Here it is, July 2, and half of 2014 has already escaped us. It hasn’t been much of a year for new investments: Both stocks and bonds have rallied this year, making them more expensive, bank CD rates have dropped, and even the I Bond fixed rate has dropped from 0.2% to 0.1%. Not much out there is attractively priced.

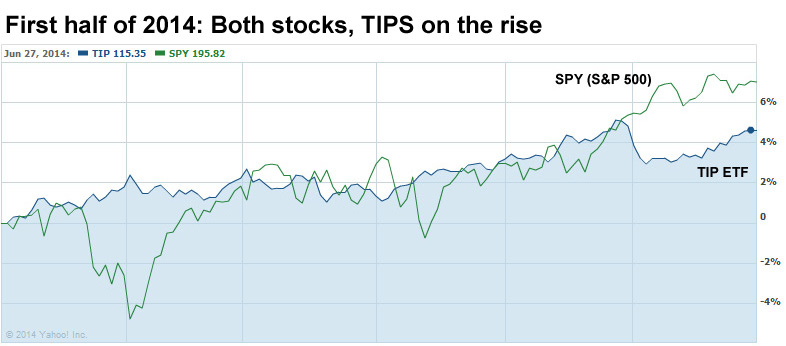

So here it is: Stocks versus TIPS in the first half of 2014. If you held either, you were a winner. This is the ‘Goldilocks market,’ not too hot, not too cold, just plain perfect.

But here is the problem:

But here is the problem:

- Stock prices are increasing because the market expects increasing economic growth, and thus, higher corporate profits. Stocks are a leading indicator, and they are indicating a strong economy.

- Bond prices are increasing (and yields are decreasing) because the markets fear slowing economic growth, as indicated by the shocking decrease of 2.9% in the U.S. gross national product in the first quarter.

Obviously, both of these assumptions can’t be true. The economy is going to 1) grow, 2) decline or 3) stagnate. Either stocks or bonds, and possibly both, are flashing a false signal.

Monetary stimulus in Europe is a factor, because Europe is pouring money into the Euro system in a desperate attempt to keep interest rates low and spur economic growth. And so you get anomalies like this:

- A 10-year US Treasury is yielding 2.61%.

- A 10-year German government bond is yielding 1.25%.

- A 10-year French government bond is yielding 1.72%.

- A 10-year Spanish government bond is yielding 2.64%.

- A 10-year Italian government bond is yielding 2.83%.

- A 10-year Portuguese government bond is yielding 3.59%.

I’d say the risk factor for the German and U.S. bonds are similar: zero. And so why aren’t the yields closer? The risk factors in France, Spain, Italy and Portugal are much higher than zero, but the yields don’t reflect that risk. The low yields in Europe are placing a cap on U.S. yields — you could argue that 2.61% remains too high in this environment.

TIPS yields have declined. The best day of 2014 to buy a 10-year TIPS on the secondary market was Jan. 3. The yield that day was 0.75%, and has been lower every single day since then, bottoming out at 0.22% on May 29. It stands at 0.32% today.

This decline in yield has returned TIPS to the ‘unattractive’ shelf in the investment store. They are expensive. Although I had two TIPS mature this year, I haven’t yet replaced them. The money is stashed in a short-term corporate ETF, awaiting a better buying opportunity.

Inflation and TIPS. We have seen a gradually rising inflation rate over the last six months, creating a rate of 2.1% over the last 12 months. The Federal Reserve will get uncomfortable if inflation rises much higher. Here is the trend:

Is rising inflation good news for holders of TIPS? I’d say yes, if inflation rises to ‘expected’ levels. We buy TIPS to insure against an ‘unexpected’ increase in inflation, but a TIPS will under-perform when inflation lags behind expectations, as it has the last two years.

Is rising inflation good news for holders of TIPS? I’d say yes, if inflation rises to ‘expected’ levels. We buy TIPS to insure against an ‘unexpected’ increase in inflation, but a TIPS will under-perform when inflation lags behind expectations, as it has the last two years.

So if inflation rises to an expected level, the TIPS performs as expected, and that’s boring and fine. If inflation rises to very high levels, the TIPS holder benefits from the ‘insurance’ that this investment provides. But very high inflation could ravage our other holdings. It’s not a desirable thing.

Also, many people think that rising inflation will cause TIPS values to increase on the secondary market — and that TIPS mutual funds, for example, will soar in value. That is true as long as interest rates do not also rise.

If higher inflation results in higher interest rates, the yields on TIPS will rise in lockstep, and the value of TIPS will decline. If the 10-year Treasury rises to 3.5%, you can expect a 10-year TIPS to be yielding at least 1.0%, possibly 1.1% or 1.2%, or higher.

The TIP ETF is trading today at $114.13 and I have speculated in the past that it is heading to $110 as interest rates increase. That is a decline of 4%, which correlates to an increase of 52 basis points in the yield of 10-year TIPS (assuming a duration of 7.66). That would put the yield of a 10-year TIPS at 0.87%, where it closed on Sept. 16, 2013. The TIP ETF closed at $110.14 on that day. In other words: This is entirely possible, not a wild fantasy.

I have no idea where the stock market is heading, but this is what I see as the future of TIPS. How long will it take? Who knows?

This trend can’t continue.

It is true that I could have redeemed it when the rate was 1.9%, and maybe could have earned more…