By David Enna, Tipswatch.com

One of the year’s most interesting TIPS auctions is coming Thursday, the reopening of CUSIP 912810TP3, creating a 29-year, 6-month Treasury Inflation-Protected Security. Like many of you, I won’t be a buyer at this $8 billion offering. But for some, this TIPS offers a unique investment opportunity.

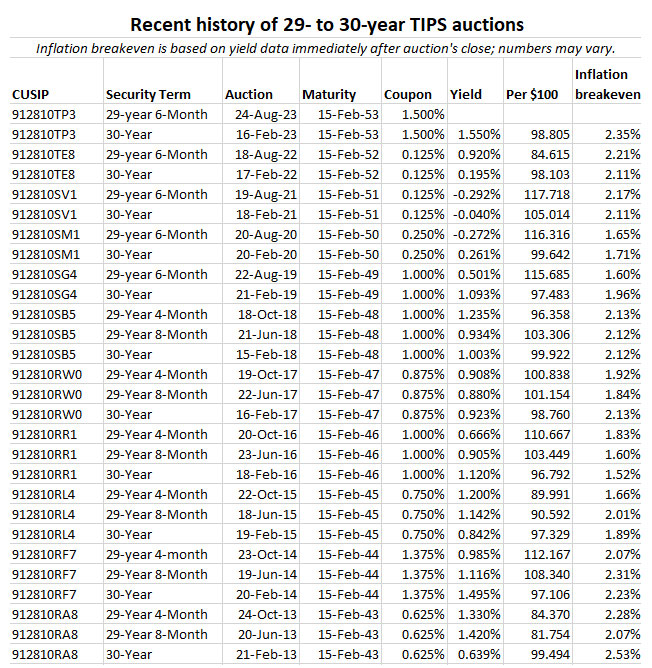

I say unique, but that could mean uniquely positive (a good possibility) or uniquely awful (there’s always that chance). But either way, this auction will be unique because it is likely to generate a real yield to maturity of close to 2.0%, or higher. No TIPS auction of the 29- to 30-year term has nabbed a real yield that high since February 2011, when a new issue got a real yield of 2.190%. Just two years ago, a similar August auction got a real yield of -0.292%.

CUSIP 912810TP3 trades on the secondary market, and Bloomberg’s U.S. Yields page shows it closed Friday with a real yield of 2.08%. If that holds on Monday, an investor could bypass Thursday’s auction and lock in a 2% yield over inflation. Or … just wait for the auction and get its result.

Definition: A TIPS is an investment that pays a coupon rate well below that of other Treasury investments of the same term. But with a TIPS, the principal balance adjusts each month (usually up, but sometimes down) to match the current U.S. inflation rate. So, the “real yield to maturity” of a TIPS indicates how much an investor will earn above inflation each year until maturity.

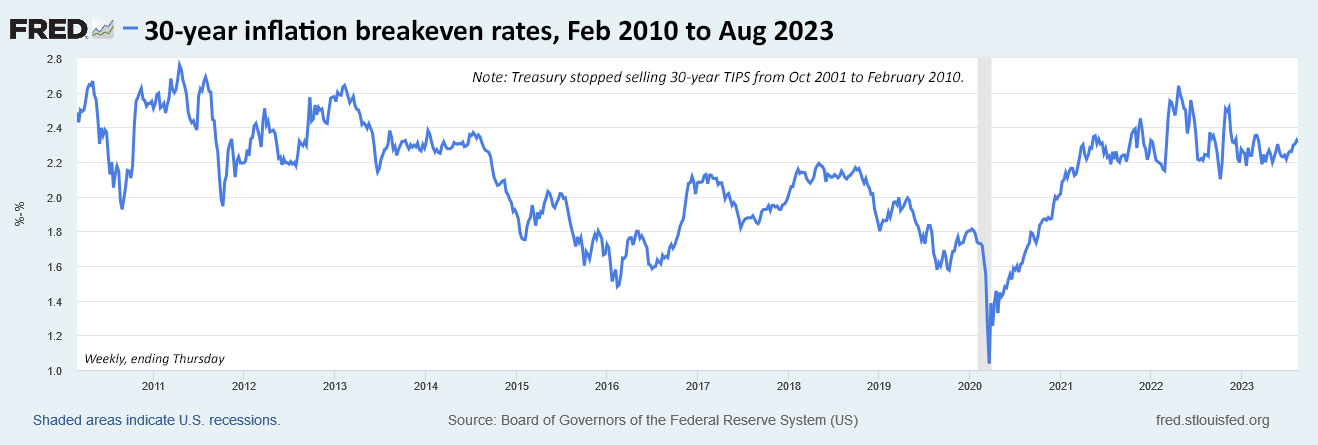

Here is the trend in the 30-year real yield going all the way back to February 2010, when the Treasury restarted the 30-year maturity after an 8 1/2-year pause:

The chart show the 30-year real yield only briefly topped 2% during this entire period, in 2010 and early 2011, and again in August 2023.

Some cautions

As I noted, I won’t be a buyer of this TIPS because it will mature when I am 99 1/2 years old. It doesn’t fit into my hold-to-maturity strategy. For others — age 60 or younger — it could fit as the top piece of a multi-year TIPS ladder.

It’s important to recognize the volatility of any 30-year Treasury investment. Even small swings in market real yields can cause substantial changes in the market value of a TIPS. For example, CUSIP 912810TP3 originally auctioned on Feb. 16, 2023, with a real yield of 1.55%, which at the time was the highest auction result in nearly 12 years. That set the coupon rate at 1.5% and the adjusted price was about 98.66 for $100 of value.

Fast forward six months and today that same TIPS has a real yield of 2.08% on the secondary market and its market price has dropped to about 87.34. So this TIPS has lost about 11.5% of its value in only six months. The lesson here is that long-maturity Treasurys are highly volatile; an investor has to recognize that going in. However, if the plan is to hold to maturity and collect 2.0% above inflation, market values aren’t much of a concern. Focus on the plan.

Also, I highly recommend purchasing any long-term TIPS in a tax-deferred account. In a taxable account, yearly inflation accruals of a TIPS (which are added to the principal balance) will be taxed each year as interest income. You won’t recoup that money until the TIPS is sold or matures after 29 1/2 years.

Pricing

On the auction’s settlement date of Aug. 31, CUSIP 912810TP3 will have an inflation index of 1.02632, which means auction investors will be buying about 2.6% additional principal. So an investor purchasing $10,000 par of this TIPS would actually be purchasing $10,263.20 of principal. At Friday’s closing price of 87.34, that principal would cost $8,963.88. Add in about $6.66 of accrued interest and you get to $8,970.54 total cost.

In essence, the investor is paying about $8,964 for $10,263 in principal, plus getting accruals to principal matching inflation for 29 1/2 years, plus collecting a 1.5% coupon along the way. This is a rough estimate based on Friday’s closing market value.

An inflation index of only 1.026 is another reason this long-term TIPS is unique. Because of very high recent inflation, the TIPS maturing in Feb 2052 has an inflation index of 1.094 (9.4% above par) and the one in Feb 2051 is at 1.170 (17% above par). Both of those TIPS also have coupon rates of just 0.125%, the lowest the Treasury will go, compared to 1.5% for CUSIP 912810TP3.

Inflation breakeven rate

With the nominal 30-year bond closing Friday at 4.38%, a 30-year TIPS yielding 2.08% would get an inflation breakeven rate of 2.3%, which is historically high but in line with February’s originating auction. Would I rather invest in a 30-year nominal paying 4.38%? Probably not, but for some this could be a toss up.

Here’s the trend in the 30-year inflation breakeven rate over the last 13 years, showing the range-bound pattern over recent months:

Final thoughts

I found an interesting article this week posted by Bloomberg on Yahoo Finance. The headline was: “Inflation-Protected Bond Bulls’ Pain Thresholds Get Tested.” It told how market strategists from TD Securities made a bet on 5-year real yields declining in the near future, hoping for a quick capital gain.

They targeted an improvement to 1.25%, expecting no further Federal Reserve interest-rate hikes and deceleration in US growth and inflation. Three weeks later, the stop-loss threshold of 2.20% was reached as those assumptions came under assault. …

Still, there’s scope for losses to deepen before support emerges, Dominic Konstam, head of macro strategy at Mizuho Securities, said in a Thursday interview on Bloomberg Television.

“There’s a limit to how far you can sell off,” he said. “Five-year real rates are pretty chunky at the moment, and if they go up another 20, 30 basis points that’s going to be quite attractive I imagine for a lot of investors.”

Why is that interesting? Because savvy market strategists got burned by betting on 5-year TIPS, the least volatile of the TIPS issues. Any bet on 30-year TIPS would have been hugely magnified, and hugely unwise.

I am not a TIPS trader and I don’t theorize on TIPS trades. It is possible that CUSIP 912810TP3 could end up being a big winner for traders, or a big loser. The only way I advise investing in CUSIP 912810TP3 is in a hold-to-maturity strategy, with full awareness of the potential losses (or possible gains) if you need to exit early.

An investor in CUSIP 912810TP3 this week can very likely lock in a 2.0% yield above official U.S. inflation for the next 29 1/2 years. And that is unique.

If you are pondering an investment at Thursday’s auction, keep an eye on Bloomberg’s U.S. Yields page, which updates in real time. It is accurate, but any auction result can bring surprises.

Thursday’s auction will close at 1 pm ET. Non-competitive bids at TreasuryDirect must be placed by noon Thursday. If you are putting an order in through a brokerage, make sure to place your order Wednesday or very early Thursday, because brokers cut off auction orders before the noon deadline.

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• Upcoming schedule of TIPS auctions

Here is a history of recent TIPS auctions of the 29- to 30-year term:

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

David, I really like TIPSWATCH. It has a lot of great information. I have been thinking about the following issue, and wonder if you have thoughts (or perhaps is a good topic for a future column). I have been buying maximum TIPs for quite a few years, and in 2022, when the rates were high, also bought some ibonds (including purchases for my wife and my wife for me) in our gift boxes at Treasury direct to capitalize on the high rates. Now it seems as though the gift bond purchases might have been a mistake — at 0% fixed rate they will no longer bear attractive interest rates. But I can’t cash them in without transferring the gifts. But if I transfer the gifts (say in 2024 and 2025), I can’t then buy new ibonds (other than with income tax refunds). I think the best plan is nonetheless to transfer gifts and buy TIPs, assuming rates remain about where they are. (things could of course change if rates change materially). Have you thought about this problem? I haven’t seen anything written on it.

Gary H

I can see the problem. I was never a fan of using the gift box strategy when the fixed rate was 0.0%, especially for multiple future years. But I do plan to use it later this year, either in October or November, to lock in a set of 0.9% or possibly higher fixed rates in November. I can understand the strategy of delivering the 0.0% I Bonds, cashing in, and then buying TIPS as a replacement, as long as TIPS real yields remain high. That seems to make sense.

UPDATE, 1:30 pm Wednesday: Secondary market trading in CUSIP 912810TP3 has it trading with a real yield of 1.95% and a price of 90.00. Real yields are dipping today after a week-long surge higher.

I bought $100 of this issue in Treasury Direct when it was issued in February. I told my spouse that I’d take her out for a half decent meal for her 67th birthday.

I would be very surprised if I notice this on my taxes. I can change the ratio of Roth to traditional retirement contributions if I think the couple dollars of unrealized income will threaten to bump us a tax bracket. In terms of part of retirement plan- I’m sure my pension plan will be investing in this TIPS.

Generally, my holdings in TD are shorter duration (6mo-5 year, a little in 5-10yr TIPS, and I-bonds) as a safe stash for near term goals/emergencies. All minor stuff relative to what others seem to throw around, but it’s something.

J.D., that’s a nice experimental purchase and it’s good that TreasuryDirect allows purchases of just $100. That particular asset should only generate about $5 of income this year, so taxes should not be a problem.

I like TreasuryDirect for that reason – the buy in threshold is low. With minimal effort, some knowledge of using pivot tables, and regular contributions TreasuryDirect allows building savings with better interest earning efficiency. It works for me (especially lately) because I exist solidly in the 12%-(soon) 15% tax bracket. Essentially, TreasuryDirect is a nice service for “the common man.”

But I am way afield from the topic of this post.

I like the idea of the 30 year TIPS, but instead I’m eyeing the 30 year bond auction in November for a “more income sooner” rather than “inflation-adjusted principle later” approach test. Every $4-5 counts when I can put the $4-5 somewhere else. When I get the principle back near my 66th birthday it may only be enough to buy a growler of cheap beer, but that’s good enough for me.

Thanks for the note on what the income will be this year on this TIPS. I need to set up another worksheet for those projections on the few TIPS I’ve purchased.

J.D. your post provides an other example of why TD is great, if a person wants tax deferred options, it is possible, if a person wants income now, it is possible, if a person wants income trickled over a duration, it is possible. A pretty well thought system. There can be much more strategy involved in selecting the best silo at any particular time than most might consider.

I’m just a TIPS beginner but have learned a lot very quickly because of this blog. As I read comments on trading vs holding to maturity and value vs interest rates, it make me think that TIPS is like going to a party where you know that you’ll have a pretty good time. There may be other parties that are a bit more fun or they may be awful … and bad parties really suck.

TIPS do offer some investment certainty (versus inflation). Other investments will likely do well, too, but don’t have that certainty.

I’m not TIPSWATCH, but I view TIPS as a supplement to Social Security, not really as an “investment.” If I could buy extra Social Security I would, but since I can’t, a TIPS ladder is the next best thing but only in a 401k or IRA.

That’s a great way to look at it IMO. It takes a lot of the investment-related FMO emotion out of the decision. Well done!

This one is well beyond my life expectancy, and I’m pretty sure the kids will just have a fire sale. I’m going to beef up a few rungs lower on my ladder, and think about picking up a few more ibonds.

No kids for me, but I agree on the 30-year span.

I’m a buyer for a small amount $15k. Also bought $15k in the February 2023 auction. Probably stocks will beat long term bonds over 30 years (I’d guess 90% probability). I want some fixed income though with a future nominal pension inflation protection is attractive so buying now at 47 to spend at 77. Hopefully I will regret it since that will have meant the rest of my stock heavy portfolio will have grown greatly.

It’s difficult to come up with a set of circumstances that would lead to 30 year TIP being a good investment at this time

David, Another great article. I totally agree with you – I buy bonds for protection of principle, so I only buy treasuries and only if I plan to hold them to maturity. I’m convinced no one can accurately predict future interest rates, so buying bonds based on what I think interest rates will do in the future is gambling, not investing. A couple of reasons why I think this TIPS auction might not be so “unique” or attractive as it first seems: 1) Back in 1999, the real yield on the 30 yr TIPS was 4.27%, so rates certainly have been a lot higher, 2) With the Federal deficient spiraling out of control, the supply of treasuries growing along with it, and a downgrade in the US credit rating, this will continue to put upward pressure on yields 3) If you are going to hold an investment for 30 years, you’d probably be much better off holding an S&P 500 index fund. The average annualized 30 yr rolling return for stocks is about 9.4%, or about 6 – 7% when adjusted for inflation

For most investors, a 30-year TIPS would fit in as part of fixed income portfolio, and would be a small percentage an overall portfolio, which would also include, probably, a low-cost total stock fund. Highly respected financial author William Bernstein recently talked about why he was buying a 30-year TIPS as a riskless asset, even though it would mature when he is 104 … https://www.advisorperspectives.com/articles/2023/03/20/riskless-at-age-104

I like the “bucket approach” promoted by Christine Benz at Morningstar. She divides her investments into 3 buckets (You can vary the number of buckets and the time limits of each if you prefer): 1) Money needed within the next 2 or 3 years, invested mostly in cash and short term treasuries or CDs. 2) Money needed in the next 5 to 10 years, “dominated by high-quality fixed-income exposure, though it might also include a small share of high-quality dividend-paying equities and other yield-rich securities”. 3) Money needed more than 10 years out, “dominated by stocks and more volatile bond types such as junk bonds.” I haven’t looked into it in detail, but some experts claim that over the long term junk bonds outperform treasuries. https://www.morningstar.com/portfolios/bucket-approach-building-retirement-portfolio

That 4.02% 30 year real yield in 2000 was a short (a fee months) window around 11/99 that seems unlikely to be repeated. If you wait for that you could miss out on a potentially good deal now.

Very good point. When TIPS were first introduced the market didn’t really grasp how to price them. So in the original period from 1998 to 2001, real yields ranged from 3.4% to 4.1% for 30-year TIPS. Then that maturity was discontinued. When it returned in 2010, the real yield was down to about 2.2%, pretty close to where we are today.

At what age is the right time to build a TIPS ladder? At retirement?

I don’t think there is a “right” answer, but the multi-year ladder is definitely a retirement cash-flow strategy. Since TIPS have maturities up to 30 years, I’d say age 60 makes sense, or a bit earlier.

“On the auction’s settlement date of Feb. 28, CUSIP 912810TP3 will have an inflation index of 1.02632…” Isn’t the settlement date in August?

Thanks agin for these informative postings…They have been so helpful!

Correct! I had both summaries up at once and mindlessly looked at the wrong one. Fixed and thank you.

It doesn’t matter whether you intend to hold it to maturity, David. What matters is whether you think it’s a good value for the money, i.e., do you foresee real interest rates continuing to go up (thus resulting in a capital loss on the TIPS) or do you think it is more likely real interest rates go down from here (thus resulting in a capital gain on the TIPS). Pretending capital gains and losses “don’t matter” just because you have convinced yourself that there is no way you would never ever need to sell before maturity–or simply desire to do so if circumstances in the future warranted–is the worst kind of mental accounting.

Of course, we disagree. I’ve never sold a TIPS early. I know what my real return will be. That’s all I need.

And it is very poor statistical analysis to make any plans, or projections of future equity returns, based on 100 years of stock market returns (1925 going forward) regardless of what pundits or professors contend. ( See, Triumph Of The Optimists, 2002, Princeton University Press)

David is right.

Hi! Thank you very much for your work. You opened a world of TIPs for me! I have an idea of dollar cost averaging into this 30 year tip if rates increase more in the future. I want to bet that the rates will eventually fall and I can sell it for profit. The strategy is the following: I buy when the rates are at 2%, if rates increase more I will be reinvesting semiannual interest and part of my paycheck into this issue basis. What do you think about this strategy? Thanks

As I noted, I am not a TIPS trader and this is TIPS trading. It could work out. Keep in mind that the 30-year TIPS that auctioned in Feb 2022 has lost about 40% of its value in 18 months. But conditions are much better now. Volatility can be your friend, or your downfall.

1.5% is not a high coupon, but I still prefer the minimal .125% coupon of TE8 and SV1, which is almost a STRIPS/zero coupon. I prefer them because there’s less reinvestment risk, or frankly, just less hassle of remembering that you have to manually reinvest the coupon in new TIPS or a TIPS fund if available to maintain maximum inflation protection. I’ll remember to do it, but when I’m gone, I seriously doubt that my 29-year-old daughter or my wife will. While I’d prefer a low bond factor too, relatively speaking it matters very little, as the risk of deflation over 29.5 years is low indeed.

I can see this logic.

Another excellent analysis….thanks!!!

Savvy market strategists did I read? I used to take the January issue of Barron’s financial magazine with its annual Roundtable discussion and wrap Christmas decorations. Then a year later one could review how their predictions worked out. Virtually no one is right consistently. Smoke and mirrors to keep the game interesting.

I subscribed to Barron’s for 20+ years. In year one, I poured over that Roundtable discussion for ideas. In year two, I skimmed it. By year five, I skipped it entirely.

A cheap education at that though.

This post made rethink getting into tips. sound like alot of things going

As always, it seems to me that it might be a great time to invest…or it might be better to wait. I guess that’s where dollar cost averaging comes in. Invest a little in this one and a little in the next. But I’ll be 80 in 30 years. I don’t think I’ll invest much for that timeframe. Birthday present to the future me.

A new 30-year TIPS will be auctioned in February and that one could also end up being attractive. But there is no way to say where real yields are heading.

David, I know the basics of real yield such as nominal minus inflation; as economy grows so do real yields and vice versa; and as Feds raise rates real yields go up and vice versa, level of US debt impacts real real yields, etc. I also know that we can track them on Blommberg.com, real time. I will love hear your opnion on i) what influences them the most, and ii) where to find real yield projections. For example, CME Feds watch is great about the Fed rates. Is there something similar for real yields?….thanks!!!

Chander, I have pondered what influences real yields for years, and I haven’t found an exact answer. Obviously Fed policy matters and real yields tend to track higher when nominal rates rise. Fear of inflation also matters, but that can create higher demand for TIPS, which can cause lower real yields. Inflation expectations seem to be settling in at about 2.2% right now, which seems optimistic.

David, thanks much for your response. As I see it, your comment “Fear of inflation also matters, but that can create higher demand for TIPS, which can cause lower real yields.” pertains to” inflation expectations” which is closely watched and monitored by the fed. I understand how fear of inflation results in higher demand for TIPS. However, how does higher demand for TIPS cause lower real yields? All these tangled reverse relationships still confuse me. So much to learn from you and all your blog subscribers.

I agree with you on inflation expectations settling at 2.2% being optimistic. I think we will most likely see 2.5 to 3.0% of inflation for a long long time…best

David, thanks much for your response. As I see it, your comment “Fear of inflation also matters, but that can create higher demand for TIPS, which can cause lower real yields.” pertains to” inflation expectations” which is closely watched and monitored by the fed. I understand how fear of inflation results in higher demand for TIPS. However, how does higher demand for TIPS cause lower real yields? All these tangled reverse relationships still confuse me. So much to learn from you and all your blog subscribers.

I agree with you on inflation expectations settling at 2.2% being optimistic. I think we will most likely see 2.5 to 3.0% of inflation for a long long time…best

One more thought: with almost all centeral banks pumping liquidity into their economies for about 4 decades, the neutral rate, representing reqiured interest rates representing equillibrium, going forward, has to be higher. Which means, gone are the days of low interest rates. As a fixed income seeking investors, it should make us happy though one never knows how all this plays out.

I don’t ask about the breakeven point for my life insurance. Why would I do that for my inflation insurance? Moreover, the insurance “premium” for TIPS is close to $0.

Chander, I agree with you on this new era of higher-than-recent interest rates. Rates could slide lower, but I don’t think we’ll see a 0.25% federal funds rate in the near- or mid-term future. The Fed is hamstrung by its huge balance sheet, which must be unwound.

Higher demand for TIPS does cause the inflation breakeven rate to rise, which means TIPS yields are falling (due to high demand) while nominals are rising or stable. Right now both real and nominal yields are rising, so you see the breakeven rates stuck around 2.2 to 2.3%.

got it…thanks!!!