By David Enna, Tipswatch.com

I noticed this morning that real yields for Treasury Inflation-Protected Securities are shifting a bit in the wake of the U.S. attack on Iran. But so far these changes seem fairly routine.

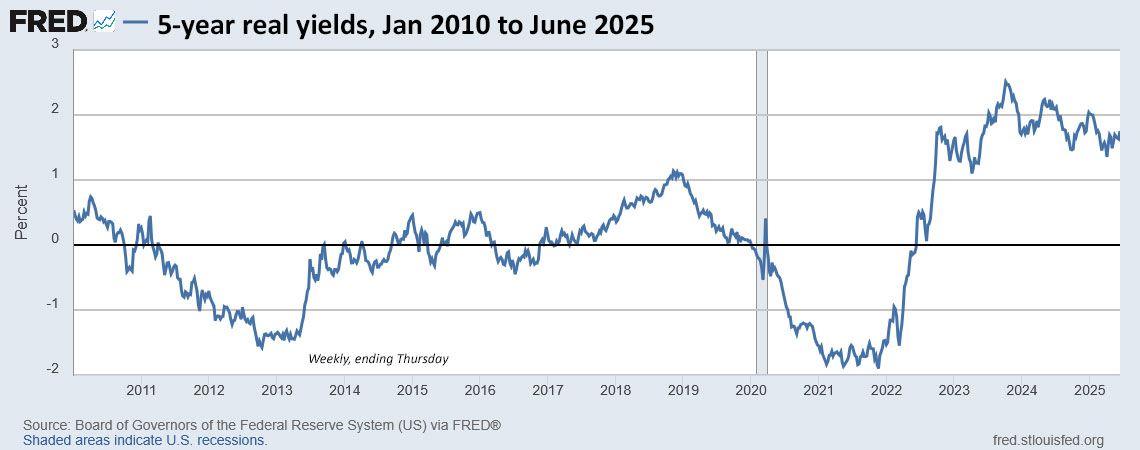

- The 5-year TIPS is trading this morning with a real yield of 1.54%, down from 1.59% at Friday’s close.

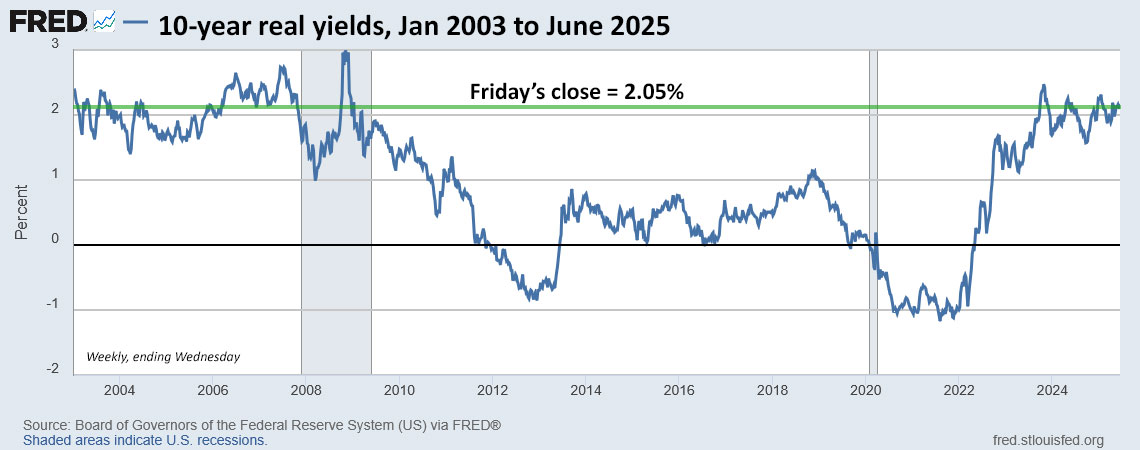

- The 10-year is at 1.99%, down from 2.05% on Friday.

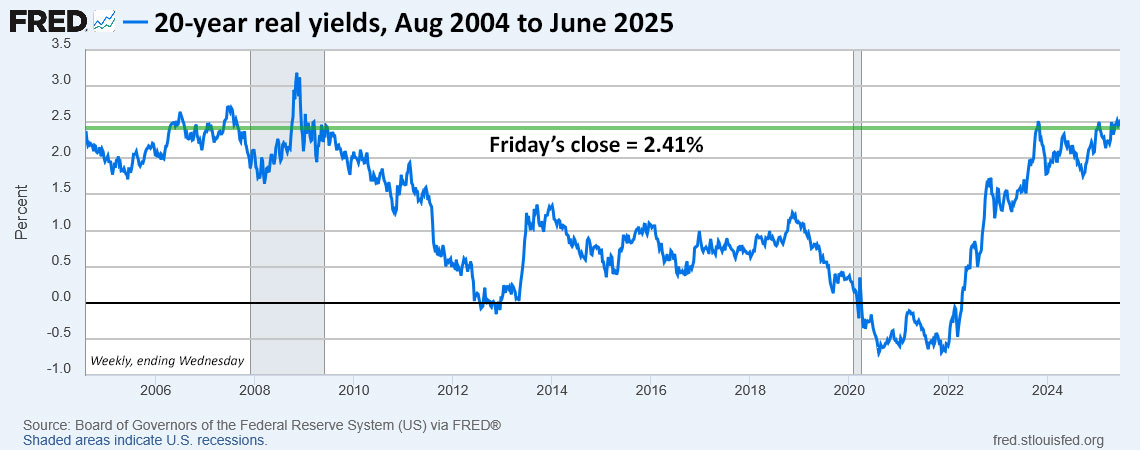

- The 20-year is at 2.52%, up from 2.41% on Friday.

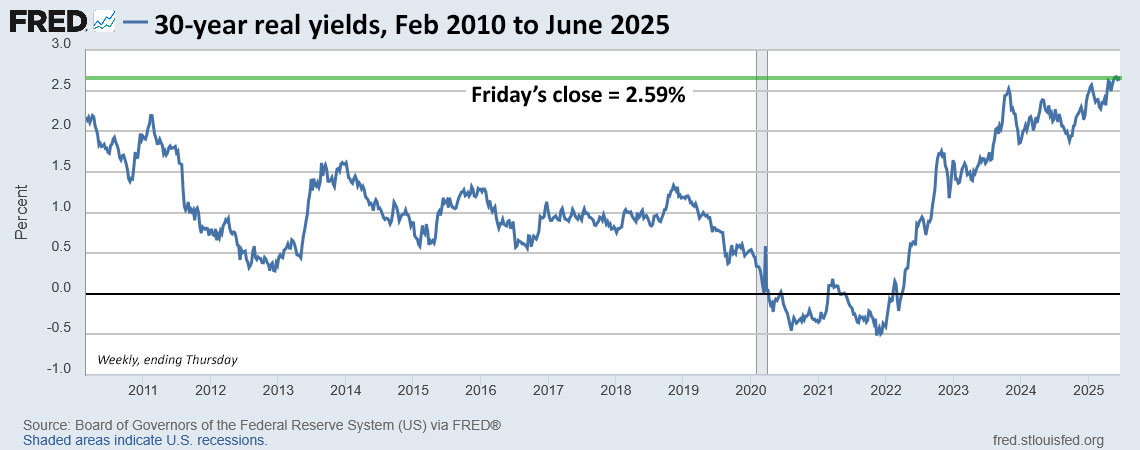

- The 30-year is at 2.57%, down from 2.59%.

The yield curve has been steeping throughout 2025 based on a couple of factors: 1) the shorter end (5 years or fewer) is more influenced by potential Federal Reserve cuts in short term rates later this year, and 2) the longer end reflects the high uncertainty about future U.S. budget deficits.

The 20-year TIPS is often an anomaly; the same goes for the 20-year Treasury bond, which often has a nominal yield higher than the 30-year bond. For many investors nearing or at retirement, the 20-year term is attractive because the term (hopefully) matches life expectancy.

Across the board, however, these real yields remain attractive. Could you call them historically “normal”? I’d say no, based on data from the last 22 years. The Federal Reserve of St. Louis compiles real yield data going back to 2003. A few years before that, toward the end of the dot-com bubble, real yields were extremely high, often reaching levels well above 3.00%. But the FRED (Federal Reserve Economic Data) database only goes back to 2003.

What is ‘real yield’?

Simply put, the real yield of a TIPS is the amount it will earn above official U.S. inflation over the term of the TIPS. If a 10-year TIPS has a real yield of 2.00%, and inflation averages 2.5% over the next 10 years, that TIPS will have a nominal return of 4.50% (give or take a slight variation because of compounding).

It’s not a difficult concept, right? But I once did a long interview with a Wall Street Journal freelancer writing an article on TIPS for a special section. He could not grasp the idea of real yield or how an investment could be pegged to something in the future. He decided to write this big piece without ever mentioning the term “real yield.”

I told him his editor would never allow it. His editor did allow it.

As regular readers of this site know, real yield is extremely important to investors in TIPS. In fact, it is the primary factor worth considering when buying on the secondary market.

So let’s look at real yields over the last 22 years.

5-year TIPS

Today’s 5-year real yield of 1.54% is in the high range when compared with the last 16 years, but fairly normal for the period of 2003 to 2007, just before the onset of the Great Recession. Notice the spike in real yields during that recession and also during the Covid crisis. Both of these were caused by panic selling of all assets, not from true economic reasons.

The 5-year real yield is nearly 100 basis points below its most-recent high of 2.51% in October 2023. But in my opinion it remains attractive, given its short term and solid safety.

10-year TIPS

The pattern here is similar to the 5-year. Real yields are very high today compared with the last 16 years, but fairly normal for the time before the Great Recession. The 10-year TIPS is a good benchmark, and a 2% real yield meets historical expectations for a Treasury investment. Even though real yields could continue rising, today’s yield levels are highly attractive.

20-year TIPS

For some reason FRED’s data only goes back to August 2004 for the 20 year TIPS. This term was issued at auction by the Treasury from 2004 to 2009, but those ended in January 2009, unfortunately. That’s the reason we have no TIPS maturing in the years of 2036 to 2039.

Today’s real yield of 2.40%+ is very close to the high over the 21-year period shown in the chart. This term is only available on the secondary market, often with high inflation accruals. For that reason, TIPS in the 20-year range are often shunned by investors. I am a fan of this weird term and its attractive real yields, but my TIPS ladder ends in 2043, when I will be 90 years old.

It is worth snooping around the secondary market for attractive TIPS maturing from 2040 to 2045, if you can handle purchasing the accrued principal above par value. Real yields are in the range of 2.25% to 2.53%.

See more: TIPS on the secondary market: Things to consider

30-year TIPS

For the 30-year TIPS, FRED data go back only to 2010, because the U.S. Treasury stopped issuing this 30-year term from October 2001 to February 2010. Again, this is the reason for the gap years in TIPS maturities. As you can see in this chart, the 30-year real yield is close to the high for the last 15 years.

Again, getting a real yield well above 2.0% is historically attractive. A 30-year TIPS is a highly volatile investment, but a good one for investors who know they can hold to maturity and ride out the fluctuations. In 2055 I would be 102 years old. I won’t make it.

Thoughts

Real yields have been on the move for much of 2025, but remain historically attractive through the yield spectrum, especially for terms of 10 to 10+ years. There is a lot of uncertainty right now, both for inflation and future budget deficits. I’d expect the volatility to continue.

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

* * *

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

My omission--Thank you!