TIPS principal balances will fall 0.2% in January, based on non-seasonally adjusted inflation.

By David Enna, Tipswatch.com

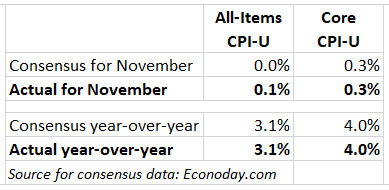

Costs of shelter continued rising in November, offsetting declines in gas prices, resulting in seasonally-adjusted all-items inflation of 0.1% for the month, the Bureau of Labor Statistics reported today.

The all-items number came in above expectations of 0.0%, but annual inflation of 3.1% matched the consensus. Core inflation, which removes food and energy, rose 0.3% in November and 4.0% for the year, matching expectations.

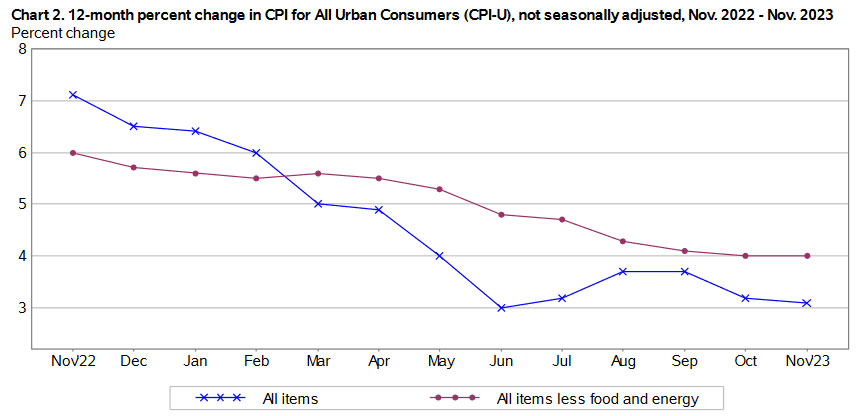

On the positive side, annual U.S. inflation dropped a notch to 3.1% for the year ending in November, down from 3.2% in October. That is the lowest annual inflation rate since June.

The BLS noted that the shelter index increased 0.4% in November, after rising 0.3% in October, and was the largest factor (about 70%) in the increase in core inflation. Shelter costs are up 6.5% year-over-year. This news is likely to set off protests that CPI shelter is a lagging indicator and doesn’t reflect current conditions. But … it is what it is. More from the report:

- Food at home costs were up 0.1% for the month and 1.7% year-over year. U.S. consumers can appreciate these moderate numbers.

- Gasoline prices fell 6.0% in November and are now down 8.9% year-over-year.

- Costs of used cars and trucks increased 1.6% but are down 3.8% over the year.

- Costs of new vehicles fell 0.1%.

- Apparel costs fell 1.3%.

- The medical care index rose 0.6% in November.

- Costs of motor vehicle insurance rose 1.1% for the month and are up a shocking 19.2% year-over-year. (Be prepared when you get your next bill.)

Overall, I’d say this November inflation report came in about on target, with shelter costs again being the “suspicious” factor pushing inflation higher. Over the next 12 months, this trend is likely to reverse. The trend over the last year has been gradually-moderating inflation, but with core locking in at 4.0% with shelter as the major factor:

What this means for TIPS and I Bonds

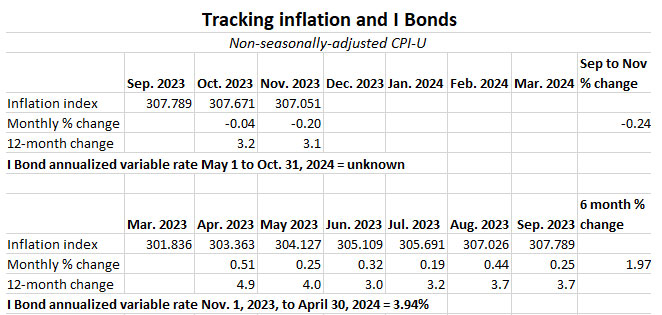

Investors in Treasury Inflation-Protected Securities and U.S. Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances on TIPS and set future interest rates for I Bonds. For November, the BLS set the inflation index at 307.051, a decrease of 0.20% from the October number.

Remember that non-adjusted inflation tends to lag the official number toward the end of the year because of holiday-season discounting. So this deflationary number wasn’t a surprise, and you can expect to see another one for December before things turn around in January.

For TIPS. The November inflation index means that principal balances for all TIPS will decline 0.20% in January, after falling 0.04% in December. Here are the new January Inflation Indexes for all TIPS.

For I Bonds. The November inflation report is the second of a six-month string that will set the I Bond’s new variable rate, to be reset on May 1. So far, with four months to go, inflation has fallen 0.24% for this period. It’s too early to make any judgement about the new variable rate. We saw a similar pattern in November to December in 2022, but then non-seasonally adjusted inflation leaped higher in January 2023.

Here are the numbers so far:

What this means for future interest rates

Although all-items inflation came in slightly higher than expectations in November, I don’t believe this will have any real effect on the Federal Reserve’s thinking on interest rates. The Fed is highly likely to continue, for now, to hold short-term interest rates in the current range of 5.25% to 5.50%.

In fact, I’d guess these current inflation numbers won’t play a deciding role in the Fed’s interest-rate decisions. More likely, the Fed will be watching employment trends. If the job market begins to sour, the Fed will begin lowering the federal funds rate.

From this morning’s Wall Street Journal report:

The Fed is on track to hold rates steady at its meeting Tuesday and Wednesday, and the latest inflation data won’t change that path. The latest reading is probably a bit firmer than the Fed would like to see to be confident that inflation is moving back quickly to its 2% goal, but it is unlikely to alter the Fed’s near-term policy stance because inflation has improved markedly this year.

Both the stock and bond markets seem confident that the Fed will begin easing next year, possibly by spring. That isn’t the message the Fed intends to send, but it could be true. The path forward, in my opinion, is going to be “choppy.”

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I am trying to understand the potential losses in buying TIPS on the secondary market. We bought 10,000 shares of 912828ZJ2 at a price of 95.8387 for a total of 11,418.60. Are we guaranteed just the 10K back? Is the 1418.60 at risk if there is deflation? or disinflation? When you say the value of TIPS went down 2% does that mean the total value of 11,418.6 went down by .002? We are buy and hold, so if it matured today, would we get back 11,418.6 x .9998? Thank you so much for your help.

Pamela, the inflation accruals of all TIPS will go down 0.20% in January — NOT 2.0% — because November was a deflationary month in non-seasonally adjusted inflation. When you buy $10,000 par of a TIPS you are guaranteed to get back AT LEAST $10,000 at maturity. It doesn’t matter how much you paid, just the par value is guaranteed against deflation. However, the risk of long-term deflation is extremely slight.

What you paid is not the principal balance. The principal balance is par value x inflation index. The inflation index of that TIPS is 1.19140 as of Dec. 14, so the principal amount is $10,000 x 1.19140 = $11,914 as of today. If it matured today (it won’t) that is how much you would get, plus one more coupon payment.

In fact, if the CPI-U stays where it is now, after falling for two months, the variable rate next May would actually be zero for ibonds. So yes, could make a lot of sense to buy before next May.

It’s likely we will see some turnaround in the January to March period, but December’s non-seasonal is also likely to be negative. I would guess the I Bond’s variable rate will drop below the current 3.94%, possibly a number as low as 1.5%. Just a guess.

You said that inflation rose by .1% in November. Is that on an annual basis, because the metric that ibonds use, which is the CPI-U fell for the month of November?

Official all-items inflation is based on *seasonally-adjusted* prices. The TIPS inflation accruals and I Bond future interest rates are based on *non-seasonally-adjusted* prices. Official inflation was up 0.1%, but non-seasonally adjusted was -0.20% for November. Over a one year period, the two numbers balance out.

I’m now glad I have waited to buy my 2023 I-bond allotment. Looks like I will get the 2023 $10K now and then most likely another round before April of 2024. It’s been a long time since I-bonds paid anything above inflation.

Despite what happened a year ago and the impossibility of predicting the future, it’s looking like a lower inflation rate for the next I bond is a likely outcome. This will make the purchase of the current I bond in 2024 before May 1st a more difficult decision despite the high fixed rate because the composite rate could indeed be lower than comparable prevailing rates in the treasury markets over the ensuing 12 month period. Then again, locking in 1.3% above inflation over as many years as one would like could prove to be too attractive to ignore.

Yes, if the investor is viewing an I Bond as a short-term investment, it probably won’t be attractive. But the comparable T-bills are all short-term investments and there is no guarantee what the future return will be. An I Bond with a fixed rate of 1.3% or higher is going to outperform inflation by 1.3% or more for up to 30 years.

You said that the principle balance on tips dropped .2 and .04%. What does that mean for me as a buy and hold investor? If I paid 11400 for 10,000 worth of principle on the secondary market. Would I lose .24 % of that 1400 at maturity (if maturity were January for example). I believe the 10,000 is protected but the 1400 is vulnerable? Thank you

What you paid for the TIPS may not be the principal balance. But if your principal balance was $11,400 and inflation fell 0.2%, then in two months the principal balance would fall by 0.2%. If you are a long-term holder, this is fairly meaningless. If a TIPS is maturing in January (I own one that is), you will lose a little of the accumulated principal.