For some investors, cashing in low-fixed-rate I Bonds makes sense, combined with the gift-box strategy to add to holdings in October.

By David Enna, Tipswatch.com

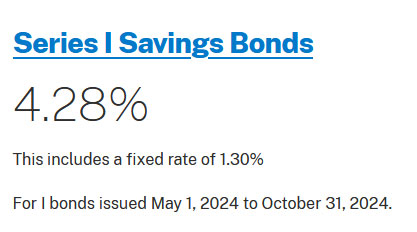

We are just a month and a few days away from the November 1 rate reset for the U.S. Series I Savings Bond, when both the 1.3% fixed rate and 2.96% variable rate are likely to fall.

Investors purchasing I Bonds in the months of September or October can lock in the 1.3% fixed rate for its potential 30-year term, plus capture a full six months of the 2.96% variable rate (creating a composite rate of 4.28% for six months). The new composite rate as of November will likely be about 3.1%, or less.

So purchasing I Bonds in September or October looks appealing, but the problem for many investors is the purchase cap of $10,000 per person per year. Most people interested in I Bonds have already purchased them to the limit in 2024. However, there are ways to get around the limit — such as adding to holdings through the gift-box strategy, trusts, or business-owner strategies.

In this article I am going to look at using the gift-box strategy, combined with a “rollover” redemption of low-fixed-rate I Bonds to purchase more of the 1.3% fixed rate, the highest for I Bonds since May 2007. This won’t be for everyone, but I get a lot of feedback from readers who are plotting this course.

The rollover strategy

OK, this seems simple: Redeem some or all of your I Bonds with very low fixed rates (0.0% to 0.2%, for example) and then use that money in October to purchase new sets of $10,000, either as your first purchase of the year or using the gift-box strategy. But it is not quite that simple.

Be careful redeeming in TreasuryDirect.

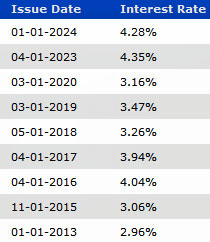

When you go to redeem I Bonds, TreasuryDirect will present a page of all your holdings, showing the current interest rate and current value (minus the 3-month interest penalty, if the I Bond hasn’t been held for 5 years).

TreasuryDirect shows you the current interest rate, but not the fixed rate for each issue. Look at the wide variety of interest rates in my example. Which ones have the lowest fixed rates, making them targets for redemptions?

This isn’t easy. For example, the I Bond issued in January 2013 obviously has a fixed rate of 0.0%, because its interest rate matches the current variable rate of 2.96%.

But what about the I Bond issued in April 2017, with an much better interest rate of 3.94%? It must have a higher fixed rate, right? No. It has a fixed rate of 0.0% but is still paying the previous variable rate of 3.94%, which will transition to 2.96% on October 1. So this I Bond is a potential target for redemption.

In this list, the best targets for redemption are: March 2020, with a fixed rate of 0.20%; April 2017, with a fixed rate of 0.0%, November 2015, with a fixed rate of 0.10%, and January 2013, with a fixed rate of 0.0%.

Also consider federal taxes.

When you redeem an I Bond, you will owe federal income taxes on the interest earned. If an investor purchased $10,000 each of those four I Bonds, here would be the tax consequences of full redemptions on October 1:

- March 2020: Proceeds of $12,136 after the 3-month interest penalty. Taxable income of $2,136.

- April 2017: Proceeds of $12,932. Taxable income of $2,932.

- November 2015: Proceeds of $13,308. Taxable income of $3,308.

- January 2013: Proceeds of $13,624. Taxable income of $3,624.

Any of these redemptions would incur potential federal taxes of $450 to $700 or more, depending on your tax bracket. That’s a factor to consider. However, you may have useful ways to use the net cash, which softens the blow.

When to redeem?

With I Bonds, you want to redeem close to the first day of the month, because I Bonds do not earn interest for the month they are sold. So that means if you are planning to use this rollover strategy, you should place your redemption order on Tuesday, Oct. 1.

TreasuryDirect does not allow you to schedule redemptions, so you will need to do this manually. Also, when you get to the final redemption screen, make sure your bank or brokerage is listed as the “payment destination.” Otherwise, your money could be placed in TreasuryDirect’s “zero-percent C of I.” You don’t want that.

When to purchase?

After you redeem, you should see the money deposited into your account in a few days. It’s always worked for me, anyway. Then you can plan your purchase of the 1.3% I Bonds, which you will want to make late in the month of October. Why? Because I Bonds earn interest for an entire month, no matter how late they are purchased in that month.

TreasuryDirect allows you to schedule purchases. I’d suggest setting the purchase date to Friday, Sept. 27 or Tuesday, Oct. 29, to avoid any end-of-month pitfalls. Any order on Oct. 31 will be registered as a November I Bond, with the new lower fixed rate / variable rate combination.

Using the gift-box strategy

This isn’t for everyone, because it requires a trusted partner, such as a spouse or relative. Harry Sit of the TheFinanceBuff.com was the first to write about this strategy in December 2021, in an article titled “Buy I Bonds as a Gift: What Works and What Doesn’t.” When people ask me about the gift box, I point them to this article, which was well researched and thorough. So, go read that article if you don’t know about the strategy.

Some basics of the gift box strategy:

- When you place an I Bond into the gift box, it begins earning interest in the month of purchase, just like any other I Bond, and continues earning interest just like any I Bond. However, this money is no longer yours. It belongs to the recipient of the gift.

- The purchase does not count against your purchase limit for that year. It will count against the purchase limit for the recipient, in the year it is delivered.

- Gift purchases are limited to $10,000 for each gift, but you can make multiple gift purchases of $10,000 for the same person. But the recipient can only receive one $10,000 gift a year, and that gift counts against their purchase limit for that year.

- You must provide the recipient’s name and Social Security Number when you buy a gift. The recipient doesn’t need to have a TreasuryDirect account … yet. Only a personal account can buy or receive gifts. A trust or a business can’t buy a gift or receive a gift.

- “I Bonds stored in your gift box are in limbo,” Harry Sit notes in his article. “You can’t cash them out because they’re not yours. The recipient can’t cash them out either because the bonds aren’t in their account yet.”

- The recipient will need to open a TreasuryDirect account to receive the I Bond. Once it is delivered, the money is the recipient’s, who can then cash out or continue to hold the I Bond.

Here is TreasuryDirect’s video explaining the step-by-step process to complete a gift box purchase:

In his article, Harry Sit also provides a very useful step-by-step guide to completing a gift-box purchase.

The next fixed rate

In recent years I have settled on looking at the six-month average of the 5-year TIPS real yield and then using a ratio of 0.65 to project the I Bond’s next fixed rate. So far, the average real yield from May 1 to Sept. 23, 2024, has been 1.9259%. Apply the 0.65 ratio and you get 1.2518%, which could mean the fixed rate will maintain at 1.3%.

We have one more month of data to add, and I think that calculation is going to slip to something just below 1.25%, meaning a fixed rate of 1.2%, which is still attractive.

However … a huge however … we have never tried to make this projection in a time of sharply declining real yields. As of Monday, the 5-year TIPS real yield was only 17 basis points higher than the I Bond’s 1.3% fixed rate.

So it is entirely possible the Treasury will recognize this reality, consider what’s coming, and settle on a lower fixed rate. But I think the fixed rate will remain 1.0% or higher into next year.

Final thoughts

I wasn’t a fan of the gift-box strategy when it first erupted onto the scene in 2022 to allow investors to purchase large quantities of I Bonds with very high variable rates, but also 0.0% fixed rates. That didn’t make sense because a high fixed rate is the all-important factor. But now the strategy does make sense, because the I Bond’s fixed rate is high.

The rollover strategy is optional. You don’t need to use it if you can easily afford the cash to buy new sets of gift-box I Bonds. A lot of investors are content to hold I Bonds with low fixed rates for use as a longer-term emergency fund. If you are in the accumulation phase, hold them. If not, consider the rollover, pay the taxes and enjoy the extra cash.

I used the gift-box strategy in April 2024 to buy two extra sets of I Bonds with the fixed rate of 1.3%. And I will do it again in September or October for another two sets.

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I really appreciate the blog and the knowledge on this site. I recently got married and my wife mailed in a request to treasury direct to change her last name. I was planning on us each buying each other a bond using the gift box to take advantage of this rate before the end of the month, but I don’t think the name change will be processed by then. Does anyone know if that matters and if the gift will still be processed correctly? Do I just need to wait for the name change to be processed to release the gift? All her other account information besides her last name are staying the same. Thanks again for your help!

This is a question that has never come up before, but a good one. I don’t know the answer. I believe it would be OK since the gift is tied to a Social Security number. She doesn’t even need a TD account until you deliver the gift.

At 4.28% for 6 months, why not buy 10 years treasury at 4.07% and you wont have to worry about renewing every 6 months? You can wait for maturity or sell before then? given the interest rates likely to go down, price not likely to go down further? Maybe I am missing something?

Nothing wrong with collecting 4.07% for 10 years. And that will “probably” exceed future inflation. The nice thing about I Bonds is the continuous inflation protection and the fact your principal balance can never go down.

Pingback: September inflation sets I Bond’s new variable rate at 1.90% | Treasury Inflation-Protected Securities

Pingback: Forecast: The next I Bond fixed rate should be 1.20% | Treasury Inflation-Protected Securities

Long time reader and long time appreciator of the blog and numerous comments that comes from each post. I would never had bought iBonds or recently TIPs without the wealth of knowledge provided. Thank you David!

My wife and I both have two sets of $10K iBonds that are at 0% base. One from June 2021 and one from Oct 2022. I just redeemed the ones from June 2021 for both of us. Along with principle of $10K, we each received interest of $1,852 (net after 3 month penalty of $88) as a result of the high variable rates from these iBonds. Nice!

I scheduled a $10K purchase for 10/29/24 for each of us, gifting to each other. (we both have fully bought for 2024).

I’m still debating the redemption of the Oct 2022 combined with a further gift purchase. I like the idea of securing a 1.3% base, but not so keen to have 2 years in gift boxes. Curious what others may have (are doing).

I also figure a $10K I-bond is about enough self-insurance to be able to get you buried when the time comes.

So I did some more searching around on what others had to say on the subject of the gifting of bonds and came across the “gift of future interest” a few times with no indication of a firm ruling on the matter with regard to bonds.

“A gift of a future interest cannot be excluded under the annual exclusion.” -IRS Form 709

“A future interest gift is one which the donee’s right to the use, possession, and enjoyment of the property and income from the property will not begin until some future date.” -IRS Form 709

That sounds very like the case of a bond in the gift box, which has not been delivered but also is unalterable and irrevocable by the donor.

There is still the exclusion of gifts to a spouse – in MOST cases but not all – but I would say this means proceed with extreme caution in loading up the Gift Box for anyone else.

BTW, Harry Sit did say largely the same thing in his December 2021 article cited by Mr. Enna. Except I’m not so sure that there is any ambiguity about whether ANY bond in the Gift Box is anything other than a future interest since none are ever delivered immediately. Even that 5 day holding period gets a little sticky if one adheres to the letter of the definition on “future interest.” Given that the 5 day period is to ensure the bond gift has value before it can be delivered, that bit can probably slide. But holding longer, even if delivered in the same calendar year, doesn’t appear to have any legal support that I can find.

In case anyone has an interest as I’m working through this for my own understanding:

“Except I’m not so sure that there is any ambiguity about whether ANY bond in the Gift Box is anything other than a future interest since none are ever delivered immediately.”

US Code Title 26 Subtitle B Chapter 12 seems to clear that up for me by referring to gifts made within a calendar year.

Since a bond delivered out of the Gift Box becomes a present interest gift by becoming available to the donee, I agree with Harry Sit that any gift bonds to non-spouse recipients should be made within the same calendar year as purchased. It is as a grandparent that this becomes important to me, unless I want the potential future hassle of filing Form 709 because I thought banking an excess of bonds in the Gift Box for a grandchild was a smart thing to do.

Good article. I think you may have missed one (somewhat) important consideration for anyone that really wants to maximize return, and that is calculating penalty interest for I-Bonds purchased in past 5 years.

And this is actually slightly trickier than it sounds and you need to carefully count the months to determine the actual penalty that you pay. The reason is: the rate/variable rate reported for each I-bond holding at TreasuryDirect is the current, up-to-date interest that issue is eligible for and currently “earning”. But that isn’t necessarily the penalty that you pay because you pay the prior 3 months of interest as a penalty, NOT 3 months at the current interest rate. A subtle difference, but it means the penalty can lag what is shown at TD by up to 3 months.

For people redeeming around now, I expect many will think they’re paying 3months at variable=2.96% but will actually be paying 3mo @3.94% variable. It only amounts to about 0.25% difference of the total redemption, but might be enough to cause people to wait a few months.

Specifically for redemptions in Oct 2024 –

And looking ahead, it appears the Nov 2024 variable rate will be quite low (1.8%?) and perhaps a better chance to pay the penalty and redeem recent I-bond purchases. Those with May and Nov issue dates are looking at waiting until after 2/1/2025 to redeem at only 3mo @1.8%? penalty. Other issues have to wait a few months longer.

It may be tricky to figure out exactly what the penalty is, but of course if all you need to know is how much you will receive on redemption, the value shown on TD is already net of any applicable penalty.

Yes, it would be better to take the 3-month penalty at 2.96% instead of 3.94%. But at this point you can still earn 4.5% on your withdrawn money, which could be a factor in doing the withdrawal now instead of later.

For what its worth, Harry Sit’s article contradicts Chris B”s opinion above about when the gift is subject to gift tax reporting: “Buying I Bonds as a gift counts as a completed gift in the year of the purchase (not the year of the delivery).”

I think counting it in the year of purchase certainly simplifies things, and again, once you gift that money it is no longer yours.

I was not giving an opinion, it is tax law. Harry Sit knows the financial world and the I bond world, but gift and estate tax law is a different space. If your giving a gift to an individual, it is not reportable by you until it is delivered to the individual and you not longer have control over it.

“I was not giving an opinion, it is tax law.” I’m afraid that this statement may come as a shock to all the attorneys who earn their living litigating before the Tax Court. Unless you can cite a recent decision directly on point (can you?) where the Tax Court or a district court (or, better yet, a circuit court of appeals or the Supreme Court) ruled in favor of the IRS on the gift taxation of I-Bonds, I think you are just giving an opinion, however well-considered it may be.

Chris, you stated “Under federal law, a gift is completed when the donor no longer has “dominion and control” over it.”

What puzzles me somewhat is that in the next line you switched from the perspective of the donor to that of the recipient. “In the gift box example the gift box receipient does no have dominion and control.”

As Mr. Enna has pointed out more than once, after a gift goes into the Gift Box it is no longer the property of the donor. The only remaining “control” seems to be little more than the formality of an eventual announcement. Tax law is certainly outside my expertise but, if any gift tax owed is the responsibility of the donor, wouldn’t that come into play when the gift is no longer the property of the donor?

People contemplating when to draw Social Security will often do some rough calculation, based on current figures (which may not prove to be future figures), of “the crossover point,” i.e., what age they would be when getting a higher monthly payment by delaying Social Security would surpass the total accumulated payouts from a lower benefit which started X years earlier. The same is often true for people contemplating the purchase of a life income annuity.

My wife and I have already done $10,000 gift box purchases, each, this year but normally don’t keep great bundles of cash lying around to do much more than that after other financial obligations are met. So our main way to do more would be through redemption of past I Bonds. And we certainly don’t want to invade our IRAs just to buy more I Bonds.

We hold 0%-fixed I Bonds going back to 2010. Although their fixed rate is 0, they now include a lot of accrued interest which will, of course, continue to compound at the current and future inflation-component rates applicable to all I Bonds. Therefore, it seems to me that these are not good candidates for redemption, if the sole purpose of the redemption is to obtain cash to buy new gift box purchases at the current 1.3% fixed rate, because the “crossover point” of new 1.3%-plus-future-inflation lies considerably far into the future compared to 0% plus the still-compounding accrued earnings of the past 10, 11, 12, 13 years.

The most likely candidates for redemption would seem to be more recently purchased I Bonds at 0% fixed that are at least a year old but, also being fewer than five years old, would incur forfeiture of the most recent three months of interest earnings. But those I Bonds also incorporate the higher inflation components that prevailed from November 2021 through early 2023. What to do.

Trying to calculate the pros and cons of such situations is the kind of thing that makes me feel that my head is going to explode, so we may just give up the idea of more gift box purchases in October and “let sleeping dogs lie.” 🙂

This is a legitimate issue for people who have already sold off their more recent 0.0% I Bonds, which had moderate interest gains after a period of high inflation. When you go back 10 years or more, the accrued principal can be up 30% or more. Do you want to pay taxes on that accrual, or just let it continue to grow?

You definitely don’t want to withdraw money from any IRA to buy I Bonds, because traditional IRA withdrawals will be taxable, and Roth accounts are already totally tax-free, so keep the money there.

This goes back to my traditional advice: “Hold your I Bonds until you need the money.” But when you need the money, redeem and pay the tax. You don’t need to hold I Bonds forever.

With regard to redeeming older I Bonds with a lot of accrued interest, consider that you can redeem less than the full position in a particular bond. The redeemed portion (say $10,000) all gets reinvested in the new, higher fixed rate bond. The remainder (say $5,621.17, to pull a number out of the air) all stays where it is, continuing to compound. You’re not losing the compounding on any part of it; just arranging to have part of it compound at a higher rate.

So unless you are thinking about redeeming within 5 years from now (in which case you need to factor in the 3-month interest penalty at some unknown future rate), it seems to me that these older bonds are fine candidates for rolling forward into new higher fixed rate gift box Bonds.

You can come back later and roll the remainder forward. I already used $10,000 each from a pair of 0% bonds to fund my regular 2024 purchases. I am left with something like $1,400 of the 0% bonds in each account, which I am now thinking about redeeming to cover part of the cost of new 1.3% gift bonds, at which point the full value of the older bonds, including accrued interest (but less a 3-month penalty in my case) will all have been rolled forward and be compounding at a higher rate.

Good point. In the past, I have just sold the entire amount, but this time I may go with your idea, just pull out $10,000 and pay a smaller amount of tax. But I wonder if it will cause me a record-keeping nightmare,. In our family, a new car (ours are 13 and 8 years old) is looming in the immediate future, so I may just want to pull down the extra cash.

I’d like to push back against the first part of your statement quoted below:

“I wasn’t a fan of the gift-box strategy when it first erupted onto the scene in 2022 to allow investors to purchase large quantities of I Bonds with very high variable rates, but also 0.0% fixed rates. That didn’t make sense because a high fixed rate is the all-important factor. But now the strategy does make sense, because the I Bond’s fixed rate is high.”

I think it’s more accurate to describe it this way:

“The gift box strategy is useful when the fixed rate is high for LONG-TERM I Bond investors (like now), and the gift box strategy is also useful when the variable (inflation) rate is high for SHORT-TERM investors (like in 2021).

It may also be useful for other reasons too, but anyone who used the gift box strategy back in May 2021 as a SHORT-TERM investment received four six-month annualized variable rates of 3.54%, 7.12%, 9.62%, 6.48%. During the first 12 of that 24 month cycle, interest rates were essentially 0% until the Fed started tightening in 2022, far exceeding any fixed rate investment back then. They were still comparatively higher for the second twelve month period as well. And when rates dropped for three months in the subsequent cycles, you could redeem those bonds with a much lower interest rate penalty and still come out way ahead.

Marce, this is a great point. I am always a long-term investor in I Bonds, but my main objection to using the gift-box strategy as a short-term strategy when the fixed rate is 0.0% came when readers told me they were loading up on 10x the purchase limit, which would require distributions over 10 years, all at 0.0% fixed rates. … That kind of overload didn’t make sense.

I can agree with that. But the gift box strategy for short-term investors doesn’t really mean loading up on 10x the purchase limit for a single investor to be delivered over a ten year period (although I’m sure there were a few exceptions). You wouldn’t go out that many years anyway if you’re a short-term investor by definition.

If you were using the gift box strategy back then, as I was, you were doing it in tandem with a partner and buying $20K between the two of you at in 2021 and buying $20K of gifts between the two of you after the November reset, which you delivered to each other just a couple of months later. That’s $40K.

if you decided to go up to $100K, you would’ve bought $60K more of gifts between the two of you and you would only be delivering for an additional three years, not ten years. The gift box strategy was lucrative for short-term investors even without a fixed rate.

David, your updates are always so timely and of enormous help. I would not have known about the discontinuance of tax refund paper I Bonds without you! Thank you so much, you saved me lots of time and a needless overpayment.

Apologies if it has already been posted here, but in case it is helpful, the I Bond historical fixed rate and variable rate components, as well as the composite, are shown in the PDF linked on Treasury Direct under the section, “What have interest rates been For I Bonds?”: https://www.treasurydirect.gov/savings-bonds/i-bonds/i-bonds-interest-rates/

That chart (https://www.treasurydirect.gov/files/savings-bonds/i-bond-rate-chart.pdf) is a bit difficult to read, but you can enlarge the pdf. On my “Q&A on I Bonds” page I do list all the historical variable rates and fixed rates.

Regarding the income tax effects of redeeming I Bonds: for those of us who are Social Security (SS) recipients and have low to medium income, the federal income taxes we pay on our benefits may be more than simply the product of our tax bracket rate multiplied by the dollar amount of our benefits. It has to do with the unique way in which our benefits are taxed. We may be taxed on anything from 0% to 85% of our benefits, depending on our tax filing status (single, married filing jointly, etc), the amount of the benefits and the amounts of not only our other taxed income but also our tax exempt interest (typically municipal interest) as that is included in the formula. There is a worksheet for figuring how much of our benefits are taxed in the IRS instructions for filing annual forms 1040, where we can see the interplay of these factors. The effect is that the more non-SS income we earn, the more of our benefits are taxed, so our effective federal tax rate is potentially as much as 85% higher than our federal bracket rate. Once we reach that 85% point, no more of our benefits are taxed, so at that point our effective tax rate will be the same as our bracket rate. The bottom line for us SS recipients is that before redeeming I Bonds, we should consider performing what-if tax projections to determine to what extent we will be exposing more of our benefits to tax.

Great point, Lou. The 85% taxable level kicks in at very low limits: $34,000 for an individual and $44,000 for a couple. (Only 1/2 of your Social Security benefits count toward this total.) The levels were set in 1993 and have not been raised since. Because people are actually earning interest on their savings this year, a lot more people are going to hit strike levels. My thinking is that eventually, 100% of Social Security benefits will be taxable, but the limits will be set higher and adjusted for inflation.

Thank you

Good AM Mr. Enna – Appreciate the info. Question: For Gift Box purchases for other than spouse, do they count against the givers IRS gift limit in the year placed in the gift box or against IRS gift limit in year delivered? Thanks. Learning quite a bit from your blog.

This is outside my area of expertise, but if you gift a savings bond to a non-spouse, I think it would apply to the annual gift limit for that person, which is $18,000 a year. Granting $10,000 to that person would not be a problem since the annual limit is $18,000, but then a couple questions: 1) Does the gift get reported in the year it went into the gift box, or when it is delivered? And 2) unlikely, but what if the interest earned exceeds the gift limit? In other words, does interest earned also count as the gift? It would be a cleaner transaction if the gift is recorded when it is placed in the gift box, and technically it becomes that other person’s property immediately. Need some tax experts to weigh in.

Under federal law, a gift is completed when the donor no longer has “dominion and control” over it. In the gift box example the gift box receipient does no have dominion and control. Bottom line, a gift is not reportable until it is delivered.

Chris, thank you. But then the question is: Was the gift $10,000 or $10,000 + future interest until delivery? I don’t know the answer.

For Gift tax reporting purpose, the gift is completed when it is delivered to recipient and recipient has control over it, so the gift would include the actual amount received – 10,000 plus interest. Of course its not an issue for gifts between spouses where there is unlimited gifting.

Thank you so much, David, for writing about this topic as it has been on my mind. One question I have and cannot locate an answer for: What happens if the gifter or giftee passes away while I Bonds for the giftee are still residing in the Treasury Direct gift box of the gifter?

Harry Sit included a section on this topic: https://thefinancebuff.com/buy-i-bonds-as-gift.html#htoc-unexpected-death

Question: Can I donate a 25 year old I bond and avoid paying federal income tax on the considerable accumulated interest income?

No. Treasury does not allow a savings bond to be donated directly to a charity. It has to be cashed and then you can donate the proceeds to a charity to receive a tax deduction, if you are itemizing. But you could still face a hit on Medicare surcharges. More on this: https://finance.zacks.com/can-donate-saving-bonds-charity-avoid-paying-accrued-interest-6044.html

I have written on this potential tax hit (which I also face in 2031) and my strategy is to begin redeeming the I Bonds over a five-year period. https://tipswatch.com/2024/02/04/long-time-i-bond-investors-face-a-tax-time-bomb/

Thank you for such a prompt and complete answer. Good suggestions for estate planning.