By David Enna, Tipswatch.com

Here’s an update on my last article, “Looming debt crisis is already roiling Treasury bill market,” which discussed the disruptions rippling through the bond market as the U.S. nears a debt-limit crisis.

Moody’s Analytics, a market research firm that is a subsidiary of Moody’s Corp., just issued an April 2023 analysis with new information about the debt crisis and the approaching X-date, when the Treasury will run out of cash needed to pay the government’s bills on time.

A key point in the analysis is that the date appears to be coming earlier than researchers originally thought:

The Treasury debt limit—the maximum amount of debt that the Treasury can issue to the public or to other federal agencies—was hit on January 19, and since then the Treasury has been using “extraordinary measures” to come up with the additional cash needed to pay the government’s bills.

Nailing down precisely when these extraordinary measures will be exhausted … — the so-called X-date — is difficult. It depends on the timing of highly uncertain tax receipts and government expenditures.

Since Moody’s Analytics began estimating the X-date early this year, we have thought it to be in mid-August. But April tax receipts are running 35% below last year’s pace, which is meaningfully weaker than anticipated. And despite weaker tax refunds than anticipated, it appears that the X-date may come as soon as early June. If not, and Treasury is able to squeak by with enough cash, then the X-date looks more likely to be in late July.

The Moody’s report reinforces my argument that the debt crisis is beginning to be seen in clear disruptions in the bond market. It says:

Time is running out for lawmakers to act and increase or suspend the debt limit, and global investors are suddenly focusing on the risks posed if they do not act in time.

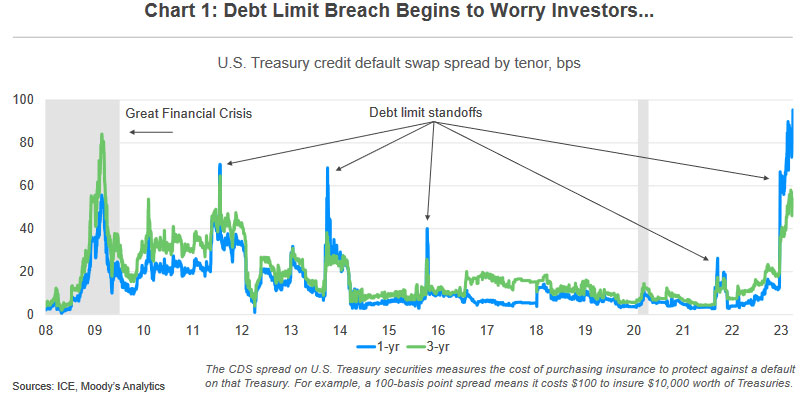

The analysis points out that credit default swaps on U.S. Treasurys — the cost of buying insurance in case the Treasury fails to pay its debt on time — have jumped in recent weeks, to levels even higher than past debt-ceiling disruptions.

At close to 100 basis points, CDS spreads on six-month and one-year Treasury securities are already substantially more than in 2011 when that debt limit drama was so unnerving it caused rating agency Standard & Poor’s to strip the U.S. of its AAA rating.

The analysis also notes the recent sharp decline in the yield of the 4-week Treasury bill, which was the major point of my article earlier this week:

As it has become clear in recent days that April tax receipts were coming in weak and the X-date may be just a few weeks away, investors have piled into the safety of one-month Treasury securities. Yields have plummeted, from 4.75% at the start of April to less than 3.4% currently. At the same time, yields on three-month Treasury bills have continued to rise. The difference between one- and three-month Treasury bill yields has never been as wide. Global investors thus appear to be attaching non-zero odds that the debt limit drama will end with a default sometime in June or July.

The GOP spending proposal

The analysis goes on to examine the ramifications of the House Speaker Kevin McCarthy’s proposal to roll back discretionary U.S. spending in 2024 to 2022 levels — in exchange for a one-year increase in the debt limit. It’s an interesting analysis, and I’ll let you read it and reach your own conclusions. It seems highly unlikely that McCarthy’s proposal will end up being the final settlement of this issue.

At any rate, the White House issued a statement Tuesday declaring that if McCarthy’s bill reached President Biden’s desk, “He would veto it.”

What’s next

Moody’s Analytics notes that the Treasury debt limit drama is heating up and is likely to get much hotter in coming weeks. It notes:

If the X-date is as soon as early June, it seems a stretch for lawmakers to come to terms fast enough, and they instead will likely decide to pass legislation suspending the limit long enough to line the X-date up with the end of fiscal 2023 at the end of September. This will buy some time …

Getting legislation that funds the government in fiscal 2024 and increases the debt limit across the finish line into law will surely be messy and painful to watch, generating significant volatility in financial markets. Indeed, a stock market selloff, much wider credit spreads in the corporate bond market, and a falling value of the U.S. dollar may be what is required to generate the political will necessary for lawmakers to avoid a government shutdown and breach of the debt limit.

My thinking has been that Congress will eventually have to kick the debt-limit issue down the road to avoid severe disruptions to the bond and stock markets. Moody’s suggests the extension could be to September, when we could relive this crisis again.

But the political divide — and the resulting game of chicken — seem a lot more severe this year, with just a few GOP House members potentially able to block any compromise. In a hopeful note, Moody’s concludes:

But when all is said and done, the legislation that lawmakers ultimately pass will likely be anticlimactic, allowing both House republicans and president Biden to declare political victory.

What should we do?

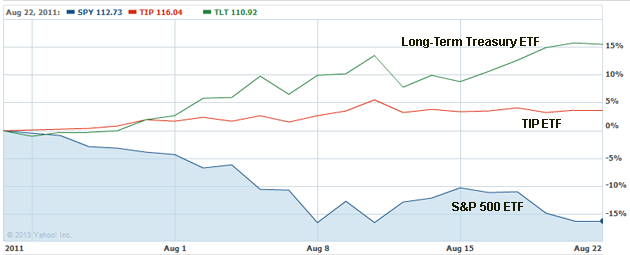

In a worst-case scenario we could see a repeat of August 2011, a very bad month for the stock market, but quite nice for bonds:

But I suspect that history won’t repeat itself in this way. Bonds benefited in 2011 from increased liquidity supplied by the Federal Reserve, but that might be out of the question in 2023 as the Fed battles inflation. The stock market in recent years has been through the wringer, over and over, and bounced back. But this time, it may not have the Fed as its savior.

I am not a financial adviser and I’ll admit that I am not doing much differently in the lead up to this crisis. For example, some possibilities:

Sell all your stocks and move to cash? One of the big differences between 2011 and today is that cash is much more attractive, with yields above 5% for many short-term Treasurys. In August 2011, the 6-month Treasury bill was paying 0.16%. Today, cash is an appealing alternative. The only problem: How safe are Treasurys in a worst-case scenario? (The answer, in my opinion: still very safe.)

No, I personally won’t be selling out of the stock market. But I could see raising some cash because of the chance to …

Snap up attractive yields when you see them. This week I bolstered my bond ladder by buying a two-year, brokered, non-callable Morgan Stanley CD paying 4.7%. The 2-year Treasury note auctioned Tuesday at 3.97%, so the CD is a better deal. (This is in a tax-deferred account, so the state income tax issue doesn’t apply.)

Watch for market chaos. There could be a buying opportunity, and it could be as short as a few hours of a single day. I’d expect yields on some short-term Treasurys to begin rising higher in coming weeks, as the fear factor sets in. Then … a compromise is announced and everything moves back to what we now call “normal.”

Do nothing. Not a bad option. In the long term, the market will adjust. In 2011, after a miserable August, the S&P 500 ended the year with a total return of 2.1%, followed by 16.0% in 2012 and 32.4% in 2014.

What do you think? Tell us your strategy in the comments section below.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

None

Hi David — Thanks for another great piece. Regarding your comment – “Snap up attractive yields when you see them, ” a question: What would the 2-5 sites you look at daily to check rates & dates on CDs, T-Bills, etc.? Not deep-dives or big articles, just quick at-a-glance looks so one can go to their brokerage site, bank site, TreasuryDirect site, etc. and to do a deeper review before buying / selling. Thanks.

Because I am shopping in a tax-deferred account, I just look at the offerings I can see on Vanguard and Fidelity for brokered CDs and secondary market Treasurys. For new Treasurys, check the Treasury’s Yields Curve site: https://home.treasury.gov/policy-issues/financing-the-government/interest-rate-statistics

Thanks…I’m using the Vanguard site advance search inputs for CDs & that T-Bill Rate page on Treasury.gov was great. Just what I needed.

What is the likelihood of getting paid after the maturity date assuming they ‘work things out’? I know that during one shut-down federal employees didn’t get paid until later, but they got paid everything. My concern is that even if a late payout scenario became policy the treasury’s IT systems would not be able to handle it since it’s never happened before and hasn’t been planned for. Considering the buggy role-out of healthcare dot gov you have to wonder how soon they could accomplish a late pay even if they wanted to.

Thank you for sharing your two-year CD purchase and the reminder about buying in a tax-deferred account so the state income tax issue doesn’t apply.

Schwab Fixed Income team recommending to extend duration to intermediate maturity via Treasury securities/CDs/Investment grade bonds given their view of declining interest rates.

Started buying the Schwab SCHI ETF in tax-deferred account. The current investment grade rated debt of companies like T-Mobile and Anheuser Busch. SCHI net expense ratio three basis points/maturity ~seven years/interest-rate sensitivity ~six years/~5% current SEC yield.

I am not much worried about the government not paying on its Treasuries. If it defaults, those are the first to be paid. The government has enough money for that. A “default” will of course make some Treasury investors nervous. If these nervous nellies stop buying Treasuries, rates will go up, which is fine with me. I am laddered so that just about every month a chunk of T-bills mature, and the money becomes available to purchase more, usually at higher rates (so far).

A prolonged default will impact other programs (social security, medicare, welfare, etc.). The stock market will take a hit.

Remember, countries do not go bankrupt. They just print more money, which leads to greater inflation, which leads to higher rates.

First Republic Bank problems and the likelihood of more bank failures are more of an issue. As I mentioned before, this may be the source of the strange 4-week T-bill behavior this month, although many attribute it to the default possibility.

I don’t know why people use TD for purchasing of Treasuries. I know Schwab and Vanguard have no commissions on buying or selling Treasuries, and you can buy and sell them at any time. I buy at auction.

Speaking of timing, I just had a 4 month T-bill mature last Thursday. I bought a 6-month T-bill on the Monday at auction before that Thursday. The 6-month T-bill settled on the same Thursday. So the day the 4 month T-bill matured, that money was used to pay for the 6-month T-bill. I made a few extra bucks for a few days while I owned both the 4-month and 6-month T-bills.

I read there is no guarantee that Teasuries would be paid first. “While the motivation to pay principal and interest on time to avoid a default on Treasury securities is clear, lawsuits would probably argue that Treasury has no authority to unilaterally decide which obligations put in place by Congress to honor.” I believe it would ultimately be up to Congress, the President, and the courts to decide who gets paid first and how much.

I’d agree there probably isn’t an absolute rock-solid guarantee. But in 2011, the government created a contingency plan that said there would be no default on Treasurys and interest would continue to be paid. I think Treasurys would be at the top of the priority list if we headed into a true default scenario.

Things are a lot more polarized now. I’m not an expert, but I think Yellen said she didn’t have the authority to decide who would be paid first. I took that to mean there is currently no law that clearly says treasuries should be paid first, regardless of whose priority that is. In that case, if Biden and McCarthy can’t reach an agreement and pass legislation that clearly states what the priorities are, lawsuits would probably be filed and the courts would decide – just like in any bankruptcy. Depending on whom the public blames, there is an absurd incentive for one side or the other to make things as painful as possible in order to pressure the other side to capitulate.

If there is a default, there is still enough money to pay off Treasury debt from tax receipts alone. Lawsuits about who gets paid first would likely be resolved according to corporate/business law, where bondholders always get paid first in the case of bankruptcy. However, well before lawsuits are filed, the debt ceiling will be raised.

Note that almost all the people in Congress are well off. You don’t really think they would jeopardize their and their families’ wealth by voting to destroy it. If there is a default, it will be of short duration. On the plus side, it might be a buying opportunity.

I like your thinking….. will look for buying opportunity

Yes, I think some people would jeopardize their wealth in order to win a partisan advantage or increase their chances of re-election. Throughout history, people have sacrificed a lot more than their wealth to fight a real or perceived enemy. During a game of chicken, people often miscalculate. People often make decisions based on emotions like fear, greed, anger, or pride rather than on facts and reason. People used to fight duels and sacrifice their lives over a perceived insult. People still risk fines, their freedom, and their lives to do some pretty crazy things. Giuliani had his law license suspended and others went to jail to push a claim of election fraud that was supported by little to no evidence. Yes, I think it is very unlikely that the US will default on its treasury obligations, but plenty of things have happened over the past 8 years that I never thought would happen. I take a lot less for granted than I used to.

In a corporate bankrupty, bond holders are not paid first, secured creditors are. If the government went bankrupt, things would be a lot more complicated. I imagine funding for the military, law enforcement, and other services that are essential to protect the health and safety of the citizens would take priority over bond holders. And it is hard for me to imagine that food and health care for poor children would be eliminated or that millions of seniors would loose all or part of their income or health care while bond holders, including hostile foreign governments, received every penny they were owed. In any case, I think things would be a lot more complicated and uncertain than you seem to suggest

Holders of Treasuries are not secured creditors. Treasuries are backed by the “full faith and credit of the United States”. As Mr. Enna says, their is a plan devised in 2011 to cover a situation when the debt ceiling is not raised.

Brookings says “Under the 2011 plan, there would be no default on Treasury securities. Treasury would continue to pay interest on those Treasury securities as it comes due. And, as securities mature, Treasury would pay that principal by auctioning new securities for the same amount (and thus not increasing the overall stock of debt held by the public). Treasury would delay payments for all other obligations until it had at least enough cash to pay a full day’s obligations. In other words, it will delay payments to agencies, contractors, Social Security beneficiaries, and Medicare providers rather than attempting to pick and choose which payments to make that are due on a given day.”

https://www.brookings.edu/2023/04/24/how-worried-should-we-be-if-the-debt-ceiling-isnt-lifted/#:~:text=Such%20an%20outright%20default%20on,credit%20to%20households%20and%20businesses.

It is worth reading all of the Brookings article. Of course anything is possible, but I am not going to hang my hat on an event that has never happened, and, which if it is about to happen, a plan is in place to deal with it. Others can do as they please.

There is no plan in place. Current Treasury officials have not said it would follow the plan that was developed in 2011. They may, or they may develop a different plan. And no matter what plan they follow, there almost certainly will be legal challenges. Of course people can do as they wish, but when I make an investment I’m not going to assume that people will act rationally or that there is no risk when there is.

Also, when Treasury developed their plan in 2011, they were trying to calm the markets and prevent a financial panic. So they wanted to assure bond holders that they would be paid. Whether their plan would have actually worked as they intended is anybody’s guess. Like most people, I think it is very unlikely that investors in Tresury securities will lose any money. But I also know there are plenty of other things that I thought were extremely unlikely but wound up happening anyway in spite of my opinion.

McCarthy’s proposal has a half dozen or so conditions that he wants met in exchange to agree to raise the debt ceiling. The Administration would probably only have to agree to one or two, such as student loan forgiveness, as part of a face saving compromise.

The problem with “compromise” (I personally would compromise) is that there are a dozen or so Senate Democrats who would not give up the student loan forgiveness, and it would harm Biden politically. So they won’t give on that. On the other side, there are about 20 House Republicans who will not give on any issue at all. So we get a crisis, practically guaranteed. The U.S. dollar will suffer.

If the stock market takes a big hit, I plan to move more shares of some stock funds from my traditional IRA to my Roth IRA.

The problem with using CofI accounts is the possibly limited amount of funds available there.

My bad, continued…

Since it pays 0%, I don’t normally keep excess money there. If the auction I intend to buy is priced higher than funds available – I lose out. So, I normally use a different account for funding

That’s true. But paying out from Treasury Direct to a bank account can result in a delay before the funds are available either to go back into Treasury Direct for another purchase or for another expenditure. It’s a balancing act. I’ve found that Treasury Direct is very quick to withdraw funds from my bank, but my bank is slower to credit transfers from Treasury Direct.

I have successfully exited from one T-bill and participated in an auction on the same day via a bank account, so it is possible. Both cleared on the same date.

TipTop, I was referring to participating in auctions PRIOR to a T-Bill’s maturity date, such that the issue date of a new T-Bill is the same date as the maturity date of the one funding it.

That’s interesting. I was worried about that in the beginning, but after running a T-Bill ladder for over a year, I’ve never had a new issue clear before the maturing one was deposited when they were scheduled for the same day. For me, when a maturity occurs on a Thursday, the funds are deposited very late on Wednesday night, with the new issues being withdraw first thing Thursday morning. Some of the Tuesday maturities have even been deposited late on Friday night when the Monday was a holiday.

To be sure I’m being clear, I use Treasury Direct’s 0% Certificate of Indebtedness as the destination and source when I have a treasury security maturing that is funding an issue the same day. I have found the transfer timing of deposits from Treasury Direct to my bank crediting them slower than transfers in the other direction. I don’t use the bank connection for closely-timed transactions.

One thought (not a prediction) on the 4-week T-bill: At some point as the crisis approaches, the 4-week could end up having the highest yield (or near the highest yield) of all the T-bills. In 2011 and 2013 the normal 4-week was yielding about 0.1%, and rose to a high of 0.16% on July 29, 2011 and 0.32% on Oct 15, 2013.

Darn, just switched 4weeks into 13 weeks for upcoming investment s

Doug, that still should work out fine. The differences shouldn’t be much, and the 13-week has had a great yield recently.

this is the summary and analysis that I have been looking for on the interwebs. thanks! Debating flattening at least a part of my portfolio to take advantage of the probably dip in the market. I will keep buying my i-bonds no matter what. Thanks again.

Doug, in my experience maturing funds that are deposited into zero-percent C of I are available the same day for purchasing new securities.

For example, say you purchase an 8-week bill on April 27 that will debit from your C of I account on May 2. If you have a 4-week bill maturing on May 2 (scheduled for deposit into zero-percent C of I, with no reinvestments), the funds from the maturing 4-week can be immediately invested in an 8-week bill for the same amount. You just have to make sure the maturing 4-week bill is not scheduled for reinvestment.

According to TreasuryDirect: “Debits to C of I will be processed daily in the following order:

Reinvestments – If additional funds are required to complete a reinvestment transaction and the original security associated with the reinvestment was purchased with C of I funds on or after May 15, 2010, your C of I will be debited.

Original Treasury marketable security purchases with C of I selected as the Source of Funds.

Savings bond purchases with C of I selected as the Source of Funds.

More info here: https://www.treasurydirect.gov/indiv/help/treasurydirect-help/user-guide/151-160/#152

This year, because of so many federally declared natural disasters, many taxpayers have been allowed to delay – without penalty – payment of their taxes for 2022 until October 15 that in normal years would already have been due by April 18. The question, then, is to what extent will the Treasury’s lack of this money bring the date of debt default even closer? Has the government run the numbers?

Interesting point, and could be a reason receipts are running low in April. Of course, a lot of those taxpayers may be due refunds, which would balance off the effect.

Many rich counties in California have deferred taxes until Oct. 15th due to natural disasters, so it’s occurred to me that the IRS may lack much needed funds when most needed. Along these lines, it’s also occurred to me with increasing natural disasters and climate change no way mitigated, municipal bonds are even riskier.

Nick Timiraos (Wall Street Journal), sent out this message via Twitter on April 26:

“Goldman Sachs says surprisingly strong tax receipts this week makes an early June debt ceiling deadline less likely and a late July deadline more likely.”

Question: How are outstanding TIPS counted as debt outstanding? With the inflation adjustment each month, does that constrain the room under the debt ceiling? Or cause it to be breached?

I don’t think any TIPS would be affected except possibly the one that matures July 15 2023 (I own that one). Since the inflation accruals aren’t actually being paid out until maturity, those shouldn’t be a problem. Coupon payments should continue, I think. It’s possible that the Treasury could issue new TIPS when one matures, such as July 15, but could it stage reopenings? Not clear.

Question. If you have all your cash in 4 week Tbills and you wanted to buy longer duration Tbills, how could you do this?

If these are at TreasuryDirect, you’d probably have to wait out the maturity. If at a brokerage, you can sell them, possibly with a loss. I generally recommend staggering T-bill purchases and rolling them over (maybe one purchase a week for the 4-week) and then you always have access to 1/4 of the money within a week.

At TreasuryDirect. So when the 4 week matures would those funds be immediately available to buy an 8 week or would you have to wait a week for the next auction?

As long as you don’t have a rollover scheduled, that money will be immediately deposited into your linked bank or brokerage, or you can have it placed in the the zero-percent C of I account. Not sure if that CofII money can be reinvested elsewhere on the same day (the 4- and 8-week auction on the same day). Others may know.

Same day works. I’ve used maturing 13’s to buy 26’s before, and they’re auctioned together.

When the 4 week matures, if those funds are being deposited into your 0% C of I in the account, you can actually have it go right back out into a 4 week or 8 week being issued the same day. In other words, you could be in the auction for the issue even before you have received the money back from the maturing certificate. Ex: if you have a 4 week T-Bill maturing on May 2nd, you can have a non-competitive order in for the 4 week or 8 week auctioning on April 27th. Maturing treasury issues are credited to your 0% Certificate of Indebtedness prior to paying out for new issues. I’ve done this numerous times myself. Caveat: I have no idea how this may or may not be affected by a default.

I recall transferring some notes out of Treasury Direct to my brokerage account some years ago. But it was a major hassle and not quick. Not recommended.

Also you can’t transfer anything out of TD until after a 45 day holding period, so a 4 week bill cannot be transferred under any circumstances.

Here are the treasurydirect instructions for selling a bill early.

https://treasurydirect.gov/help-center/treasury-bills/selling-treasury-bills/