By David Enna, Tipswatch.com

Let’s all admit one thing: 2025 has been a bizarre year for the U.S. economy, inflation, government effectiveness and the certainty of economic statistics. In fact, my code word through the entire year has been “uncertainty,” so much so that some readers complained I use that word too often.

In this year:

- President Trump launched an seemingly dangerous policy of high tariffs on U.S. imports, threatening friends and foes across the world. At first, the market reacted in fear, with the S&P 500 index falling nearly 5% on April 3, the day after “liberation day.”

- But … after a few pauses and restarts, the tariff policies seem to have been accepted by the markets. The S&P 500 has had a total return of 19.2% year-to-date. Euphoria over artificial intelligence has helped overcome the fears.

- The Federal Reserve cut short-term interest rates three times in 2025, with the effective federal funds rate falling from about 4.32% in January to 3.64% this week.

- But … the Fed’s rate cuts have had almost no effect in lowering longer-term interest rates. The yield on a 20-year Treasury bond has fallen just 10 basis points since January 1. The 30-year bond is actually up, now at 4.81% versus 4.79% on January 1.

- Elon Musk breezed into Washington on a mission to cut government spending. He did cut jobs: Government payroll numbers are down about 9% this year.

- But … Despite the cuts, government outlays have increased about 6% in 2025, according to studies by the Cato Institute and Brookings Institution.

- The U.S. government shut down for 43 days because of Congress’s failure to pass budget bills or a continuing resolution. The shutdown (and continuing high deficit spending) has shaken confidence in the value of the U.S. dollar, which has fallen 10% this year.

- But … The shutdown also eliminated or delayed reporting of many crucial economic statistics, including for inflation and jobs. Which means we are now in “a fog” as we head into 2026.

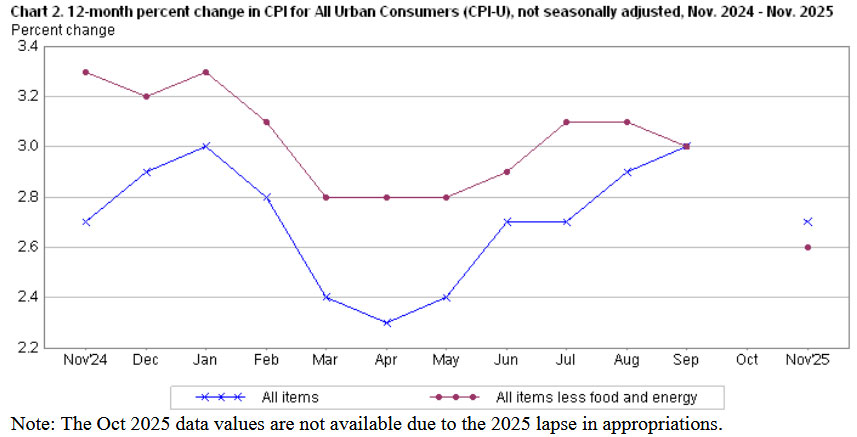

Inflation

In November 2024, annual U.S. inflation stood at 2.7% for all-items and 3.3% for core. Today — if you want to believe the November 2025 inflation report — those numbers stand at 2.7% for all-items and 2.6% for core. That looks like an improvement for core inflation, but the number is skewed by the lack of October housing data.

This one chart — unique in the history of U.S. inflation reporting — says it all:

Inflation could truly be on a declining slope, but because of the lack of data we really can’t be sure. And this problem will most likely continue, and I will again get to use the word “uncertainty.”

Clearly, this is a problem for investors in Treasury Inflation-Protected Securities and Series I Savings Bonds, which have returns tied to official U.S. inflation. As the saying goes, “The devil is in the details.” Right now, we have no details. Good luck finding the devil.

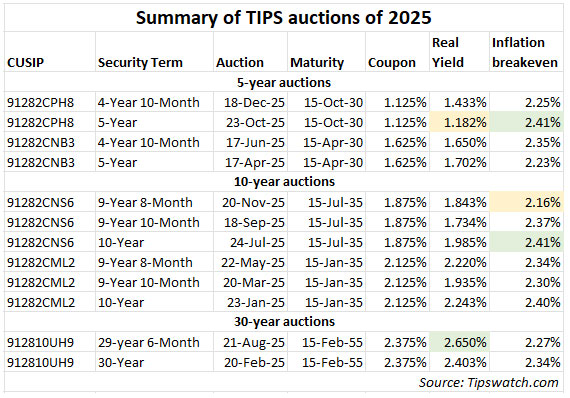

Treasury Inflation-Protected Securities

Real yields for longer-term TIPS have held up quite well throughout 2025, which is good news for people attempting to build a ladder of TIPS issues extending well into the future. You can still find real yields at 2.0% or higher — sometimes much higher — for maturities in 2040 to 2055.

Even the 10-year real yield remains attractive, now sitting at a still-appealing 1.90%, down from 2.23% on January 1.

Here is a look at the 12 TIPS auction through the year:

I have highlighted the highs and lows for the year, which don’t tell you much except that the yield curve has steepened, and that inflation expectations are higher in the short term but lower for the long term. Plus, note the big move higher for the 5-year TIPS after the October government shutdown and the resulting black hole of inflation data. TIPS yields are facing a “confidence tax.”

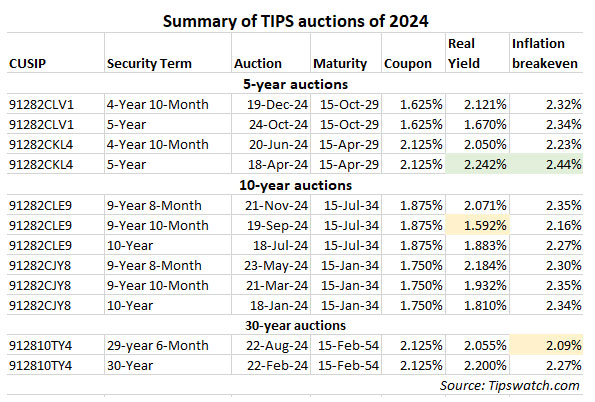

Compare that chart with the same summary for 2024:

Here is the key difference over the last year: The yield curve has steepened. In early 2024, the highest real yields were for 5-year TIPS. That trend reversed in 2025, mainly due to the Federal Reserve’s actions to lower short-term interest rates. Today, the highest auction yields are for 30-year TIPS, which I would say “is normal.”

Here is the trend line for the main TIPS categories over the last year, showing how the spread has widened for long-term versus shorter-term:

Overall, I’d say TIPS yields remain attractive, and that might be because the market doesn’t trust the inflation data coming now and into the near future. Plus, obviously, federal deficits will continue to rise. So investors are demanding higher real yields.

U.S. Series I Savings Bonds

These inflation-protected savings bonds started the year with a fixed rate of 1.2% and a six-month composite rate of 3.11%. Today, the fixed rate for new purchases has fallen to 0.9%, but the composite rate has increased to 4.03%.

Am I still a fan of I Bonds? Sure. But at this point a 5-year TIPS with a real yield of about 1.44% is definitely a competitive investment. And the 10-year TIPS is even more attractive with a real yield of 1.90%.

The problem for all inflation-adjusted investments is trust in the U.S. statistical reporting system. The government shutdown threw a wrench into the November inflation rate, and that disruption could linger unless the Bureau of Labor Statistics finds a way to make adjustments.

I will be likely to purchase a 2026 allocation of I Bonds, but definitely not before mid-April when I can see where both the variable rate and fixed rates are trending.

In summary

I am getting tons of feedback from readers who no longer trust the system. Deficits are out of control. Official inflation reports are jumbled, which is probably being kind. I have no idea where we are heading. I will admit that. The stock market could soar … or plummet. Inflation could reignite … or move toward deflation. The labor market could remain solid … or jobs will disappear.

Unless we have a deep recession, I can’t see inflation lessening dramatically in 2026. But I know that trying to predict future inflation is impossible. So all I can say is:

Have a wonderful New Year. Let’s stick together and figure this out.

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I see the 30-yr tips is losing value: https://www.eyebonds.info/tips/hist/tips102histb.html. Does it mean that there is a deflation going on?

There was one month of non-seasonally adjusted deflation. That was for November, reported mid-December, and used to adjust TIPS principal values through January, thus the decline in the value of the 30-year that you saw. Deflation in the non-seasonally adjusted CPI is not at all uncommon in October, November, and December. January through April have the worst non-seasonally adjusted inflation of the year.

I see, thank you for the explanation!

I surely don’t know what inflation will be in ’26, but I am pretty certain that we will have 12 months of surprises.

No matter any and all future turmoil, the 30-year TIPS paying 2.5% over inflation appears likely the surest bet that the cash will still be there for use in the future and most likely paying ever increasing cash quarterly payments for a long time.

Paying biannually the increasing interest dividends for a long time, I meant to say.

What will happen to inflation rates, real interest rates, and 30 year TIPS bought today if inflation accelerates, possibly into hyperinflation, due to the growing $38 trillion national debt and fiscal dominance as discussed by Janet Yellen described in this article from Fortune https://fortune.com/2026/01/05/janet-yellen-warns-38-trillion-national-debt-fiscal-dominance-eric-leeper-heather-long/ ? Is it a good idea to buy the TIPS figuring they will stay ahead of the inflation by their very definition, or will real interest rates actually rise from their relatively attractive levels now, lowering the secondary market value of the bond if sold before maturity? During inflation, will the rise in interest rates generally be only in the nominal rates, or would real rates rise too?

Assuming we got hyper-inflation (10%+) in coming years, today’s 30-year TIPS would provide a real return about 2.6% above the inflation rate, whatever it is. Hold to maturity and that would be fine. But in that scenario, I am sure you would see real yields rise as nominal yields rise, so in the short run the TIPS could lose value. All you can really compare today is a 30-year nominal bond (4.85%) versus the TIPS with a real yield of 2.6%. That nominal bond would underperform inflation by 6% or more.

David,

Enjoyed your columns for at least a decade and would like to contribute, but I don’t use Paypal or Venmo. Could I write a check to you/PO Box?

I’d like your input on some upcoming CD maturities that I want to reinvest in TIPS or maybe corporate bonds, I’m getting 4.5-5% now, but I know the Fed will be lowering rates with Trump’s thumb on the scale come May.I read your outlook for inflation and what’s real value at this time. I worked for BLS at state level and am concerned about the CPI process and lack of transparency on the last report (putting “0” in missing housing data). When we were missing employment reports we used a 10-year average for an estimate until the final data was received. So I’m skeptical about the CPI report going forward, plus Trump disbanded the non-partisan committee that gave input on BLS data.

What would be the safest investments with the highest yield going out no longer than 10 years, preferably 5-7 years.

Thanks again for your invaluable information and the effort your put into it.

BrentChandler, AZ

You state

“But in that scenario, I am sure you would see real yields rise as nominal yields rise, so in the short run the TIPS could lose value.”

I am curious if you would know what history has to say about the short term resale value of long dated inflation indexed government bonds for any country that had issued some, and then subsequently had a severe surge in inflation afterward?

I don’t follow international inflation-linked bonds, which are offered by a few countries including the UK, Spain and Australia. Canada stopped offering these bonds in 2022 and Germany cut them off in 2024. These operate under different rules and indexes, so I don’t know if they can be compared directly with TIPS.

The sad fact is government issued numbers are suspect, shutdown or not. The director of the U.S. Census Bureau and the commissioner of the Bureau of Labor Statistics are political appointees, as is the Fed chairman. I go with the flow, but I realize that government issued numbers may or may not have anything to do with reality.

Some good news (as in avoidance of bad news), my “income for being taxed by IRMAA” for 2025 is $4000 below the IRMAA cutoff. But this year I will be taxed (yes, IRMAA is a tax) about $1000 for being $700 over the cutoff based on my 2024 income. I would have been better off if I had never gotten that $700.

Pingback: Why “good news” economic numbers still don’t calm people down – Now Rundown

For me the key item for the year was the senate resolution to essentially back date several trillion dollars of debt by resolving that the original Trump tax cuts of a ten year duration were essentially meant to last to eternity. I think this completely absolves the government of any responsibility for keeping debt down or even trying to increase revenue. The same process was put forward by democrats to keep ACA premiums in check and can be used for virtually any budget category. One could postulate a similar solution for the looming Social Security crisis that we will see sometime between 2032 and 2034. Using the same logic, Social Security has always been 100% funded so we can simply continue to pay the checks out. The OBBB and elimination of debt consideration has been great for the stock market and could continue to be great for the stock market long into the future. On the other hand, I can’t see inflation getting under control under these conditions.

Nice summary. It appears more people are not trusting the inflation statistics, but David did give some comfort by saying, and forgive me if I misquote, but he basically said the BLS does have a lot of good people that have integrity and will not do anything shady. I can only have faith. Good luck to everyone and have a great 2026.

Thanks for the excellent recap and insights David. I share the concerns of many of your readers. The “full faith and credit of the U.S. government” isn’t what it used to be. If one were to view the U.S. government’s state of finances on its own merit, no sane investor would buy their bonds. However, we all know that it persists on the strength of the dollar and the perceptions of the players in the world financial system that US Treasuries are a safe haven and the U.S. is still the bastian of world financial strength.

Ray Dalio, renowned Chairman of hedge fund Bridgewater, has chronicled the downfall of major world empires and their currencies over centuries in his important book and LinkedIn article series. He has shown how the U.S. is in decline (based on many important and objective metrics), the dangers of the debt, impact on the dollar, not to mention the changing world dynamics – political, economic and social divides. As such, in the very long view, we are in uncharted territory for the U.S., but predicable in terms of what has happened to other major countries throughout history.

I have a significant amount invested in TIPs, IBonds and Treasuries. However, I am trimming that exposure due to the ever increasing risk. I believe at some time (perhaps not any time soon however), there will be some type of major financial market reset for the dollar and US debt. The most likely one, happening now, is the decline in purchasing power of the dollar and inflation. For those unfamiliar, one can view the Shadowstats website which shows the much higher true inflation rate when the 1980’s CPI computational method is used. Shadow Government Statistics – Home Page

That is why in my view, TIPS provide decent inflation protection, but depending on an individual’s personal inflation rate, they may fall short. As you know, I’ve written a series promoting TIPS investing on SeekingAlpha, which you graciously featured here some time ago.

Thanks for your continued work to help us be better investors.

Happy New Year and best wishes for a great 2026!

Happy New Year to all. I’d add some additional context to this year-end fiscal summary:

The government shutdown, aside from its partisan aspect, was actually done to call attention to a real problem — the expiration of the ACA subsidies which will double (or more) the net out of pocket cost of health insurance premiums for 22 million Americans.

Tariffs, I would argue, did cause significant inflation. We didn’t see it in the CPI numbers because it coincided with OPEC increasing oil production which offset it and lowered gas prices. I would also argue that tariffs are a regressive tax on American consumers, having a far greater impact on lower and middle class folks.

Let’s all hope for a more rational 2026.

Again, only the enhanced subsidies are expiring not the Premium Tax Credit subsidies that are part of the ACA. And when are we going to learn that subsidies cause prices to rise.

And the article misses one key stat – US GDP growth at 4.3% annual rate in the 3rd quarter.

That combined with increased tariff revenue of $195 billion along with less government spending on federal jobs (remember many of those job reductions included severance pay) and perhaps a significant reduction in the billions of dollars of fraud may result in lower deficits along with lower inflation.

Maybe a little positivity is needed instead of all the doom and gloom.

Not pessimistic, just realistic.

4.3% GDP was indeed a good number, the highest in two years since the 3td quarter of 2013 when it was 4.9%.

And the tariffs have indeed brought in substantial revenue, albeit regressively on the backs of lower and middle class Americans and not paid for by foreign countries as we were told they would be.

unfortunately, even with that revenue and high GDP, the debt still ballooned this year

“In 2025, the U.S. gross national debt increased by approximately $2.23 trillion, reaching a total of $38.40 trillion by early December. “

To fix that, we are going to need to raise taxes, continue to grow the economy, and cut spending a lot more. In other words, it’s highly unlikely.

Right or wrong, the ACA subsidies were needed because the Supreme Court struck down the tax penalty for people with no insurance at all. Who were those voluntarily uninsured people? Most likely the most healthy people. So the remaining people — the ones without jobs that included health insurance — where much more risky for insurers. The ACA requires insurers to ignore existing conditions. This current system is highly inefficient. So you could say I agree with Trump on that point. But the solution is to provide Medicare-like insurance for everyone in massive group plans, ignoring existing conditions. Can that ever happen?

Typo – 2023, not 2013

Tariffs and tax policies have been so successful that The debt has risen from 36.2T (on may one) to 38.4T.

I think it’s entirely possible that the real yield on 5-year TIPS climbs thru the winter and early spring to the point where we see > 0.9% fixed rate on I Bonds in May. Right now the “magic formula” produces 0.889417 which rounds to 0.9… still lots of time between now and April 30, though.

David, likewise wishing you and all of us a good 2026.

In 2025 my wife and I continued to buy I Bonds. We also continued to think, not always but from time to time, “This bond issuer is $38 trillion in debt and its partisan officeholders may be fiddling, or planning to fiddle, with the inflation statistics. Are we nuts to continue buying I Bonds?”

So, to mix metaphors, all of us interested in inflation-linked bonds are in the same boat, and (oddly) only future hindsight will reveal whether the boat proved seaworthy. Maybe this is what’s called faith-based investing? 🙂

Note that TreasuryDirect assures you that savings bonds are “backed by the full faith and credit of the U.S. government.”

Bank on it!

Thank you for this summary! And thank you for another year of insight, research, and wonderful writing. How do treasuries fit into this 2025 summary, and what is the outlook for 2026? Happy new year!

Uncertainty is a word to use looking forward; not backward. There you just look at the performance. Pick your indicator, GDP growth, inflation, new home builds, S & P, etc. And depending upon what indicator you pick that’s your review.

“I am getting tons of feedback from readers who no longer trust the system.”

If your goal is to destroy the system, destroying trust in the system is a logical place to begin.

Thumbs up!

Right! Go with the crowd!

David: Your post brings to mind one of my favorite quotes–from the 1958 Italian novel, The Leopard:

“If we want things to stay as they are, things will have to change.”

For me it is ominous that we continue to have huge Federal deficits even though the economy seems to be in decent shape. It is as though we are addicted to a fiscal fentanyl. I hesitate to think what could happen if we slide into a recession or worse.

I think it is interesting that in the UK, one of the budget balancing techniques adopted by both the Conservative and Labour governments is a freeze (for ten years now from 2021 to 2031) on inflation adjustments to tax brackets. There are also suggestions that the CPI-related increases in the UK state pension may have to be trimmed to meet budget constraints.

The UK has been pushed to these drastic remedies because it has not shared the license that has been enjoyed by the US to run ever larger deficits. If (or when) the open-ended access to financing that the US has long enjoyed reaches its limits, CPI adjustments to tax brackets, Social Security, etc., could well be targeted here.

The Leopard! My Sicilian ancestors would be proud of this reference. You raise excellent points. We have had surprisingly strong economic growth in 2025 along with cuts in government jobs and yet the deficit continues to rise. We are not going to “grow” out of this problem. It is going to take some pain and a rare streak of courage from our politicians.

David, we note the recent deletion of a post…any secret way of doing that?

I can do it, but I don’t think you can. That deletion was an exact duplicate comment, which happens fairly often.