By David Enna, Tipswatch.com

Long-time readers of this site know when I go on holiday, bad things happen. There’s consistently a debt crisis overload, a banking crisis, housing collapse, Fed reversals, lavish tariff announcements and roll-backs, etc.

I’ve been touring Scandinavia since May 10. That’s three weeks, but it feels like a lifetime in an era of financial unrest. During that time, I saw very little financial news. Although I could sometimes watch CBNC on board the Viking Vela, my wife usually nixed that channel immediately. Plus, I was dealing with a 6-hour time shift.

So now, knowing little about what happened since May 10, I am going to look at what matters: the actual results.

Our net worth

From May 10 to June 1, our family net worth increased 1.78%. Case closed. This is the only financial measurement that matters, right? Things worked out well, no matter the potential chaos between those dates. But keep in mind that my stock allocation is only 35%. If yours is higher, you did even better.

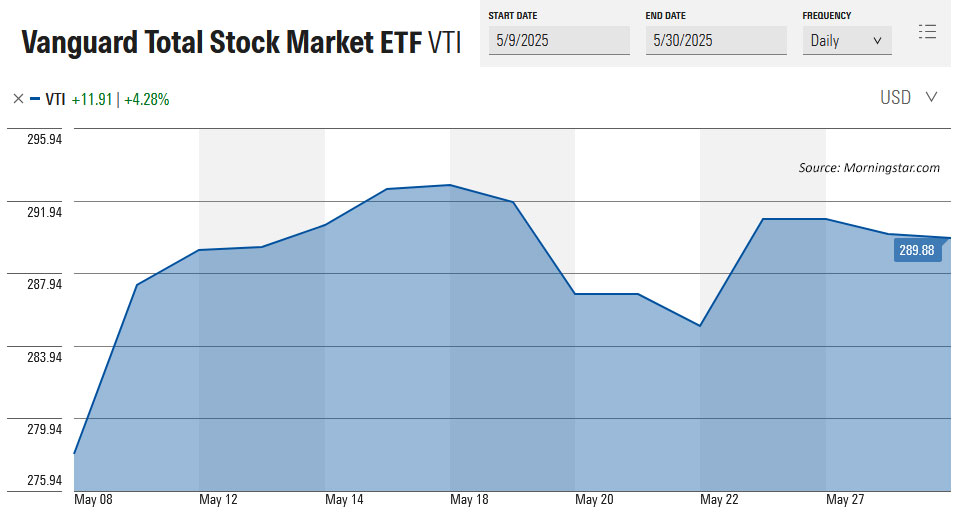

Total U.S. stock market

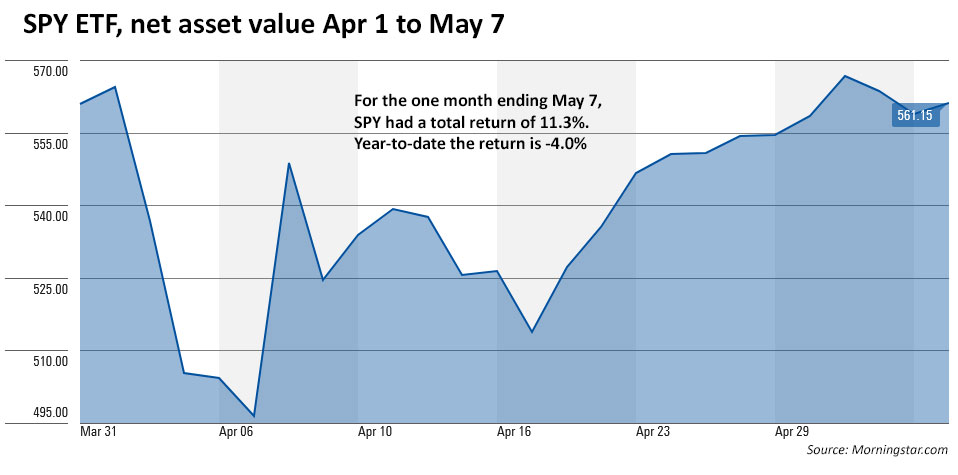

Using Vanguard’s VTI ETF as the baseline, the net asset value of the total stock market had a positive return of 4.28% from May 10 to May 30. Over the last month, its total return (including dividends) was 6.25%.

Total international stock market

Using Vanguard’s VXUS ETF as the baseline, the net asset value of the total international stock market had a positive return of 3.03% from May 10 to May 30. Its total return over the last month was 4.82%.

Total bond market

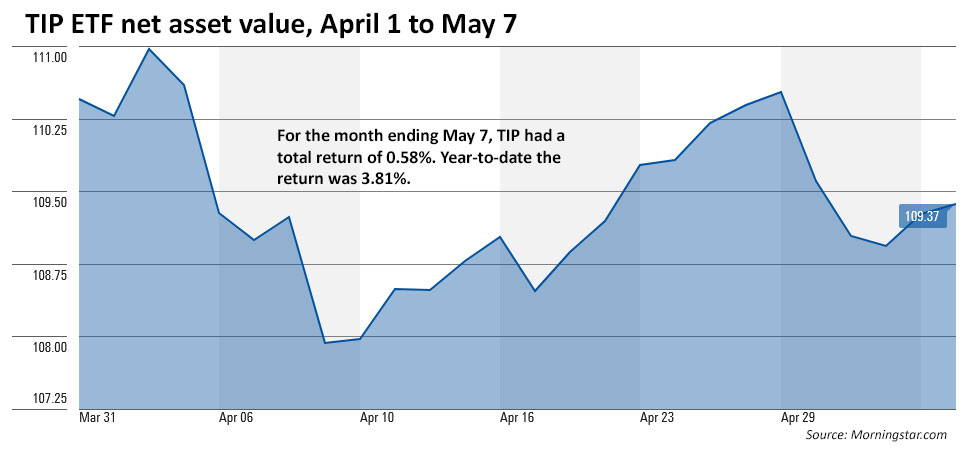

Using Vanguard’s BND ETF as a baseline, the net asset value of the U.S. total bond market increased 0.28% from May 10 to May 30, despite fairly large swings in Treasury yields during that period. However, its total return for the full month of May was -0.67%.

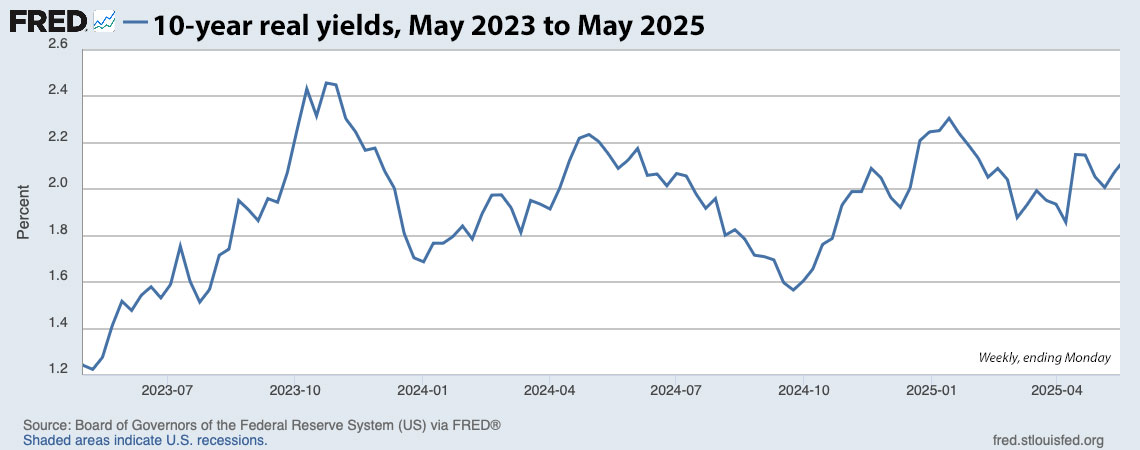

Real yields

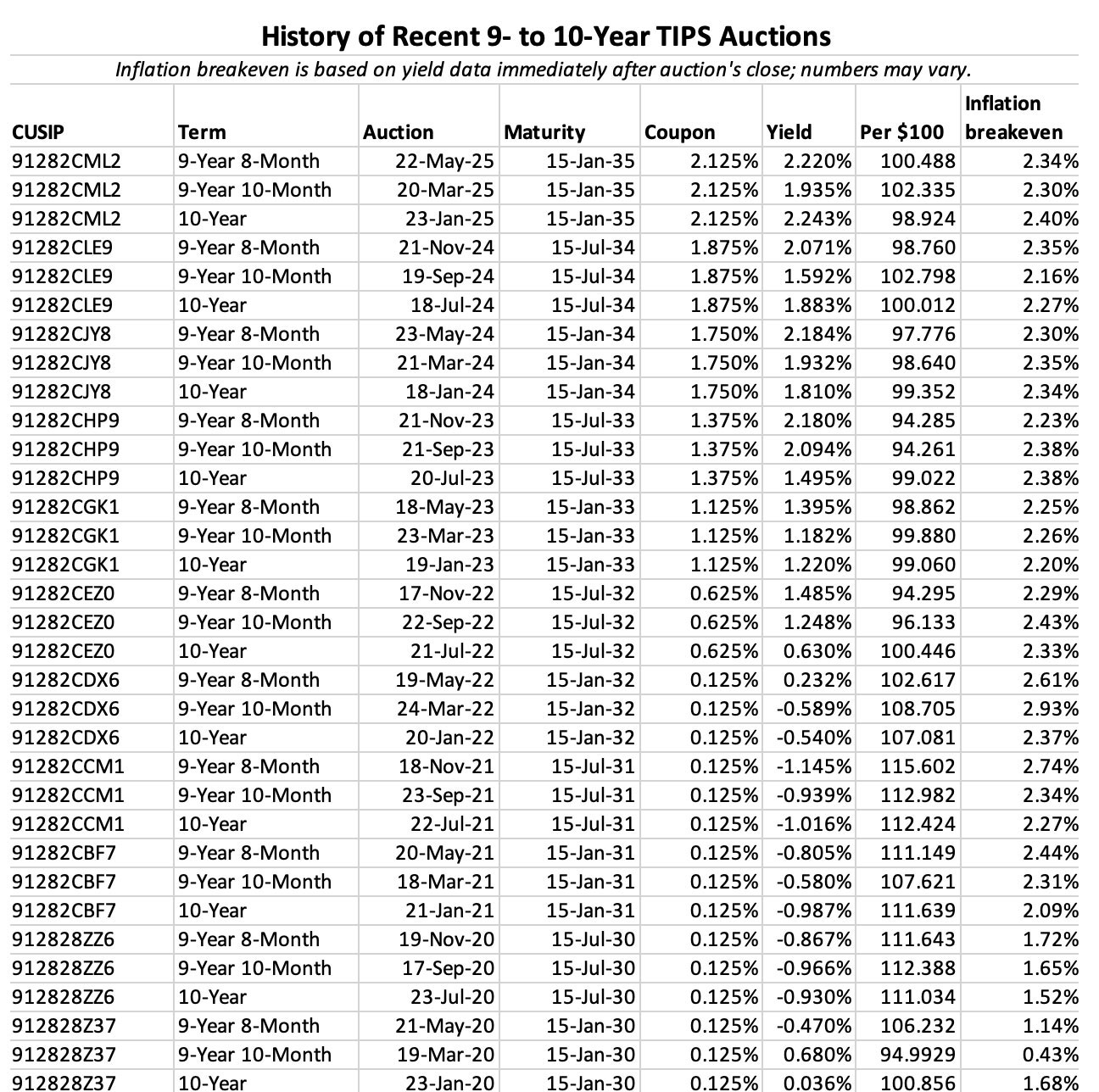

Throughout 2025, the real yield curve of Treasury Inflation-Protected Securities has been steepening. Longer-term investors are being rewarded with higher yields to compensate for the higher risk of a long-term investment. This is actually a return to “normalcy,” but we haven’t seen it often in the last dozen years.

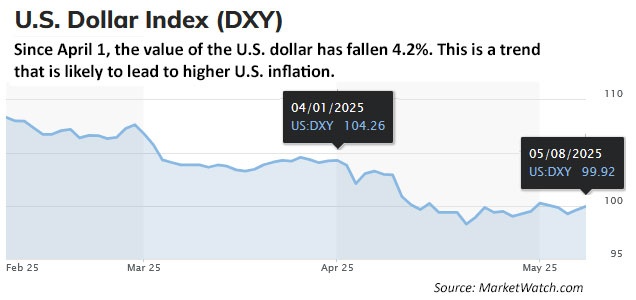

Based on tax and spending proposals moving through Congress, U.S. deficits appear likely to continue increasing (possibly sharply) over the next five to ten years. The bond market is unhappy — and the result is higher yields, especially for mid- to longer-term Treasury investments. Here is what happened over the last three weeks:

What’s interesting in this chart is that real yields ended May at their lowest level of the three-week period. The shorter end of the curve is much lower, possibly reacting to potential Federal Reserve interest rate cuts later in 2025. But the longer-term end of the curve is holding solidly higher. These are attractive levels, in my opinion, for hold-to-maturity investors. Others disagree, as reflected in this report from Bloomberg this morning:

For DoubleLine Capital, there are two approaches to consider when it comes to 30-year US Treasuries: either avoid them, to the degree they can, or outright short them.

Wary of America’s swelling federal budget gap and growing debt burden, the money manager led by Jeffrey Gundlach is part of a wave of investment firms — including Pacific Investment Management Co. and TCW Group Inc. — that are steering away from the longest-dated US government bonds in favor of shorter maturities that carry less interest-rate risk but still offer a decent yield.

Bob Michele, the global head of fixed income at JPMorgan Asset Management, said last week that the long bond isn’t trading now like the risk-free asset Wall Street always believed it to be, and that the possibility of a reduction or cancelation of the auctions is real.

“I don’t want to be the one to stand in front of the steamroller right now,” Michele said in a Bloomberg Television interview. “I’ll let somebody else help stabilize the long end. I’m concerned that it’s going to get worse before it gets better.”

So, despite the positive news that the stock market brought in the last three weeks, the U.S. Treasury market remains troubled. It is impossible to say where real yields are heading, but higher is a definite possibility if the bond market stages a revolt.

In my headline I used the phrase “good things.” I am not sure that the events of the last three weeks match that phrase, but so far the markets are adapting.

What’s ahead

I’ll try to catch up on financial news, of course. We will get the May inflation report at 8:30 a.m. on June 11, then get a 5-year TIPS reopening auction on June 17 (a Tuesday)!

Eventually the debt-limit debacle will reach crisis mode before it is solved. That could end up creating aberrations in the short-term Treasury market. I will be watching for that.

If you have ideas for new content, or just strong (but not overly political) opinions, let everyone know in the comment sections below.

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

* * *

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

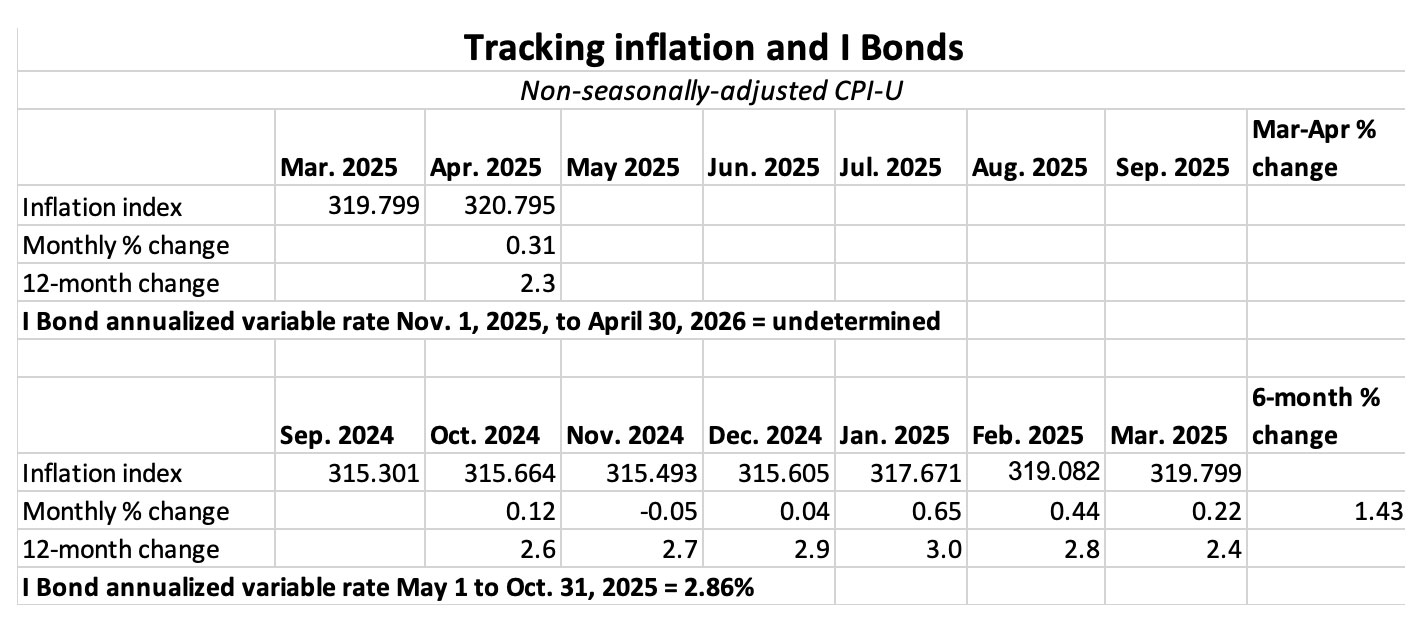

This is where holding I Bonds through six month lulls in the composite rate can pay off. An I Bond…