Composite rate will fall from 6.89% to 4.30%, but the fixed rate of 0.9% is highly attractive for long-term holders.

By David Enna, Tipswatch.com

Surprise! I Bonds purchased from May to October 2023 will get a fixed rate of 0.9% and a composite rate of 4.3%, TreasuryDirect announced this morning, jumping the gun on its expected May 1 press release. It’s all right there on its homepage:

At first, I thought this was posted by mistake, jumping ahead of Monday’s announcement. In the 12 years I have been writing about I Bonds, the new rates have never been announced early.

A few minutes later, the TreasuryDirect site went down, possibly because of the “what the hell?” factor driving traffic. But I was able to return to the site a bit later and it loaded, with the same information.

I had been speculating that the I Bond’s new fixed rate would be about 0.6%, so 0.9% is great news. It is the highest fixed rate since the reset in November 2007. The fixed rate tells you how much the I Bond will earn above official U.S. inflation. It is equivalent to the “real yield to maturity” of a Treasury Inflation-Protected Security.

The site has the full information on the new rate and how it was determined, combining the new inflation-adjusted variable rate of 3.38% with the new fixed rate of 0.9%.

| Fixed rate | 0.90% |

|---|---|

| Semiannual (1/2 year) inflation rate | 1.69% |

| Composite rate formula: [Fixed rate + (2 x semiannual inflation rate) + (fixed rate x semiannual inflation rate)] | [0.0090 + (2 x 0.0169) + (0.0090 x 0.0169)] |

| Gives a composite rate of | [0.0090 + 0.0338 + 0.0001521] |

| Adding the parts gives | 0.0429521 |

| Rounding gives | 0.043 |

| Turning the decimal number to a percentage gives a composite rate of | 4.30% |

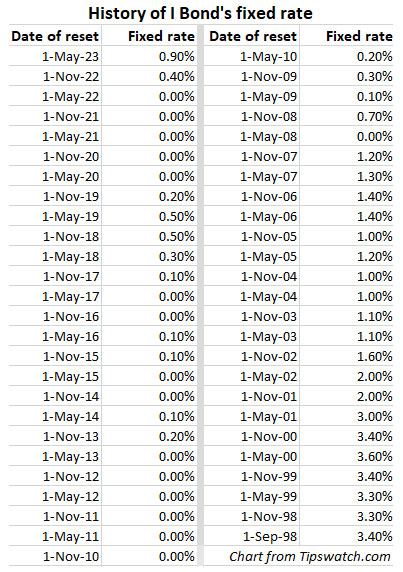

TreasuryDirect’s page listing the history of fixed rates now includes the 0.9% rate, more than doubling the 0.4% fixed rate in effect for purchases through April 30.

The current composite rate for I Bonds purchased through April 30 is 6.89% and that will fall to 4.3% for purchases from May to October 2023. But the fixed rate of 0.9% makes the May-to-October purchases very attractive.

Just as an aside, the new composite rate for I Bonds purchased from November 2022 to April 2023 will be 3.79%, which reflects the fixed rate of 0.4% and inflation-adjusted rate of 3.38%.

TreasuryDirect said this week that the last day to place orders for the 6.89% rate was yesterday, April 27. (I placed my order on April 26.) So I am assuming that any I Bond purchased today will get the new May 1 rate. And that could be why the Treasury decided to post the new rate information, since we can assume it will take effect for purchases today.

EE Bonds

The Treasury also announced that the new fixed rate for EE Bonds will be 2.5% for savings bonds issued from May 1 to Oct. 31, 2023. This is up from the current fixed rate of 2.1%. The Treasury is retaining the policy that EE Bonds are guaranteed to double in value if held for 20 years, creating an effective interest rate of 3.53%.

Gift box strategy?

The Treasury limits purchases of I Bonds to $10,000 per person per year, so investors need to think through a strategy for the best time to invest. If you were planning on holding the I Bonds for less than 2 years, the smart move was to buy in April, locking in an annual return of about 5.4%. For long-term holders, buying in May is preferable, locking in the 0.9% fixed rate for the full 30-year term of the I Bond.

Earnings from the new 0.9% fixed rate create a breakeven period of about 3 years, 8 months. If you plan to hold less than 3 years, 8 months, buying in April works out better. Anything longer will make the May rate more attractive.

The dilemma: Now the fixed rate rises to 0.9%, but you already bought your full allocation this year. (True for me.) What do you do?

If you bought in April, like I did, you can still use the gift box strategy if you have a spouse or a trusted friend or family member with a separate TreasuryDirect account. Using this strategy, anytime before the end of October you can place $10,000 into the TreasuryDirect gift box, assigned to your partner, and your partner would do the same for you.

Some basics of the gift box strategy:

- When you place an I Bond into the gift box, it begins earning interest in the month of purchase, just like any other I Bond, and continues earning interest just like any I Bond. However, this money is no longer yours. It belongs to the recipient of the gift.

- The purchase does not count against your purchase limit for that year. It will count against the purchase limit for the recipient, in the year it is granted.

- Gift purchases are limited to $10,000 for each gift, but you can make multiple gift purchases of $10,000 for the same person. But the recipient can only receive one $10,000 gift a year, and that gift counts against their purchase limit for that year.

- You must provide the recipient’s name and Social Security Number when you buy a gift. The recipient doesn’t need to have a TreasuryDirect account … yet. Only a personal account can buy or receive gifts. A trust or a business can’t buy a gift or receive a gift.

- “I Bonds stored in your gift box are in limbo,” Harry Sit notes in his article. “You can’t cash them out because they’re not yours. The recipient can’t cash them out either because the bonds aren’t in their account yet.”

- The recipient will need to open a TreasuryDirect account to receive the I Bond. Once it is delivered, the money is the recipient’s, who can then cash out or continue to hold the I Bond.

Rolling over 0.0% fixed rates?

If you are holding I Bonds with 0.0% fixed rate — especially those held for five years or more — you can consider redeeming those older I Bonds for new ones with the 0.9% fixed rate. When you redeem, you will owe federal taxes on the interest earned.

I think this is a sound strategy, especially if you don’t want to raise another $20,000 to buy I Bonds this year in two separate accounts.

One key thing to consider is to wait until the current variable rate of 6.48% has completed and the new rate of 3.38% has begun. You have until October to make a purchase of I Bonds with the 0.9% fixed rate. No rush.

If you have held the I Bond less than five years, consider waiting an extra three months to have the three-month interest penalty apply to the lower composite rate.

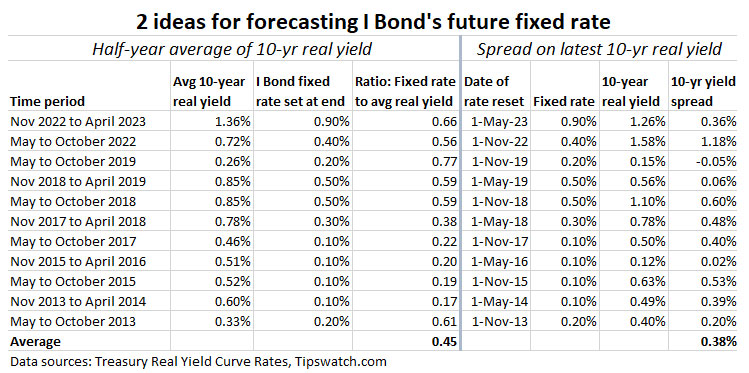

Projecting the fixed rate

We still don’t know how the Treasury decides on setting the fixed rate of the I Bond, but it’s becoming clear that the rate tracks higher and lower with real yields of Treasury Inflation-Protected Securities. We just don’t know how much. TreasuryDirect recently added this “less vague” statement to its FAQ page on I Bonds, clearly indicating that market real yields are a factor in setting the fixed rate:

The Secretary of the Treasury, or the Secretary’s designee, determines the fixed rate. The rate is based on market rates that have been adjusted to account for the value of components unique to savings bonds. These include the early redemption put option, tax deferral feature, deferred purchase feature, and Treasury’s administrative costs.

Here is the final version of my two prediction models for the I Bond’s fixed rate. The columns on the left show how the fixed rate compares with the average of the 10-year real yield over the last six-month rate-setting period. The columns on the right show how the fixed rate compares with the latest real yield of the 10-year TIPS.

I have limited these numbers to the times when the Treasury raised the fixed rate above 0.0% going back to November 2013, solidly in the era of Federal Reserve intervention in the U.S. bond market.

If you look at the calculation on the right, the average yield spread between the latest 10-year TIPS and the I Bond fixed rate is 38 basis points. The new fixed rate of 0.9% is 36 basis points below the current 10-year real yield of 1.26%. So that looks good as a predictor, but this calculation isn’t very reliable except to predict if the fixed rate is likely to rise or fall.

The half-year average calculation is more reliable, I think, and in more recent rate changes the ratio has been in the range of 0.59 to 0.77. Today’s fixed rate announcement of 0.9% puts the ratio at 0.66, right in the middle. I think this half-year-average formula is more reliable, but still nowhere near perfect.

To close, here is the history of all fixed rates for I Bonds back to their inception in September 1998:

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

The 0.9% fixed rate is obviously interesting but the variable rate is low and likely to go lower still in 6 months. Which is an interesting conundrum.

Can I check the wisdom of the crowd here?

I have 3 i-bonds (only one US citizen in the family so $10k/year limit), bought in Nov18 (0.5% fixed rate), Apr19 (0.5% fixed) and Apr22 (0% fixed).

The last purchase wouldn’t have happened if it weren’t for the variable rate being so high, and given the zero fixed rate I feel that long term it makes sense to replace it with a new one with 0.9% fixed rate, even after the short term tax and interest penalty hit. But given that the composite rate is lower than alternatives (savings, t-bills), there’s no rush to do this until late October.

So I’m thinking: in end of October I buy $10k of new ibonds, then sell the Apr22 ones either early November or 3 months later, depending on the new variable rate and savings rates at that time. Am I missing something?

In my opinion inflation will get stuck at about four percent and will prove stubborn so I’m not convinced the variable rate will continue down in the near term. It does make sense to swap out the Apr 2022 bond for one with the higher fixed rate. I would sell the Apr 2022 in January of 2024 so you are giving up three months of the lower rate. Buy the new bond before the 0.9% fixed rate expires but wait to sell the one with a zero percent fixed rate.

I’ve been retired since 1999 (I was young). Got out of the market after the meteoric rise on the 90s. I have been adding to I-bonds since then and this past year I purchased TIPS for the first time.

I-bonds may not (probably are not) the best investment but… They are simple and safe. TIPS are just as safe but not as simple. The market may be better but it is neither safe nor simple. Given that I made what I needed in the 90s I figured why risk it. And I haven’t

This fall I will probably use the gift box to purchase my last I-bond. Between SS ,an annuity, and my complete 30 year bond ladder I hope to be set until after 100.

Financial incompetence gets many of us as we age. I-bonds help to prepare for that as does SS and annuity income.

To cynicalanddisgusted,

Your username could change to cynicalanddisgustedandsmart.

Thank you for sharing these words of wisdom. I also took stock market money out early in 1999. Then, watched stocks increase 25% into early 2000. Cannot remember what i did last week, but can still recall that unpleasant experience.

Very wise of you to not have risked permanent impairment of capital when it was not necessary to do so.

If we consider an average inflation of 4% (worst case scenario) and an effective tax rate (what you actually pay/what you actually make) of 20% or less (which would apply to most in states with no state tax and only federal tax), the after tax real return on this bond would be close to 0 (if we consider compounding the interest), meaning it is a very good option if you want to mantain the purchasing power of your money with close to 0 risk and total liquidity (after two years).

Here my calculations: (4%/(1-20%))-4%=1% which is more or less the 0.9% fixed rate (plus the variable rate) compounded through the years.

If you wanna put it in another way, if you were to go in a space ship and return in 30 years with no communications with planet Earth, no doubt this I bonds would be the safest option (in case there are no tax increases and your effective rate remains the same or lower).

If I was the Treasury this would have been my calculations in case I wanted to sell more I bonds, which might be the case if they consider they might soon be defaulting.

How much worth of ibonds can be bought if I were to open a brand new LLC in NJ ? Also, can I open a LLC incorporated in DE even if I an resident of NJ and use it to buy ibonds ?

An LLC has the same limit as an individual, $10,000 each but you can have as many LLCs as you want. The states I looked at require a physical address in the state but I am not familiar with NJ or DE.

I like Don’s LLC trick. You have to pay fees to register an LLC, as I recall, and get an EIN. I don’t know how much the fees are. My I-bonds are registered as a living trust, but since it has my social security number, I am still limited to the $10,000 annual maximum.

The Savings Bond Calculator has still not updated. Maybe TD spent all their energy cosmetically modifying their web-site.

No EIN required.

So how does the IRS and TD keep track of your LLC registered bonds? Is there some other number that they use?

An LLC is a separate legal entity from its owner even when it uses your SS#. Mine all use my number.

“Single-member LLCs (or sole proprietorships) may not need an EIN. If you are the owner, manager, and director of your home-based business, you do not need an EIN. Instead, you can use your social security number (SSN). However, once you decide to hire employees, you must have an EIN.”

– Upcounsel

Sounds like you need either a social security number (SSN) or an EIN for an LLC. If you use your SSN, I would think you would be subject to the $10,000 annual max per SSN. Note that a single member LLC can apply for an EIN. Maybe Treasury does not care about the $10,000 max per SSN if you are an LLC.

I have not had any issue with many LLCs using the same social. The Treasury Department reached out to me once I passed 100 accounts to ask what I was doing. They looked at my documentation and said everything was fine. I have kept building my portfolio from there with no problems. It’s been over a year now. No EINs all on my social and tied to one bank account.

Seems strange, but I am glad it works. Thanks for telling us.

“Kentucky is the cheapest state to form an LLC, with a filing fee of $40. Whereas, Massachusetts is the most expensive state to form an LLC with a filing fee of $500. In some states, it is also required to publish notice of the formation of the LLC in a local newspaper (Arizona, Nebraska, and New York).” California has a $70 filing fee, but a $300 renewal fee.

Do you have to maintain your LLC status for the entire time you own your bond?

While there is no automated check to see if the LLC is still active it seems like a good practice. Mine are all active and documented. In Michigan, after the initial set up you are asked to renew and pay a lesser fee each year. However, if you fail to renew for two years from your renewal the LLC is no longer considered to be in good standing. So my initial fee covers me for three years and longer if I am willing to be lacking in good standing. When the Treasury Department contacted me they wanted proof that the LLCs existed and that I was authorized to transact on their behalf. Each article of incorporation lists my son as the agent as he lives in Michigan and me as the organizer. I showed them three sets of articles and they said that everything was in order.

If I wanted to I could cut the number of LLCs in half this year by doubling up on the first half and then closing out the second half of my LLCs. The same thing could be done in subsequent years so over time you would end up with many fewer LLCs than you started with.

You need a physical address in the state. A post office bix will not work.

Here is a link with LLC initial filing fee and subsequent annual fees by state. Missouri looks like the best overall deal with $50 initial, no subsequent annual filing fees or other hassles. But as Don says, you have to have a physical address in the state you are filing in OR a registered agent in the state. The site has a lot of info.

https://www.llcuniversity.com/llc-filing-fees-by-state/

Wow Don! I understand that each state is going to be different, but is this the basic model (?) :

1– setup 100 LLCs in year-1 at some “TBD” state for $40/yr each = annual, recurring out of pocket cost = $4000

2– buy $10,000 IBonds for each LLC = $1,000,000 worth of IBonds in year-1

3– I can afford 5 years of $10,000 IBonds per each LLC

4– so I buy another $10,000 IBonds for each LLC in year-2, year-3, year-4 and year-5

5– assume 4.5% interest on IBonds = $45,000 interest per year on each $1,000,000 IBond purchase

6– at the end of 5 years:

6a– (5 x $4000) = $20,000 out of pocket costs of maintaining the 100 LLCs for the 5 years

6b– my gross return on $5,000,000 worth of IBonds across 5 years is = ($45,000 x 5) + ($45,000 x 4) + ($45,000 x 3) + ($45,000 x 2) + ($45,000 x 1) = $675,000

7– my net return after year-5 is $675,000 – $20,000 (the LLC maintenance cost) = $655,000

And at year-5, I start withdrawing from the $655,000 and never touch the $5,000,000 worth of IBonds … forever.

Do I have that right Don? Is that the model?

Well at the time that I started this it was known that 7.2% was going to 9.6%. From there I assumed it would be lower but still attractive. It turned out to be 6.5%. The fifty-dollar LLC fee nets to $38 after tax and covers me for at least three years and longer if I am willing to hold LLCs in an LLC that exists but is not in good standing, but three years was fine for my purposes.

So, each $10,000 earned $360 then $497 then $353 so a total of $1,210 less the $38 fee so a net of $1,172. The bonds are held for twenty-one months. If I want to continue adding in year two, you do not need another LLC. Just add a second bond to the existing LLC without additional fee.

Do you plan to pass through your income to Schedule B or file Schedule C on your I Bond interest, given that you seem to be in the business of buying I Bonds (and paying self employment tax in addition to regular income tax)?

Single member LLCs are disregarded entities for the IRS. The interest will flow right to my personal return.

Brilliant Don. Thanks for this line in your reply: “The bonds are held for twenty-one months. If I want to continue adding in year two, you do not need another LLC. Just add a second bond to the existing LLC without additional fee.” Really ties the strategy together for me. You’re doing real active-management on this asset category.

Here are detailed instructions from Harry Sit’s site: https://thefinancebuff.com/buy-i-bonds-business-sole-proprietor-llc.html

Make sure you set up and renew directly through your state to avoid or minimize fees. My state has no fees but I get solicited to use a middle man, which is not needed.

Would appreciate your opinion on my situation, which I’m sure also applies to other readers: in my mid-50’s, buying I-bonds for longterm/retirement, purchased the maximum already on April 26, no spouse or kids to use the gift box strategy. Is it worth it to form an LLC to buy more in 2023 (no prior experience with LLC’s)?! I’m in NY, an expensive state for fees.. Thanks in advance for any comments!

I’ve never done it. Possibly others who have can give an opinion.

The process to set up an LLC is easy. It takes me about eight minutes to set up an LLC and a TD account and find it. You don’t need an EIN or separate bank account. New York is expensive at $200. I live in Oklahoma where the fed is $109 but I have a son that lives in Michigan where the fee is $50. The fee is deductible and good for three years. Do you have a friend or relative in a less expensive state?

Thanks for the reply! Unfortunately no, I don’t have a contact in a less expensive state, although I have a relative in a less expensive county of NY, which I think would significantly reduce the ridiculously expensive cost of the newspaper publishing requirement ($1500 in NYC?!) I think the total would be around $500 give or take if I use the upstate mailing address? Maybe one of you math whizzes can tell me at what breakeven point it would be worth it? 🙂

I wouldn’t do it for $500. Probably renewal annually. Michigan is $50 and works for three years. All deductible.

In Florida $125 to set it up and $138 every consecuent year.

What about a revocable living trust?

https://thefinancebuff.com/simple-living-trust-software-i-bonds.html

I looked at that. You need a lawyer and a bank to set them up. The LLCs were cheaper and easier.

I’ve done a more accurate analysis and selling the Nov-21 bonds in October and using the proceeds to buy new bonds at the current variable and fixed rates will produce $180 more by October 2028 and $672 more by October 2033. I will break even in March 2026 (4 years 3 months).

FYI, here is the Treasury’s official release on the new rates: https://www.treasurydirect.gov/news/2023/release-05-01-rates/

My wife and I are doing tons of homes improvements this year so I’ll be cash-poor through the end of the year and therefore can’t afford to buy any more I Bonds without raising some cash elsewhere. However, I definitely want to take advantage of the new 0.9% fixed rate, so this is what I came up with.

In October, I’m going to sell the $10K in I Bonds that I purchased in Nov-21, which are currently yielding 3.38% With the three-month interest penalty I should receive $11,272 from TD. I’ll then buy $10K at the new variable and fixed rates. This will give me an additional $1,272 in cash for our home improvements but will cost me an additional $273 in 2023 income taxes. I figure that by October 2028 the new bonds will have produced at least $300 more in interest than the Nov-21 bonds and $800 more by October 2033.

Hi. I purchased ibonds for the first time in April 2022 and have been advised that I may want to redeem them in January 2024, so that I lose 3 months of a lower interest rate. In the last few days I’ve been thinking I would redeem in January and purchase the current ibond with the .9% fixed rate. But might that .9% fixed rate change in November 2023, along with the variable rate? Would it be better to buy more ibonds in October 2023, and just redeem my initial ibonds in January 2024 as originally planned? I’d be interested in any advice about best moves.

Does the .9% fixed rate mean you’re guaranteed to earn that much above inflation for as long as you hold the ibond? But why is the new annualized composite rate ‘only’ 4.3%, including that .9% fixed rate, if inflation is around 5%?

Thanks.

That looks correct on the timing, which I discussed in this article: https://tipswatch.com/2023/03/29/want-to-exit-your-i-bond-investment-youd-better-have-a-plan/ … The fixed rate is permanent and lasts for the 30-year potential life of the I Bond. The composite rate is determined by combining the fixed rate (0.9%) and the six-month variable rate (3.38%) to give you 4.3%. The variable rate tracks the last 6 months of inflation, which was 1.69%, or 3.38% annualized.

A couple things to consider: If you bought $10,000 in April 2022, by redeeming in January 2024 you will be giving up about $84 of interest and you would owe federal taxes on the $1,208 interest you will have earned through the end of September 2023.

Isn’t the interest give up much less than that? The fixed rate on those is zero. The variable rate you will be conceding is 3.38%. Three months of that is about $84.

Thanks. I’m thinking I should buy more in Oct 2023 and sell my initial ibonds in Jan 2024? If I wait until Jan to swap out my current ibonds, the .9% fixed rate might no longer be available?

That is true. The 0.9% fixed rate is good for purchases through October. There is no guarantee that the fixed rate next year will be the same. I use LLCs to buy my I bonds, literally hundreds of them all tied to my SS# and one bank account. The cost is minimal and deductible. The Treasury Department looked at what I was doing and blessed it last year. That would allow you to buy this year to take advantage of the fixed rate and cash out next year.

Don, you now get a seat at the “I-Bond Obsessed” table. If you have plenty of assets — which obviously you do — this strategy is clever and exciting. I personally buy $20,000 a year for us as a couple, but this year it will be $40,000 using the gift box.

The 7.2, 9,6, 6.5 was just too good to pass up in a market where stocks and bonds both got trashed. Now I will roll them out after three months of 3.4 and move my fixed income portfolio over to TIPS, Bank CDs, and Treasuries depending on the rates (and maybe some I bonds as well). The I bond strategy carried me to a point where I can now lock in some more attractive rates long term. My fixed income portfolio had been earning 1% before the I Bond party rolled into town.

Last year I spoke with a company that was looking at borrowing $100 million from a bank and using an automated system to screen scrape the system to open 10,000 LLCs and TD accounts to acquire I Bonds. I’m not sure if they ever did it or not but they had a thorough plan. They planned on creating about $4 million out of thin air with the arbitrage.

It’s a small point, but didn’t you mean to say the 3 months of interest given up for January 2024 redemption would be $95 due to compounding?

I bought $65K of April issue and already calculated the interest through April 1, 2024. $11,208 x 3.38% = $378.83/4 = $94.71 forfeited for January 2, 2024, redemption.

That seems right. I didn’t calculate compounding.

Don, you are right and I edited my comment to fix my mistake.

At that rate the payback for swapping out for the 0.9% fixed rate is less than a year. Swapping out the Aprils after a great eighteen months makes sense.

Nancy, I should have noticed your January purchase date. It’s true that the 0.9% fixed rate will end for purchases after October. Of course, it could go higher in November. Or it could go lower. So wait until mid-October to make a decision. You could redeem/buy then and face a higher interest penalty, or wait until January and hope for a higher fixed rate.

What happens to bonds in the gift box when a person dies? At some point, they need to be delivered to the recipient. If they are delivered all when the giver dies, couldn’t that cause problems for the recipient under the 10k/yr/person purchase limit?

Example: my husband and I have 10k of bonds gifted to each other in the gift box. This year we have maxed out our 10k allotment in non-gifted bond. One of us dies this year. If the bonds are gifted immediately upon death then doesn’t giving spouse have a problem of going over the 10k/year limit?

I can see this getting compounded if spouses keep adding gifts to each other (or others) each year.

Harry Sit of the TheFinanceBuff.com has answered this question: https://thefinancebuff.com/buy-i-bonds-as-gift.html#htoc-unexpected-death

His advice is to name a second owner or a beneficiary for the I Bond in the gift box.

Thank you for the link to Harry’s site.

Harry says . . . The principal amount of delivered gifts counts toward the $10,000 annual purchase limit of the recipient in the year of delivery.

I am still puzzled by this scenario . . . Let’s say the giver has (over a period of years) maxed out the 10k gift to their spouse. The giver dies. How can the recipient/surviving spouse receive these multiple gifts if they can only get 10k/year of savings bonds in their name?

I believe inherited I Bonds do not count toward your yearly $10,000 limit. (I tried to find a link on Treasury Direct stating this but couldn’t find it.) And it makes sense because when you inherit, you’re not buying any I Bonds; rather, the ownership of an already purchased I bond is being bequeathed to you.

Fiscal Service Form 4000 must be filed along with death certificate of decedent to change the savings bonds ownership. The deceased registrant is removed and bonds reissued to surviving registrant(s).

I had asked my brothers, the ungrateful and underserving beneficiaries in my gift box, to research/get the facts and neither one of them did anything.

So, the above are my notes when I looked into it. And, there is no need to be puzzled. The gift box of decedent is not subject to any limit or restriction as no longer considered a gift. Just do not die – that is the most important part.

Thanks Alan. I called Treasury Direct (1.5 hour hold time, but better than the 2.5 hours with my utility company!) to confirm. You are correct, the gift recipient just inherits the funds without any issues.

So, from what I can tell, my spouse and I are free to gift each other 10k/year (while also doing 10k/yr outside of the gift box) and accumulate the bonds in the gift box. The second allowable name on them are POD to our two children (5k each/year). So, when the first of us dies, the bonds go to the surviving spouse with our kids being the next in-line beneficiary when spouse #2 dies. HOWEVER, the surviving spouse’s gift box bonds to the spouse that just died, are now part of the deceased spouse’s estate and would then go to our 2 children. Thus, the surviving spouse would NOT get those gifted bonds back to them. This is not a problem for us, as we will not live to see them mature, we won’t need the funds and the kids will get them sooner.

After spouse #1 dies, spouse #2 is the owner in your case and nothing “goes” to any children just yet.

The bonds of deceased spouse #1 now belong to spouse #2 and nobody else. Surviving Spouse #2 files Form 4000 requesting change of bond ownership.

Once the inherited bonds are registered in the name of Spouse #2 Beneficiary Account that is when the two children, subject to good behavior, can again be registered as beneficiaries.

You followed the solid advice of Doctor Enna in naming two beneficiaries. Best to check in with him before making major moves, which is what i will be doing when he comes back from chasing boobies. For example, why exactly did you use the gift box for spouse when not required to do so?

Sorry a fixed rate of .9% just does not excite me.

That’s fine. I Bonds aren’t for everyone.

For inflation protection, I invest in both TIPS and I Bonds. To me, the 0.90% fixed rate is very exciting, looking through the lens of comparing this new Series I bond’s 0.90% fixed rate to the 30 year TIPS real yield of 1.51% (as of April 28, 2023). For those people who intend to hold this I bond for less than 10 years, a comparison to the 5 year TIPS (1.31%) or 10 year TIPS (1.26%) makes this I bond look even more attractive.

Given many of the advantages of the I Bond (such as ability to redeem before 30 years without the usual interest rate risk, deferral of taxes until redemption, deflation protection, flexibility of a 6 month window to make a purchase decision, etc), I will happily accept the 0.90% fixed rate.

In my situation, just the tax deferral benefit alone makes this I bond worthwhile.

I don’t think anyone’s crystal ball is going to work six months for now, but it would really be nice if this fixed rate persisted for the November-April period so I could take advantage in 2024. As it stands I just made my 2023 purchase on my sole proprietor account yesterday. I have another $5,000 coming when I decide to finish my taxes, and as the variable rate rolls over for my different bonds, I will be cashing out all the ones which are over five years old and paying 0% fixed rates, and strongly considering cashing out the ones paying 0.1% and 0.2% as well. I don’t need that much in dry powder now.

I agree, it is a bit painful to see the fixed rate rise in the May to October period, since that won’t carry over to 2024. With the rate volatility we have seen, and economic crisis always around the corner, it’s impossible to predict where the fixed rate will be in 2024.

My wife and I have treasury accounts and we both purchased the $10,000 maximum in January 2023, can we still each gift one another $10,000 more in 2023?

Yes, you can place the investments in the gift box (each of you in your separate accounts) but you can’t deliver those until at least 2024, since you are both at the limit for 2023.

Why should I buy this I-Bond? It matures in 30 years when I’ll be 100, when I almost certainly won’t need the cash and most likely won’t need the cash before then; and given its high fixed rate it will certainly be the last I-Bond I cash out.

Sorry, just pondering Ben Franklin — “a penny saved is a penny earned” vs. “nothing is certain except death and taxes.”

Hoya! You know better. An I Bond has a flexible maturity date. You can redeem after 1 year with a 3 month interest penalty, or after 5 years with zero penalty. Your investment and all the interest it earns can never go down in value. After 5 years, you have a cash-equivalent investment paying 0.9% above inflation, for as long as you want to hold it.

However, if you feel you will never need cash in the next 30 years, you should be a happy person and enjoy life on your private island?

I am a bit confused and worried about my decision. I bought some bonds in May 2022 for me and my babies. I wanted to let the babies grow for the 30 years and mine to grow past the 5 year mark for as long as possible (even 30 years.) But now that I know about the 0.9%. I feel like my bonds won’t make its full growth potential. What should I do? (In simple terms.)

My usual advice is to hold all I Bonds, no matter the fixed rate, until you need the money, especially after holding them 5 years. They grow with inflation and taxes are deferred. But we haven’t seen a 0.9% fixed rate in 15 years, so that is attractive. You have until October to decide if you want to redeem the 0.0% I Bonds to buy new 0.9% I Bonds, or just buy the new ones at 0.9% since it sounds like you haven’t bought yet in 2023. If you bought in May 2022, you got 9.62% for six months and then 6.48% for six months. That’s a great start.

I wouldn’t even consider redeeming it or any I Bond before five years, and I’ve got plenty of older 0% fixed rate bonds that I’d redeem first, which I probably won’t need to do. Plus, I’ve got TIPS, thanks to yours… 😉

To reinforce one of your observations about the gift box purchases being in limbo — especially for those with a dual-spouse strategy (A buys gifts for B and B buys gifts for A) . Rather than maxing out purchases for yourself, get those 0% rates bonds delivered and then backfill them with another gift. In fact I would do this every year (deliver over purchase) but it’s clearly disadvantageous to hold the 0% bonds in the gift box. It’s the complement to the redemption strategy of continuing to hold the better fixed rate bonds (all else being equal).

And maybe that’s intuitive — but I thought I’d say it anyway.

This is the reason I never made a gift box purchase in the mania days of a 9.62% variable rate with a 0.0% fixed rate. It’s not worth locking in a 0.0% fixed rate for years to come. But a 0.9% fixed rate, the highest in 15 years, is worth locking up.

Dave, so I was one of those who bought into the 9.62% iBonds mania by buying $30K for me and the Mrs. as gifts to each other in 2022. We delivered the first $10K to each other this past January 2023 so we have 2 more years of $10K 0% fixed iBonds to gift to each other which takes us to 2025.

As such, we have accumulated a fair stache of 0% fixed iBonds for inflation protection and wealth preservation over 8 or so of the past 12 years (in addition to TIPS thanks to you). So in not wanting to miss out on the fixed iBonds we also just bought $5K each of the .4% fixed for each other yesterday.

Now in light of the .9% fixed I plan to buy $15K more each as gifts for each other before November 2023 which will take us to 2027.

Since we acquired iBonds as inflation insurance I’m thinking it just may make sense to let them all continue to run rather than cashing in any of the 0% fixed. Thoughts on approach?

deeMatrix

Holding I Bonds is never a bad decision. So you are on the right track, until you need the money.

Wow. The fixed rate hasn’t been that high since 2008. I wonder if the early announcement has anything to do with the website changes. They have been updating pieces of it here and there, and this morning there was a notice that the virtual keyboard was going away.

It might not be the site changes, but TreasuryDirect’s decision to be more up-front about what you were purchasing. If you bought today, you might have thought you were getting the 6.89% rate. Instead, you are getting 4.3% for six months … but with a nice bonus of a 0.9% fixed rate. This is good work by TreasuryDirect, even though it super-complicated my day.

Yes, that makes more sense. Whatever the reason, I’m glad to have the early announcement. It looks like they haven’t updated the rates for the pre-2005 EE Bonds. It’s still showing 2.99 for those. I suppose those will be up on Monday.

It appears that the Treasury has deliberately given no guidelines for the fixed portion of the i bond rate to allow it the flexibility of manipulating the fixed rate as a plug to make the composite rate competitive with other inflation indexed products such as TIPS. The 5-year tips closed @ 1.32% real rate so there is a delta of 0.42% but one should not forget that unlike tips, I bonds offer protection against deflation (which is very likely in the coming months) and a federal tax deferral to boot. Makes it quite attractive to rollover the ones with 0% fixed rate. This will also keep $ with Treasury which it sorely needs because of the impending debt limit and it will keep these $ from circulating back in the economy thereby somewhat helping the Treasury in combating inflation.

I definitely agree that the I Bond’s fixed rate tracks along with the real yield of TIPS, but we just don’t know the exact formula or even if there is an “exact” formula. The 0.9% fixed rate is perfectly placed below the real yield of 5- to 10-year TIPS, in my opinion.

I’m not sure if this is new info in the Treasury Direct FAQ. Seems a just a bit more information than they’ve provided previously (but still no exact formula).

“How is the fixed rate on an I bond determined?

The Secretary of the Treasury, or the Secretary’s designee, determines the fixed rate. The rate is based on market rates that have been adjusted to account for the value of components unique to savings bonds. These include the early redemption put option, tax deferral feature, deferred purchase feature, and Treasury’s administrative costs.”

Steve, another reader pointed out that paragraph to me a week ago. I had never seen it before. It seems to be a clear statement that the Treasury looks at market real yields and adjusts downward for the I Bond to reflect its advantages as an investment.

Are some saying you can “rollover” or swap older bonds into new fixed 0.9% bonds by selling the old ones even if you already maxed out 2023 purchases? Or are you just saying that is a strategy for those who haven’t made their 2023 purchase yet and don’t want to increase overall ibond holdings?

No, if you bought the maximum in 2023 you can’t buy more in your own account. I’m suggesting that you could use the gift box strategy, which involves buying another $10,000 for someone else, and having them do the same for you. The gift box does not trigger the purchase cap until the I Bond is actually delivered.

Thanks, after thinking through what I wrote, I realized it couldn’t be the case. Would be nice though…

It’s incredible that we get to earn 5% nominal interest while waiting until the latter part of October to make the ibond purchase decision. Depending on what the TIPs real yield moves – it might be a big gift box opportunity in October.

Reviewing the fixed rate predictor model and the new .9% fixed rate. This is the best model of the ones I have looked at.

I posted this a couple of weeks ago.

Mr. Enna’s “Half-year average of 10-yr real yield” from Oct 2013 to Oct 2022:

Sample size is 10.

Fixed rate = f(Avg 10-year real yield). R-squared is .54. P-value on avg 10-year yield is significant.

This equation forecasted a Mar 2023 fixed rate to be .708%. Not bad, considering the actual rate turned out to be .9%. It is above my gut feeling forecast of .4% and Mr. Enna’s range of .4% to .6% (but I think Mr. Enna said it could go higher).

This is the same model, but I include the Mar 2023 new fixed rate of .9%.

Mr. Enna’s “Half-year average of 10-yr real yield” from Oct 2013 to Mar 2023:

Sample size is 11.

Fixed rate = f(Avg 10-year real yield). R-squared jumps to .80. P-value on avg 10-year yield is significant.

This equation estimates the Mar 2023 fixed rate to be .828%, fairly close to the actual rate of .9%.

As with all time series models with short series, much can depend on the time frame. I would say this model, which starts in Oct 2013, is a good predictor of the fixed rate.

Patrick, I have updated the article to include the two models with updated information through April 27, the date the Treasury made the decision for the May 1 fixed rate.

What I have shown today is just one model, as in it uses the same Y variable and the same X variable, just different dates. The first regression uses data Oct 2013 to Oct 2022 and was used to predict today’s fixed rate. It predicted .7% This you have seen before. The second regression simply adds today’s .9% datapoint to the sample . It can be used to predict the next fixed rate in October 2023. The extra datapoint improves the fit significantly, R-squared going from .54 to .80. I figure you know this, but I want to be clear.

Patrick, I know this? Oh hell no. I will need your help in October. Please stand by on permanent retainer.

Okay, I can email you the Excel file with data, graphs, and equations if you send me an email address. It can all be done easily in Excel, except for the P-values, but I know using another program that they are significant.

A nice surprise! I already maxed out in April, but will use the gift box method to buy more for later delivery. My hubby has no interest in these so I can gift him the max for this year and next. At some point I’m planning to unload my few 0 fixed rate holdings.

Great news for long-term I-bond buyers.

So if we maxed out already, will the bonds we purchased prior to May 1st earn 4.30% for the 6 months from May 1-October 31 or will they earn just 3.40%?

If you bought from November 2022 to April 2023, your new composite rate will be 3.79% for six months. The start date will depend on the month you originally bought the I Bond.

Please excuse my ignorance, but how did you arrive at 3.79%. Also, what do you mean by “before April”?

I meant for a purchase from November 2022 to April 2023, and I fixed my comment to be more clear. The 3.79% comes from the Treasury’s composite rate formula: 0.004+(2*0.0169)+(0.004*0.0169) with 0.004 being the fixed rate and 0.0169 being the inflation rate.

Ah, I understand now. We won’t get any of the new 0.9% fixed rate. Thanks.

Maybe the fixed rate does not follow a formula, but the composite rate. In this way the fixed rate is determined so that the composite reflects the current (insert your yield) when the most recent 6 month CPI-U was (whatever it was).

I don’t think so. It’s definitely based on current real yields, minus some spread.

Well, the model predicting .7 percent looks like the right one, if this release is real. This early release seems VERY strange.

I wonder if the Treasury decided since purchases of the April I Bond ended on April 27, it should post the new composite rate for purchases on April 28 or later. That’s a good thing to do, but it never did it before.

I would argue we should legally be allowed to get the “old” rate up to 11:59 pm EST on April 30. We cannot help it if Treasury is slow to process new orders, nor can I understand why it is so slow. It is all done by computers nowadays. Couple this with today’s early release of the fixed rate, I begin to have a lot less confidence in the people who are supposed to be running Treasury Direct.

Of course with the new fixed rate, people should wait until May 1 to buy I-bonds if they want to buy them.

I believe when you buy an I-Bond, no matter when – 1st day or last day – it tells you it will be schedule for the next business day (at the earlies). Since the next business day on 4/28 is 5/1 (and therefore after the rate reset), the TD announcement that 4/27 was the last day to buy an I-bond with the then current rates was consistent with its operations.

My question would be: since once can schedule a purchase in advance — what happened if someone scheduled a purchase to happen on 4/28 — my guess is they got the Nov-April rate. I scheduled my purchase for 4/27 a while ago just to be sure I received the Nov-April rate

If the purchase was made April 28, I think the buyer gets the May rate.

You probably follow this more closely and certainly have more experience.

But I interpreted the TD announcement as 4/27 being the last day to buy the April rates as an announcement for the masses : “Don’t log in on 4/28 and expect to buy and get the April rate — the last day to do that is 4/27” And as I think about it more — if anyone logged in on 4/27 to buy, their purchase happened today (whether they knew it or not)– and they got the April rate. It’s kind of like a a T+1 settlement for ad-hoc purchasers, but a same day settlement for scheduled purchasers.

I think the Treasury is consistent and was responding to Patrick’s comment about legally being allowed to buy “up to 11:59 pm EST on April 30”. I believe that happened. Purchases happen on business days; Purchases never happen the day entered. So in order to buy at the last possible moment and get the April rate (the intent of Patrick’s statement), one had to place/schedule their order no later than 4/27.

But I could be wrong for sure.

If Treasury is going to play the T+1 settlement game, then they should put it in writing as their policy. I have not seen it, but maybe it exists somewhere buried in all their bureaucratic verbiage.

I am also uneasy about the early release of the new rate. I tried today to use the Savings Bond Calculator, but it did not work past May 2023, even though the data are now available to get interest monthly to Nov 2023. In the old days, the Savings Bond Calculator worked on the day of the update.

People who have no spouse or children are at a disadvantage with others having the gift box option. Treasury needs to up the annual maximum, bring back the $30,000 limit and increase it each year by the CPI. They also need to jack up the fixed rate to two or three percent like in the early days (but that would certainly mess up my model).

Enough complaining. The I-bond program is interesting, but its implementation still needs a lot of work. Most important, Treasury needs to tell us how they calculate the fixed rate, if it is a calculation, and not just some guys in some back room coming up with a number.

I will give TreasuryDirect credit for being upfront on this settlement issue, which is obviously “allow one business day for your purchase to clear.” TD had a large announcement on its homepage stating that the last day to purchase the April I Bonds was April 27. And that was widely reported. After the 2022 fiasco, I Bond investors should have gotten the word that waiting until the very last day to purchase could be a disaster. But then again, there was a lot of media coverage that said “buy in April!” which I thought was iffy advice, even though I personally bought in April. So there could have been last-minute buyers, who were lucky enough to get a 0.9% fixed rate.

Maybe they decided that they should release it now rather than risk a leak over the weekend? I know the fixed rate, after the fact, of the I Bond is pretty low on the hierarchy of sensitive information, but still.

Thank you Mr. Enna. Your boots were on the ground for us. It does look like good work/better communication by Treasury Direct.

I am surprised by the 90 basis point fixed rate – was expecting only 60 so that the composite rate would start with the number 4 (vs the number 3) on the “May 1” announcement.

And, in the 20+ years of buying I and EE , cannot remember any early announcement like this one that you have brought to our attention.

If you think about a five year horizon I am seeing TIPS with a 3.5% real yield. That would seem to more than be worth it even with the tax implications and the lack of deflation protection.

A 5-year TIPS currently has a real yield of about 1.31%, so it does have a 41-basis-point advantage over an I Bond. This is fairly typical.

Thanks. I misread the search results or more likely forgot to check the show-only inflation-protected securities box on Schwab.

If true, definitely swapping out some 0% for these new ones. we’ll see what Monday brings, but to me it looks like they just went ahead and posted it early.

Wow, that’s a shocker, in two ways:

Early Announcement; I’m guessing it wasn’t a mistake and they posted it because they know anyone buying today would get the new rate anyway, so it’s not really early in the sense of undermining current purchases. I’m effect, it makes no difference announcing it today vs. Monday.

Fixed Rate Amount: A raise of the fixed rate during a period of still rising interest rates isn’t that surprising, but the delta more than doubling that component from 6 months ago is higher than anyone anticipated. Is it possible the lingering debt ceiling crisis played a role as a way to increase short-term revenue to the Treasury while people are still paying attention to I Bonds?

It’s probably right. They posted it after the opportunity to buy in April was closed. The next purchase opportunity is Monday, May 1st.

Wow. That would be very appealing. In fact swapping out bonds bought last year for new ones would have a payback of less than a year. It is still up.

Wow, higher that your post SVB implosion prediction range of 0.4 – 0.6%.