By David Enna, Tipswatch.com

It’s Day One of the U.S. government shutdown, and the crucially important, non-partisan Bureau of Labor Statistics now has one working employee: acting commissioner William Wiatrowski. The other 2,054 employees have been (or will soon be) furloughed.

The Labor Department last week published a contingency plan for the shutdown, which included these details:

- The Labor Department’s working employees will be reduced from 12,916 to 3,141.

- The BLS is listed in the group that will “completely cease operations.”

- No economic data will be released.

- All active data collection activities for BLS surveys will cease.

- The quality of data collected in the future could be impaired.

- The BLS website will not be updated.

The one qualification for the BLS was that activities related to backing up systems may take up to three days.

Coinciding with the shutdown, President Trump on Tuesday withdrew the nomination of E.J. Antoni to lead the BLS. A White House official offered the New York Times no reason for the sudden change, saying only that Antoni was a “brilliant economist” and that Trump would announce a new nominee soon.

Antoni turned out to be an extremely controversial choice for a job typically filled by non-partisan, lifelong government statisticians. Trump chose him for the job after firing Erika McEntarfer in August and claiming the BLS “rigged” data to make his administration look bad.

Antoni, who authored parts of Project 2025, has been critical of how the BLS collects data. He also called for McEntarfer’s firing during an appearance on Steve Bannon’s “War Room” podcast, agreeing with the host that they needed a “MAGA Republican” at BLS.

That was a bad look for a non-partisan job, but Antoni’s nomination was further hurt by photos and video showing he was in the crowd at the Jan. 6 riot at the U.S. Capitol. Antoni contends he was a “bystander.” And then his nomination was doomed after CNN’s KFile investigative team discovered Antoni ran a since-deleted X account with sexually degrading and bigoted attacks.

All of this made me wonder if Antoni would even get to a confirmation hearing, where a lot of this inflammatory material would be discussed and Antoni would have to respond under oath. The hearing was “scheduled” for September but was continuously delayed. Apparently Republican senators Susan Collins and Lisa Murkowski refused to even meet with Antoni and others said privately they were not likely to confirm him, according to CNN.

So the nomination was pulled, and this is a good thing for the BLS on a day when 2,054 workers are being furloughed. Trump will name another nominee soon and I have a suggestion: Elevate William Wiatrowski, the interim commissioner, to the job. He was acting BLS commissioner from January 2017 to March 2019, during Trump’s first term.

The BLS shutdown

About 11 a.m. the BLS.gov website finally posted a notice about the shutdown: “This website is currently not being updated due to the suspension of Federal government services. The last update to the site was Wednesday, October 1, 2025. Updates to the site will start again when the Federal government resumes operations.”

These economic reports, among others, will not be issued during the shutdown:

- Oct. 3: September employment report

- Oct. 15: Consumer Price Index for September

- Oct. 16: Real earnings for September

- Oct. 17: Producer Price Index for September

The Bureau of Economic Analysis, which is part of the Commerce Department, has posted a notice on its site: “Due to a lapse in appropriations, this website is not being updated.” The BEA issues the Personal Consumption Expenditures Index, the Federal Reserve’s favored measure of inflation. The next report is due Oct. 31. Let’s hope the shutdown has been resolved by then.

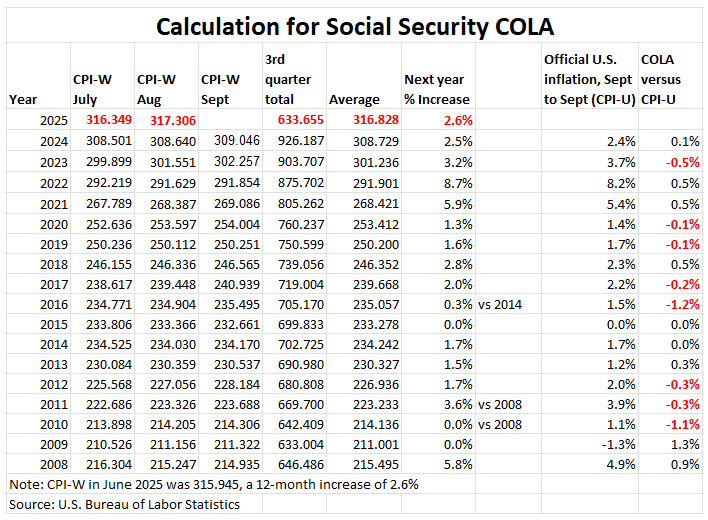

Things are going to get tense if the BLS cannot release a CPI report for September, which is the last month of data needed to determine next year’s Social Security cost-of-living adjustment and the new variable rate for the U.S. Series I Savings Bond. In addition, that September data is important in calculating next year’s Medicare rates, IRMAA levels and even 2026 income tax brackets.

The Federal Reserve is going to be flying blind until the shutdown is resolved, with both jobs and inflation data being locked down. From the New York Times:

“It pains me that we wouldn’t be getting official statistics at exactly a moment when we’re trying to figure out is the economy in transition,” said Austan Goolsbee, president of the Federal Reserve Bank of Chicago and a voting member on this year policy-setting committee.

What’s ahead?

It’s difficult on day one to see how this crisis will be resolved, since the Trump administration seems perfectly willing to embrace the shutdown and Democrats won’t take action to end it.

Assuming the White House doesn’t go “nuclear” by implementing widespread firings of federal workers, Democrats could possibly work out a separate deal (outside of the continuing resolution) assuring consideration of legislation to extend Affordable Care Act subsidies. A lot of Republicans want those ACA subsidies extended, as noted by the Wall Street Journal:

GOP leaders are already hinting that they are open to negotiating, and some are floating ideas that would give Democrats much of what they want. “I don’t love the policy, OK?” Speaker Mike Johnson said recently. “But I understand the political realities.”

My opinion is that the GOP has the upper hand in the “spin war,” and that is why you see Republican after Republican on television extolling their “clean 7-week continuing resolution,” without any baggage they’ve added in the past (build the wall, abolish Obamacare, etc.)

Any solution is going to take time, ticking toward that crucial Oct. 15 inflation report. From the Wall Street Journal:

House lawmakers aren’t expected to return to Washington until next week and any compromise funding proposal would need their approval. Congress hasn’t passed any appropriations bills, so unlike during the 34-day partial shutdown that ended in 2019, no government offices have been funded.

Nothing about this shutdown is good news.

NOTE: While this posting has triggered ‘healthy debate,’ I have decided to shut down commenting so we can go back to focusing on real yields, inflation and safe investments.

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

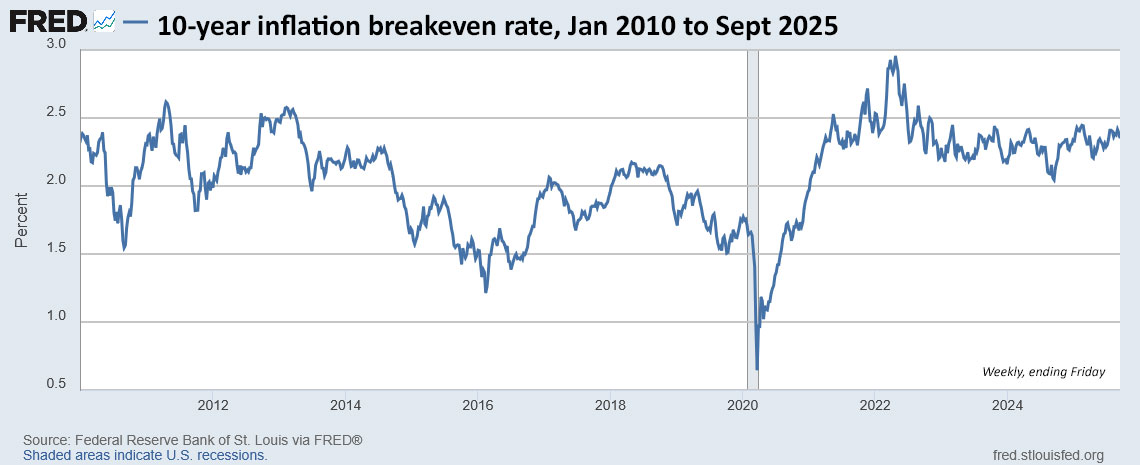

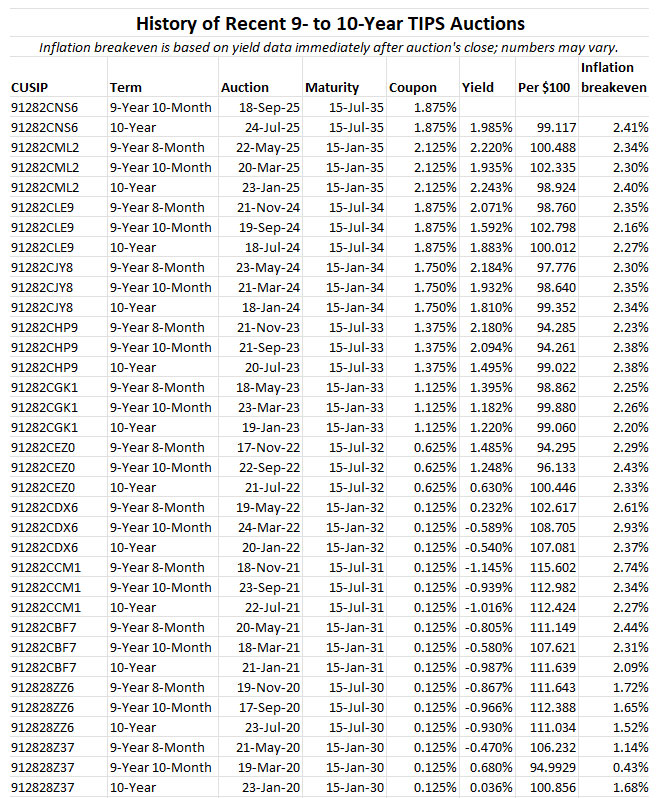

Dongchen, I always say that the inflation breakeven rate reflects sentiment but is a fairly lousy predictor of future inflation.…