By David Enna, Tipswatch.com

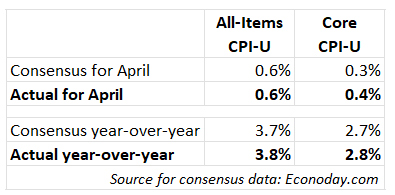

The lingering war in the Mideast, and its oil-price shock, sent U.S. seasonally-adjusted inflation 0.6% higher in April and pushed the annual rate to 3.8%, its highest level since May 2023, the Bureau of Labor Statistics reported today.

Core inflation rose 0.4% for the month and 2.8% for the year — both numbers higher than expectations.

Economists expected an ugly report for April, but this was a bit uglier than forecast. Gasoline costs were a key factor, of course, rising 5.4% in the month after soaring 21.2% in March. Gas prices are now up 28.4% over the last year. The BLS said energy costs accounted for 40% of the all-items increase.

Shelter costs rose 0.6% for the month, a high number that was boosted by April survey data replacing missing data for October 2025. For October, when no data were collected, BLS set shelter inflation at 0.0%, obviously too low. This report begins to bring annual inflation back into line. Did shelter costs truly rise 0.6%? Probably not.

Also in the report:

- Food at home costs increased a disturbing 0.7% in April, after falling 0.2% in March. The annual rate is now 2.9%.

- Costs of fruits and vegetables were up 1.8% for the month and 6.1% for the year.

- Beef prices rose 2.7% for the month.

- Apparel costs rose 0.6% for the month and 4.2% for the year.

- Airline fares were up 2.8% for the month and are now up 20.7% for the year.

- Costs of new vehicles fell 0.2% for the month and are up only 0.2% for the year.

- Costs of used cars and trucks were flat for the month.

- Costs of medical care services were flat but up 3.2% for the year.

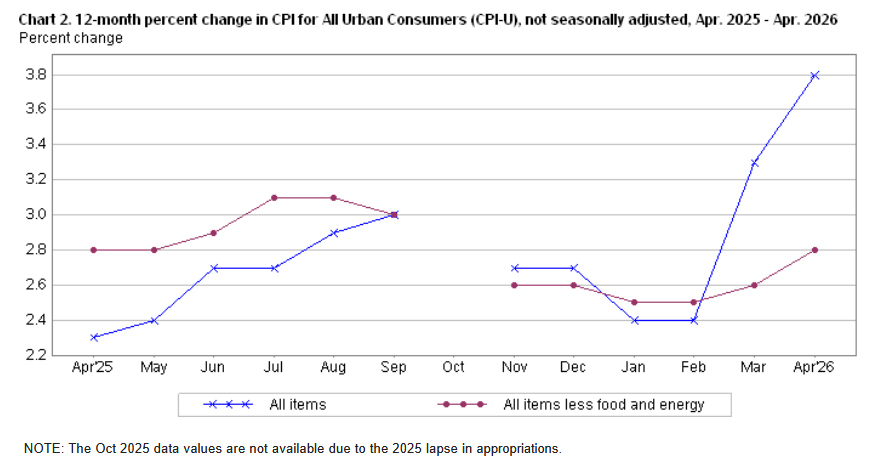

Although gasoline and shelter dominated this April report, there were many signs of inflation creeping across the economy — food, airline fares, household furnishings, apparel, etc. The result is this very scary chart:

What this means for TIPS and I Bonds

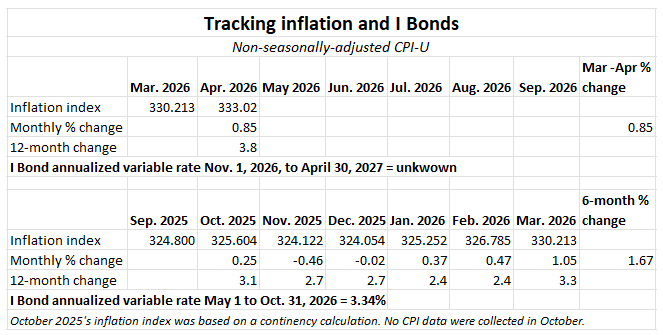

Investors in Treasury Inflation-Protected Securities and Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances for TIPS and set future interest rates for I Bonds. For April, the BLS set the inflation index at 333.020, an increase of 0.85% over the March number.

For TIPS. The April report means that principal balances for all TIPS will rise 0.85% in June after rising 1.05% in March. These are gaudy numbers, but will be balanced off later in the year when non-seasonally-adjusted inflation runs lower than the seasonally-adjusted version. Here are the new June Inflation Indexes for all TIPS.

For I Bonds. April is the first of a six-month string that will determine the I Bond’s new variable rate, which will be reset November 1. We can’t draw any conclusions from this one-month 0.85% increase, but I can say it is the highest April number over the last 14 years I have been tracking this data.

What this means for future interest rates

We can be certain the Federal Reserve, even under Kevin Warsh’s new leadership, will not be cutting short-term interest rates until this energy shock settles down and we can see the lasting results.

With inflation surging, should the Fed be raising interest rates? Also not likely, especially if the U.S. economy begins slowing down under the weight of energy costs. So I am thinking we are in a period of uneasy stability for short-term rates.

From today’s Bloomberg report:

Even if the current ceasefire holds and the Strait of Hormuz reopens soon, economists anticipate higher costs are likely to persist in the months ahead as oil output normalizes and shipping flows recover. …

The FOMC is likely to be concerned by renewed signs of food inflation accelerating, given the risk that higher gasoline and food prices together will further boost households’ inflation expectations.

And the Wall Street Journal:

The April report is the latest sign that the rate cuts that markets were pricing in at the start of the year are no longer a 2026 story. … Now, the policy debate within the Fed has shifted away from when to cut rates and toward when to start signaling that a rate hike is as likely as a rate cut.

It’s possible we could see inflation begin to stabilize in coming months, while remaining in a range around 4.0%. That is not the set-up for cuts in interest rates. And once again, we can see the value in investing in inflation protection.

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I welcome donations, any amount. And FYI, ads on this site pay for about one visit to Costco.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I don’t see how that inflation will be coming down much in the next few months with the current high energy and fertilizer costs extended projections.

Last month I pointed out that the I Bond rate would be smoothed out by timing, because the first spike in inflation due to the war occurred during the final month of the May 1 reset, and the second would occur during the first month of the next period. With today’s CPI Report being as bad as expected, or even worse, I decided to ask Chat GPT what the rate would be if the reset period shifted one month forward. In other words, what would the composite rate have been if you lopped off the September CPI and included April. Here’s what it calculated:

Today’s April CPI report showed the NSA CPI-U at 333.020.

So if you hypothetically shifted the calculation window forward one month — effectively using April instead of March — the numbers would look roughly like this:

Actual May 2026 semiannual inflation factor: about 1.66%

Hypothetical factor using April CPI: about 2.58%

Annualized variable rate: about 5.16%–5.18%

Using the current fixed rate of 0.90%, the composite rate formula is:

Where:

F = 0.009

I \approx 0.0258

That produces a hypothetical composite I Bond rate of approximately:

6.1%

instead of the actual 4.26% announced for May–October 2026.

OK, I did the same calculation: The six-month inflation rate was 1.65%. Subtract October’s 0.25% and add April’s 0.85%, and you get 2.25%, which equates to a variable rate of 4.50%. Add in the 0.9% fixed rate and you get a composite rate of 5.42%.

This is why we invest in TIPS and I Bonds. Thanks for your continued efforts to keep us educated.

Edward, thank you for sharing your horror story of interacting with Treasury Direct. Just when I start sniffing around I-bonds again; your story hardens my resolve to not invest in TD again.

Unrelated to this particular post. but i think a good reminder for people who use Treasury Direct. On February 25, 2025, I purchased a 30 year treasury note on the Treasury Direct website no problems it worked as expected. My ignorance was that I didn’t realize that you can not sell securites inside the Treasury Direct account. So I began the process of transfering the security to my brokerage account( discount broker). On July 15, 2025, I initiated a transfer request going through my brokerage account to transfer the security from the Treasury Direct Account to my brokerage account, that took about two weeks to complete. (I went this route because we do not have a Medallion Signature Guarantee in the small town where we live.) I finally got notice that Treasury Direct received the transfer request through an email on August 14, 2025. Then I waited. I called Treasury Direct every few months to check on the status. Once they tried to tell me that there was no request under my name, so I gave them the Transfer Request number, and they were finally able to find it. (Always keep your evidence of the transfer.) I was informed every time I called that it was an extra ordinary request, and that it could take up to 12 months to complete. I finally received notification May 6, 2026 that the transfer had completed and indeed it showed up in my brokerage account on that date. Lessons learned through trial. 🙂

I would caution all who use Treasury Direct to consider whether your purchase could be done in a brokerage account. I know you can’t buy I Bonds via brokerage. I’ve had an account with them for over 25 years, and I am winding down my I-bonds as they approach maturity. Mr. Howard’s example is one of many I’ve read about the trials of using Treasury Direct. Think about how bad this could turn if your heirs had to deal with TD? Best to all!

Thank you for writing about your experience. I Guess your lucky it was done in under 1 year.

With the 10 Year TIPS auction opening on May 14th, we shall see what the yield will do. I would wager that it will be over 2% as of now it’s 1.95.

Thank you for your speedy post.

Can you say more on your thought process here? I was wondering if there would be increased demand because of the headline-generating inflation numbers, which then would drive down the real yield.

The big question I have is will Wednesday’s 30-year bond auction price with a 5 handle. It’s just above 5 this morning.