By David Enna, Tipswatch.com

The U.S. Treasury on Thursday will auction $21 billion of a new 5-year Treasury Inflation-Protected Security, CUSIP 91282CGW5. The coupon rate and real yield to maturity will be set by the auction results.

For months, I have been considering this auction as a sure-fire purchase, because my TIPS ladder is quite weak for the year this one matures, 2028. I will still be a buyer, but I can see why some investors might opt out. There are equally safe and equally attractive nominal investments out there. And that makes this investment decision complicated.

As of Friday, the U.S. Treasury was estimating the real yield (meaning the yield above inflation) of a 5-year TIPS at 1.29%, well below the 2023-high of 1.87%, set on March 8 just before the Silicon Valley Bank collapse. But 1.29% is okay, in my opinion. Take a look at 5-year real yields over the last 8 years:

After a decade-plus of extremely low or even negative real yields, I can’t complain about getting 1.29% above inflation. It’s fine.

The complicating issue is that you can capture nominal yields with non-callable 5-year bank CDs — either direct or brokered — that are competitive with this 5-year TIPS. A best-in-nation 5-year CD paying around 4.50% creates an inflation breakeven rate of 3.21% against this TIPS, meaning the CD will out-perform if inflation averages less than 3.21% over the next five years.

Will inflation average more than 3.21% through April 2028? I think it’s possible, even likely, but it is going to be close. The CD also looks like a sensible investment. However, forget about the 5-year nominal Treasury note, with a current yield of just 3.60%. The CD and TIPS are much more attractive.

This chart shows how each 5-year investment will perform under different inflation scenarios. At low inflation rates, the bank CD is the winner, with even better real returns if deflation strikes. When inflation rises above 3.21%, the TIPS is the winner, with unlimited upside potential if severe inflation strikes. But there is no scenario where the 5-year Treasury note is the winner.

One thing to consider is that interest from TIPS is exempt from state income taxes, which isn’t true for bank CDs. But if you are putting these in a tax-exempt account, that issue is moot.

So is this Thursday’s 5-year TIPS auction attractive? Yes, it is, as long as real yields hold around current levels through the week. But you could consider pairing it with nominal investments like T-bills (paying 5%+ for a six-month term) or solid bank CDs (paying around 5.15% for 1 year or 4.50% for 5 years.)

Or, just buy the TIPS. It will do fine if you hold it to maturity.

Pricing

If the real yield holds at 1.29%, this new TIPS will get a coupon rate of 1.25% and should be priced just below par. It also will carry an inflation index of 1.00241 on the settlement date of April 28. So at this point the price should be very close to $100 for $100 of par. There will also be a very small amount of accrued interest.

Inflation breakeven rate

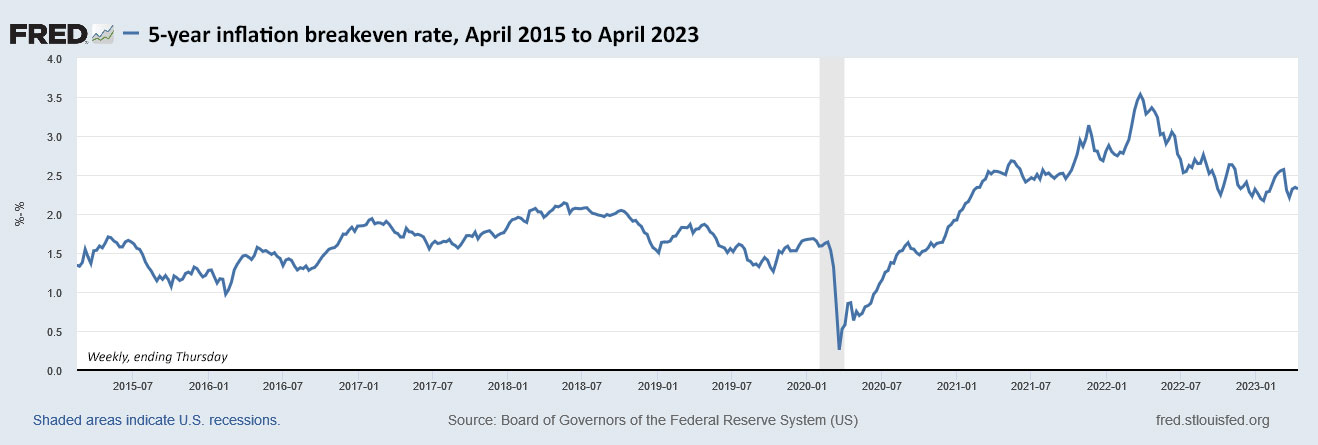

The official inflation breakeven rate will be set by the spread in yield between the 5-year Treasury note (currently yielding 3.60%) and the TIPS real yield (let’s estimate 1.29%). That creates an inflation breakeven rate of 2.31%, fairly high by historical standards but fairly low compared with recent auctions.

Here is the trend in the 5-year inflation breakeven rate over the last 8 years:

U.S. inflation has been trending downward over the last year, going from an annual rate of 9.1% in June 2022 to 5.0% in March 2023. I think that trend will continue for several more months before stabilizing around 3.5%. But that is a guess, of course. No one can accurately predict future inflation.

Over the last 5 years, U.S. inflation has averaged 3.3%.

Final thoughts

Although I still plan to be a buyer at this auction, on April 10 I took half of my planned investment and bought a non-callable 5-year brokered CD yielding 4.61%. It’s hard to pass up these attractive nominal yields, even for an inflation-fighter like me.

We are finally in a prosperous time for ultra-safe fixed-income investing, something we didn’t see for more than a decade. Will this trend continue for years? Possibly. I hope so. But enjoy it while it lasts.

If you are considering bidding at Thursday’s auction, keep an eye on the Treasury’s Yield Curve estimates, which update at the close of the market each day. Non-competitive bids at TreasuryDirect must be placed by noon Thursday. If you are putting an order in through a brokerage, make sure to place your order Wednesday or very early Thursday, because brokers cut off auction orders before the noon deadline.

What are your thoughts on this TIPS auction? Post your comments below.

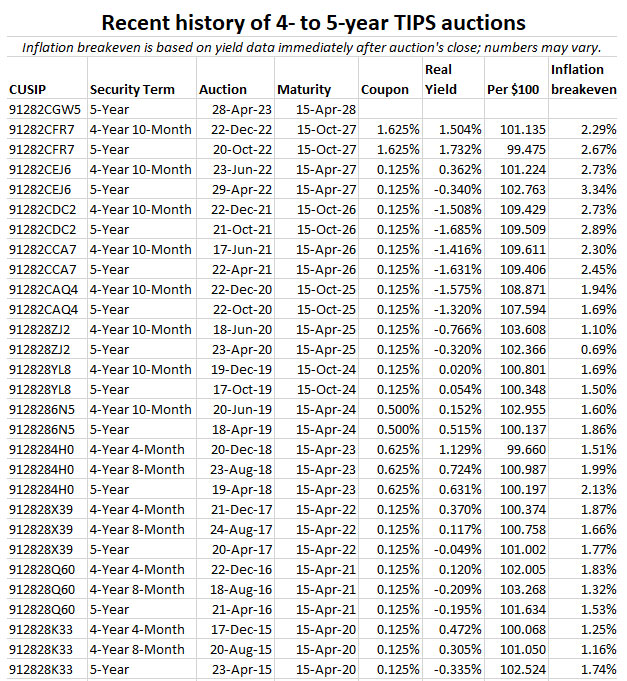

I’ll be posting results Thursday after the auction closes at 1 p.m. EDT. Here is a look at auctions of this term back to 2015. Note that you only have to go back one year, to April 29, 2022, to find a negative real yield:

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• Upcoming schedule of TIPS auctions

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Hi, thank you so much for this very helpful site! I bought actual TIPS for the first time today, this 5-year issue. Schwab says Settle Date: 04/28/2023. So does that mean I can sell my SWVXX money market fund the day before to generate the proceeds in time? Thanks!

The settlement date is 4/28, that is correct. Maybe raise the cash on April 26th, just to be safe?

Great, thanks! And it looks like the order went through. What do you calculate the final yield over inflation to be? The issue name says “1.25%” – is that accurate for those who bought the initial issue at market?

JBR, the real yield to maturity is 1.32%. You are buying that 1.25% coupon rate at a discount.

In my experience with Fidelity, they will help themselves to the money from your money market fund at settlement

That’s what Fidelity has always done when I was purchasing Treasury securities, CDs, or stocks

Best to call and verify

So David, what’s your take on tomorrow’s auction at this point? Thanks in advance for any perspective.

I put my order in yesterday, because this looks good enough. The Treasury Real Yield estimate closed today at 1.38%; that’s fine. This auction could be tricky though because it is $21 billion of new supply, which gives big-money investors a chance to go big, which would lower the real yield. I know from experience that auctions can get tricky … We’ll see.

Here is a massive fan of TIPS – a billionaire banker no less.

https://www.marketwatch.com/story/andy-beal-americas-richest-banker-makes-a-massive-bond-bet-on-inflation-f524dc1e?mod=home-page

This came up in another article’s comment section. The Morningstar article is strange, in my opinion. It says Beal quadrupled the bank’s assets by buying TIPS, but anyone who has been buying TIPS knows their value hasn’t quadrupled in a year. We’re looking at total returns of maybe 5% over the last year. Even if you figure he captured 1.5% above inflation, he would have about a 6.5% return. So there was a lot more going on at Beal Bank.

To all: If the yield is near the 1.375 level just before the auction, would you agree that this auction might be worth throwing an “overweighted” investment into?

Looks like the coupon might be a lot higher than it looked just a few days ago, based on CNBC website:

Yes, 1.375% is now a possibility

Came at a 1.32% yield

Treasury release on auction results:

Click to access R_20230420_3.pdf

Harry, I have posted my article on the auction: https://tipswatch.com/2023/04/20/new-5-year-tips-gets-a-real-yield-of-1-32-an-attractive-result/

Thanks!

And thanks again for your excellent blog!

Real yields are on the rise

04/13/2023 1.22 1.18 1.16 1.29 1.40

04/14/2023 1.29 1.25 1.22 1.34 1.46

04/17/2023 1.34 1.30 1.28 1.41 1.52

If the real yields continue to rise into Wednesday what that may mean for the Thursday TIPS auction?

This is a good trend, but the TIPS market is constantly in flux. So what goes up can come down. I like what we are seeing today.

I’m wondering if yields have resumed their march upwards after the banking interruption of March. Now the May Fed increase seems to be certain and markets are also starting to price an increase in June..

It’s possible, but both real and nominal yields have been volatile — up and down — over the last year. We’re still not near the highest yields we saw last fall. So there is room to go higher.

Hello. In your comparison between a 5 year CD and the upcoming 5-year TIPS, you stated: “the CD will out-perform if inflation averages less than 3.21% over the next five years.” But I’m confused as to why the coupon rate of the TIPS isn’t a factor in this calculation as well. If the real yield of the TIPS is 1.29% and the coupon rate ends up being 1.25%, doesn’t that effectually mean that inflation would only need to average more than 1.96% for the TIPS to outperform the CD? (I’m taking 4.5% for the CD and subtracting the sum of the real yield and the coupon rate of the TIPS–but maybe this isn’t how it works, I’m confused).

The reason: The coupon rate is already factored into the real yield to maturity.

I see. Thank you for the reply. I’ve really enjoyed reading through all of the great information that you’ve provided. If you have a post explaining how the real yield on a TIPS is calculated, could you post a link to it?

Funny story on this: I once spent an hour talking to a Wall Street Journal reporter about TIPS and the importance of real yield. He just couldn’t get it, and ended up leaving out real yield entirely in a lead story about TIPS in a special section on investing.

I took a stab at explaining all the facets here: https://tipswatch.com/tips-in-depth/

Hi David,

I was wondering what’s the benefit of buying 5y TIPS in auction vs second market assuming that you are expecting %1.29 yield. In my vanguard account, I see these two :

– 04/15/2028 (3.625) 110.882 %1.362 (YTW)

– 07/15/2028 (0.750) 97.390 %1.266 (YTW)

Buying on the secondary market is fine if you find an attractive real yield. That 4/15/2028 TIPS has a massive inflation index of 1.855 and a price of about 110.75. So to buy $1,000 par of that TIPS you would have to pay about $2,054. (You’d be buying $1,000 par and total principal of $1,855). A lot of investors would shy away from that, and so it has a higher real yield.

The July 15 2028 TIPS has an inflation index of 1.195 and a price of about 97.25, so it isn’t as onerous and its real yield is pretty close to current market value. Still, if you buy $1,000 par you would be paying about $1,162 for about $1,195 of accrued value.

The advantage of buying on the secondary market is that you can see exactly what you will pay and what you will get. At auction, those results depend on how the auction goes. Could be sightly better than you expect, or slightly worse. But you always get the highest accepted yield, which is a benefit, even for a very small purchase.

Thank you, David. Appreciated your reply.

I know you already know this David, but others may not realized it is possible to lose a massive amount of principal on a TIPS like that if inflation became deflation.

If you buy it in a taxable account, the interest you collect is taxed each year (at your full tax bracket) but a loss on principal is a long term capital loss at maturity or early sale, only $3000 of which can be deducted from income each year.

A very unpleasant situation to find your self in, which as you suggest, is why many savvy investors might avoid issues like that.

I see many posts on this site concerning fears of deflation for the US dollar. Do that many people think that deflation, other than for brief monthly corrections, is more than a very remote possibility? Could you offer a scenario where deflation will become a reality?

I think we’re facing massive tax increases or an extended financial crisis because of:

1) funding for SS and Medicare

2) Debt service on the national debt

Debt service goes up almost $400 billion with every 1© increase in the average rate on the debt. This year, debt service will be almost $1 TRILLION, more than double last year

I have held TIPS in a taxable account for 20 years and this never happened, even during a decade of severely low inflation. Yes, it could happen, but let’s not overstate the risk. (All my new TIPS purchases are in a tax-deferred account.)

Median yield* on “Corporate B” bonds is 4.9%. The 5-year TIPS would break-even if inflation > 3.9%. My bond ladder is based on corporate paper with a minimum rating of BBB.

*Per Fidelity bond page

Corporate bonds are fine but you can’t compare that investment with a U.S. Treasury. There is some level of extra risk with corporate bonds.

I read that about 50% of all “investment grade” corporates are only one downgrade away from junk status

Hi David,

Dumb question of the week. I bought two original issue TIPS in 2021 where I paid a premium for each bond. Their current mark-to-market value in my brokerage account is below what I paid for them and what I thought was their face value.

When these two TIPS bonds mature, (here it comes) what will be their maturity date payout? Face value, face value plus inflation, my original purchase price, or something else?

Thank you, Mike

When a TIPS matures, there is no longer anything called “market value.” What you get at maturity is par value x inflation index + one last coupon payment. I personally track all my TIPS, even ones held at a brokerage, using par value x inflation index, to show the current accrued principal. Market value is irrelevant to me since I am holding to maturity.

Does buying TIPS at auction provide better protection against deflation than buying a similar duration TIPS on the secondary market?

Example: If you buy at auction this week, as mentioned above, you will get a par value of about 100.

On the secondary market, CUSIP 912810PV4, maturing in 4 years 9 months, would have a par of 145 (after multiplying by the inflation index).

With auction, your floor is what you buy at.

In the secondary market purchase, you’d have to lose value from 145 to 100 before your deflation protection sets in.

Is my reasoning correct or am I missing something?

I’d say buying at an originating auction — like the one this week — does provide additional protection against deflation, because you are buying at very close to par. Only par value is guaranteed to be returned at maturity even if severe deflation strikes. However … it is possible to find TIPS on the secondary market selling below par value if market real yields have risen well above the coupon rate.

Once you buy a TIPS and hold it awhile, it will have accrued inflation that is not guaranteed to be returned if deflation strikes. So really, TIPS are always going to have some deflation risk (and I think the “severe deflation risk at maturity” is extremely small).

Thanks David for all the information.

Agree that the risk is extremely small, but every once in a while, we get an unexpected risk that no one plans for. So I thought it wouldn’t hurt to minimize it if possible.

I was looking forward to David’s take on this, very helpful, thanks!!! I just checked Fidelity, Vanguard, and Schwab; their 5 year CDs with higher rates are either callable or around 4.4%. Within my wife & my roll over IRA accounts, I have been holding some cash, potentially targeted for TIPS, in money market funds with 4.68 to 4.83% nominal yields. I am ok with 1.29% or 1.25% fixed rate for the upcoming 5 year TIPS auction, however, as you all know, the real bet is on the inflation rate. After listening to the Wall Street, so called, experts, my narrative, tainted with, surely some, wishful thinking, I expect inflation to stay around 4% for a longer period than most expect. With 2024 elections not far, the independent Fed (:)) wants to avoid anything more than a mild recession. Last week’s bank earnings look encouraging; ok, enough of my wishful thinking…yes, will monitor the rates before Thursday and will place the trades/orders Wednesday night…BTW, I did buy, in my our Taxable brokerage account 2-year Schwab CDs at 4.95%…thanks to all!!!..best

If the 5 year TIPS has a real yield of 1.29% and an IBOND has a real yield of 0.4%, why would anyone buy IBONDS?

At current yields the TIPS is more attractive, but I Bonds have several important advantages: tax-deferred interest, much better deflation protection and a flexible maturity date. After five years they become an inflation-protected cash alternative, with zero chance of ever losing a penny of accumulated value.

I agree with the idea of a good mix. I ladder short term treasuries, have years of I Bonds, TIPS and 5-7 year MYGAs with rates at 5-5.5%. I purchased the 5 year TIPS at 1.72 and am hoping to add the upcoming 10 year TIPS.

Thanks to David and commenters for great information and ideas.

Interested in knowing more about MYGA, would you care to share which ones you have?

I thought about this auction but found MYGAs through Gainsbridge to be more attractive. Currently, their 3 – 10 year MYGAs are 5.25%. I speculated that inflation across these years will be below the likely break-even rate so I laddered some IRA money. You do have company risk, but the insurance company is A- rated and my amounts are below the state guarantee, so I am comfortable with going this route.

My most recent was with Americo, which is A rated. There are websites that let you sort by rating, rate and term.

Thanks, as always for your commentary. I’ve been eagerly awaiting your view on this offering but didn’t anticipate such a brain-teaser! Unfortunately, the highest 5-yr CDs that Fidelity (where I was planning to invest IRA money) offers are callable and don’t get call protection. until the not-very-appealing 4.40% level. And Vanguard offers nothing at all above 4.40%. Shorter terms are more appealing—higher rates and non-callable. I’ll probably go with the TIPS this week unless that rate plummets in the next few days.

Meanwhile, are you planning to do a post-mortem on the .625% yielding 5-yr TIPS that hit its maturity date yesterday (4/15)? From what I can see, it looks like that turned out to be a winner. Thanks again.

I have already posted the results on my TIPS vs Nominals page and will write something this week. (It was a winner.)

Thanks. I hadn’t noticed that TIPS vs Nominals page before. Good resource.

How about buy April with half money, then buy another half in June reopen? The thinking is that in June will know the coupon rate at least.

Thanks.

I will most likely be looking to buy at all the 5- and 10-year TIPS auctions this year, if yields hold up. Especially the 10 year. At an originating auction like this one in April, the coupon rate will always be 1/8th percentage point below the auctioned real yield. So the price should be close to par.

Pairing TIPS with nominal securities? This is what David Swensen, renowned manager of Yale’s endowment fund, has always advocated. I do likewise, but erring on the side of caution, not 50/50 as he suggests. About 70-80 % TIPS is my comfortable allocation.