By David Enna, Tipswatch.com

Back on Oct. 8 I posted an article, “The I Bond’s fixed rate will rise. But by how much?” attempting to forecast the potential new fixed rate for the U.S. Series I Savings Bond, which will be reset by the Treasury on Nov. 1.

At the time, I noted one month of data remained — meaning through the end of October — and I warned that things change quickly in the financial markets. And of course, things did change, with the 10-year real yield initially falling from 2.47% on Oct. 6 to 2.29% a week later, before settling back to 2.44% at the market close on Oct. 26.

So here are my current projections, based on real yield data through October 26:

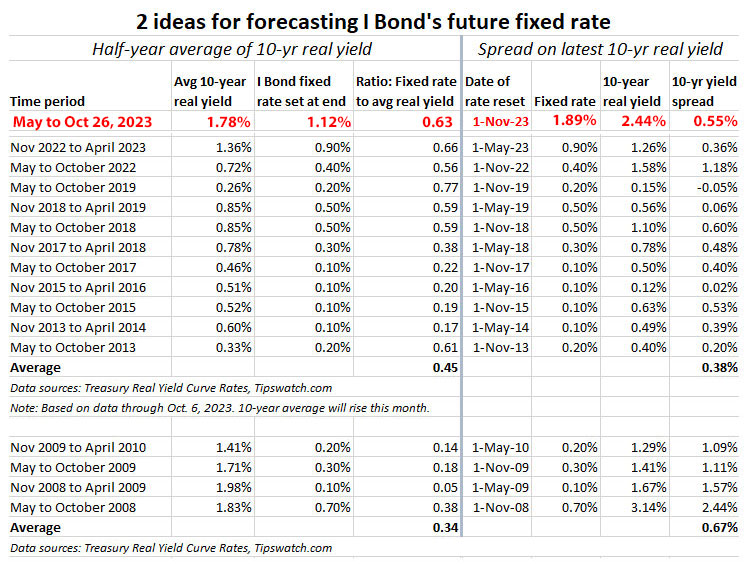

Half-year average: On the left is the projection using the half-year average 10-year real yield, which through Oct. 26 is 1.78%. This is the number I predicted in my earlier projection .

In the last five rate resets, the average ratio of fixed-rate to real yield has been 0.63. If you apply that to the 1.78% half-year average, you end up with a projection of 1.12% for the November 1 rate reset. Because the Treasury sets the fixed rate only to one decimal point, that could result in a fixed rate of 1.1% or 1.2%, above the current rate of 0.9%.

Latest 10-year real yield spread: The current real yield for a 10-year TIPS is 2.44%, much higher than the half-year average of 1.78%. This is because yields have surged nearly 50 basis points higher in the last two months.

In recent years, the typical spread between the fixed rate and the 10-year real yield has been in the range of 50 to 60 basis points. I used 55 basis points in this example. The result is a projection of 1.9% for the November 1 rate reset.

Conclusion

I believe the half-year real yield predictor (which is pointing toward a fixed rate of 1.1% to 1.2%) is a more reliable forecast. However, a fixed rate that low would be a massive 120+ basis points below the real yield of a 10-year TIPS, which would make I Bonds much less desirable in comparison.

So, if the Treasury sees this yawning gap, it should be willing to set the I Bond’s fixed rate a bit higher. Or not. Who knows?

I think right now we are heading toward a fixed rate in the range of 1.1% to 1.4%. That’s based partly on data, partly on “gut feeling.” Or possibly “wishful thinking”?

If the fixed rate ends up being 1.2%, the new composite rate will be 5.16%, below the nominal yield of a 1-year Treasury bill at 5.39%. This is a problem for short-term investors, which I addressed in my recent article, “Are U.S. Series I Savings Bonds losing their appeal?“.

What comes next

The last day you can buy an I Bond with a 0.9% fixed rate will be Monday, Oct. 30, because TreasuryDirect requires that purchases be made with one business day remaining to clear. Purchases on Tuesday, Oct. 31, are likely to be shifted to the new fixed rate (unknown) and new variable rate (3.94%).

So it is possible that the Treasury will announce the new fixed rate on the morning of Tuesday, Oct. 31. This early release is what it did at the May 1 reset and I think it is a good idea. Buyers should understand what they are purchasing.

By the way, standard practice for I Bond investors is to buy close to the end of the month because a purchase on any day of the month gets a full first month of interest. So there is no need to jump quickly into the new I Bond, no matter what the fixed rate is.

• I Bonds: A not-so-simple buying guide for 2023

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

What’s your prediction for fixed rate reset on May 1st?

Still looks like 1.2% or 1.3%, but things can change. Read this: https://tipswatch.com/2024/02/26/lets-check-in-on-the-i-bonds-next-fixed-rate/

I-bonds offer a deflation bonus. TIPS offer deflation protection because during periods of deflation TIPS don’t lose purchasing power while I-bonds gain purchasing power

Yup 1.3%

The new fixed rate just got released. 1.3%, 5.27% combined rate.

https://treasurydirect.gov/savings-bonds/i-bonds/

1.30

Thanks! Not very exciting to me, may buy more TIPS instead. Or some longer treasuries if the rates continue to rise.

Fixed is 1.3%

We had an upside surprised last time (prediction of 0.60 with the Treasury setting it at 0.90.) Lets hope it happens again.

I am considering selling some of 0% fixed I Bonds Nov 1st and buying back Nov 25th. Not very liquid right now, considering doing this to $10-$20k. What are your thoughts? And is anyone else doing this?

IMO fixed rate will be 1.3%-1.5% with upper end 1.5% very likely. With 10Y TIPs >2.45% and average 6month ~1.75% this seems likely.

Reminder: If you’ve already purchased I-bonds in 2023, you’re already into your maximum tax year allocation. If not, you’re free and clear to do the “swap.” Yes, many of us are doing what you’re considering.

Yes, I haven’t bought for 2023 yet. Was waiting for higher fixed rate..

Wise move

David, I’ve never cashed out from an I-bond purchase but plan to do so soon. If I want to cash out on the first of the month (to optimize the redemption), do I do it right on the first day of the month, or a day or two before?

You need to wait at least until the first day of the month, because that is when the previous month of interest is credited.

Thank you for responding. I thought there might be a settlement delay, just as Treasury Direct allows purchases of the current “on-the-run” I-bonds only until the penultimate day of October.

That’s not exactly right. There’s a two business day lag from redemption request to payment processing. TD will show you the interest earned for the first of the month upon redemption request if it takes place a day or two beforehand. Weekends and holidays cause an even greater lag in days. Here’s an example from my own experience.

I intended to cash out an I Bond to receive the money on 9/2. I initiated the redemption on 8/31 (with 9/1 interest included) and the confirmation indicated I would receive the funds on 9/5 (which was two business days later because of the weekend and Labor Day). It just so happens my bank credited the balance as “pending” on 9/2 (two days later), which not all banks do, but the pending designation lifted on 9/5 as indicated.

This may be a self-fulfilling prophecy? If I were on the committee at TD responsible for setting new I Bond rates, the first thing I would do would be to check what fixed rate investors are expecting.

“That David Enna guy is saying we’re only going to offer 1.1%. Let’s go with that!”

Nah, tell them I said 1.4%!

What is the rationale for excluding the periods with 0.00% fixed rates?

While I dont think the rate will go that low at the next reset, it seems flawed to exclude those periods from the analysis.

The 0.0% resets often came at times of negative real yields for the 10-year TIPS. Since the fixed rate can’t go below 0.0%, the spread gets totally skewed. Such as on Nov. 1 2021: fixed rate of 0.0%, real yield of -0.92%. So I only look at times when the Treasury set a rate of 0.1% or above, which would mean real yields were high enough to justify the positive fixed rate.

In essence, when the Treasury sets a 0.0% fixed rate, we don’t know how low it could have gone using the usual Treasury rate-setting techniques — it cannot go below 0.0%.

How ironic is it that the annual purchase limit for inflation bonds (I-Bonds) is not adjusted for inflation?

I nominate Roger’s reply for the best comment ever posted on this site. 👏

I second that motion.

401k, catch up, tax brackets, ss cola, etc, etc, all increase every year. Why is IBonds stagnated at 10k???

Making the Ibond difficult to purchase in excess does trim the future risk to the treasury a little. The purchase limit could be a protective measure. Not stating a specific method by which the fixed rate is set is also a protective measure. Stating that the program can close at any time is also a protective measure.

especially since the limit used to be 30,000 annually.

Considering treasury’s funding needs, my guess is that the fixed rate would be higher than 1.1%. At 1.1%, it’s not going to attract any investors

As I have noted, I Bonds are not a significant source of funding for the Treasury. The $10,000 purchase cap equals small total investments.

It seems to me that we are in a real rate period similar to 2006/2007 when the iBond fixed rate was 1.4%. As real rates increase, the value of the Put that comes with the iBond decreases. The result should be less drag on the fixed rate.

Perhaps David can make contact with a quant friend to provide some analysis on the value of that Put which allows the iBond holder to sell back the iBond at Par. This protection from increases in market real rates has some quantifiable value.

I thought I-Bonds were not transferable in that fashion…

The Put feature I’m referring to is the ability to redeem the iBond after one year at face value (less 3 months of interest) or after 5 years at face value with full accrued interest. Much different than TIPS which fluctuate in value based on market rates.

There was a post over on the bogleheads i bonds mega thread earlier in the week.

https://www.bogleheads.org/forum/viewtopic.php?p=7518290#p7518290

Using very similar methodology to yours he/she predicted a 1.3% fixed rate.

Thanks for your prediction. Unfortunately, unless the treasury throws us a curve ball, you’re going to be right with your range.

1.3% looks like a good projection

Excellent original analysis and helpful prediction update a few days out from the official announcement. It’s always helpful to have an idea of what to expect from one’s investments in advance of purchase.

A range of 1.1% to 1.9% for the I Bond Fixed Rate, with the lower end of the range being more likely, will make this the highest I Bond Fixed Rate since November 2007. If the rate ends up in the middle of the range, it would be the highest since November 2002. From that historical perspective, it will be a great time to buy the next I Bond as an investment for anyone looking to hold it for more than one year and certainly for five years, based on the treasury equivalents.

The ideal strategy, in my view, is to have that $10K in a 13-Week, 17-Week or 26-Week T-Bill earning 5.5% and maturing sometime before mid-April with those funds available to purchase the next I Bond then.

Excellent analysis, thanks

On “goodwill gesture” and “good deal for the treasury”

I accept both of these and I have both electronic and paper I Bonds, but I am growing more concerned due to the treasurydirect approach to cashing of paper HH Bonds which are still in their interest earning period.

From Treasurydirect “Cashing a Series HH savings bond where you are named on the bond and you send it in requires at least 3 months of processing time.”

How is this acceptable and is it “goodwill”?

Cannot blame the public for having a short term mindset.

FYI, Treasury has very recently improved processing times.

I recently did a conversion of over 91 bonds needing 2 manifests. It took less than 2 week after they were received at treasury, so things are definitely improving.

You can view it for yourself at treasury direct but here are the new processing times.

The following transactions require at least 4 weeks of processing time and also require that the bonds and/or TreasuryDirect accounts are in your name.

— Cashing paper Series EE or paper Series I savings bonds where you are named on the bonds and you send in the bonds with your request

— Unlocking your TreasuryDirect account or updating your banking information within that account

— Converting your paper savings bonds into electronic format (in a TreasuryDirect account)

I apologize, I missed the HH part, still 3 months.

Can we add or change a bank account now without paperwork and a Medallion stamp?

I think the rules have changed because few banks will do the Medallion stamp: https://treasurydirect.gov/research-center/signature-certification/

The form for changing a bank account still says: “Notary certification is not acceptable.”

Click to access sec5512.pdf

[video src="https://treasurydirect.gov/videos/tools/how-to-add-a-new-bank-account/how-to-add-a-new-bank-account.mp4" /]

Txs, now what were those security words I never used.

How do you plan for your heirs to cash on the paper bonds. Sounds like an estate nightmare.

It’s probably wise to deposit the paper I Bonds at TreasuryDirect, with updated registrations. (I haven’t done this yet, but my mother-in-law did. Tedious, but it worked.)

I don’t know if this is right or wrong, but I started I bonds years ago with the intention of setting aside some money for later on. I’m retired on Social Security and I purchase one $250 each month on the fifteenth. I’ve always looked at I bonds like a 5 year CD, just set it and forget it.

Seems to me this is a great strategy

David: It seems to me that there are at least three issues you are not taking into account.

First, will Treasury be guided by past and current real rates or instead by their expectations as to future real rates?

Second, does Treasury “need” the money that comes in from I-Bonds and consider them to be a valuable source of funds or are I-Bonds just a legacy program that is tolerated because it could not be terminated without Congressional criticism?

Third, does Treasury consider that I-Bonds have been abused by short-term traders, so that they would prefer a low real rate to squelch that perceived abuse?

I don’t know the answer to any of these questions, but I would not be surprised by the announcement of a real rate that is lower than your forecast.

This posting was an update to the longer original explanation of the forecast so I didn’t intend to go into great detail.

1) I do think the Treasury at least “considers” future trends in real yields and that would justify a fixed rate in the 1.4% range, or even higher. But it might not be the key factor.

2) I Bonds aren’t a significant source of incoming cash for the Treasury. Savings Bonds are a goodwill gesture for average Americans, plus an incentive to save. But I think they are important to the Treasury for those reasons.

3) The short-term traders are redeeming and they probably won’t be coming back to I Bonds in this current era of high short-term nominal rates. The benefit to the Treasury was a massive surge in public awareness of I Bonds.

I Bonds are a pretty good deal for the Treasury. They get a potentially long-term investment at below-market real yields, with no outflow until redemption. Payouts before five years get an interest-rate penalty. So the fixed rate should be set fairly, and I think it will be.