Have you given up on longer-term Treasurys? It’s time to get back in the game.

By David Enna, Tipswatch.com

You’ll never see me screaming “buy, buy, buy” like CNBC’s resident madman, Jim Cramer, but I do think that sensible, conservative investors should take a look at Thursday’s 10-year TIPS reopening auction.

The Treasury is offering $15 billion in a reopening of CUSIP 91282CEZ0, creating a 9-year, 10-month TIPS. An interesting side note is that $15 billion is the highest-ever amount offered at a 10-year TIPS reopening auction. These offerings have grown from $12 billion in March 2020, to $13 billion in March 2021, to $14 billion in September 2021 and now $15 billion in September 2022. That’s an increase of 25% in 2 1/2 years, and is evidence that the Treasury isn’t de-emphasizing TIPS in these inflationary times.

CUSIP 91282CEZ0 had its originating auction on July 21, 2022, when it generated a real yield to maturity of 0.630%. Its coupon rate was set at 0.625%, making it the first 10-year TIPS with a coupon rate above 0.125% since July 2019.

Definition: The “real yield” of a TIPS is its yield above official future U.S. inflation, over the term of the TIPS. So a real yield of 1.07% means an investment in this TIPS will exceed U.S. inflation by 1.07% for 9 years, 10 months.

Because this TIPS trades on the secondary market, we can track its current real yield and price in real time on Bloomberg’s Current Yields page. It closed Friday with a real yield of 1.07% and a price of $95.84 for $100 of par value. The price is at a discount because the real yield is well above the coupon rate of 0.625%.

If the real yield holds above 1% at Thursday’s auction, this would be the first 9- to 10-year TIPS with a real yield that high since November 2018, very close to the end of the Fed’s last tightening cycle. In fact, since November 2018 there have been 22 TIPS auctions of this term and 12 of them generated real yields negative to inflation. These days, a real yield of 1% or higher is something to celebrate.

In this chart, I am taking a long view of 10-year real yields, back to January 2010, a year before the Federal Reserve began aggressive quantitative easing. The chart shows how yields peaked at the end of the Fed’s last tightening cycle in November 2018, and then went deeply negative after the Covid outbreak in March 2020.

Pricing for this TIPS

CUSIP 91282CEZ0 will carry an inflation index of 1.01972 on the settlement date of September 30, meaning that investors will be purchasing a bit less than 2% of additional principal, but at a discount of $95.84 for $100 of value (a current pricing). That will work out to about $97.73 for $101.97 of principal, plus maybe 13 cents of accrued interest, making the total cost around $97.86 for $101.97 of principal. That is a rough estimate and things can change before Thursday’s auction.

And keep in mind that the inflation index on this TIPS will drift down slightly in October, ending the month at 1.01936, based on slightly negative non-seasonally adjusted inflation in August. The markets know this is coming, and the auction price will reflect the minor change.

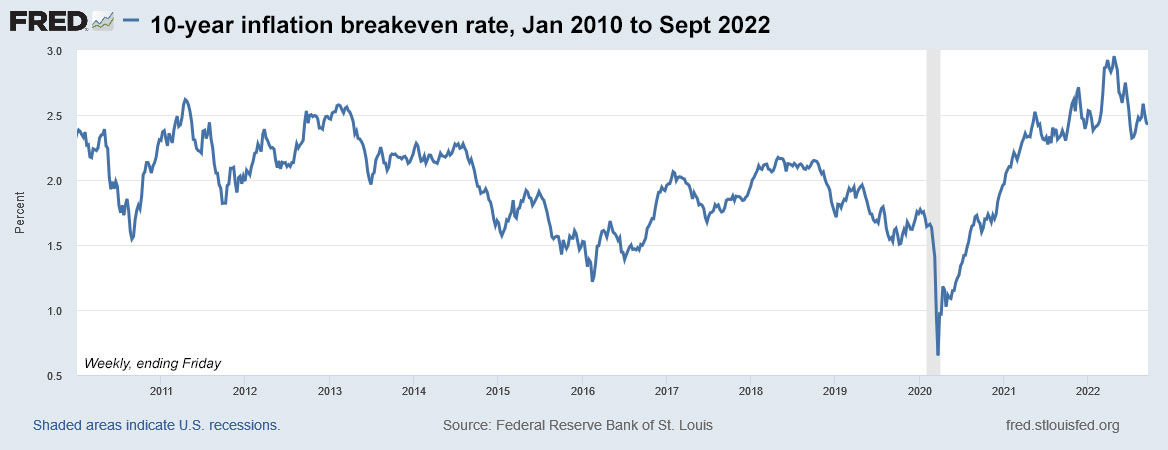

Inflation breakeven rate

With a 10-year nominal Treasury note now trading with a yield of 3.45%, this TIPS currently has an inflation breakeven rate of 2.38%, which looks like a reasonable and attractive number. Inflation over the last 10 years, ending in August, has averaged 2.5%. If you believe that inflation will run lower than 2.38% over the next 9 years, 10 months, buy the nominal Treasury. If you believe inflation will run higher, buy the TIPS.

Here is the trend in the 10-year inflation breakeven rate since January 2010, showing how inflation expectations have been backing off since the Fed began tightening measures in March 2022:

Conclusion

It’s no secret that I am a fan of this auction’s potential, as long as real yields continue to hold throughout this week. That’s no sure thing, with a potential market disruption coming Wednesday when the Federal Reserve announces its decision on short-term interest rates. The market expects a 75-basis-point increase. If that what happens, yields should hold. But a month ago, on Aug. 18, the 10-year real yield was sitting at 0.36%. Anything can happen. In fact: Expect anything to happen.

Anyway, I was a buyer of this TIPS at the originating auction on July 21, and I was pleased with the real yield and coupon rate set at 0.625%, which can help cover the effects of any minor deflationary months. For the hold-to-maturity investor, there is very little risk in this TIPS. Obviously, I will be a buyer Thursday, if conditions hold. This is my opinion, and I am a journalist, not an adviser.

How high could real yields rise? This will depend on how high the Federal Reserve allows nominal rates to rise. If the 10-year note reaches 5%, it’s conceivable that the real yield of a 10-year TIPS could rise to 2.2% to 2.5%. But will the Fed sustain the courage to push rates higher, even if the U.S. economy is in turmoil? My gut says “not likely.”

I know there is also a lot of interest in the new 5-year TIPS auction coming up on Oct. 20. That one could produce a coupon rate of 1% — or maybe even 1.125% — and a real yield of about 1.13%. It will be reopened at auction on December 22, when we will know the full extent of the Federal Reserve’s interest rate decisions. In the last tightening cycle, the December 5-year TIPS reopening auctions were always among the best of the year.

Potential investors in CUSIP 91282CEZ0 can check how it is trading in real time on Bloomberg’s Current Yields page. This auction closes at noon Thursday for non-competitive bids, like those made at TreasuryDirect. If you are putting an order in through a brokerage, make sure to place your order Wednesday or very early Thursday, because brokers cut off auction orders before the noon deadline. I’ll be posting the results soon after the auction closes at 1 p.m. EDT.

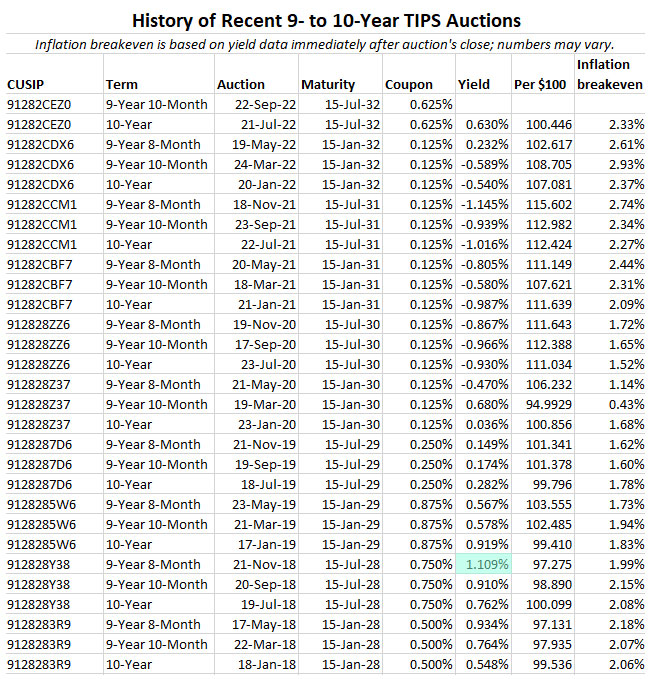

This same 10-year TIPS will be reopened at auction again on Nov. 17, giving investors one more chance at it. Here’s a history of all 9- to 10-year TIPS auctions dating back to January 2018. I have highlighted the single auction, in November 2018, with a real yield above 1%.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

At this point in time, what coupon and real yield does the current market indicate?

The reopening auction this month retains the 0.625% coupon rate and the current market yield is about 1.51%.

If one intends to hold to maturity while disregarding price volatility, then the YTM is most important. The coupon level only affects the price convexity and not the ultimate yield. Agree?

Correct

Wednesday evening update: CUSIP 91282CEZ0 closed Wednesday on the secondary market with a real yield to maturity of 1.16% and a price of $95.09 for $100 of par value. (Tomorrow could be quite volatile.)

Dave,

Would it make sense to just buy this TIPS on the secondary market or perhaps split 1/2 now in secondary and other 1/2 via auction? I originally purchased back the original offering and considering adding to the position.

Thanks as usual,

deeMatrix

I don’t actively buy TIPS on the secondary market, so I can’t say what sort of pricing you will see. Today the real yield has popped up to 1.15%, I notice. If you find a price and terms you like, why not? Just don’t second guess yourself after the auction, if the auction turns out better. (It might not, of course.)

The upcoming 10 year re-opening is certainly a better deal than the original issue that I popped for back in July (not that that was a bad deal).

Unfortunately, I’m getting to the age where going-out 10 years is butting-up against my expected remaining shelf life.

Another poster on this site stated that they use TIPS to provide inflation insurance for their future RMD’s.

Since I thought that was a great idea I’ve adopted the same approach. And, I’ve already allocated that amount to 10 years out (plus a fudge factor).

Due to that I’m afraid that I’ll have to pass on this one in the hopes that the current yields hold-up for the new issue of the 5 year TIPS in October.

Today, I noticed that the 5 year TIPS have an adjusted inflation price of under par (this despite a nearly 5% inflation factor).

Since I didn’t take my entire allocation for the 5 year TIPS that I planned to take back in June’s reopening I’m tempted to purchase some more now.

With the 5 year TIPS original auction only a month away, that probably sounds pretty strange.

But like you’ve pointed-out, the Treasury bond market has been so violatile recently that even a month seems like an eternity.

Speaking of eternity, I wonder how other people factor in their age in making their TIPS purchases.

Once you get over 65, the longevity tables provide a sobering look into what the wonks like to call your “investment time horizon”.

White guys your age have a 98% chance of making it into next year. At my age that drops to 97%.

Cumulative over 10 years, that’s 20% and 30% of the “age cohort” passing into the event horizon of a black hole (my preferred term for dead).

That’s why I really liked that stratedgy of using your RMD as a minimum amount to put into TIPS each year.

The government’s longevity tables are already factored into the RMD amount. So, you don’t even have to do the math.

Thanks for the nice insight. I have a question from the article:

“This auction closes at noon Thursday for non-competitive bids, like those made at TreasuryDirect. If you are putting an order in through a brokerage, make sure to place your order Wednesday or very early Thursday, because brokers cut off auction orders before the noon deadline. I’ll be posting the results soon after the auction closes at 1 p.m. EDT.

This same 10-year TIPS will be reopened at auction again on Nov. 17, giving investors one more chance at it.”

Question: Can you also buy this bond in the secondary market (from a broker) for a similar bid?

Yes, this TIPS trades on the secondary market and you can purchase it through a brokerage. Your price and real yield might vary from what you see listed on the Bloomberg site, based on lot sizes available and the bid-ask spread. The one advantage of buying at an auction is that non-competitive bids always get the “high” real yield (some competitive bidders get less). But sometimes the auction comes in lower than the recent secondary price, so it could be a toss-up.

When a TIP has a real positive yield, if held to maturity, will it always outperform an Ibond with a Fixed Rate of 0%? I think so…making sure.

Not necessarily. It’s highly likely that a TIPS with a real yield of 1% would outperform an I Bond with a fixed rate of 0.0%. But the problem comes with extended periods of deflation. An I Bond’s accrued principal can never decline; it just would earn 0.0% after a period of deflation and then get a nice bounce-back off the 0.0% floor when inflation returns. But with a TIPS, monthly deflation leads to a monthly reductions in accrued principal. When inflation returns, the TIPS would have to recover the deflation losses.

I think one holds a TIPS from issue to maturity one is guaranteed to get back, at the very worst, the original principal thereby offering the same deflation protection as I Bonds.

Correct on a TIPS receiving the original par value if held to maturity, guaranteed. However, because an I Bond can never go down in value over its 30-year term, every penny the I Bond earns in interest is guaranteed to be returned at redemption. The inflation accruals of TIPS can go down in value, which is happening in September and October this year, because of a slight reduction in non-seasonally adjusted inflation. So the I Bonds have superior deflation protection, and I’d actually say “much superior.”

I finally understand your rational for TIPS “But will the Fed sustain the courage to push rates higher, even if the U.S. economy is in turmoil? My gut says “not likely.” I read this as, FED chickens out before inflation is under control.

TIPS have a safety net of maturity. Sounds great.

The stock market has no maturity and no safety net( unless you believe in the plunge control team). Sounds bad.

I have to consider what my “market” positions might do if I accept your scenario, where the real damage could be done to my wealth.

If you are my age, you know how dangerous sustained inflation can be. That is why, as insurance, I allocate a portion of my portfolio to inflation-protected investments. But not the entire portfolio, which still includes mostly plain-Jane stock index funds, total bond funds and some nominal CDs and Treasurys.

I’m 73 and lived through alot of inflation times. Still got a good retirement. I bought some lifetime annuities, 7% payout plus inflation with 45% of my cash funds that are still cooking as the payouts get higher. I always like high payouts using the least amount of money.

At this point – why just not buy a generic TIP ETF or Fund vs. picking a specific security? The whole TIPS complex has been hit very hard … and now that real yields are north of 1%+ (nominal yields = real + expected) are even more attractive. At this point you are getting a nice yield + possible price appreciation. Frankly even the 1Yr hit 4% which is also interesting. Thank you – I’ve learned a lot from your website!!

A fund does not have the safety net of maturity! Cuz like you observed there is lots of downside risk.

That is a fair point. I would say ‘lots’ of downside risk – but yes, there is no set maturity, as the ETF rolls the TIPS exposure. Thank you!

As I noted in my last article, the TIPS funds are a lot more attractive now, but I’d still prefer to buy individual TIPS when I see decent yields and hold them to maturity. I then ignore day-to-day market fluctuations. But I do still own VTIP and SCHP in a traditional IRA.

As an avid reader of your excellent financial journalism over the past 17 years, I owe most everything I’ve learned about TIPS to your insights, your unique ability to clearly convey knowledge, and to the patience and respect you have for your readers. Thank you.

I will also be a buyer at Thursday’s Reopening of this 10 year TIPS, but am also considering buying a 20 year TIPS (through secondary market) while rates are so much better. I’ve waited with dry powder for quite a long time (too long) for better rates and my thinking is that I could push this type of reinvestment risk out 20 years if I lock-in while I can get a fairly decent real rate (1.41% last I looked). What am I possibly not considering on a bond of this duration held to maturity? For example, what’s your “gut feeling” on interest rates in relation to inflation going out next couple of decades? If I read it correctly, your previous post emphasized the fact that the Fed has, since 2008, nearly always kept nominal rates below the inflation rate, unlike the prior 60 years when they were very often kept above the inflation rate. It seems to me that the Fed will have their reasons to continue this fickle trend of the last 15 years over the coming decades however much it punishes savers. Does locking in now on a 20 year TIPS at current rates make any sense if the object is simply to preserve a little buying power and not be worrying whether you’re buying “right at the top” of the current upward rate trend? What other risks am I missing here?

Sure appreciate.

I’ve often said I wish the Treasury would issue new 20-year TIPS, which is probably the longest maturity I would consider. Buying on the secondary market has some complications. That particular TIPS that matures in Feb 2043 was originally a 30-year, so it has built up an inflation index of about 1.288, meaning you’d be buying 28% principal above par. But the coupon rate is 0.625%, so you’d get it as a nice discount, maybe a bit more than $85 for $100 of value. The inflation-adjusted price will be about $109.83. The additional principal isn’t deflation protected.

Thank you, David. So, I’m having trouble getting my head around HOW should I think about the fact that I’d be buying in with the already 28% of principal above par being vulnerable to deflation, whereas if it were a newly issued TIPS, that risk wouldn’t immediately exist going forward. The fact that I can buy this bond at the nice discount is a totally separate aspect/reason for possibly buying, right? That aspect of it simply means I’m getting a heavy discount in exchange for being saddled with the lower coupon rate till maturity, as simple as that, and should have no effect on my thinking regarding the deflation concern, correct? Is all this true? If so, I guess then what I’m asking is: what consideration should I give to the 28% above par being immediately vulnerable to deflation in deciding if I deem this a good investment? Hope all this makes sense, and please forgive my lack of understanding.

Great question! This is not an answer but another question. Seems like safety net in these is maturity at par. I think any time you pay above par it erodes the safety net. I think the seller is making out on this, since they are taking their money now and think its run its course? Seems Kinda like stock options the price is high when volitility is high. I think one buys these thinking inflation will not be tamed.

I don’t worry much about the risk of deflation on my TIPS holdings. The fact is, any TIPS an investor is holding has some amount of inflation accrual above par, and that amount above par isn’t guaranteed to be returned at maturity. For example, I own CUSIP 912810FH6 with a coupon rate of 3.875% and an inflation accrual of 80.2%. That still has 7 years to maturity, so all that accrual is at risk if prolonged deflation hits. I probably wouldn’t buy this on the secondary market (it’s priced at a 20% premium), but I’m also not going to sell it. Many TIPS investors tell me they are nervous about the deflation risk to accruals, but I think the risk is quite small, over the long run.