment for 2023. The SSA uses a three-month average of a different index, the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W), to set its COLA.

For August, the BLS set CPI-W at 291.629, an increase of 8.7% over the last 12 months. However, CPI-W actually fell 0.2% for the month. But remember, it will be the average of July to September inflation indexes — compared to the same three-month average a year ago — that will determine the Social Security COLA. A year ago, that average was 268.421. If we have zero inflation in September, the COLA will be 8.7%.

Keep in mind that one month remains, and the COLA calculation could push slightly higher.

Here is my updated projection:

What this means for future interest rates

The S&P 500 just opened for trading today and it is down about 2.3%, after flashing higher minutes before the August inflation report was released. The reason: The markets are losing hope — a false hope in my opinion — that the Federal Reserve would begin easing off on tightening as U.S. inflation drifts lower. Although the monthly all-items number looks mundane, this was an ugly inflation report, with prices increasing across the economy despite a quick and steep decline in gasoline prices. Core inflation jumped from an annual rate of 5.9% in July to 6.3% in August.

U.S. inflation remains close to a four-decade high. This is not the time for the Federal Reserve to back off on its clear, necessary goal: to bring inflation down to a level at least approaching its target of 2%. Today’s report all but guarantees a 75-basis-point increase in the federal funds rate next week.

From today’s Wall Street Journal report:

Broad price pressures have proven resilient, causing the Federal Reserve to keep raising interest rates to fight inflation, said Kathy Bostjancic, chief U.S. economist at Oxford Economics.

“Inflationary dynamics are improving and moving in the right direction,” she said. “But they’re still running way too hot for comfort, either for individuals and businesses or the Federal Reserve.”

From Bloomberg:

The acceleration in inflation points to a stubbornly high cost of living for Americans, despite some relief at the gas pump. Price pressures are still historically elevated and widespread, pointing to a long road ahead toward the Fed’s inflation target. …

“If there was any doubt at all about 75 — they’re definitely going 75” at next week’s Federal Open Market Committee meeting, Jay Bryson, chief economist at Wells Fargo & Co., said on Bloomberg Television. “We thought they’d be stepping it back to 50 in November. At this point, you’d say 75 is certainly on the table in November.”

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Pingback: This week’s 10-year TIPS reopening auction is worth a serious look | Treasury Inflation-Protected Securities

With the Federal Reserve increasing interest rates, do you think the fixed rate on the IBond will increase in November?

It’s definitely a possibility, but not likely in my opinion. The 10-year TIPS real yield of 0.95% easily justifies setting the I Bond’s fixed rate at 0.2%, I’d say. But demand for I Bonds remains very strong, so I suspect the Treasury will hold the rate at 0.0%. I will be writing about this later in October.

David, I believe you stated you do not do the gift purchase process. But I cannot come with a con to doing so except not documenting it in case something drastic happens before you deliver the gift.

With rates possibly dropping I cannot find a reason not to buy another 10K at these rates. The holding period, interest, etc all start immediately. If you like the new rate you can continue to hold off on delivering for another year.

Am I missing something?

There are no “huge” negatives. When you gift $10,000 in I Bonds, you are no longer the owner of that I Bond. It belongs to the person you named as the recipient. When they receive the gift, it will count against their purchase total in the year the gift is received. One potential negative would be that the I Bond’s fixed rate rises dramatically in the future, but that’s not a huge concern. You could simply not deliver the gift that year. I think this strategy makes sense for I Bonds you plan to gift in 2023; you can lock in six months of the 9.62% variable rate and then deliver the I Bond next year, when the variable rate will likely be lower.

My plan was to buy 10K in my account to gift to my wife. And buy 10K in her account to gift to me. Thanks for the quick reply.

Your articles are very clear and very useful! I am using them to guide my investments.

Thanks for the praise. Just remember that I am a journalist and not a financial adviser. My main goal is to provide useful information.

David, Thank you very much for the articles in this topic. I learn so much from you. Since Fed is fighting the inflation until it reach to 2%. Does that means I bonds variable inflation rate will be negative soon. The next time reset (May 2023 and after …) I bond interest rate will be 0

Anything can happen, and it’s possible the I Bond’s variable rate could fall to 0.0% sometime in the future. It fell to 0.16% in the May 1, 2016 reset and hit -1.60% in May 2015. The composite rate the I Bond pays can never be less than 0.0%, however.

So Dave, back to my confusion. So 3 rungs of my 5 year TIPS ladder that was purchased on the secondary market with maturities in 10/2024, 4/2025 and 4/2026 that had accrued inflation included go down in value? What does this net out to even though inflation was worse than expected?

Thanks in advance, deeMatrix.

It’s true that all TIPS that have any accrued inflation will lose a slight amount of principal value in both September (0.01%) and October (0.04%). However, these are minuscule numbers, amounting to about $1 to $4 on a $10,000 investment. It’s not a big deal.

Thanks Dave, how do they go down in value when inflation is worse than expected? So this is basically giving back some of the accrued inflation I paid for when purchasing these rung of TIPS on the secondary market?

Thanks once again in advance, deeMatrix.

August’s inflation shock was about expectations, with the markets expecting deflation but getting slight inflation instead. TIPS get a principal adjustment based on non-seasonally adjusted inflation, which was very slightly negative. This balances out over time. Your investment is going to do fine. Don’t fret about it.

I guess I’m still confused. It says inflation is up 0.1% yet the CPI is -0.04%. What number went up 0.1%? Obviously apples and oranges, but I’m confused by it.

Seasonally adjusted was up 0.1%. Non-seasonally adjusted was down 0.04%. For TIPS and I Bonds, non-adjusted is the useful number.

i too was initially puzzled by the media’s headline indicating a rise in inflation, yet the CPI-U number used for TIPS/I Bonds actually went down. i guess it’s just a good reminder to ignore the headlines, and just seek the specific information in the BLS news release that is of particular interest.

I’ve noticed that real interest rates on TIPS have steadily increased over the past month, currently about 1% after this morning’s inflation report. I am somewhat expecting that this might suggest a significant increase in the fixed rate component for the upcoming Series I bond rates, to be announced on November 1. Thoughts?

I wouldn’t say a “significant” increase in the fixed rate is likely, but a small increase to 0.1% to 0.2% seems possible. Most I Bond experts i talk to are skeptical that the Treasury would raise the fixed rate while demand for I Bonds remains so strong. So right now 0.0% seems like the most likely result. I will be writing about this later this fall.

Dave, what do you think about the front loading strategy to buy let’s say $50k worth of I bonds at the current 9.62% rate as the gift to a spouse and transfer them to spouse account at $10k maximum limit per year over next 5 years? Thanks

In this case, you would be locking in 5 years of I Bond purchases, now owned by the person named as the recipient. The possible negative would be that the I Bond’s fixed rate rises in the future, and stays higher. The future gifts would retain the 0.0% fixed rate. Because the 9.62% rate is so high (equating to $481 over the first six months) the strategy probably makes sense.

A few months ago you talked about buying T-bills (13wk and 26wk, I believe). I’ve bought I Bonds, but never T-bills, so just dipping my toes in. Am I correct that if we expect interest rates to continue to go up that this is still a good idea? This is for spending money that I’ll need later this year and early next year. I’m also thinking of buying 4wk and 8wk bills with other cash and having them automatically re-invest so I catch the rate increases, as I don’t expect to need this money in the near future. What do you think? Thanks! Have been following you for a LONG time!

For a short-term investment, T-bills look even more attractive, with the 13-week now yielding 3.17% and the 26-week at 3.56%. The 4 weeks are at 2.62%.

thank you! I appreciate you answering me.

David,

Do you think a bank would have an issue with too many transactions with short term instruments? i.e. a lot withdrawals and deposits?

I don’t think this would be a problem.

Man that guy is good at explaining what is going on and how it isn’t going to stop on a dime.

AWESOME SUMMARY SIR! My calculation sez COLA would be a little lower if we have the same 291.629 print in September but clearly likely to be 8.5% or better unless there is an unforeseen collapse in prices. Pretty amazing after the index going up an average of 2 points or more a month for most of a year, CPI-W softens right as the COLA calc is made. LOL.

Thanks. After I finished my article I updated the projection on the COLA page and saw you are right. So that has been updated.