By David Enna, Tipswatch.com

The Treasury’s $8 billion reopening auction of CUSIP 912810TP3 — creating a 29-year, 6-month Treasury Inflation-Protected Security — went off pretty much as expected Thursday, generating a real yield to maturity of 1.970%.

While that result fell just short of a milestone 2.0% real yield, it was higher than where this TIPS was trading most of the morning, at about 1.93% to 1.94%. So investors should be pleased. The real yield of 1.970% was the highest for any 29- to 30-year TIPS auction since February 2011.

This TIPS had its originating auction on Feb. 16, 2023, which generated a real yield of 1.550% and set the coupon rate at 1.50%. So, six months later, real yields for this term have increased 42 basis points. And that means this TIPS sold today at a discount, because of the wide gap between the auctioned real yield (1.970%) and the coupon rate (1.50%).

Investors got an unadjusted price of 89.533532 for $100 of value. The inflation index on the settlement date of Aug. 31 will be 1.02632, pushing the adjusted price to 91.890055, still well below par value.

In essence, investors paid about $91.89 for about $102.63 of principal, and will now collect accruals to principal matching U.S. inflation, along with 1.5% annual interest on the inflation-adjusted principal. Here is how the pricing worked out:

Inflation breakeven rate

With a nominal 30-year Treasury bond trading today at 4.29%, this TIPS gets an inflation breakeven rate of 2.32%, which is in line with the February result but higher than other auctions of this term over the last decade. Investors in this TIPS are betting that inflation will average higher than 2.32% over the next 29 years, 6 months.

As this chart shows, 30-year inflation expectations have been rising since 2020, but have been in a range of 2.2% to 2.4% for the last several months:

Reaction to the auction

The bid-to-cover ratio was 2.42, which indicates reasonable demand. The yield came in fairly close to secondary market trading, so by all indications this auction went off without a hitch.

After strong increases in real yields over the last two weeks, the trend turned slightly downward on Wednesday, with the Treasury’s 30-year real yield estimate falling from 2.07% on Tuesday to close at 1.93% on Wednesday. So today’s end result of 1.97% looks like a positive auction for investors.

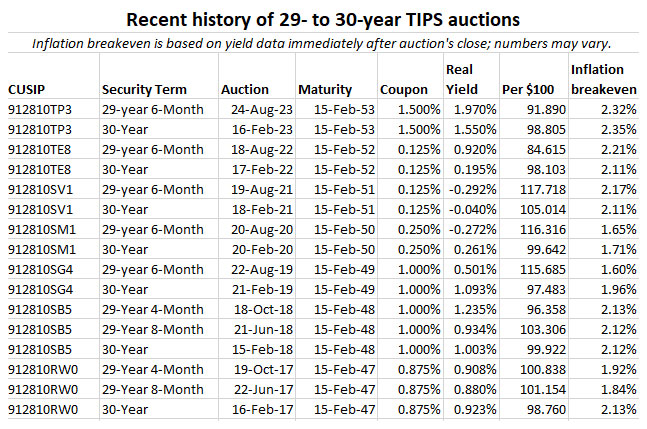

Here is the trend in recent TIPS auctions of this term:

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• Upcoming schedule of TIPS auctions

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

the commentary starting at 49 minutes here indicates to wait for further yield

improvement in UST over the next two quarters. What are people’s takes on this? https://youtu.be/hn-9ffDhGAo?si=Kh10bkHu7gZ5uM39&t=2940

I’d agree that long-term rates seem too low given the U.S. borrowing needs, but it’s impossible to predict. I praised Fitch for its debt downgrade, even as mainstream Wall Street was skeptical. So, what do you do? Stay in cash to hope rates rise? (And feel regret if they fall?) Or gradually invest in as rates rise?

I didn’t watch the video, but I would say that trying to time it to hit the absolute top of interest rates would be more a matter of luck than skill. Who really knows?

Because I had a large cash position before rates started rising, I have more in treasuries and CDs than I ever imagined. A good number are short term so if rates remain high or continue rising I can hopefully lock in some longer term rates. Won’t be trying to guess the top…

Ah yes. Good point. Thank you for being patient with me.

I am certainly getting interested in buying TIPS at this time. Pardon me for being naive but would you kindly let me know what you think of the below:

I understand that one should not be timing when it comes to buying something like TIPS and wanting to hold till maturity.

With that said 🙂

I am thinking, I would be a buyer of TIPS (10 or 30 Y) when BOTH of the below conditions are satisfied. Am I being too ambitious? 🙂

The real yield is greater than or equal to 2%

The break even rate is less than or equal to 2%

Please let me know your thoughts.

I actually think some level of timing makes sense. It kept me from buying TIPS for years when real yields were deeply negative to inflation. At this point, it will probably be hard to find 10- to 30-year TIPS with both real yields above 2.0% and breakeven rates below 2.0%. If you are truly holding to maturity, looking for that 2.0% real yield is a good goal. My opinion is that the breakeven rate is less important unless you are considering nominal Treasurys as an alternative.

Ah yes, I could buy either (nominal or TIPS). I guess, I have to pick sides right?

Either,

I should be inflation protection (and therefore 2% real yield goal)

OR

I should be simply buying one vs. another based on what is baked into the breakeven rate.

Am I thinking correctly?

Nominal Treasury is a lot riskier than TIPS. Unless you hold them to maturity, you will go the SVB route. Learn from David. He has no axes to grind, and gives an honest outlook that is his opinion. Learn and invest as per your situation.

But don’t TIPS have the same investment rate risk as nominal treasuries? If SVB held TIPs instead of nominal treasuries, wouldn’t they have had the same issue since they didn’t match the duration of their holdings with their liabilities?

Bo + Known + Michael … To be clear, I have nothing against investments in nominal Treasurys, and Michael is right that long-term TIPS have the same interest rate risk as a long-term Treasury bond. Holding to maturity lessens (or even eliminates) that risk, for either kind of investment. Right now, as I have noted in other articles, I am going with nominal Treasurys and bank CDs for investments of less than 5 years, and TIPS for investments of longer terms. I do believe that inflation protection is extremely important for a long-term investment, and getting 2% over inflation is attractive. …. On the other hand, if we hit years of severe deflation, that 20-year nominal bond paying 4.5% is going to look great.

Bo, this site focuses on inflation and inflation protection, so most people here are interested in TIPS over nominal Treasurys. I tend to use nominals for shorter-term investments, 2 years or less or even 5 years at times (for example, bank CDs). The idea with TIPS (and I Bonds) is to create savings in safe investment that will be guaranteed to match or exceed future inflation.