The US Treasury just announced that the fixed rate on Series I Savings Bonds will remain at 0.0% from May to October, meaning I Bonds purchased in this period will earn a composite rate of 0.0% for six months. In addition, the Treasury raised the EE Bond fixed rate to 0.3% and left intact the guarantee that EE Bonds will double in value if held for 20 years.

The US Treasury just announced that the fixed rate on Series I Savings Bonds will remain at 0.0% from May to October, meaning I Bonds purchased in this period will earn a composite rate of 0.0% for six months. In addition, the Treasury raised the EE Bond fixed rate to 0.3% and left intact the guarantee that EE Bonds will double in value if held for 20 years.

The earnings rate for Series I Savings Bonds is a combination of a fixed rate, which applies for the 30-year life of the bond, and the semiannual inflation rate, also called the variable rate.

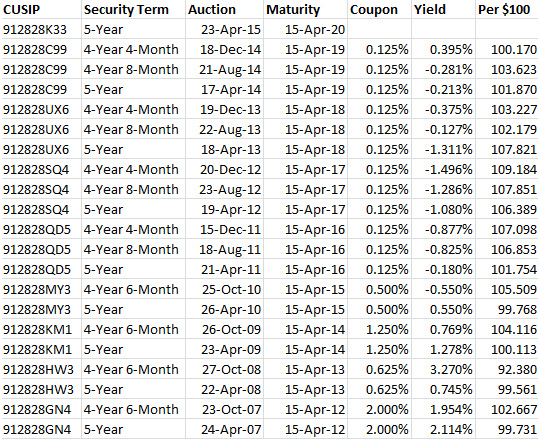

The new I Bond variable rate of -1.60% (annualized) was set in stone when the Bureau of Labor Statistics released the March inflation number. This May 1 adjustment is determined by non-seasonally adjusted CPI-U for September to March. Here are the numbers, from my Tracking Inflation and I Bonds page:

The composite I Bond rate is determined by adding the variable rate (-1.60%) to the fixed rate (depends on when the I Bond was issued). Any I Bond with a fixed rate of 1.60% or less – and that is every I Bond issued in the past 13 years – will get a composite rate of 0.0% for six months. This is because I Bonds cannot pay negative interest; the lowest they can go is 0.0%. The starting date of that 0.0% period depends on which month you purchased the I Bond, but they will all get six months of it.

The composite I Bond rate is determined by adding the variable rate (-1.60%) to the fixed rate (depends on when the I Bond was issued). Any I Bond with a fixed rate of 1.60% or less – and that is every I Bond issued in the past 13 years – will get a composite rate of 0.0% for six months. This is because I Bonds cannot pay negative interest; the lowest they can go is 0.0%. The starting date of that 0.0% period depends on which month you purchased the I Bond, but they will all get six months of it.

One point to consider: Since inflation fell at an annual rate of 1.60% over the last six months, your I Bond paying 0.0% is beating inflation by 1.60%. This is one of the benefits of I Bonds: They lose no value in times of deflation, which isn’t true of the principal balance of TIPS, which declines with each deflationary month.

Should you dump your I Bonds paying 0.0%? One word answer: No. Since you are limited to I Bond purchases of $10,000 a year per person (plus $5,000 as a tax refund), I don’t think selling your I Bonds is a good idea. Unless: 1) you need the money today to meet current expenses, or 2) the I Bond has reached its 30-year maturity (none have as of yet, of course). The idea in I Bond investing is to build as large a cache of inflation-protected money as possible, to use as a resource in the future. Selling out of I Bonds will keep you from reaching that goal. Just be patient; wait out the six lousy months.

Should you buy I Bonds paying 0.0%? One word answer: No. It makes no sense to buy I Bonds in this May to October period. Instead, wait until the November 1 adjustment, which could bring a positive variable rate and the possibility of a fixed rate higher than 0.0%. You’d still have two months to buy your 2015 allocation. Inflation has already started ticking up, rising 0.6% in March on a non-seasonally adjusted basis. There is a good chance I Bonds will be paying a decent variable rate starting November 1.

What about EE Bonds? The Treasury’s decision to pump the fixed rate from 0.1% to 0.3% was a nice gesture, but in effect it is meaningless. The key to EE Bonds is this clause:

All Series EE bonds issued since May 2005 earn a fixed rate in the first 20 years after issue. At 20 years, the bonds will be worth at least two times their purchase price.

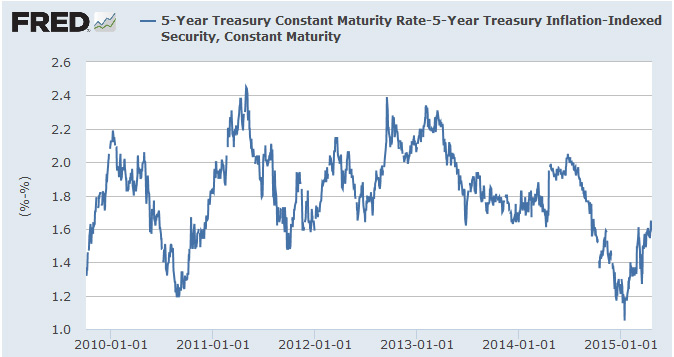

The Treasury kept intact the 20-year doubling of value, which in effect creates a 20-year, tax-deferred Treasury bond paying 3.5%. This is an outstanding value, given that a 30-year traditional Treasury is currently paying 2.75%, and a 20-year is paying 2.49%, more than 100 basis points lower. That is a huge difference in a 20-year investment.

EE Bonds are the investment of choice in mid-2015, if … and only if … you can afford to hold them for the full 20 years.

I'm new to the TIPS world but in the past year have funded about 1/2 of a 25 year TIPS…