By David Enna, Tipswatch.com

Yes, Tuesday. This month, the U.S. Treasury is breaking from its tradition of holding auctions for Treasury Inflation-Protected Securities on a Thursday. This month, it will be Tuesday, June 17.

Why? Well, you could ask Google’s AI bot and you would learn it has no idea:

According to TreasuryDirect, the U.S. Treasury’s website, 5-year TIPS are generally auctioned on the next to last Thursday of April and October, and reopenings are typically auctioned in June and December. However, the specific date of June 17th being a Tuesday for a 5-year TIPS auction would indicate a deviation from the standard schedule.

Really? That wasn’t helpful. Let’s try Microsoft’s version of Chat GPT:

The shift in the auction date is likely due to scheduling adjustments based on Treasury borrowing needs, policy decisions, or holiday considerations.

OK, also not helpful. So let’s ask Dave, the human editor of Tipswatch.com:

Thursday, June 19, is Juneteenth, a federal holiday that commemorates the end of slavery in the United States. On June 19, 1865, Gen. Gordon Granger ordered the final enforcement of the Emancipation Proclamation. Because June 19 is a federal holiday, the TIPS auction was moved to Tuesday, June 17.

The auction

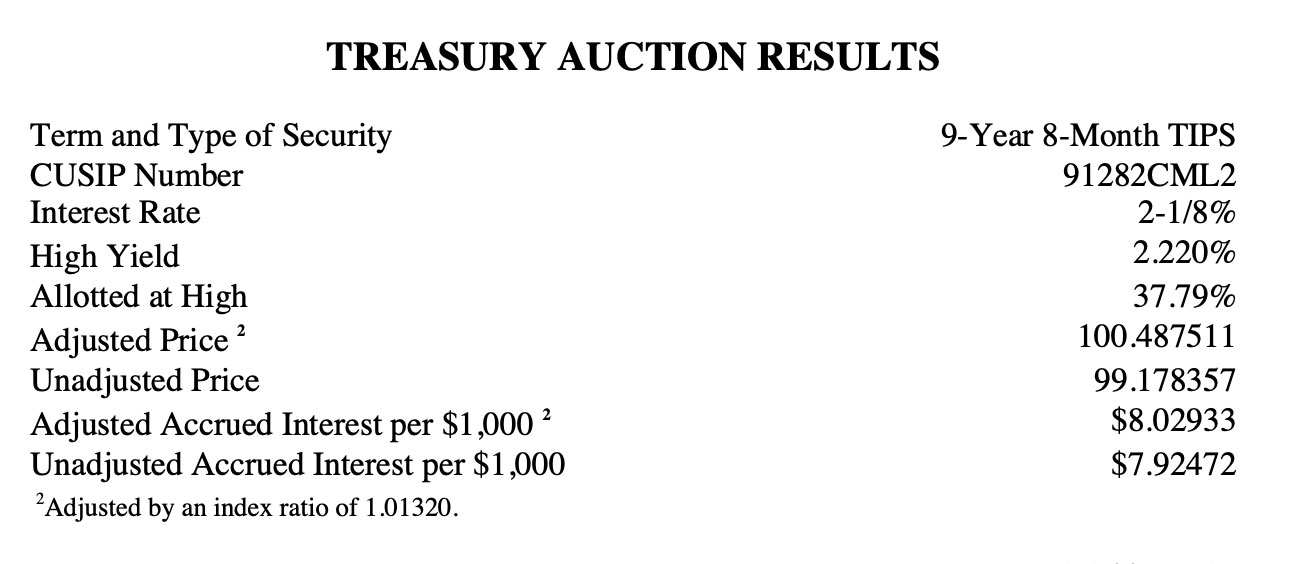

The Treasury will offer $23 billion in a reopening auction of CUSIP 91282CNB3, creating a 4-year, 10-month TIPS. This TIPS was originated on April 17, 2025, when the auction generated a real yield to maturity of 1.702%. Its coupon rate was set at 1.625%.

For anyone who cares, $23 billion is the largest offering for any 5-year TIPS reopening auction in the 28-year history of this investment, up from $22 billion in December 2024.

CUSIP 91282CNB3 trades on the secondary market, and it closed Friday with a real yield of 1.68% and a price of 99.77. That’s a very small discount because the real yield remains slightly higher than the coupon rate. You can track this TIPS in real time on Bloomberg’s Current Yields page. It is the 5-year TIPS listed there.

Friday was a day of fairly strong market volatility in the wake of Israel’s attack on Iran’s nuclear-processing facilities. But the real yield of this TIPS inched just a bit higher. Next week could bring chaos. Or stability. Be prepared.

Definition: The “real yield to maturity” of a TIPS is its yield above or below official future U.S. inflation, over the term of the TIPS. So a real yield of 1.68% means an investment in this TIPS would provide a return that exceeds U.S. inflation by 1.68% for 4 years, 10 months.

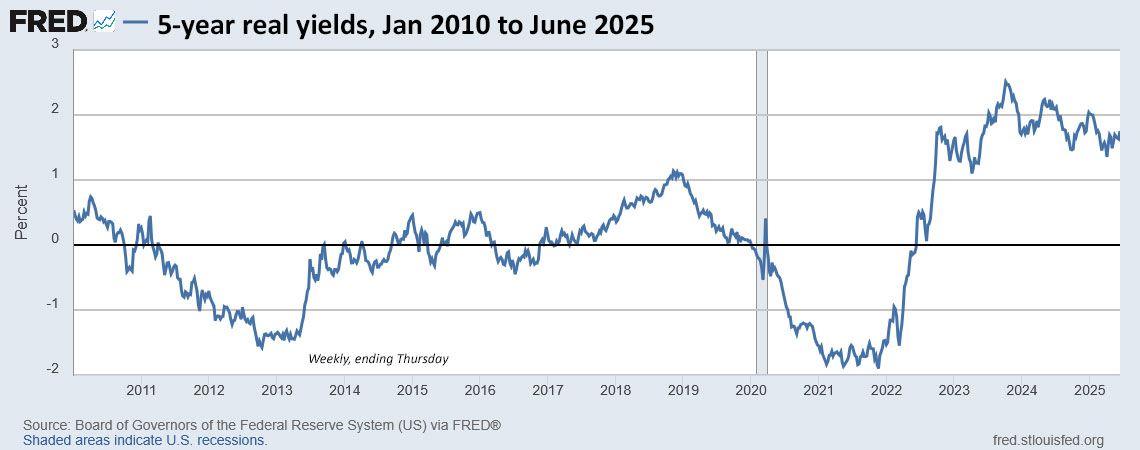

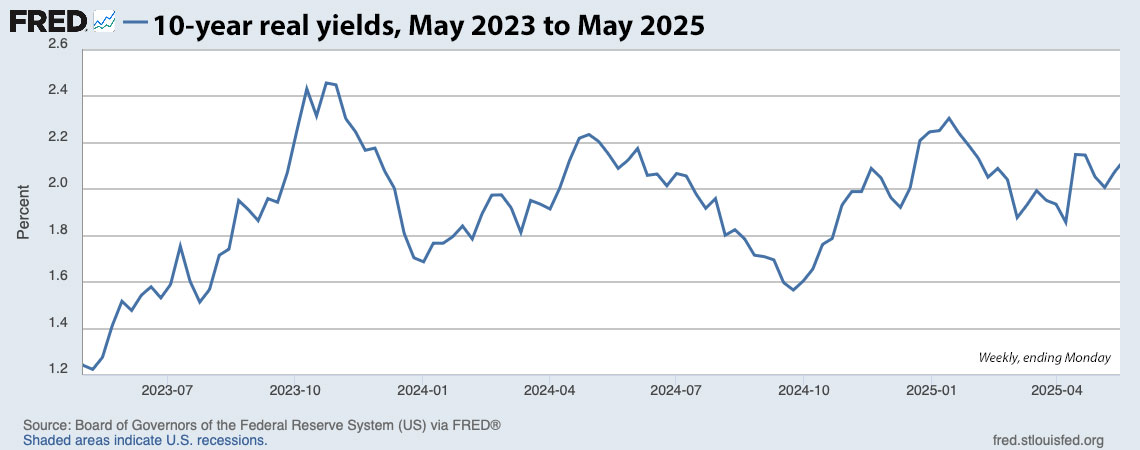

Here is the trend in the 5-year real yield over the last 15 years, showing the recent decline in yields, most likely caused by anticipation of future Federal Reserve cuts in short-term rates. But a 5-year real yield of 1.68% remains attractive, historically:

Of the monthly TIPS auctions, the 5-year is the most sensitive to Fed rate decisions. The Federal Reserve’s open market committee is scheduled to announce a rate decision on Wednesday, the day after this auction. It is highly unlikely to announce a rate cut on that day. But it could provide future guidance. Too late to matter for this auction.

If we see volatility over the next two days, it will likely come from dangers in the Middle East, not the Fed.

Pricing

At this point, it looks like the reopening auction should be priced close to par value. The current trading price is 99.77 and this TIPS will have an inflation index of 1.00764 on the settlement date of June 30. If the price holds (it won’t, but let’s use it as an example), this is what a purchase of $10,000 par value will look like at Tuesday’s auction:

- Par value: $10,000.

- Actual principal purchased: $10,000 x 1.00764 =$10,076.40.

- Cost of investment: $10,076.40 x 0.9977 = 10,053.22.

- + accrued interest of about $34.

Things will change by Tuesday’s auction, but this can give you a pretty good idea. You can also buy CUSIP 91282CNB3 on the secondary market before the auction, or after.

The advantage of buying at auction, especially through TreasuryDirect, is that even small-lot purchases will get the auction’s high yield. The advantage of the secondary market is that you can see exactly the price and real yield you will be receiving. The negative is that you may face a small bid-ask spread. Most of the time, it doesn’t make a huge difference.

Inflation breakeven rate

The 5-year Treasury note closed Friday with a nominal yield of 4.00%, which gives CUSIP 91282CNB3 a current inflation breakeven rate of 2.32%, more or less in line with recent auction results for this term. This means the TIPS will outperform a nominal Treasury if inflation averages more than 2.32% over the next 4 years, 10 months. Inflation over the last 5 years ending in May has averaged 4.6%.

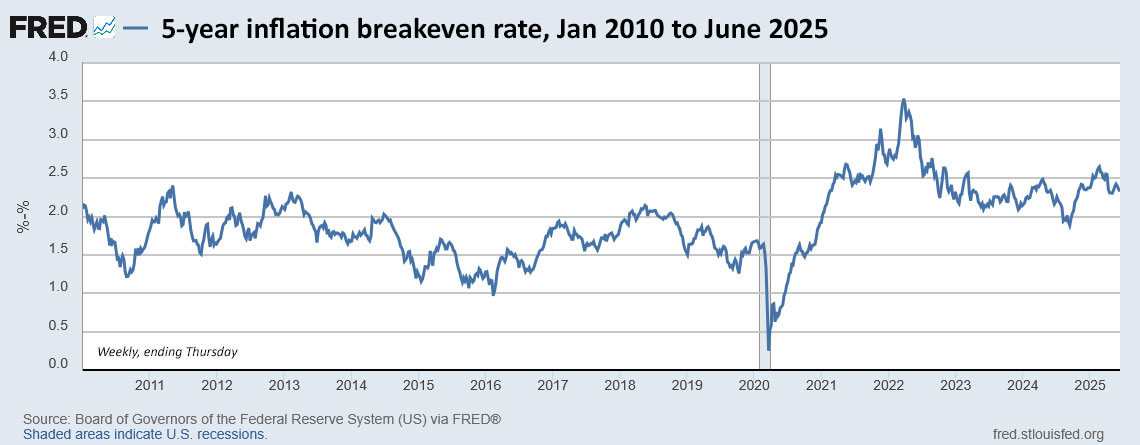

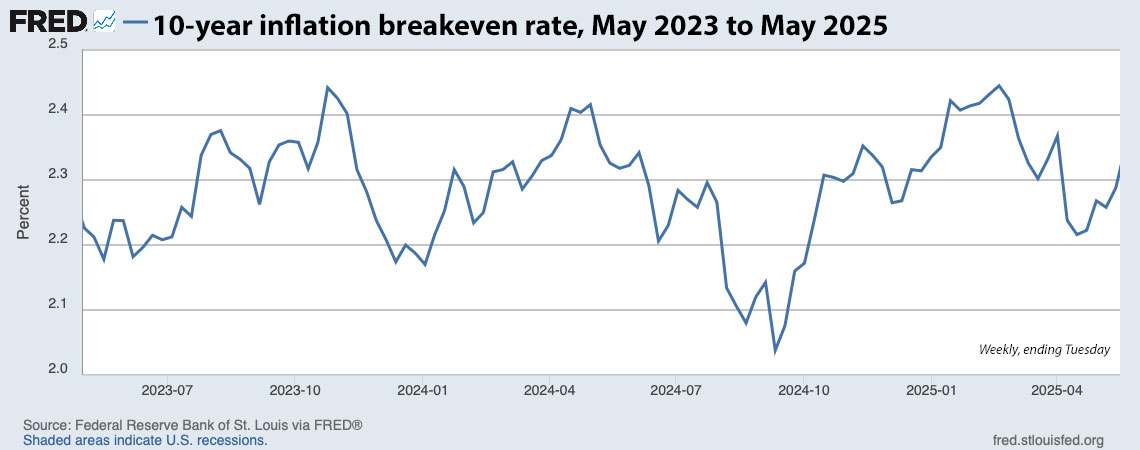

Here is the trend in the 5-year inflation breakeven rate over the last 15 years, showing the decline in inflation expectations since a peak in early 2022:

Thoughts

The Treasury market has returned to some “normalcy” with shorter-term TIPS having lower real yields than those for longer terms. The 5-year real yield of 1.68% is 95 basis points lower than the yield of a 30-year TIPS at 2.63%. That makes sense given the uncertainty surrounding future U.S. budget deficits.

I won’t be a buyer Tuesday because I have filled the 2030 rung of my TIPS ladder with issues I purchased at lower real yields (1.432%) and higher (2.009%).

If you are considering a purchase at this auction, keep an eye on Bloomberg’s Current Yields page, where you can track secondary market trading in real time. That should be a good — but not perfect — indication of where this auction is heading.

The TIPS auction closes Tuesday at 1 p.m. EST. Non-competitive bids at TreasuryDirect must be placed by noon Tuesday. If you are putting an order in through a brokerage, make sure to place your order Monday or very early Tuesday, because brokers cut off auction orders before the noon deadline.

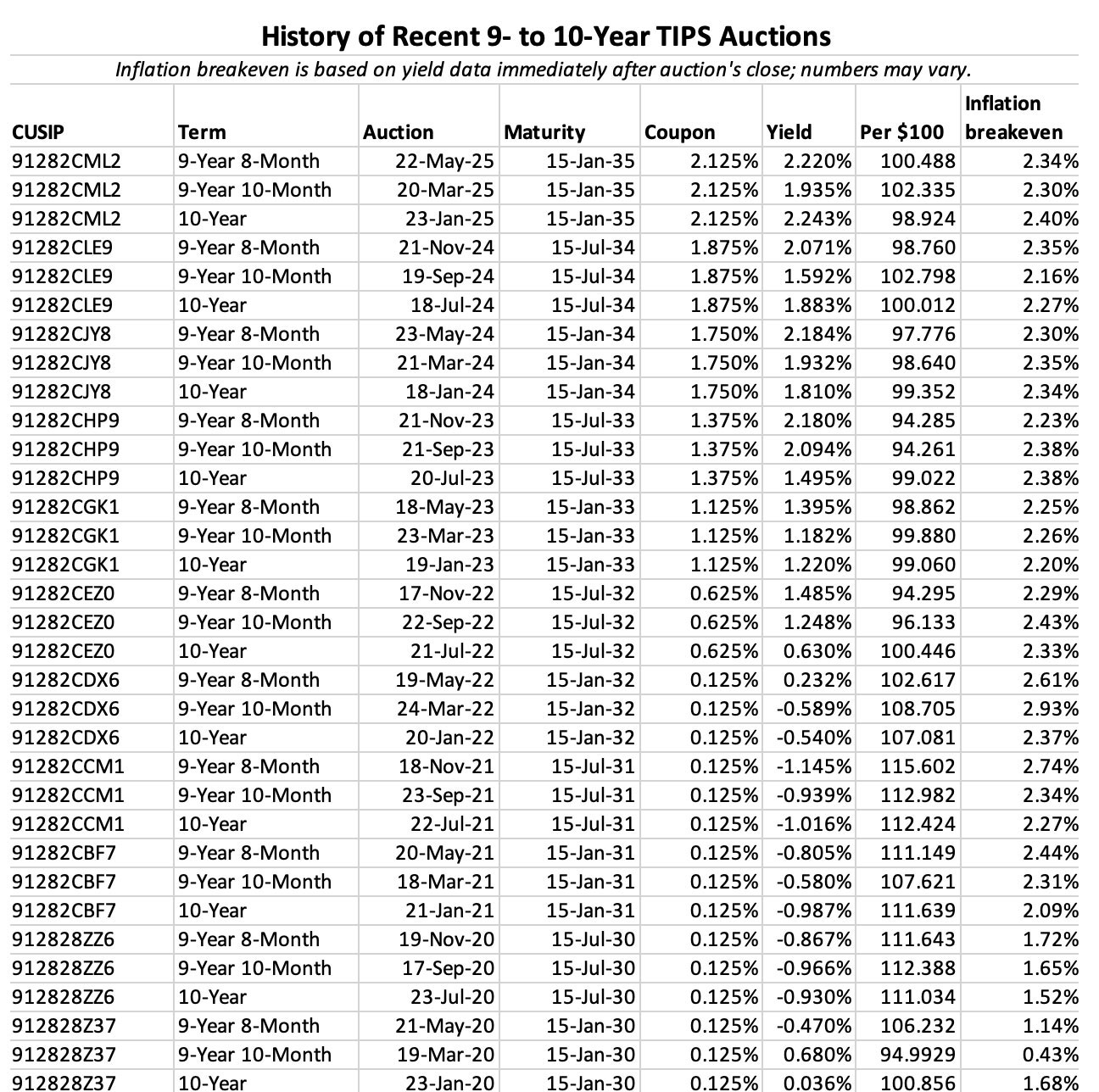

I will be posting the auction results soon after the close on Tuesday. Here is a history of auction results for this term over the last 5 years:

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

* * *

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

It definitely caused at least a small reduction in six-month inflation. What's amazing is if the United States didn't attack…