The 2011 crisis led to an S&P downgrade of U.S. debt. This year could be worse.

By David Enna, Tipswatch.com

When I launched this website back in April 2011, I figured I had chosen one of the most placid and unexciting corners of the investing world: inflation-protected investments. Boring. Staid.

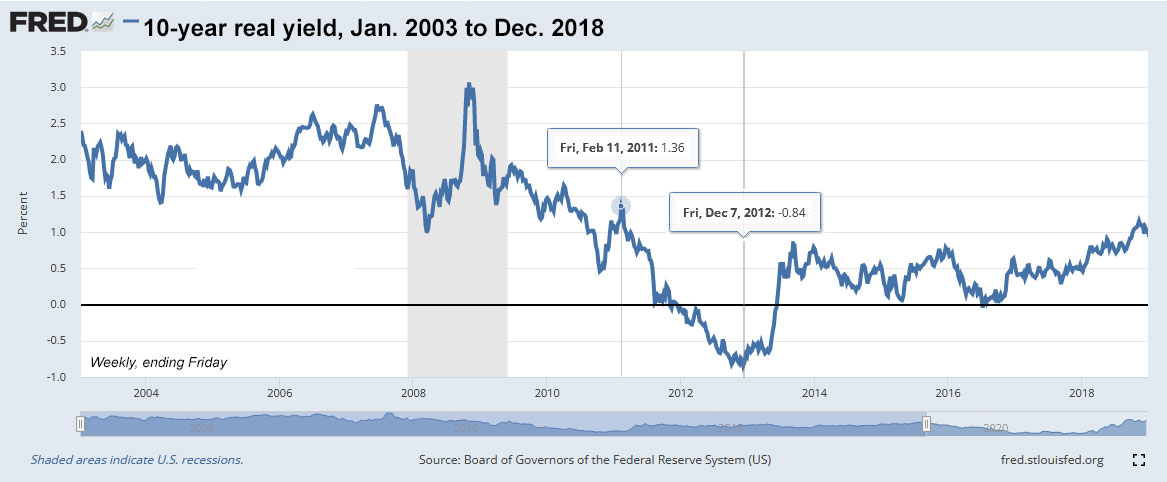

In the days leading up to my first post — on April 10, 2011 — real yields on a 5-year TIPS had started to slip below zero. That was a milestone, and a bit of a shock. But the 10-year TIPS was still yielding a solid 0.96% above inflation.

All of that was about to change. By the end of 2011, the 5-year real yield had plummeted to -0.76% and the 10-year also broke into the negative, at -0.07%. This chart shows the amazing drop in TIPS yields over the course of 2011 and through the entire year of 2012:

In the middle of 2011, something shifted, but why?

Debt-limit crisis of 2011: A monumental event

Back in late 2011, I was quick to blame Federal Reserve manipulation of the Treasury market for the pathetically low yields on TIPS. One of the episodes of quantitative easing had to be behind this sudden shift, right? Wrong.

- QE1 began in November 2008

- A second phase of QE1 began in March 2009

- QE2 began in November 2010

So in the years leading up to 2011-2012, real yields were declining but gradually. Something else happened exactly in late July to early August 2011: A crisis over increasing the U.S. government’s debt limit, the exact crisis we are rolling toward in 2023. A government in crisis; Congressional negotiations heading nowhere. Here are some headlines from that time, which we could see repeated this summer:

- July 22: Obama again presses GOP to move on taxes in debt deal

- July 24: Debt-ceiling standoff grinds on

- July 25: Obama says debt deal must include revenues

- July 26: GOP leaders seek to build support for Boehner debt plan

- July 27: An ‘altar call’ as Boehner pushes GOP for votes

- July 28: House delays vote on Boehner debt plan

- July 29: Obama blasts Boehner debt-ceiling bill, calls for bipartisan deal

- July 29: Amid crisis, TIP ETF hits an all-time high

- July 31: Parties agree to debt-ceiling deal, pending votes in Congress

- Aug. 1: U.S. leaders strike debt deal to avoid default

- Aug. 6: S&P downgrades U.S. credit rating

Yes, on Aug. 6, 2011, for the first time in history, Standard and Poors lowered its rating on U.S. debt from AAA to AA+, with a negative outlook.

Market reaction

Global stock markets declined on August 8, 2011, following the S&P announcement. All three major U.S. stock indexes declined 5% to 7% percent in one day. However, U.S. Treasurys, which had been the subject of the downgrade, actually rose in price and the dollar gained in value. The flight to safety was on.

This chart compares the performance of the TIP ETF, the long-term Treasury ETF (TLT) and the S&P 500 (SPY). It shows how the market earthquake struck precisely in mid 2011 and hit Treasuries (positively) and stocks (negatively):

Fear was the trigger: The stock market dropped and Treasurys soared. The Federal Reserved stepped in – one month later – to begin Operation Twist, selling short-term debt and using the money to buy longer-term debt. The intent was to flatten the yield curve (a problem that does not need fixing in 2023).

One last chart shows the massive moves in Treasurys and the stock market in a single month, August 2011:

What is truly remarkable is that Treasury investments thrived amid this debt crisis and the downgrade from Standard and Poors. Fear was the driving force, and U.S. Treasurys were again shown to be the world’s premier “safety-first” investment.

2023: ‘This time is different’

Here we are, in March 2023, rolling toward the exact crisis we saw in 2011. Just like then, we have a Democratic president and a divided Congress (in 2011, by the way, Vice President Joe Biden was serving as the Senate President). But this isn’t a deja vu event. Things are quite different:

- A divided Republican party. I am trying to avoid making this about politics, but it’s clear that about 20 House Republicans will attempt to block any attempt to raise the debt ceiling, right to the brink of disaster.

- A no-compromise Democratic Party. Democratic leaders are strongly opposed to cuts in spending for social programs, including Social Security and Medicare. Most Democrats are refusing to even discuss spending cuts. A compromise will be very difficult to achieve in 2023.

- Where’s the middle ground? It’s going to take middle-of-the-road Republicans and Democrats to break from party pressure to reach a debt-limit agreement. In 2011, a lot of people were talking compromise. In 2023, you can hear crickets.

- A hamstrung Federal Reserve. U.S. inflation is likely to continue running well above the Fed’s target of 2% all summer. The Fed has limited ability to step in to support the bond or stock markets, even if disaster looms.

- A volatile Treasury market. In June 2011, the 10-year note was yielding 2.96%, very close to what it was a year earlier, 3.29%. Today, the 10-year is at 3.97%, up 211 basis points from one year earlier. This market is now more unpredictable and less steady than it was in 2011.

- A weakening economy. As interest rates continue to climb, many economists have been sounding the alarm about a looming recession. In 2011, the U.S. stock market was able to recover fairly quickly from the debt crisis, with the S&P 500 posting a total return of 16% in 2012 and 32% in 2013. There’s a lot more risk in 2023 with stocks still at fairly high valuations and the economy on a tightrope.

On the positive side, Biden has skills at negotiating a Congressional compromise. Eventually, both sides will probably have to “give” — a little.

Also interesting: Current Fed President Jay Powell played a key role is settling the 2011 debt crisis. At the time, Powell was a former Treasury official who was working for $1 a year as a visiting scholar at the Bipartisan Policy Center. Powell used his influence to help settle the issue, as CNN note in a recent article.

NPR’s Planet Money did a podcast recently on Powell’s role in 2011. Give it a listen:

Worst-case scenarios

A lot of readers have been asking me what will happen if the debt-ceiling negotiations fail and the U.S. government goes into debt-lock. My answer is: I don’t know. Will I Bonds continue to be issued? Will the United States continue paying interest on its debt? Will the U.S. pay out maturing Treasurys? Will Social Security payments get slashed? I don’t know.

The most probable outcome, in my opinion, is that we will come to the brink of debt disaster — and maybe even take a quick leap off the cliff — before Congress settles the issue by kicking the can down the road. Maybe Democrats will need to bend on some future spending cuts. Maybe Republicans will have to silence the ultra-hawks.

The Brookings Institution earlier this year issued a paper titled, “How worried should we be if the debt ceiling isn’t lifted?” It starts off with a bang:

“Once again, the debt ceiling is in the news and a cause for concern. If the debt ceiling binds, and the U.S. Treasury does not have the ability to pay its obligations, the negative economic effects would quickly mount and risk triggering a deep recession.”

In speculating on how a debt-lock could be handled, the authors note that the U.S. government created a contingency plan in 2011 at the height of the crisis:

“Under the plan, there would be no default on Treasury securities. Treasury would continue to pay interest on those Treasury securities as it comes due. And, as securities mature, Treasury would pay that principal by auctioning new securities for the same amount (and thus not increasing the overall stock of debt held by the public). Treasury would delay payments for all other obligations until it had at least enough cash to pay a full day’s obligations. In other words, it will delay payments to agencies, contractors, Social Security beneficiaries, and Medicare providers rather than attempting to pick and choose which payments to make that are due on a given day.”

You can read the full contingency plan here.

The Brookings paper also speculates on the level of non-interest spending cuts needed if the government goes into debt-lock:

“If the debt limit binds, and the Treasury were to make interest payments, then other outlays will have to be cut in an average month by about 20%.”

And it continues with this grim scenario:

“If the impasse were to drag on, market conditions would likely worsen with each passing day. Concerns about a default would grow with mounting legal and political pressures as Treasury security holders were prioritized above others to whom the federal government had obligations.

“In a worst-case scenario, at some point Treasury would be forced to delay a payment of interest or principal on U.S. debt. Such an outright default on Treasury securities would very likely result in severe disruption to the Treasury securities market with acute spillovers to other financial markets and to the cost and availability of credit to households and businesses. Those developments could undermine the reputation of the Treasury market as the safest and most liquid in the world. “

This Brookings scenario seems to indicate that Treasurys (and savings bonds) would continue to pay interest and continue to be issued in at least scaled-back form. All other government spending would be at risk. It’s highly likely we would see severe disruptions in the stock and bond markets.

Final thoughts

I am going to move forward trusting that a solution (although a temporary one) will be found for 2023’s version of the debt-ceiling crisis. But this is going to get ugly. Fasten your seat belts.

Note: Comments are welcome, but keep them constructive. No political flame-throwing will be allowed. However, politics is the issue today; so just keep comments on the topic and focused on solutions.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

David, do you have any ideas if the Brookings’ worst-case scenario happened? In the case of any substantial loss of confidence in US Dollars and Debt backed in faith by the US Treasury, perhaps some Canadian (or take your pick) government bonds or government- issued precious metal coins in hand would be prudent?

I hate to say this, but my theory is that eventually the world’s financial focus would turn to Asia.

From the field reports from some equipment manufacturers and suppliers in Asia, I believe there is credence to this. There are countries with large populations and growth acting as well-organized giant corporations and not looking to fail for a long time.

Thanks David for the excellent article. Your work is always good but I found this unusually insightful.

I was working on Capitol Hill in 2011. I worry about 2 things:

1. The nature of the House Speaker election in January was a test vote for default.

2. Biden’s lesson from 2011 is not to compromise. I think many Democrats involved in that compromise feel like there was not a honest negotiation. There were honest participants from both parties on the supercommittee, but it became obvious quickly that it was set up to fail, despite the existence of the Simpson-Bowles report. There was no leadership from the top of Congress and there is a huge theological chasm between “government helps people” and “Government is the problem. And no taxes.”

For a compromise, both sides need to offer solutions.

Maybe we will yet see one out of the House. But I am not sanguine. Republican caucus dynamics are brutal (see: speaker election). Holding defense spending and entitlements constant while eschewing tax increases makes the math pretty much unworkable. Maybe that is just an opening bid. We’ll see …

Thank you for this excellent feedback.

Thank you David, for the historical context. While many 1-3 year FDIC-insured CDs at 5.25% being offered thru my brokerage are somewhat tempting, i still view TIPS as being a “safer” bet. So I’m filling in my TIPS ladders now, getting YTMs at 1.7% – 2.2%.

Debt will ALWAYS be inflated away in the end. That is the main lesson history is trying to teach mankind.

That said, I wonder about the availability of TIPs. I can imagine the Treasury in the future no longer wanting to sells TIPs, but only fixed rate bonds.

“Maybe Democrats will need to bend on some future spending cuts”

Maybe Republicans will need to bend on some of the absurd aspects of the Trump tax cuts.

Ron Johnson refused to sign on until there was a provision that reduced taxes on passive income, benefitting the wealthy like Johnson and Trump

And since corporations managed to spend $5.6 TRILLION on stock buybacks in the decade prior to the TCJA, perhaps they didn’t NEED the reduction in their tax rate?

In 1950, corporate taxes were 6% of GDP. Now they’re less than 1%

In fact, at some point, the massive redistribution in wealth and income between the top 1% and the bottom 90% since 1980 needs to be reversed. For example, in 1980 the top 1% had 9% of national income. Now they have 25%

Republican tax cuts for the wealthy are responsible.

There are more of “us” than them, wake up people

It is neither tax cuts or tax increases that are the solution. Because taxes are just a redistribution system. It doesn’t really add anything of value.

The only thing that adds value to an economy is the productive capacity of its people. In layman terms: jobs. The more (well-paying) jobs, the better the economy.

Unfortunately, as long as there is an incentive to ship jobs oversees, the economic situation is not going to change. No matter how many tax cuts or tax increases.

“It is neither tax cuts or tax increases that are the solution. Because taxes are just a redistribution system.”

False for several reasons

Lowering taxes has exactly the same effect as the government handing out money

Tax reductions have the exact same effect as equal increase spending. Both increase the national debt by the same amount

And the national debt has impact for both the current and future generations.

As for redistribution, I’ve just started to indicate how income and wealth HAVE BEEN REDISTRIBUTED FOR 40 YEARS, towards the wealthy and away from everyone else.

Here’s a start for your reading list:

I do wonder if this will lead to an increase in the I Bond fixed rate. Another speculative article has this author thinking of a fixed rate at 1%, which I think is highly unlikely: https://archive.is/5FuBR

I do think the I Bond fixed rate will increase on May 1, but probably not because of the debt crisis. Something around 0.8% seems logical, but it’s impossible to predict.

Hello David, Will you have more to say about this before May 1?

Rob, I’ll be trying to analyze and “predict” the next fixed rate after the March inflation report comes out on April 12. At that point we will know the next variable rate.

How does this issue affect any liquid cash we have in our bank checking/savings accounts? Would they be difficult to access/withdraw to pay bills?

I’d assume these accounts would not be affected.

Unaffected as long as you stay under the FDIC insurance limit, $250,000, which can be higher depending on various scenarios.

FDIC insurance provides you will be paid back “as soon as possible”

https://www.fdic.gov/consumers/banking/facts/payment.html

No bank could survive if everyone who has money on deposit came in to withdraw their money. We have a “fractional banking system”

https://corporatefinanceinstitute.com/resources/economics/fractional-banking/

Banks are allowed to lend out as much as 85 of their deposits (I don’t know the precise ratio, I’m relying on memory, the current ratio is set by the Federal Reserve. So no bank could survive if everyone who has money on deposit came in to withdraw their money.

The FDIC insurance is funded by the banks it covers, and if there was a run on the banks, there’s not enough money held by the FDIC to pay everyone.

The assumption is that everyone WILL get paid back because of an implied guarantee by the “full faith and credit of the US”

Which of course isn’t going to be there

https://www.thebalancemoney.com/what-is-the-fdic-315786#:~:text=FDIC%20insurance%20is%20funded%20by%20the%20banks%20that,insurance%20coverage%20pay%20a%20premium%20for%20their%20coverage.

“Funding Deposit Insurance

FDIC insurance is funded by the banks that are insured. It’s similar to your auto or home insurance—the banks receiving insurance coverage pay a premium for their coverage. Another similarity to other forms of insurance is that the premiums charged are assessed by the riskiness of the bank.2 That prevents any single bank from abusing the system and taking unnecessary risks with the expectation that other banks will clean up their mess if they fail. The more risks a bank takes, the more they have to pay for FDIC insurance.

Although it is self-funded through premiums, FDIC insurance is “backed by the full faith and credit of the U.S. government.”3 The assumption is that the U.S. Treasury would step in if the FDIC insurance fund were to run out of money, but as of September 2020, this scenario has not been tested.”

Title 31 United States Code § 5112 (k):

The Secretary may mint and issue bullion and proof platinum coins in accordance with such specifications, designs, varieties, quantities, denominations, and inscriptions as the Secretary, in the Secretary’s discretion, may prescribe from time to time.

Ah, the Trillion Dollar coin scheme

Oops! There goes the US dollar’s role as the world’s reserve currency

And there go all the advantages that come from having the world’s reserve currency

Ah yes, the downgrade. I got a kick out of remembering Geithner saying in April there was no chance of it:

“(US could lose AAA credit rating?) no risk of that, no risk….(S&P is wrong, US will keep its AAA credit rating?) absolutely.

-Tim Geithner, US Treasury Secretary, April 19, 2011 – Fox Business Interview – HYPERLINK “http://video.foxbusiness.com/v/4651704/geithner-no-risk-us-will-lose-aaa-credit-rating/?playlist_id=87185”

I admire your attempt to be bipartisan, when discussing this issue, since the main purpose here is to discuss our inflation-protected investments.

Reasonable people agree that it’s important for the federal government to address the ever-growing national debt. Likewise, most agree that it’s problematic (actually dangerous) to do so in the context of raising the debt ceiling. The reason it’s impossible to avoid politics in this discussion is because the entire crisis is politically-driven. It’s not a coincidence that the last time this happened, the political configuration was the same. There is no actual crisis, there is only an invented one. The federal government must pay the debt it has already incurred. It’s not difficult and it’s not a choice. It’s the only responsible course of action.

The obscene national debt is a function of excessive accumulated annual deficits dating back to the 1980s. If you can’t reduce/eliminate the annual deficit and generate a surplus by reducing spending and/or generating more revenues through taxes or economic growth, it’s difficult to meaningfully reduce the national debt. That’s why the proper context for addressing the issue is not a choice between political parties, but rather a function of timing. It should be addressed during the budget process in times when the economy is doing well, regardless of which party is in power at the time, not during the debt ceiling process in a time when we have elevated inflation caused by the pandemic reopening, supply chain issues, and disruptions caused by Russia’s war in Ukraine.

Both political parties understand that it is irresponsible to jeopardize the full faith and credit of the U.S. Government for political advantage, but here we are again. If we go over the fiscal cliff, it would be an epic failure of leadership and responsible governance. The consequences of doing so are financially unacceptable and politically unviable. That is why it ultimately will not happen.

Thank you for contextualizing the discussion in terms of how a situation that should never happen would impact our investments. The contingency plan is fascinating, reassuring, and scary all at the same time. The only way I can think of to avoid this from becoming Groundhog’s Day in the future is to institute term limits. We have to find ways to put our country’s well-being before the interests of political parties to remain or regain power.

When a corporation goes bankrupt, bond holders get paid first. Of course the U.S. government is not a corporation. I have read that countries cannot actually go bankrupt. David has nicely outlined some of the consequences of a default on the U.S. debt in the past, in a different economic environment compared with today. What bothers me, and should bother others, are the unknown consequences of a default today. These are consequences we won’t know until the event happens, something like unintended consequences.

Having said that, I am fairly certain Congress will not allow such a default, if for no reason other than most in Congress are what we would call rich and well-off or are controlled by the rich and well-off, and they do not really want to jeopardize their net worth or the net worth of their controllers.

The well-off will fight tooth and nail to prevent any increases to their taxes. The well-off will fight tooth and nail to weaken any favorable tax laws in maintaining generational wealth passage to their heirs. Many on both sides were all-in on the big tax cut that most favored the well-off. If articles written by respected journalists about the largess of taxes owed and uncollected by the well-off are close to true, that’s money that could be used to pay down some on the couuntry’s huge debt. To me it comes down to a question of morality, that is should those who have done extremely well financially through family connections, birthright privilege, top flight tax/legal advice (and yes sometimes honest effort), not have a moral obligation to give back some more financially to their country through taxation than they have for a long, long time.

If you lucked out and made a lot of money and want to give it away, you set up a charitable foundation. “There is no federal inheritance tax, but there is a federal estate tax. The federal estate tax generally applies to assets over $12.06 million in 2022 and $12.92 million in 2023, and the estate tax rate ranges from 18% to 40%.”

Just FYI, the federal estate and gift tax exemptions are due to sunset in at the end of 2025, and then would drop to something like $6.2 million, and the maximum estate tax is due to rise to 45%. Also after 2025, the so-called “Trump tax cuts” are due to end, along with the $10,000 limit on state and local tax exemptions. Will that happen? Seems highly unlikely. House Republicans have already proposed legislation to make the tax cuts permanent. Maybe Democrats will try to get rid of the $10,000 limit on state and local taxes? So, does anyone actually think Congress is serious about deficit reduction when this is going on?

Quite frankly, every time I hear talk of “reforming” Social Security, I have to cringe. There’s been studies showing that Social Security could remain solvent thru 2095 simply by raising the payroll tax rate from 6.2% to 8.1%. This approach was done in both 1977 and 1983.

Politicians seeking to limit Social Security payments just want to use the “current” crisis as an excuse to eventually eliminate Social Security entirely. This all started with Reagan wanting to make Social Security a voluntary program. Then Bush sought to privatize it.

Those same politicians created a national debt crisis by cutting taxes without making any spending offsets. Then they hold the country hostage by refusing to raise the debt ceiling for government spending that has already been passed by Congress. Then they blame Social Security!

The whole thing is a huge red herring. Social Security is paid via payroll taxes and the trust fund. Some people like to distort reality by saying that the trust fund doesn’t really exist. This is despite the fact that the trust fund consists of Treasury obligations.

The real problem is that those bonds are now being redeemed to cover the shortfall that’ Social Security is now experiencing. Paying back Social Security means that the government can’t use those funds to cover the government’s general fund spending.

Actually, the real problem is the politicians that don’t want to honor the commitments made in the past. It starts with refusing to raise the debt ceiling. It continues with refusing to raise payroll taxes to keep Social Security solvent.

Social Security has always been based on payroll taxes. Despite Reagan calling it welfare, it’s not. Baby boomers paid extra into the system over the last 40 years to create the trust fund surplus. If that’s not adequate, get rid of the wage cap that panders to the rich.

The average Social Security payment is a paltry $1500 a month. The 3 million people who make up the wealthiest 1% of Americans are collectively worth more than the 291 million that make up the bottom 90%. Yup, let’s give them tax breaks and use the deficit argument to cut Social Security.

Thank you for the usual excellent content. Good reminder to Prepare for dramatic and volatile scenario.

Even “protected” securities such as TIPS and I Bonds will suffer if they cannot be redeemed or the interest cannot be paid. Since all paper/digital “wealth” will be unreachable or at least far decreased in value, that leaves things with a perceived “store of value” which can be used as barter. No wonder Gold spiked in 2012. De Ja Vu? Also, seems all China (and a few others) have to do to dominate us is to wait this thing out.

One area I didn’t get into is that defense spending would be frozen (or at least slashed) by a debt lock. Would China, North Korea and Russia attempt to take advantage of that crisis?

NPR’s “Planet Money” podcast ran a story recently on Chairman Powell’s role in the ’11 debt ceiling standoff that i thought was interesting, worth a listen

Thanks for this tip. I am adding a link in the article.

Hi David:

Thank you so much for such an eloquent and very informative article. I was CAPTIVATED from the start.

The information you provided is of utmost importance to those of us who hold positions in US Treasury Securities.

You are 100% on point. This time around will be different than summer 2011. President Biden is well equipped (experience wise) this time around to negotiate a deal before financial and economic consequences.

The thought of a contingency plan (I had no idea one existed) makes feel better about my Treasury Securities.

-With gratitude + utmost respect

David,

Very nice re-cap of history. One suggestion for possible correction, “is that will we come to the brink ” did you intend “will we” or should it be “we will”? I do not mean to be a toad, I understand how it could be presented either way and I am happy with your decision in either direction.

It’s great to see someone is reading so carefully. Thanks for the alert and it is fixed.

The Democrats will not compromise. They want a default or near default. They need cover for the financial train wreck coming from their endless spending and give aways. Not just to lay blame on the Democrats-the financial shenanigans and miss management has been building for decades under both parties. By drawing a line in the sand now on not negotiating on “Paying our debts” all the results of the coming financial chaos, that is inevitable whether or not we raise the debt limit, can be blamed on the Republicans. It is a win-win for them. Also as the party of “Never let a crisis go to waste” they can see the endless social engineering and spending they can do to “Rescue” our economy.

Sigh.

Conclusion from this good analysis: “Whose fault is the debt? Everyone, really. Not useful for political jockeying, but important to know.”

https://www.washingtonpost.com/politics/2023/02/07/debt-republicans-democrats-trump-biden/

SS has never and can (undercurrent law) not borrow a dime. It has funding problems of its own and need to be addressed. If not it will self correct.

The general budget has a problem tax cut AND out of control spending have created a 31T debt.

The two problems should be addressed separately as SS cannot solve the debt problem and the budget cannot (by law) solve the SS problem.

See. https://shawnpheneghan.wordpress.com/2023/02/15/straight-talk-on-social-security/

Politicians seeking to limit Social Security payments are more concerned about limiting future debt obligations in the big picture. By law, Social Security does have a solution to its problem — automatically cutting payments by about 25% sometime around 2032. But that is politically undesirable and few politicians seem to be willing to compromise to address the issue.

Cutting Social Security benefits (either directly or by “back door” methods such as increasing the age to collect a “full” benefit) is, of course, the Republican approach.

Another is to increase Social Security’s revenue base. There is a cap on the amount of annual earnings subject to the tax which supports Social Security. In 2023 it’s $160,200. So a person with salary earnings of $1,602,000 or $16,020,000 doesn’t pay a dime more Social Security tax than a person earning that $160,200. This is among the many ways the national tax code allows the rich to opt out of supporting the common good.

A 2020 report of the Senate Special Committee on Aging, exploring various methods of strengthening Social Security, found that elimination of that salary cap would, by itself, in the absence of any other program changes, resolve nearly all of Social Security’s funding problems for 75 years. See discussion beginning on p. 46 of the downloadable PDF version of the report, here:

https://www.congress.gov/congressional-report/111th-congress/senate-report/187

And that is aside from the fact the weathy derive a disproportionate amount of their income from financial speculation and other income sources which, because they are not “wages,” are not subject to the Social Security tax.

So whenever I hear anyone suggesting benefit cuts, I remember that Senate report and think: Eliminate the cap FIRST and then we can talk about whether any further actions are needed to “strengthen” Social Security withOUT weakening its benefits.

Although Social Security is a tangential part of this discussion since it has been taken off the table, first by Democrats, and then very publicly (whether intentionally or not) by Republicans at the State of the Union address, I think you’ve summarized the issues well. There is no doubt adjustments need to be made to continue to fund the program, just as there have been in the past. This is nothing new, and will happen outside of the process of raising the debt ceiling.

The political problem with lifting the cap is that it becomes a tax increase for those earning more and less than $400,000 a year (and above $162,000 a year) which President Biden has continually reiterated he won’t do and which Republicans are not inclined to do. So either Biden goes back on his word to support that in the context of shoring up Social Security and taxing the wealthy (even though it will also tax those not considered that wealthy), which is one of the things that doomed President George HW Bush’s re-election (read my lips), or another solution will need to be found.

The Social Security tax is a regressive tax because everyone pays the same rate up to the $162,000 limit. Perhaps a way to accomplish the goal would be to cut some discretionary spending and at the same time cut taxes on those making less than $400,000 a year, as well as change the Social Security tax into a progressive tax with escalating percentage ranges just like the Income tax. If it could be worked out that the net tax impact on those making less than $400,000 would be the same or lower, I think that would satisfy all parties (in theory).

My non-partisan view is that the two easiest things for Congress to do are: 1) raising spending and 2) cutting taxes. So there will be very little support for cutting spending (except for Republicans) and raising taxes (except for Democrats). Social Security is definitely a revenue issue, so raising the income cap looks like a necessity. Democrats would probably suggest leaving the $160,000 cap and then reinstating it for income above $400,000. Republicans would fight that. But something has to be done. Also: 1) very gradually increase the “full benefit” age, which is currently about 67. 2) Start making 100% of SS payments federally taxable, instead of just 85% for people with higher incomes. 3) Potentially start limiting benefits for higher-income people.

I don’t think it’s viable to raise full retirement age (again), which is a cut to Social Security, now that U.S. life expectancy is at its lowest level since 1996 — 76.1 years. The 0.9 year drop in life expectancy in 2021, along with a 1.8 year drop in 2020, attributable in large part to Covid, was the biggest two-year decline in life expectancy since 1921-1923. That’s not the way you want to extend the program, but that is one unintended consequence of the pandemic. As it stands now, beginning retirement at full retirement age doesn’t even equate to a averageten year retirement (67 to 76). The other ideas, IMO, are more likely.

Those with family histories of longer life expectancy can never be sure when their time is going to end. Covid helped drop life expectancy numbers, and I think of busy actuaries updating life expectancy tables. The financial media likes to bang the drum on Social Security about “wait till seventy to draw” if you can. In France and elsewhere, they get in an uproar over talk of raising the age to retirement and benefits. People everywhere realize life is very uncertain and big health issues can come up unexpected. I’m in that situation now. After you’ve lived long enough to see family/extended family/friends/people in-the-news, dying at ages unexpected – you come to realize (and likely have well before), that there is a narrow window to enjoy retirement in a relatively healthy state before things start to breakdown. Also let’s be realistic, some have great medical care and many have so-so medical care. We who have worked so long to enjoy some retirement years, should not suffer the worry that the rug will be pulled from under their feet by some wealthy politicians seeking to divide the American people.

The problem with Social Security is that for decades, it was handing out cash to “freeloaders” (early retirees) who didn’t pay a dime in taxes into the trust fund. And now that the cash is running low, future generation are supposedly to pay more and more into it so current retirees can live the high life??? Must be joking. Although I expect nothing less from a geriatric congress…

It has been 40 quarters to collect benefits for as long as I can remember.

Not paying a dime is inaccurate but… SS retirement benefits can be and are being seriously gamed. ( https://shawnpheneghan.wordpress.com/2019/11/25/gaming-social-security/ ).