The I Bond’s fixed rate could rise to 0.6% or higher on May 1. Should you wait? Or look at alternatives?

By David Enna, Tipswatch.com

Update, April 28, 2023: Treasury raises I Bond’s fixed rate to 0.9%; new composite rate is 4.30%

So here we are, in April’s magical two-week period where we can make a somewhat informed decision about buying U.S. Series I Savings Bonds in 2023.

We learned a key piece of information Wednesday with the release of the March inflation report, which set the I Bond’s new variable rate at 3.38%, down dramatically from the current 6.48%. But this drop in yield was expected. U.S. inflation has fallen from a high of 9.1% in June 2022 to the current rate of 5.0%, the lowest since May 2021.

A key thing to understand is that 5.0% is still unacceptably high inflation, reinforcing the importance of long-term inflation protection, which is exactly what the I Bond provides.

But the big difference today versus the last decade is that investors now have equally safe nominal investments with attractively high yields — insured bank CDs, online savings accounts, Treasury money market funds, along with U.S. Treasury bills, notes and bonds.

In addition, there is this obvious alternative: Treasury Inflation-Protected Securities, a more complicated investment that currently offers superior above-inflation returns.

One year ago, in April 2022, you could invest in an I Bond with a yield of 7.12% for six months, then 9.62% for six months. At that time, a 1-year Treasury bill was paying 1.84%. A 5-year TIPS had a real yield of -0.54%. I Bonds were a massively attractive investment in April 2022. Things aren’t so clear today.

So what is an investor to do? First, let’s look at some I Bond basics:

What is an I Bond?

An I Bond is a U.S. government security that earns interest based on combining a fixed rate and an inflation rate.

- The fixed rate will never change. Purchases through April 30, 2023, will have a fixed rate of 0.4%. That could change on May 1, when the Treasury resets the rate. It’s possible that rate could go higher, which would benefit people buying after May 1.

- The inflation-adjusted rate (often called the variable rate) changes each six months to reflect the running rate of inflation. That rate is currently set at 6.48% annualized. It will adjust on May 1 to 3.38% annualized, based on U.S. inflation from September 2022 to March 2023. The new variable rate will eventually roll out to all I Bonds, depending on the original month of purchase.

- The combination of these two creates the I Bond’s composite rate, which is currently 6.89%. The rate after May 1 will depend on how the Treasury sets the fixed rate. If it remains at 0.4%, then the new composite rate will be 3.79%. But remember it could be higher, but only for I Bonds purchased after May 1.

When you purchase an I Bond, you get the current composite/variable rate for a full six months, and then you transition to the next variable rate for a full six months.

Buying in April. April buyers know both the current composite rate (6.89%) and the next one (3.79%), locking in a compounded return of about 5.4% over the next year.

Buying in May. For a May purchase, investors only know the first six-month variable rate of 3.38%. The new fixed rate won’t be announced until May 1.

One key “negative” of I Bonds is that the Treasury limits purchases to $10,000 per person per calendar year. For this reason, I advise people interested in inflation protection to invest in I Bonds up to the limit each year, and continue holding until they really need the money.

Also, I Bonds cannot be redeemed until you own them 12 months. If you redeem them after 1 year but before 5 years, you will lose the last three months of interest. After five years, you can redeem any amount at any time with no penalty.

Is the fixed rate heading higher?

Back on March 9, I wrote an analysis suggesting that Treasury would be likely to raise the I Bond’s fixed rate to somewhere around 0.6% to 1.0% — leading to a guess of 0.8%. But on that very day, Silicon Valley Bank collapsed and we began weeks of financial turmoil, forcing real yields down dramatically. The equation of my highly-thought-out “guess” has changed.

The Treasury has no announced formula for setting the I Bond’s fixed rate, so that means anything I am saying is pure speculation. But my observations — and those of many savvy Bogleheads — indicate that the fixed rate tends to track higher when the real yield of a 10-year TIPS tracks higher. In other words, there is a correlation, but it is not a set formula. It appears to be a formula combined with the whim of the Treasury Department.

The fixed rate is extremely important for an I Bond investor, especially a long-term investor, because it stays with the I Bond for 30 years, or until the I Bond is redeemed. A higher fixed rate is very desirable.

In recent days, without giving this a lot of thought, I have been saying I think the May 1 reset of the fixed rate will fall into a range of 0.4% to 0.6%, but I’d lean more toward 0.6%. Here is an updated chart of the information I am using to make my “guess”:

Most recent real yield theory. On the right side is the equation I have used for years, comparing the potential fixed rate with the most recent real yield of a 10-year TIPS. This technique is hugely inconsistent, but it does a good job of predicting a rise or fall in the fixed rate.

In November 2022, the Treasury set the fixed rate at 0.4%, creating a spread of 118 basis points with the 10-year TIPS. The typical spread in recent years was around 50 basis points, so that 0.4% fixed rate was too low, in my opinion.

But note that since November 2022, the 10-year TIPS real yield has fallen from 1.58% to 1.14%. If you take 50 basis points from 1.14% you get 0.64%, so using this method I think we could see a new fixed rate of 0.6%.

Half-year average theory. On the left hand side of the chart is my newer theory, suggested by readers. To apply this theory, I determined the average 10-year real yield over the rate-setting periods — May to October and November to April for each period the fixed rate was set above 0.0%. Then I calculated the ratio of the new fixed rate to the six-month average.

In the most recent rate reset in November 2022, the fixed rate of 0.40% was 56% of the 0.72% six-month average for the 10-year real yield. If you applied that ratio to current 10-year real yield average of 1.37%, you get a fixed rate of 0.80%, rounded to the tenth decimal point. (Fixed rates are always set to the tenth decimal point, such as 0.40% currently.)

This method lessens the importance of the recent fall in 10-year real yields and points to a new fixed rate of 0.8%, which would be highly attractive.

Conclusion. I’m now guessing a fixed rate of 0.6% to 0.8%. But remember, this is a guess backed up by data, but still a guess.

Higher yield vs. higher fixed rate

Investors buying I Bonds in April get the advantage of locking in a 6.89% composite rate for six months and then 3.79% for six months. So even if the fixed rate rises, buyers in May will need several years to catch up. One of my readers, an Excel whiz who goes by “hoyawildcat,” came up with this explanation of the breakeven periods:

Here are the breakeven dates for I Bonds bought in May (at the new 3.38% variable rate and different fixed rates) vs. I Bonds bought this month (at the current 6.48% variable rate and 0.4% fixed rate).

0.4% — Breakeven: Never

0.5% — Breakeven: April 2040 (16 years 11 months)

0.6% — Breakeven: May 2032 (9 years)

0.7% — Breakeven: June 2029 (6 years 1 month)

0.8% — Breakeven: October 2027 (4 years 5 months)

0.9% — Breakeven: January 2027 (3 years 8 months)

1.0% — Breakeven: May 2026 (3 years)

I’ve seen similar breakeven numbers posted in the Boglehead forum, slightly different, but close enough to get an idea of the April vs. May purchase decision. Most of the Bogleheads seem to be opting for an April purchase.

Remember, you get a ‘mulligan’

While the Treasury limits I Bond purchases to $10,000 per person per year, savvy investors have uncovered a loophole that bypasses that limit: the gift box. This technique works best for spouses or family members, who can each purchase another $10,000 (or more) in I Bonds for each other, deposited in separate gift boxes.

I Bonds placed in the gift box begin earning interest immediately and capture the current fixed rate. When they are delivered in a future year, they apply to that year’s purchase cap for the recipient.

Harry Sit of the TheFinanceBuff.com was the first to write about this strategy on Dec. 27, 2021, in an article titled “Buy I Bonds as a Gift: What Works and What Doesn’t.” When people ask me about the gift box, I point them to this article, which was well researched and thorough. So, go read that article if you don’t know about the strategy.

Some basics of the gift box strategy:

- When you place an I Bond into the gift box, it begins earning interest in the month of purchase, just like any other I Bond, and continues earning interest just like any I Bond. However, this money is no longer yours. It belongs to the recipient of the gift.

- The purchase does not count against your purchase limit for that year. It will count against the purchase limit for the recipient, in the year it is granted.

- Gift purchases are limited to $10,000 for each gift, but you can make multiple gift purchases of $10,000 for the same person. But the recipient can only receive one $10,000 gift a year, and that gift counts against their purchase limit for that year.

- You must provide the recipient’s name and Social Security Number when you buy a gift. The recipient doesn’t need to have a TreasuryDirect account … yet. Only a personal account can buy or receive gifts. A trust or a business can’t buy a gift or receive a gift.

- “I Bonds stored in your gift box are in limbo,” Harry Sit notes in his article. “You can’t cash them out because they’re not yours. The recipient can’t cash them out either because the bonds aren’t in their account yet.”

- The recipient will need to open a TreasuryDirect account to receive the I Bond. Once it is delivered, the money is the recipient’s, who can then cash out or continue to hold the I Bond.

Investment alternatives

A lot of investors have flooded into I Bonds in the last two years, enticed by extremely attractive yields and near-total safety. Those investors were often looking for immediate, short-term returns at a time when savings accounts and money market funds were paying something like 0.05%.

But now, things are totally different. There are many attractive alternatives to I Bonds, such as:

- 1-year insured bank CD paying 5.1%.

- 13-week Treasury bill paying 5.02%.

- 1-year Treasury bill paying 4.64%.

- A 5-year TIPS with a real yield of 1.17%, well above the I Bond’s 0.4%.

- Online savings accounts paying about 4.1%.

- Money market accounts paying more than 4%.

Realistically, I Bonds purchased in April remain competitive, offering a nominal return of 5.4% over one year. But if that I Bond is redeemed in April 2024, the investor loses three months of interest, dropping the yield to about 4.4%. That’s still a good return, but not anything stellar.

I’ve heard from a lot of readers who are planning to bypass buying I Bonds this year and even beginning to redeem I Bonds in coming months as the lower variable rate kicks in. Can’t argue with that, if the investor’s goal is getting the highest near-term yield possible.

I Bonds remain attractive, however, for people seeking to push inflation-protected money into the future, with near-zero risk. I Bonds have better deflation protection than TIPS, have a flexible maturity date and are free of state income taxes. After five years, they become an easily accessible, inflation-protected savings account. You can never lose a penny of principal with an I Bond.

Final thoughts

A month ago, I thought the I Bond’s fixed rate would rise on May 1 to a range of 0.6% to 1.0%. Then came the banking fiasco, and my prediction fell to 0.4% to 0.6%. After writing this article and doing a better analysis, my prediction rises to 0.6% to 0.8%. As I have noted, this is a guess backed up by data.

I am opting to buy our full allocation of I Bonds in April and have set April 26 as the purchase date on TreasuryDirect. If the fixed rate rises dramatically on May 1, I will use the gift-box strategy to add to our holdings. In other words, I can’t lose.

In addition, I most likely will be investing in the new 5-year TIPS going up for auction on April 20. I’ll post a preview article on that April 16.

Later this year, as the lower variable rate kicks in, I may begin redeeming some 0.0% I Bonds that have hit the 5-year mark. Those will become retirement spending money, the reason I bought I Bonds in the first place.

Another viewpoint …

Jennifer Lammer, a YouTube content creator who closely follows I Bonds, just posted this video, reaching a similar conclusion: Buy I Bonds in April, but with a plan to buy more later in the year. There’s a lot of good information here.

What is your strategy? Post your ideas in the comment section below.

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

David – Just curious if you are you still buying your full allocation of I-bonds before May 1st?

Yes, I completed my purchase April 26.

.9 Fixed Rate – https://www.treasurydirect.gov/savings-bonds/i-bonds/

Regrets?

No regrets, because in my situation in a two-member household, I get the “mulligan” of 2 gift box purchases anytime through October. In early March I did think the fixed rate could rise by 0.8%, but then the banking fiasco sent real yields tumbling. I’m am happy with loading up on I Bonds with fixed rates above 0.0%.

I went to TreasuryDirect web site this afternoon in order to buy iBond, and multiple times the system said to try again later. I called TD, and got a message that they are too busy and not taking any more calls. I have two more days to try to purchase. Okay. Don’t wait for last minute. I’ve never had trouble with their web site and making purchases before.

Great information, thanks.

There is an IBond Rate FAQ that vaguely says how the fixed rate is determined.

https://www.treasurydirect.gov/help-center/savings-bond-faqs/#i-bond-rates

How is the fixed rate on an I bond determined?

The Secretary of the Treasury, or the Secretary’s designee, determines the fixed rate. The rate is based on market rates that have been adjusted to account for the value of components unique to savings bonds. These include the early redemption put option, tax deferral feature, deferred purchase feature, and Treasury’s administrative costs.

Nice find. I’ve never seen this before. Although vague, it does clearly state that the Treasury looks at “market rates” balanced off by the inherent advantages of low-risk I Bonds.

Familiar with: The Random Character Of Interest Rates, Applying Statistical Probability To The Bond Markets by Joseph R Murphy?

(I keep forgetting to mention it. One approach to the dilemma.)

If I bought I bonds sometime during the high rate period of May 2022 to October 2022 and wish to cash them in, it seems to me that the best time to do so would be in early July , August or September 2023 (at least one year after purchase). That way the 3 months interest forfeited would be at the lower 3.38% rate rather than the higher prior rates. Is that logic accurate? Thanks.

If I am going to buy in April and the funds I am using aren’t earning more that the current rate, is there any reason to wait until the 26th instead of just buying it today? I suspect not, but I’ve seen that date mentioned in a few places so I want to be sure I’m not missing something.

It’s not life changing, but if you are currently earning 4% on your money, you can hold it an extra week and collect that 4% interest. We’re talking about less than $10, but you do get to double-dip.

I got on the wagon in 2021 and 2022 with the full 10,000 purchase, but with the rate in May not great I backed off and only purchased 5,000 by 4/14/23. Then I sold $2,360 worth of I bonds greater than 5 years old with 0% fixed rate and purchased in May or Nov. Made 2,360 purchase of new bonds. The 2,360 of bonds will get 6.48% for 5 months, then 6.89% for 6 months. Will max out the 10,000 purchase, but only 5,000 new money. The rest swapping 0% bonds for new bonds with fixed rate.

Am I the only one who holds their I Bonds in a trust-registered account with TreasuryDirect (and thus ineligible to benefit from the gift box strategy)?

A lot of people use trusts to purchase I Bonds (I don’t), but wouldn’t you still be able to open a personal TreasuryDirect account and buy another allocation in any year?

Treasury Direct considers a “personal” account (registered in the name of a human being) and a trust account (one of several account types which Treasury Direct calls “entity” accounts) to be separate, even if for tax reporting purposes they are using the same Social Security number and even if the trustee of the trust is the same human being who already has a non-trust personal account. Someone who has an individual account and an individual trust account can therefore buy up to $10,000 a year of I Bonds in each, for a total of $20,000. If each member of a married couple has an individual account and an individual trust account, that would allow a total of $40,000 across the four accounts. If a married couple also has a JOINT trust account (i.e., it’s a trust but with a different registration and trust creation date from their respective individual trusts), that would allow still another $10,000 per year.

See, for example, this discussion by Harry Sit/The Finance Buff:

https://thefinancebuff.com/buy-more-i-bonds-treasury-direct-trust.html

I’ve purchased 10k i Bonds in each account I have set up

at TD. One in my trust, and one in my personal name.

Using full data from 2008, the two models predict a .3% fixed rate. Restricting the models to start in 2013, one model predicts a .3% fixed rate, the other .7%. This is all based on past data obviously. The guys at Treasury believe inflation will drop to more normal levels in the future, so we should consider that when guessing the next fixed rate. I am sticking with my gut, .4%, maybe even .3%. Remember, the fixed rate is for 30 years. If you are on the fence, you can always buy half your bonds in April, and half in May.

For short term investors, buy Treasuries. Six month T-bills are yielding around 5%.

What about those of us filing our tax return on April 18th and using the refund to buy paper Ibonds? Will I get the fixed rate based on the November 2022 rate or is there a chance the IRS will delay my purchase until after May 1st for the May 2023 fixed rate?

If you file on April 18th, I think it is highly probable you will get the new rate set on May 1, just considering processing time.

I filed on Feb 18th and my bonds were issued in March. I would count on a May issuance for April 18 filers.

I filed on April 12. Hoping my $1,000 I bond is issued in April, but realize it’s probably a coin flip at this point. Last year I filed on the 10th and my paper bonds arrived in the mail on the 22nd (which means this year it will probably take longer than usual).

My sense is that paper bonds are purchased from the Treasury as soon as the IRS approves a refund, even if the remaining direct deposit balance hasn’t been sent to your bank. But I could be wrong on this.

Very quick turnaround this year.

Federal return accepted March 15th

Excess federal refund direct deposit received March 20th

$5,000 paper I-Bond received today March 29th

Seems silly to some, I’m sure, but I am excited to finally receive the 5k denomination. I have been overpaying with extension 4868 since 2012 and always had received the 50, 200, 500, 1000 collection.

I think the Treasury stopped breaking up the denominations for the 2021 returns.

I much prefer getting just one envelope in the mail rather than several spread over several days. I miss seeing all the various portraits, but I guess I can look at prior years to see them.

I still received the assortment last tax year 2022 for my 2021 return but I filed early. I’m guessing last year had so much IBond interest the fed decided at some point to just start sending the 5k again but I was a bit early.

Like I said, I’ve been doing this for over 10 years and this is the first year I received the one 5K denomination. I much prefer it. Over the 10 years I’ve had 3 separate tax years missing a $50 bond. It’s a PITA filing the paperwork to retrieve it. Can’t really blame the USPS as their mailed in wafer thin envelopes. Probably got stuck in a mailing or magazine.

I was on the fence about I Bonds this time. I own some purchased in Dec 21 and more purchased in Jan 22. This time I took half my money and bought a 18 month CD paying 4.85 and with the the other half a 1 year T bill that will be 4.7-4.8 most likely when it closes Tuesday. I hope I won’t regret skipping the I Bonds but I just didn’t want to lock my money up for 15 months (to reduce the penalty) for a small boost in yield.

If your investment horizon is around 1 year, T-bills make more sense at the current yields, in my opinion.

I ran a couple of linear regressions using Mr. Enna’s data.

Model 1. Mr. Enna’s “Half-year average of 10-yr real yield”:

Fixed rate = f(Avg 10-year real yield). R-squared is .12. P-value on avg 10-year yield is not significant.

Model 2. Mr. Enna’s “Spread on latest 10-yr real yield”:

Fixed rate = f(10-year real yield). R-squared is .41. P-value on 10-year real yield is significant.

The higher the R-squared, the better the fit. Model 2 is the better model.

These are very simple models. When subjected to time series analysis, nothing is significant. Nonetheless, both models predict a new fixed rate of .3%. The 95% confidence interval using Model 2 goes from 0% to .7%. This means 19 out of 20 times the predicted fixed rate will fall between 0% and .7%, not exactly surprising. However, a rate of .8% would be an extraordinary outlier.

Model 2 accurately came up with .4% for the last six month’s fixed rate (Model 1 came up with a little under .3%).

Much can depend on the time frame used, as with all time series models.

So I will go with a new fixed rate of .3% as a best guess based on data shown by Mr. Enna, with a range of 0% to .7%. The range is large because the models are not particularly good. Before this analysis, my gut said .4%. It is not easy trying to guess what the guys in some back room at Treasury will come up with.

You can do the linear regression analysis with Excel, but I use a different program (GRETL) to more easily calculate P-values and confidence intervals.

This is fun. Try re-running it eliminating all the years before 2011, when the Fed started messing things up.

Mr. Enna suggested running the regressions restricting the data to 2013 to 2022 (there are no 2011 or 2012 data).

Model 1. Mr. Enna’s “Half-year average of 10-yr real yield”:

Fixed rate = f(Avg 10-year real yield). R-squared is .54. P-value on avg 10-year yield is significant.

Model 2. Mr. Enna’s “Spread on latest 10-yr real yield”:

Fixed rate = f(10-year real yield). R-squared is .38. P-value on 10-year real yield is significant.

The higher the R-squared, the better the fit.

Model 1 has a better fit this time. It forecasts a .7% fixed rate.

Model 2 forecasts .365%, a bit higher than last run.

As I said, much can depend on the time frame. A couple of crazy data points included or excluded from a short series can alter the results a lot.

I am still going with my gut which says .4%.

BTW, I notice all the 0% fixed rates appear to be missing in Mr. Enna’s table. My analyses might be more accurate if I could use all the rates, but then again, they might become completely useless. One should add this note to my analyses: “Note: These analyses only include data where fixed rates exceed zero.”

There is a lot to ponder with this thread. I was initially inclined to split my investment 50/50 with half before May 1 and half after, but now with the apparently valid Patrick model approach returning .3% as the most likely fixed rate for May there is cause to reconsider. With Mr. Enna’s .6 – .8% projection alone, I am more comfortable risking half of the investment for after April 30. I can live with the 9 year breakeven and even if the fixed rate was .5% a 17 year breakeven would not be that big a deal to me and in a sense still coming out ahead. But now with the possibility of a .3% fixed rate in the mix, it might make sense to take the sure thing and invest all in April. Except for the early years of the I Bond program, I have never considered the Treasury’s policy concerning the fixed rate to be one of generosity.

NOTHING is certain, but I think it would be a disgrace if the Treasury lowered the fixed rate below 0.4%. So that should be the floor, in my opinion. But … we don’t know.

David, thank you for that insight. I will take that into consideration.

I wanted to let you know that the IRS may have improved on the problems it had last year with processing paper returns. I filed a paper return for tax year 2022 and have received my paper I bond and refund. The bond was dated March 2023.

If the fixed rate remains at 0.4% then you will never breakeven if you buy in May. However, I like David’s suggestion of playing it safe and buying in April and if the fixed rate is > 0.4% in May then going the Gift Box route to purchase more I Bonds in May.

Patrick, the reason I only use fixed rates above zero is because the fixed rate can’t fall below zero, while real yields can go deeply negative. So those are crazy spreads. No fixed rate has ever been above zero when the 10-year real yield was less than zero.

Also, this second run could prove significant because it hints at the Treasury’s method for setting the fixed rate. If it ends up at 0.6% or above, that indicates the six-month average is more meaningful.

In the November 2022 rate increase, a lot of people speculated that demand for I Bonds, which was very high, would keep the rate at 0.0%. But the Treasury raised the rate to 0.4%, so that disproved the “demand” theory.

Thanks for the explanation. Yes, that zero minimum on the fixed rate can be a problem for analysis. As it is, the way we did it is probably the best we can do. Model 1 worked well 2013-2022. It predicts .7%, which seems intuitively high to me (I know you like .6%). This all makes the next fixed rate decision much more interesting to me. As you say, if it comes in at .6% or .7%, we might be onto something. It would be very useful to be able to predict with some confidence the composite rate a couple of weeks before it comes out. Treasury really should provide us with their method, oh well.

inflation will go through the roof again in second half of the year so I am buying more ibonds in May

That’s an argument for buying I Bonds, not for waiting until May. If you believe that inflation will go through the roof later in the year, why not buy an I Bond in April? That way you lock in the current 6.89% rate for the first 6 months, which is better than any 6 month rate anywhere, and you will eventually benefit from roof-busting inflation at some point later on.

I Bonds purchased in May will certainly miss out on the current 6.89% rate (6.48% variable plus 0.4% fixed). However, if the new fixed rate is 0.5% or more, then bonds purchased in May will eventually break even with bonds purchased in April, as David showed in the breakeven table in his original post. Obviously, the higher the May fixed rate the sooner the breakeven point will occur, so it essentially boils down to a question of how long one is willing to wait for the May bonds catch up with the April bonds — nearly 17 years if the fixed rate is 0.5% down to 4 years 5 months if the fixed rate is 0.8%.

Waiting 17 years for a possible 0.5% fixed rate to catch up with a definite 0.4% fixed rate is not a good investment strategy. That’s a difference of $10 per year on a $10,000 I Bond which is like watching paint dry.

It seems to me that a short-term investor should want to lock in the “better-than you-can-get-anywhere”and third highest ever 6.48% I Bond inflation rate for the next six months and a still “slightly better-than you-can-get-anywhere” 5.4% rate for the next 12 months and can see how it goes from there.

A long term investor who values the fixed rate should want to lock in the third highest I Bond fixed rate since 2008. To me, this decision is a no-brainer because the May fixed rate is like “vaporware” in the software industry. Until it’s released, it doesn’t exist.

It seems to me both roads lead back to buying an I Bond now before the May 1 rate change, especially when the gifting strategy enables you to hedge that decision if the best case scenario for the fixed rate occurs.

Pingback: re: I-Bonds – Musings of an Amused Writer

Is tax deferment and advantage of ibonds over tips?

Yes.

Appreciate your thoughts on this.

Excellent analysis as usual David. I tried to concoct a similar breakeven chart myself but didn’t have the math chops to pull it off. I’m still leaning towards waiting to purchase (perhaps to November) as the fixed rate seems more valuable to me than the variable. I’m wondering how that breakeven chart would look if we added a third comparable; those who wait to buy in November BUT keep their funds in T-bills earning 5% rather than buying the May 1st issue. I imagine the breakeven terms would shorten a bit… I still believe we’re in a hiking cycle that’s got longer to go than most people think and that rates all throughout the curve have yet to ‘accept reality’. I’m also surprised by the number of financial pundits who are predicting rate cuts (even this year). My greatest amazement lies in the fact that EVERYONE (even those who don’t see rate cuts this year) seems to accept as orthodoxy that the Fed will cut in the face of any economic hardship (be it a banking ‘crisis’ or a mild recession). I’m not so sure they will and even if they do, it may not be as quick or deep a cut as many expect. So, with higher fuel prices (that I’m already seeing here in NY) and a volatile global/political backdrop that I see as more inflationary than not, I think there’s a decent chance that the Nov 23 I bond will have a higher variable rate (3.38% plus) and at least a comparable (if not higher) fixed rate. Thoughts anyone?

There no benefit in waiting until November since you can buy the November issue from January – April of 2024 in addition to the April or May – October 2023 issue..With that in mind, the choice is between buying now or waiting until after May 1. And as David points out, you can do both with the gifting strategy. If you don’t or can’t use the gifting strategy, I would buy now (a bird in the hand is worth two in the bush) because of the certainty of what we know now, if you agree with David that the fixed rate I’ll increase, you can always split the difference and buy $5K now and $5K after May 1.

As for you other comments, we can’t predict the future of inflation or Fed action or gas prices, but the inflation trend has indeed been downward for upwards of 8-9 months, amd with higher numbers from a year ago coming off the books, the year over year rate is likely to continue its downward path, IMO.

Thanks Marc. My thinking is to identify the best time (for me) during 2023 to buy the Ibond. Every year, we have three choices: the first four months, the next six months and then the last two. If I were to buy the November issue I’d do so using my 2023 limits, and then buy again in Jan. ’24 for my ’24 allocation. My wife and I have gorged on IBonds since Nov.’21 and have built up a decent holding. All of the bonds we own have a 0% fixed rate. I realize I will want to ‘trade these in’ for higher fixed rate issues in the future, but I see no need to do so before the 5 year holding period. We’re in our mid-fifties and have a longer-term view. I want to avoid having a glut of low (or no) fixed rate bonds. So, I’m trying to maximize within my annual limits keeping the fixed rate as my priority to balance out my Ibond holdings.

It’s undeniable that the inflation trend has been downward recently, and will probably continue to decline for the next couple of months. But I disagree with your interpretation about the ‘higher numbers coming off the books’. Yes, they will come off the books but this will make for difficult year-over-year comps for CPI and Core in the second half of the year. Granted, this wouldn’t affect Ibond rates directly as they’re based on a six-month lookback, but it might create a very difficult environment for the Fed to pause (let alone cut) even without a rise in gas prices. I guess I’m just a bit more cautious about higher rates than consensus right now. I don’t pretend to predict rates or gas prices or anything else but the consensus view does and it seems to be overwhelming with one voice; we’ve hit peak rates.

Maybe; but I’m not so sure…

Good points made by all!

Don’t forget, too, that amongst those three choices (to either purchase in the first four months, or the next six months, or the last two), you can hedge your bets and do all three.

TreasuryDirect allows the purchase of electronic I bonds starting at a $25 minimum, and at any amount above that, to the penny. For example, you can buy an I bond for $36.73.

Therefore, you could buy $333 in April, $333 in the May-October timeframe, and $334 in November-December.

Glen,

This is a worthwhile discussion to have. Here’s my take, with the understanding that we are talking about your money which makes it your choice entirely.

If a fixed rate is your priority for buying I Bonds and holding them for the long haul, then I don’t see how you can possibly wait until November to buy your 2023 allocation. You would be “gambling” on a complete unknown and disregarding the very thing you covet which is guaranteed now. There is some indication (based on educated guesses) that there will be a fixed rate applied to the May 1 issue and it could be similar to, or slightly higher than today’s 0.4% fixed rate. David is making that guess. Maybe, possibly, hopefully…

But David is buying in April to lock in the fixed rate and high variable rate, as am I. He will use the gift box after May 1 if his guess turns out to be accurate, as will I. I guess what I’m saying is that at least there is some data upon which to base a possible May 1 buy, and a legitimate way to acquire it. There is no such data to base a guess on the November issue. If you wait until then and the fixed rate turns out to be 0%, you’re out of luck for the entire year. Gifting is a safety net for buying now, and so is the fact that the November issue can be purchased in 2024

“ I am opting to buy our full allocation of I Bonds in April and have set April 26 as the purchase date on TreasuryDirect. If the fixed rate rises dramatically on May 1, I will use the gift-box strategy to add to our holdings. In other words, I can’t lose.”

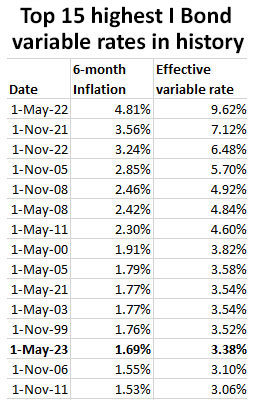

Me too! As I noted yesterday, this is a historically good I Bond offering that has been obscured by the recency bias of comparing it to the 9.62% high water mark.

– The current 6.48% annualized inflation rate is the third highest I Bond variable yield ever.

– The current 0.4% fixed rate is the third highest I Bond fixed rate since November 2008 (and the two higher ones were just 0.1% higher at 0.5%).

– Even the next 3.38% annualized inflation rate is the fifth highest I Bond variable yield since May 2011.

I know the focus of this article is the buying strategy, but the only thing I’d add is the I Bond selling strategy that I think should go along with it. Three months into the next 3.38% rate would be a possible time to take the penalty hit and sell 0% fixed rate I Bonds being held for less than five years, but with inflation trending downward, the next inflation rate could be even lower. That makes the October 12 CPI report when we’ll know the next I Bond inflation rate a key date to make this determination.

One thing I’m having trouble wrapping my head around is the issue of state taxes, in deciding to buy an I Bond in April vs a CD. I live in a very high tax state.

As a short term I bond investor, do I buy an I bond yielding 4.4% (factoring in the 3 month penalty) in which I don’t have to pay state taxes on the interest, or do I buy a 5% CD where I do have to pay taxes? Which would net me more $$ at the end of the day?

I’m not much of a mathematician, is why I ask…

The actual math is a little bit more complicated than this, but here is a simple, back of the envelope approach that will get you close to the right answer:

Calculate the post-state/local tax return on the CD as follows: CD Yield * (1 – state/local tax rate). For example, if your combined state/local tax rate is 10%, then the 5% CD would yield 5% * (1-0.1) = 4.5% post state/local taxes.

Now you can compare that number to the 4.4% early withdrawal I-Bond.

This approach ignores a few small factors like the additional federal taxes on the higher coupon of the CD and the ability to defer I-Bond taxes into a future year with a judicious choice of the redemption month, but it should be good enough for most purposes.

Another factor to consider is the timing of your deposits/withdraws. An ibond bought near the end of the month and sold near the beginning vs a CD bought at the same time would be close to 1 month up on the CD as far as interest goes.

IE buy on April 28th. May 1st your ibond has a full month’s worth of interest whereas the CD only has a couple of days. On June 1st, ibond has 2 months of interest while the CD has little over 1. etc. Which would effectively make the 3-month early withdraw penalty of the ibond equivalent to a 2-month one in comparison with the CD.

Have you consider US Treasury Bills? They are also exempt from local and states tax and comparable to Today CD rates (for short term)

3 months 4.99%

6 months 4.97%

12 months 4.75%

This is extremely helpful and well thought-out. Thank you for this analysis!

Excellent article, thanks for posting. I think I’m in the same boat as far as buying in April, and if the fixed rate jumps up, buying again as gifts. the only difference is I think I’ll have to redeem some 0% fixed bonds to do it, and pay the 3 month penalty to do so. Not the end of the world, and the fixed rate bump will overcome the 3 month penalty in under two years. I am using I bonds as our cash cushion for retirement in 5 – 10 years.

On thing to consider: If you buy after May, then you have all the way to October to make the purchase. So you can wait and let the I Bonds you are redeeming fall to the lower interest rate to lessen the penalty.

Yes, definitely! I also think I would redeem the newest I bonds that fit the schedule to minimize taxes.

Depends on one’s situation. For example if one happen to be in a low tax bracket this year (for example a retired worker who is not yet old enough for RMDs) and expect to be in a higher tax bracket when the older Ibonds expire (IE said retired worker has reached RMD age and expects significant sized RMDs), it could be better to take the tax hit on the older bonds now while taxes are lower leaving you with the longer deferral time of the newer bonds to give you more runway in choosing when to cash those in.

I surrendered years ago. I bonds 5000 in January, 5000 in May. TIPS purchases similarly spaced throughout the year. I think of this as my ” sampling technique” which, for me, has worked better than any predictive analysis I could concoct. Not to denigrate other’s attempts, but whose to follow?

A perfectly reasonable strategy.

Is there a downside to just dividing the $10k yearly amount by twelve? For example each month purchasing a smaller I-bond ($833.33) vs only buying twice a year ($5000).

I think that approach is fine.

Only downside I can think of is having a dozen ibonds each year vs 2 to keep track of.

I usually do just two $5k purchases and see no reason to go beyond 3 in a year (one in Jan-April, one in May-Oct, and one in Nov-Dec), not counting any gift box purchases.

The 10K purchase limit is, for most folks, not really much of a restriction. A couple planning for retirement at age 4o can buy 20K each year creating a pretty well funded bond ladder by retirement age.

I personally retired in late 1999 (at 48) and began to invest in I-Bonds. Having made significant bucks from the markets rise in the 90s, savings bonds seemed like a good way to go. Earn some interest and risk nothing.

I agree, even though many people point to the $10,000 as a huge downside for more wealthy investors. If a couple buys to the limit over several years, they can end up with a sizable allocation in I Bonds, creating a great cash-equivalent holding.

The gifting strategy mostly negates the $10,000 limit critique.

Really wish that it was made super clear both here and on Bogleheads that the gifting strategy only works if you are married. Singles will either have to make do with the $10k restriction or find a family member willing to go out on a $10k limb every year.

Agree. I know many people have used the gift box for children, but that probably won’t generally be a two-way transaction.

Well, technically, it doesn’t have to be a family member. A very close and trustworthy friend would do in a pinch (remember the two of you’ll need to share your SSNs with each other in order to gift, so only do so with someone you are certain you can trust with that information). But it’s a good point that outside of marriage, finding a gifting buddy isn’t easy.

Professor Zvi Bodie made a very good case for not holding equities in retirement.

Worry-Free Investing, 2003

I generally agree. Foreseeable retirement expenses should be covered by guaranteed savings/incomes. (see myblog on Retirement Planning). If you have “excess” and want to play the market – go for it. Remember though that as you age your cognitive abilities will fade and elderly are very popular marks for grifters.

I am a big fan of Professor Bodie, “the father of I Bonds.” But I disagree with him on this point. I am comfortable with a 35% allocation in low-cost stock index funds.

I started with 40% in the market but when the market changes, the ratio changes and I did not do anything. Mine was up to 60% before Covid and such but back down to 40% now. Guess the thing to do is rebalance to your decided ratio? Course with cash starting to yield something the swings should not be so dramatic. Its hard to sell winners. I do not worry about cost, the least one will every lose is a management fee!

I think there’s a good chance we’re looking at at least a decade of dead money in the stock market

We’ve had well above trend gains in equities for a long time, when in fact GDP growth is well below what used to be trend (US is a far more mature economy than it used to be)

Accounting games have devalued historical P/E comparisons, and the cost of increased debt service is a staggering drag on the economy going forward (even if we ignore the inevitable tax increases to address Medicare and SS deficits)

Rip Van Winkle approach.

Imagine I had $$$$$ in the Vanguard 500 or total market index January 2000. Using the handy inflation calculator at the BLS website when would my $$$$$ again be worth what they were in 2000? Early 2014.

( This ignores rebalancing effects or dollar cost averaging in more funds.)

Risk Less And Prosper by Zvi Bodie charts this through 2011.

Donald, I look at our asset allocation every quarter, but we don’t make changes unless things move more than 2% out of line. In December, after both stocks and bonds fell, we were still in line. But in April, stocks had gotten too high. So time to re-balance.