Can U.S. economic data be trusted?

By David Enna, Tipswatch.com

Bloomberg carried an article last week with a stunning headline: “Distrust In US Inflation Data Threatens $2 Trillion Market.” The premise was that the $2 trillion market in Treasury Inflation-Protected Securities could crack if U.S. inflation data are politicized.

This comes as no surprise to Tipswatch readers, where commenter discussions have raged over the last week on the safety and value of TIPS and Series I Savings Bonds, which also rely on accurate inflation data. The fury was set off by President Trump’s firing of Erika McEntarfer, head of the Bureau of Labor Statistics, after a huge downward revision in jobs numbers. Some examples:

The firing of the BLS Commissioner for no reason will mark a seminal moment in our economy and markets. World markets and investors will question whether our data is being manipulated for political purposes. …

CPI stats will diverge completely from reality, and anyone who talks of it will be blacklisted and fired or their employer punished into firing them. TIP and i-bond payouts and all COLAs will be paid based on these opinion statistics. …

My worst fears as an I-bond and TIPS investor are about to be realized. Manipulated inflation data is on the way. …

I will definitely be holding off on new purchases until I see what happens with the BLS numbers. …

I’m NOT reaffirming my commitment to TIPS.

Reality check

The Bloomberg article (the link is outside the paywall), noted that government data have a major effect on asset prices and especially for TIPS, which rely on monthly inflation data to set ongoing principal adjustments and future coupon payments.

“If there is politicization of the BLS, and somehow the data is not credible it poses an enormous risk over time to the TIPS market,” said Amar Reganti, fixed income strategist at Hartford Funds.

That concern was echoed by Michael Feroli, chief US economist at JPMorgan Chase & Co. “The $2.1 trillion market for TIPS is built on a foundation of trust in the construction of the CPI data,” Feroli wrote.

Fear that the Trump administration will “cook the books” predates the firing of McEntarfer, but the firing set paranoia into overdrive. Is this fear realistic? About a month ago, I had a long talk with a now-retired high-level official of BLS who worked on the jobs reports. He noted that the economists and statisticians at the BLS would mightily resist any attempt to fake the numbers.

“It won’t happen,” he said. “There is only one political appointee at the BLS, the commissioner.” (Until Aug. 1, the one political appointee was McEntarfer. She has been replaced temporarily by William Wiatrowski, who has been deputy commissioner since 2015 and acting commissioner under both Trump and Biden.)

The retired BLS official did note that the BLS’s declining budgets, cuts in staffing and poor survey response levels could lead to inaccuracies. The BLS is relying more on “estimation” when full data aren’t available. “When you are estimating, you tend to go more with the status quo until you get a more complete picture,” he said.

This was the topic of a recent Bloomberg Odd Lots podcast, where hosts Joe Weisenthal and Tracy Alloway interviewed Bill Beach, BLS commissioner from 2019 to 2013. Listen to the podcast, titled “How Trump just politicized US economic data.”

A lot of the discussion is a deep dive into BLS operations, but here is one key point: Beach noted the BLS commissioner (up to this point) “plays no role whatsoever in massaging the data.” Trump accused McEntarfer of “faking” the jobs number and manipulating them for political purposes. I’d say with near 100% certainty that didn’t happen, and faking the numbers will be difficult for any future Trump appointee.

See also: A historical look at political influence over the BLS

Jack Hough’s Streetwise podcast also took on this topic this week, from an investor’s viewpoint, airing a fascinating interview with Thierry Wizman, a strategist at Macquarie Group and author of a recent report titled “How Do You Play the Data Integrity Mess?”

Wizman pointed out the poor jobs data for June actually worked in Trump’s favor, at least partially, because the Federal Reserve now seems likely to cut short-term interest rates two to three times this year, something Trump has been demanding. But surging inflation data would be viewed very negatively by Trump because it would be an indictment of his tariff policy.

Obviously, firing the head of the BLS is a way of acting upon his impulses, or at least his inherent view, that there is something wrong with these agencies. And that just changing the person who’s running the show is a way of fixing this. If you take this all at face value, what he wants is accuracy. Do we really believe that? Probably not.

What I think he wants, which is more consistent with his appointments generally speaking during this administration, is someone who is loyal. … And I mean politically loyal.

Hough asked Wizman specificially about TIPS from an investor’s point of view if inflation data becomes suspect.

That is a risk, and I would venture that if people start thinking this way about these changes, well then they’re not going to want to hold these TIPS. They certainly don’t want to hold the ones that mature during the period in which you believe that the physical agencies may corrupt the CPI calculation. But again, we’re in the realm of speculation here. We’re not yet at a point where we can say that the process will be affected.

The big picture

Will investors now look at all the BLS jobs and inflation reports with a wary eye?

Yes, of course they will. It is human nature. Every economic report we see going forward is going to have a faint stigma of manipulation, even if it isn’t true. From Barron’s columnist Randall Forsyth last week:

“In a scenario where TIPS are unable to provide a hedge against inflation because of the uncertainty around the CPI index published by BLS, its overall demand might start decreasing,” wrote Morgan Stanley fixed-income analysts Aryaman Singh and Matthew Hornbach in a client note.

In other words, if the market senses the CPI is being suppressed artificially, it will exact a penalty in the form of a lower price for the securities, which translates into a higher yield.

Forsyth goes on to note historical instances of data-manipulation in China, Argentina, Turkey, with mostly disastrous results. These are not models the United States should follow. He ends with investment advice:

The suppression of reported inflation would mean inflation-indexed investments such as TIPS would underperform. … A better hedge would be gold, which should benefit if the CPI is manipulated.

An alternate view

Michael Ashton, a reliable inflation watcher who tends to support Trump’s economic policies, dispelled some of the gloom and doom in a podcast posted Aug. 6. He also noted the problems in BLS data collection and admitted that economists worry the firing of McEntarfer “could diminish the credibility of the Bureau of Labor Statistics.”

Ashton asks, “Is this a sign that the end of government credibility (okay, stop laughing) is nigh?” Opposing views are important to hear, so here you go:

“This particular problem falls into the category of it doesn’t really matter,” Ashton says, noting that interim commissioners have headed the BLS about a quarter of the time since the 1990s. He makes the argument that CPI reports — even with some estimation — are much more reliable and consistent than the jobs data.

Ashton, by the way, has argued the Fed should not be cutting short-term interest rates in this current economy because the risks of inflation remain high.

My thoughts

Is the sky falling? No. But things are very cloudy.

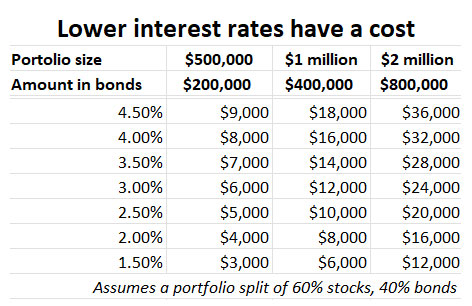

Staffing, budget and process issues at the BLS have been called “a slow-moving train wreck” requiring immediate attention. Beyond TIPS and I Bonds, the CPI data are used to calculate Social Security benefit increases, some pension increases, wage increases, etc.

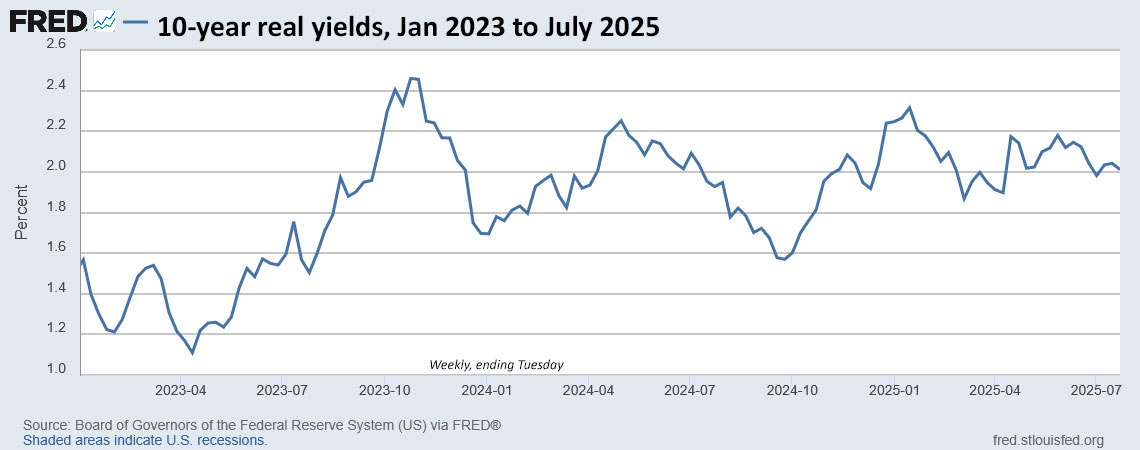

I remain committed to TIPS and I Bonds as investments. I don’t think inflation data will suddenly become an outright fantasy, but could be manipulated in minor ways. Budget and staff cuts could cause inaccuracies. And it could be that because of investor wariness over data, we will see real yields on medium- to longer-term TIPS begin to rise.

We will get the July inflation report at 8:30 a.m. EDT on Tuesday. Economists are forecasting an increase of 0.2%, a run-of-the-mill number. Whatever the result, I think we can trust that BLS staffers did their best. The interim commissioner has been at the BLS for a decade. Nothing has changed at this point.

It’s unfortunate that these two ultra-safe and ultra-useful investments — TIPS and I Bonds — are now called into question because of a rash decision by the president. Yes, the firing of McEntarfer could be justified after the massive jobs-number revisions. That was a big miss. But when Trump accused the BLS of “faking” and “manipulating” numbers for political reasons he opened a dangerous Pandora’s box.

Investors have noticed. The result could be declining demand for inflation-linked investments. That’s too bad.

Aug. 1: President Trump fires head of the Bureau of Labor Statistics

Aug. 4: Treasury reaffirms its commitment to TIPS

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Thanks!