There is an explanation for everything, right?

By David Enna, Tipswatch.com

As they say, “You learn something every day.” At least you should learn something every day. Thursday’s TIPS auction result, which you can read about here, caused some angst among readers: Why did the real yield come in below the market?

I was especially curious when I saw that the “when-issued” real yield prediction used by bond traders was 2.42%, well below the Treasury’s yield prediction of 2.57% for a 5-year TIPS (that prediction dropped to 2.43% after the market closed yesterday.)

Unfortunately, I can’t see the when-issued prediction until the auction closes. But if it was 2.42%, that indicated bond traders knew the Treasury estimate was too high. The auction actually got fairly lukewarm demand, and the resulting real yield ended up at 2.44%, above the when-issued prediction.

So what happened, and what can we learn from this?

Thursday’s lesson was about relearning something: Seasonal variations in TIPS yields. I discussed this topic in a post on Sept. 10: “‘Inflation Guy’ explains seasonal adjustment (or lack thereof)“, where inflation expert Michael Ashton explained why there are seasonal variations in TIPS yields.

But I clearly did not realize how much these seasonal variations affect one particular auction a year: the new 5-year TIPS issued each October since 2019. Could seasonal variations be the reason bond traders saw a yield of 2.42% while the Treasury and secondary market seemed to pointing to 2.57%?

The answer seems to be yes.

Beth Stanton, an editor for U.S. interest rates at Bloomberg, posted an excellent explanation on Twitter yesterday (I refuse to call it X, by the way). Here is how the series of tweets began:

And this is her explanation that followed:

Auctions of new 5Y TIPS have been held twice a year — in April & October — since 2019. (The June and Dec 5Y TIPS auctions are reopenings of one or the other.) …

The October auction usually produces a yield *significantly lower* than the current market yield of the one from April, despite maturing 6 months later. Normally in bonds (tho not so much lately), a longer maturity warrants a *higher* yield. …

The 5Y TIPS being sold on Thursday is trading at a yield of around 2.42%. The one sold in April (auction yield 1.32%) now yields around 2.53%. That’s a big gap for 6 months, especially since the new issue is the biggest-ever TIPS auction at $22b. …

The question is, why would someone buy the new issue at a yield of 2.42% when the old one can be had at 2.53%? The main reason is what inflation people call seasonality premium. …

Interest on TIPS is paid on a principal amount that’s indexed to the CPI — with a lag. The final index values for TIPS that mature in Oct are determined by the Aug CPI. The final index values for TIPS that mature in April are determined by the Feb CPI. …

The CPI used to adjust TIPS is the not-seasonally-adjusted one. And inflation has had a strong seasonal pattern. The pattern fell apart in 2020, but prior to that, prices reliably rose more early in the year than late in the year (when discounting is rampant). …

The Oct 5Y gets inflation accruals for six months after the April one matures. The months are March-Aug, which historically have been “better” overall than Sept-Feb. That gives the Oct issue extra value that gets reflected in a lower yield (i.e. higher price) than the April one. …

Other factors contribute to the Oct 5Y TIPS yielding less than the April, such the inverted yield curve (longer maturities in general command lower yields than shorter ones) & a liquidity premium for the new issue. But inflation seasonality is the biggest piece. /END

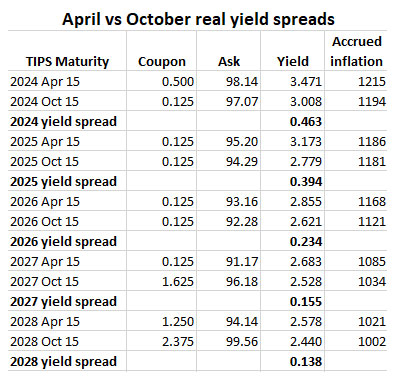

Again, this is something I knew about, but I hadn’t associated these seasonal fluctuations directly with the auction of a new 5-year TIPS each October . It’s a hard trend to decipher because these October auctions only have a 5-year history, dating to October 2019.

This chart proves Stanton’s point quite clearly:

The yield spreads get larger as the maturity date gets closer, because the effect of seasonality is strongest when fewer months remain. So, based on this analysis, a 14-basis-point yield spread looked predictable coming into Thursday’s auction. And it also indicates that investors at Thursday’s auction didn’t get “ripped off.”

Lesson learned. File this one away for future October auctions of 5-year TIPS.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Pingback: What about Thursday’s auction of a new 5-year TIPS? | Treasury Inflation-Protected Securities

Pingback: Questions surround this week’s 5-year TIPS reopening auction | Treasury Inflation-Protected Securities

Good afternoon David. We just purchased our first TIPS a few months ago. I understand that TIPS are adjusted monthly for inflation, but interest is paid only every six months. Do you have an article that walks through how the monthly adjustment works and where to find the inflation numbers so that we can track it in Excel? We are planning to buy more and will hold to maturity, so the market value is not really helpful.

The value of all TIPS is adjusted for inflation every day, based on non-seasonally adjusted inflation two months earlier. You can see how that works in this chart of November inflation indexes for all TIPS, based on inflation in September https://www.treasurydirect.gov/instit/annceresult/tipscpi/2023/CPI_20231012.pdf …. So the principal balance is constantly adjusted, but interest (based on the coupon rate) is paid every six months. The interest is paid out, it does not add to principal.

I include a link to those inflation index charts every month when a new inflation report comes out. And tomorrow we will get the December indexes, based on October inflation.

You can track the inflation index for each TIPS here: https://treasurydirect.gov/auctions/announcements-data-results/tips-cpi-data/

I have a general question that has no definitive answer, but would like to hear from others. Even if to justify my approach.

When tracking total portfolio value do you use “current” value of a TIPS. based on the index or do you use “market” value if you sold before maturity. Since I intend to hold to maturity, I think I’m justified in using the current value as per the index.

And it makes me feel better. 🙂

If you really seriously + absolutely intend to hold to maturity (as I do) then I highly recommend tracking par value x inflation index in a spreadsheet separate from your brokerage account. (If you have TIPS holdings at TreasuryDirect, this is more or less how you will see them there.) But in your brokerage account and probably in software like Quicken, you will continue to see market value. And that market value will be the amount that determines future RMDs if you face that issue.

As David said, for you, tracking par value x inflation index is the way to go. Market value has value for those who want to trade, and, as you know, it constantly changes; it may have use for going through wasted emotions 🙂 I did not know about RMDs use market value, thanks David!!, well, I have 5 years before I may need to use this.

A bit off topic, David. I am 70 and would like to protect a sizable portion of my retirement portfolio from inflation for future use. I don’t need to draw on these funds for a decade or so. Would you recommend an evenly divided ladder, a ladder weighted toward 2033, or putting it all in 10 year TIPS?

You have a great blog. I have found it very helpful.

Forgot to mention, these funds are in a traditional IRA account.

This is a question for a financial adviser who understands your needs and style. A quick thought is that if you don’t need the money for 10+ years, you could focus purchases on individual TIPS maturing in 2030 to 2033, which have very good yields. If you hold to maturity you should do fine. Or just purchase a TIPS maturing in 2033.

Thanks, David. I was thinking along the same lines.

Paul

If the rate on the 10 year is about 5%, why is the coupon at 3.875%? I see that the 2 year is at roughly 5.11% and the coupon is 5%, which makes more sense to me. I know the price can be dropped, but why doesn’t the government adjust the coupon more quickly, and how does the process work when the government adjusts the coupon?

Those quotes you see are the last issue trading on the secondary market. The price you pay will be discounted on the secondary market, so you get 5.1%.

Thanks! I’m using Vanguard to buy at auction, and was surprised at the lower coupon, but with a discount. I guess it all works out, but just expected the coupon to be more reflective of (ex 5% on a 10 year). I thought the coupon might work in increments of 0.125 up to the rate, and then the bond would be discounted to be more precise. But my expectations weren’t based on anything other than my few observations.

I believe that was a 10-year reopening, so the yield was set by the originating auction.

This is just my thoughts i am sharing:

Complaints arise from the individual investor mind that had expectations about something going a certain way and disappointment when it didn’t and confusion / suspicions when the reasons for it are not readily apparent.

David did such a selfless and good job in this post that settled many “bundles of thoughts”, each one. one’s own, rooted in disappointment, confusion, doubt, etc. when auction yield did not align with expectations arising from bloomberg and other sources of predictions for expected yield.

Yes, H is correct ! It is not an issue of a “prediction” miss,

It is an issue of an unexpected COST or FEE. It is like an expense ratio for a mutual fund or an ETF. Instead of 2.57% we got 2.44% because of an unexpected 0.13% “expense ratio”

every year over the 5 year holding period.

The “loss” was due to some Headache producing esoterica explained by Beth Stanton – a Bloomberg Pro.

David did a GREAT research job digging out the reason for the “loss”; -And a great job explaining it.

At least we know we were not out right cheated.

I would have NEVER expected such a thing on a simple treasury auction for TIPS.

It turns out TIPS prices at auction can be very complex.

I guess it is also true it won’t “break the bank” and we still got a reasonably decent investment all considered.

I am very thankful we have this wonderfully informative Blog.

What is a prediction worth anyway? I am just happy to get 2.44% real yield after getting only 1.32% real yield in April. In the long term it’s not going to make any difference in anyone’s life whether you get 2.57% or 2.44% in this auction. So what are people complaining about?

While 2.44% is far higher than the 1.32% that we got in April, it’s a wrong comparison. By that logic 1.32% in April was far better than the zero or negative yield in earlier years. One has to look at what the alternative similar investment options are yielding concurrently. I am sorry but comparing current 5-year TIPS yield to past yields is a form of rationalization.

Thoughtful response. I see your point. As Dave says, getting 2.375% rate on a TIPS is a very positive development, have net seen a deal like this in the last 15 years..

I look at it this way, 2.42% is still very nice compared to the -1 percentish we were getting just a few years ago.

Reminder: When you buy a new-issue 5-year TIPS at a below-par price, with a coupon rate of 2.375%, you are guaranteed to get a positive return of at least 2.375% annually even if we get 5 years of deflation. That’s a very positive development and something we haven’t seen in 15 years.

Sorry, wrong website URL / Address for CNBC daily 5 yr TIPS yield chart on my previous post. It Should be:

https://www.cnbc.com/quotes/US5YTIPS?qsearchterm=

I suspect they are measuring real time yields in the secondary

( then adjusted for the current day based on discrete secondary CUSIPs interpolated) ….as done by the daily close yield values on :

https://home.treasury.gov/resource-center/data-chart-center/interest-rates/TextView?type=daily_treasury_real_yield_curve&field_tdr_date_value_month=202310

on 10/19 after market close CNBC picked up the auction yield = 2.44%

Even tho the auction I think took place near noon.

Frustrating confusing stuff !!!

** Disappointing** but still ok/decent even at lower rate as you say.

Tracking thru entire day 10/19/23 Yield never hit the low at auction on:

https://tradingeconomics.com/united-states/5-year-tips-yield

and…

https://www.cnbc.com/quotes/US5Y

I am not sure if Bloomberg rates thru day got it right either.

**This left a bad taste in my mouth.**

I had always thought the treasury auctions looked out for the “little guy” investor,

but apparently they do not !!

——

after market close auction rate appeared on treasury.gov:

https://home.treasury.gov/resource-center/data-chart-center/interest-rates/TextView?type=daily_treasury_real_yield_curve&field_tdr_date_value_month=202310

—————————

Thanks for the twitter Find that “explains”.

So complicated tho that it is useless for trading for the average person !

Only “takeaway” is TRADE ON THE SECONDARY FOR TIPS !!!!!

Can you explain when the principal amount of the TIPS get adjusted for inflation. I have 5 yr TIPS from earlier in the year with a 1.62% yield but the principal amount keeps going down due to the rate increases. However, I thought that the principal amount got adjusted every 6 months but just don’t know when it will happen. Just don’t understand the details so looking for some clarification.

The actual principal amount is adjusted for inflation daily. The market value goes up or down depending on if real yields are going up or down.

If you intend to hold that 5-year TIPS to maturity, then you can safely ignore the current market value, which will vary as real yields change. The redemption value at maturity is based entirely on the inflation index, as are all of the semiannual coupon payments.

I’m not convinced by this analysis. I think the inverted yield curve may have more of an impact than you are allowing for. If you restructure your comparison to show October 2026 vs April 2027, etc. there are much smaller differences for the 6 month periods.

Steve, that’s an interesting point. It does show how a limited sample can skew the view. But looking at that small sample it is also clear that the April yield has been higher than the October yield immediately preceding and following. That does seem to fit with the theory regarding seasonality. I think the overall pattern of descending yields through this sequence may be playing to the differences observed.

Thanks, I agree with you and David. So would you buy the October or April maturities? I’ve been buying the April 2027, staying short term and grabbing the higher yield.

So being unaware of this seasonal variation before David’s post, I bought more Apr ’28 a few days prior to the October auction instead of waiting for the auction. To me it was just close enough not to get worked up about a few points. The defined benefit public pensions my wife and I have – our major source of retirement income – provide a degree of inflation protection. Our TIPS purchases are relatively small, to provide a bit of similar protection through our IRAs. We started with buying at auctions, then expanded a bit to secondary offerings to fill in as we learned more. The advantage of buying the auctions rather than secondary have been to dip in at smaller quantities. Our minimums in our IRA brokerage accounts are $1K increments for Treasury auctions vs. $5K in the secondary market. In the 5 year maturities we hold both October and April fairly split. It just worked out that way. Which will we prefer in the future? Whichever seems more appealing at the time we have the desire and the money to fill in another spot on the ladder. None of this makes enough difference to me to sway me one way or the other. It’s more a bit of intriguing data to explain why some differences exist. We’ll be taking it into consideration for additional 5y and 10y TIPS purchases, but we’ll focus on the macro of the real yields rather than the minutiae of a few points difference.

The inverted yield curve is a factor for short-term TIPS (as Stanton noted), because the market expects inflation to glide lower in months/years. But if you look at these sets of yields, notice that April is the highest, October is the lowest, and January (the later month) is always higher than October:

2025 Apr 15 3.184

2025 Oct 15 2.760

2026 Jan 15 2.840

2026 Apr 15 2.813

2026 Oct 15 2.565

2027 Jan 15 2.670

2027 Apr 15 2.642

2027 Oct 15 2.469

2028 Jan 15 2.564

Doesn’t the disparity between projections (2.57%) vs, actual (2.44%) reek of market manipulation?

No.

So 2.42% of a bigger number is better than 2.53% of a smaller number so 5 year TIPS purchased in the Fall is the better choice?

Or … basically a wash?

Hi David, I’ve been thinking about this and am glad there finally is some actual data to help provide an explanation for yesterday’s result. Thank you. So what are the GENERAL lessons here? Should one always buy TIPS that mature during the first half of the year even if that means buying on the secondary market rather than at auction? I bought TIPS on the secondary market about 45 times over the past year (looking for best yield and an adjusted price close to or below par) and 44 out of 45 times the TIPS I purchased mature in either Jan or April. And second, under current market conditions (historic high real yields) is it better to buy a similar TIPS a day or 2 before an auction rather than wait for the auction? Seems like the drop in yield at auction has been fairly common all year long (not just later in the year.) Are there any data to compare real yields at auction vs the day or 2 before across all maturity dates? Thanks!

I think main point Beth Stanton is making is that the TIPS real yields reflect the reality of future inflation adjustments, especially for shorter-term TIPS. So the market is balancing off the real yield versus potential dip in inflation accruals for certain months. The market is pricing things correctly. On the issue of purchase dates, in 2022 auctions consistently were getting slightly better yields than the secondary market. But that reversed in 2023. And because there is now an opportunity to get great yields across all maturities, the secondary market is the way to go.

I wasn’t really concerned about whether the market was pricing things correctly or not. I suppose one can always come up with some explanation for what the market did (rational or not.) My real question was: do you think the pattern is clear enough so that you would avoid any auctions for TIPS that mature in the second half of the year? Thanks.

I wouldn’t avoid auctions in the second half of the year. In some past years, the December 5-year reopening was the best auction of the year, mainly because the Fed had raised short-term rates a few days before each auction.

Agree on your first part – whether or not it was priced correctly is moot point. Whatever rate it gets is the real market rate.

The real question for me is : Now that we know this, how do we estimate the correct rate ? Article says that bond traders were estimating it at 2.42% vs on the secondary market 2.57%. Clearly, their estimate is better than what we were going by. How do we get access to what bond traders were seeing, before the auction ?

Spend $30k per year for a Bloomberg terminal?

We need ONE READER who has the Bloomberg terminal who can provide this information in advance. Who is volunteering?

If there was any clear benefit to buying at one time of the year as opposed to another, my assumption is the market would correct for that and that you’d end up with the (approximately) the same final ending point either way.

I think being priced correctly means that you are getting equivalent value if you had bought the April issue on secondary market versus October issue at auction on the same day.

The real yield (which is just yield above inflation) for April is slightly higher, but the average remaining inflation accrual is expected to be relatively lower based on historical trends. The October auction just got a lower real yield, but average inflation accruals are expected to be higher overall because it includes the 6 months after the April issue matures and that is the part of the year with higher typical inflation. That inflation difference is expected to offset the real yield so the overall return rate will be roughly equal for both.

If inflation were not systematically (i.e., seasonally) variable throughout the year, then the real yields would behave more consistently regardless of month of issue.

That is how I understand this anyway. If I’m correct, the point is that buying an issue from one month versus an issue from another month may bring a systematic difference in real yield, but that doesn’t mean you are likely to earn less from one versus the other.

Paul, Yes, I agree with your explanation of what “being priced correctly” means, but there is no way to know that until both the April and Oct issues mature in 2028 and then you can compare what the total return would have been if you had bought the April issue on secondary market versus October issue at auction on the same day. If the returns are essentially the same, then we can say the Oct issue was priced correctly. In that case, it would support the hypothesis that it doesn’t really matter if you buy on the secondary market or at auction – there was no advantage either way. But even then, it’s not exactly an apples-to-apples comparison since you are comparing returns over slightly different time periods.

So is there a similar pattern among the 10y TIPS with their original issues in January and July? It seems like there might be since those auctions fall within the same seasonality windows albeit closer to to other ends of the windows.

Yes, a minor effect. That is what I saw when I posted that Michael Ashton article. But it isn’t always consistent. Right now Jan 2033 is at 2.535% and July is at 2.493%. That’s just 4 basis points. If you look at 2032, Jan is at 2.527% and June is 2.485%, also 4 basis points.

Knowing this fact, will the Dec. reopening auction behave in a similar manner?

That’s a good question. When we look at the December reopening we will be predicting based on the current market yield of this new TIPS, 91282CJH5. The seasonal factors don’t change because you are still looking at the final inflation accrual months of July and August. But in December, non-seasonal inflation hits the lowest point of the year, which could give that December auction a slight boost in yield to compensate for the hit coming in 2 months.

More evidence that these investments are too complicated for a lot of people without considerable financial aptitude. Unless losing a few points doesn’t make that much difference to you.

Sharing my thoughts which I am STRIVING to FOLLOW in practice:

It is NATURE of MIND that whenever we BUY something, that we WANT the BEST PRICE and an ongoing comparison to PAST and FUTURE price to ascertain we GOT the BEST.

if we got it, however small the ODDS of nailing BEST price ever for a moving target, we are happy. if price changes against us, we are disappointed.

This NATURE of MIND is not limited to BUYING TIPS – it is also for buying potatoes, groceries, general merchandise, clothes, cars, houses, airplanes etc.

So whether one is a billionaire, a millionaire or just has a few 100’s for BUYING, this NATURE of MIND / MINDSET to get BEST PRICES can make one miserable as the ODDS are low.

Mind is just a bundle of thoughts. Best to shake off the mindset by GET/FORGET approach, BUY and HOLD commitment, replacing thoughts that make one miserable with thoughts of CONTENTMENT, etc. This way, we can TRAIN the MIND to BE HAPPY / a change of mindset.

As far as investment options go, money market funds are the ONLY VEHICLE that assure STABLE VALUE while giving yields close to 5%. I-Bonds also offer PRINCIPAL protection. Savings accounts do and one can shop around for best rates but once we open account, we will always find someone else giving something better. Life in this day and age is like that! Constantly agitating mind (bundle of thoughts) so business can CAPITALIZE on the agitations with newer and newer SOLUTIONS whereas we can personally do better just by letting go the mindset that is not serving us well!

+1 for content -.25 for capitalization 🙂

I am (practicing)CONTENT(ment) with whatever I get +1 and -.25 🙂 – TIPS numbers too 🙂

+1

YES. YES. that’s exactly why I have to PRACTICE CONTENTMENT besides INVESTMENT.

let me explain.

The strange thing is when the SENSES come in contact with the +1 mind is HAPPY. For -0.25 MIND has to THINK about it whether to CHOOSE TO REMAIN HAPPY or not. hence CONTENTMENT practice is crucial to BE HAPPY no matter what.

This is no different from the TIPS price and REAL YIELD fluctuations in a yo yo market – if it goes in my favor, I am HAPPY. If it does not, then I have to begin the CONTENTMENT practice techniques again…….and again……until I AM PERFECTLY CONTENT no matter what. Then i can say I am a successful investor who is HAPPY come what may 🙂 Afterall, LIFE IS SHORT – no denying that! better to be a HAPPY INVESTOR than let DISCONTENT spoil the mind’s happiness!

Reminder to myself: TIPS offer PRINCIPAL PROTECTION, INFLATION PROTECTION and a decent coupon rate as a BONUS. Sounds good! 2 times to look at a TIPS holding – TAX TIME and upon maturity 🙂

I agree. Maybe you can get a jacket for 50% off, but if you had waited it might be 75% off. On the other hand, it might be sold to someone else.

Boston used to have a store called Filene’s Basement which would mark down surplus clothes by 25% a week. If it went to 0% it would be donated to charity. The game was whether to buy now or wait another week. It sounds like your kind of store.

This TIPS issuance, which a small amount is now sitting in my account, has a coupon rate of 2.375%. That’s good, isn’t it?

Dear Robt, Coupon of 2.375 is VERY GOOD by historical standards which numbers David has shared in prior blog posts. You get 2.375% coupon payments (interest) I believe biannually on your principal and ON TOP OF THAT, inflation adjustments too.

I am new to TIPS too….I learnt what I did from the TIPS GURU David. Learning new things is easy if we put a little effort. Its just the mindset I talked about that complicates life – so I am working on the mindset now that I have the TIPS in hand 🙂

H – I am not that new to TIPS but I don’t feel any closer to understanding them as far as what makes a good coupon rate or not. And forget about real yield.

I can wrap my head around I Bonds for the most part and treasuries.

Yeah, pretty much. I wouldn’t even have participated in a couple of 5 year TIPS auctions if not for some of the details including historical provided here. As to the nuances of small pricing differences – my brain hurts! But I appreciate the explanations. This may be it for me – already filled my intermediate bond allocation in tax deferred accounts.

Unless of course we get another historically high set of upcoming auctions next year, ha ha.

Bingo! What a relief

In a way, this seems similar to a 2-year CD to currently be paying 5.35% compared to an 18-month CD currently paying 5.4%, since the experts seem to be expecting interest rates to be decreasing at the tail end of the CD term.

If it’s any consolation, the 5 yr TIPS yield on Bloomberg this AM is 2.38%

And gold is lifting off…

I think, though, that Bloomberg immediately switches to the real yield of the most recent 5-year TIPS, which is now 91282CJH5. Vanguard shows the April 2028 5-year trading at 2.506% for a large order, 2.477% for a small lot.

Good god!