April 30 update: I Bond gets a new fixed rate of 1.10%, composite rate of 3.98%

By David Enna, Tipswatch.com

Sometime on Wednesday, April 30, the Treasury is likely to unveil its new fixed, inflation-adjusted and composite interest rates for the U.S. Series I Savings Bond. In the past, using reliable analysis methods I could tell you:

- The new inflation-adjusted rate will be 2.86%, up from the current 1.90%.

- The fixed rate will be 1.10%, down from the current 1.20%.

- The composite rate, which combines the fixed and variable rates according to a set formula, will be 3.98%, up from the current 3.11%.

I think these will be the most likely results for I Bonds purchased from May to October 2025. In fact, I am fairly confident these will be the results, but not 100% confident. There are too many uncertainties in Washington these days for certainty.

Inflation-adjusted rate

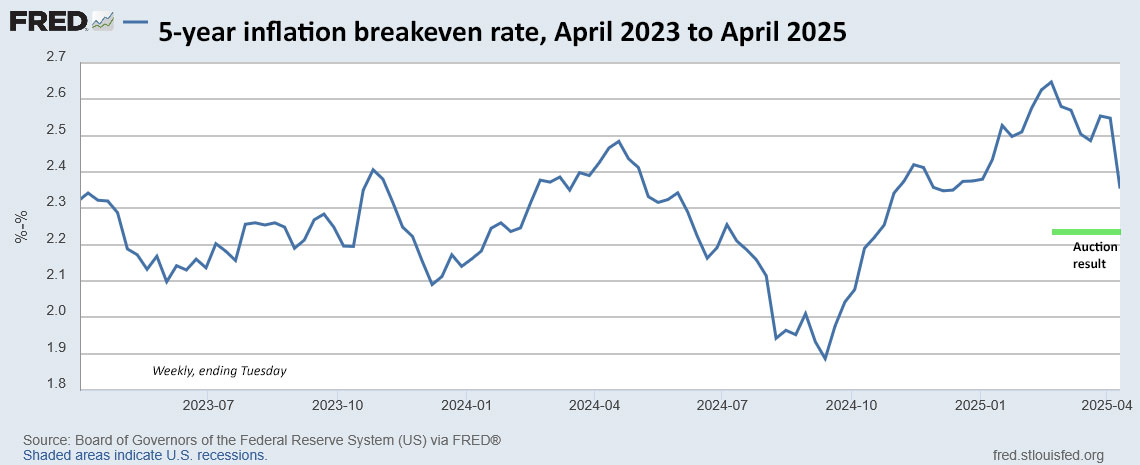

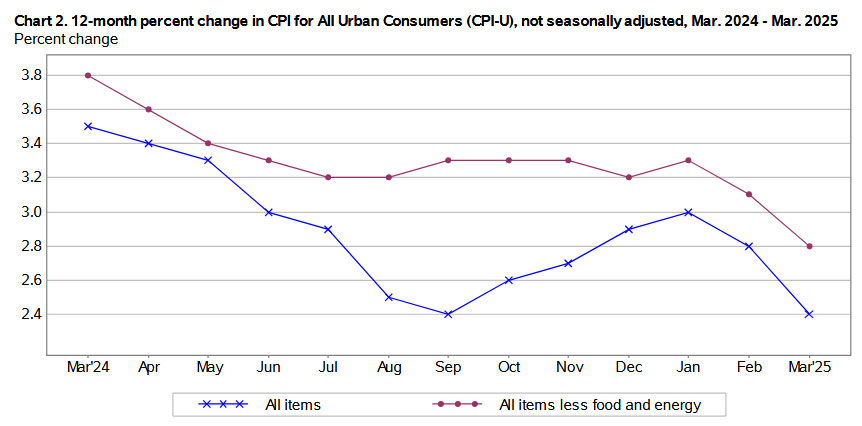

Of these three, the inflation-adjusted variable rate of 2.86% is a certainty. It is based on six months of inflation from October 2024 to March 2025, which ran at 1.43%. That rate is doubled to reach the variable rate of 2.86%.

The fixed rate

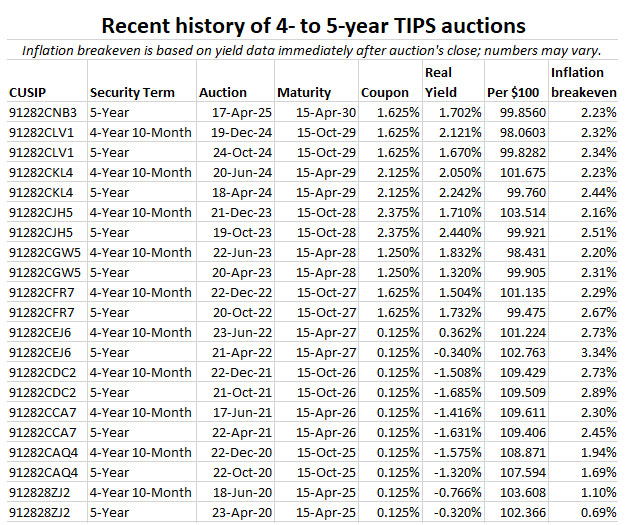

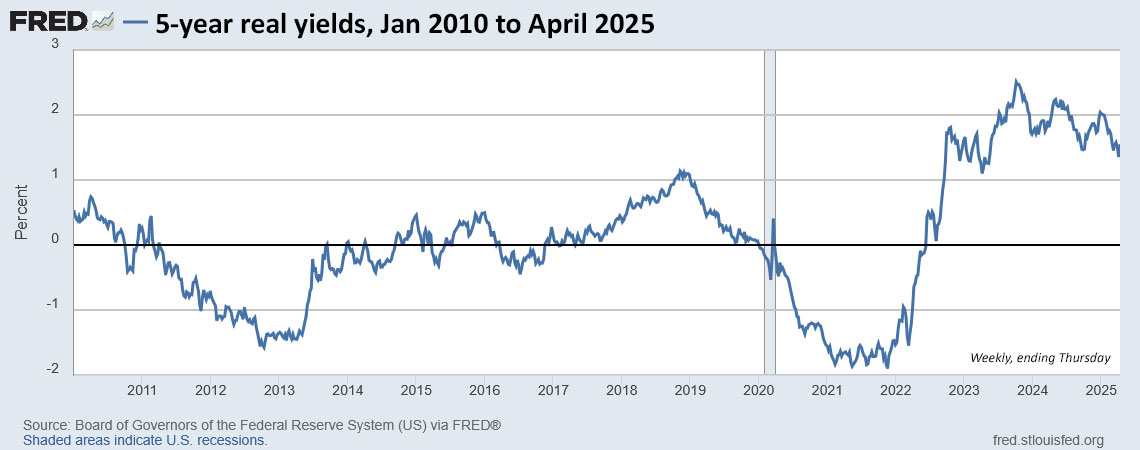

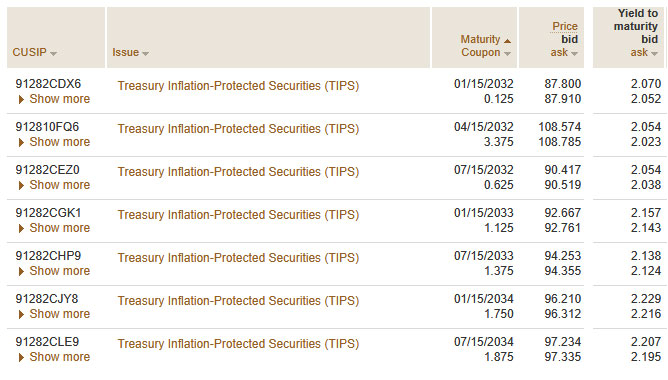

The Treasury has no announced formula for setting the I Bond’s fixed rate, meaning there is no calculation required by law or regulation enforcing the process. It is up to a decision by Treasury officials. However, I Bond watchers have settled on a forecasting tool that seems to work: Apply a ratio of 0.65 to the average 5-year TIPS real yield over the preceding six months. This formula has worked without fail at least since 2017.

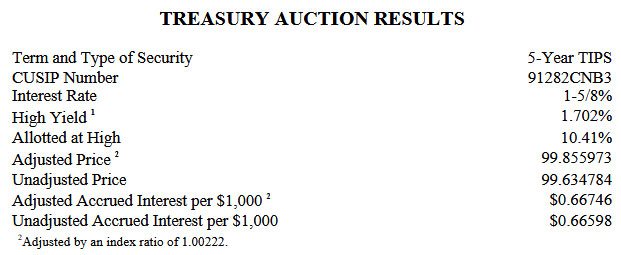

On Friday I updated my 5-year real yield data from the date of the last reset on November 1, 2024, to the close of April, 25, 2025. The data predict the I Bond’s fixed rate will fall to 1.10% at the May 1 reset:

The I Bond’s fixed rate is always set to the one-tenth decimal point and that means the result of the 0.65 ratio calculation has to be rounded, which results in a projection of 1.10%. This has been the running result for more than a month and won’t change in the few days before the reset.

However, there is no way to be sure what formula, if any, the Treasury will use to set the new fixed rate. I think the result will be 1.10%, but this is not certain. This week’s reset could jumble everything. I hope that won’t happen.

The composite rate

The I Bond’s composite rate isn’t calculated by simply adding the variable and fixed rates. The Treasury uses a formula that adjusts for compounding factors of the fixed rate:

[Fixed rate + (2 x semiannual inflation rate) + (fixed rate x semiannual inflation rate)]

So if my prediction of a fixed rate of 1.10% and inflation rate of 1.43% are correct, the new composite rate calculation will look like this:

0.011 + (0.0286) + (0.0001573) = 0.0397573

Rounding gives you 0.03976. Turning the decimal number to a percentage gives a composite rate of 3.98%.

I believe this will be the result of the May 1 reset, but I cannot be 100% certain. The U.S. Treasury is currently undergoing an overhaul, including cuts to employees in the Bureau of Fiscal Services, which oversees the savings bond program. From an April 10 article on Govexec.com:

The Treasury Department has begun slashing some offices as part of President Trump’s efforts to reduce the federal workforce, adding several divisions of the Bureau of Fiscal Service to the cut list.

The department is outsourcing the work at the bureau’s Servicing of Savings Bonds, Debt Cross-Servicing Program and Paper Check Printing and Ancillary Services offices. The exact number of employees impacted was not immediately clear but multiple employees familiar with the matter expected it to be hundreds.

An investment quandary

There is still time — but urgently short — to buy an April 2025 I Bond with a fixed rate of 1.20% and a composite rate of 3.11% for six months, before transitioning to a composite rate of 4.08% for the next six months. A purchase in May is likely to earn 3.98% for the first six months, and then an uncertain rate for the next six months.

A higher fixed rate is always a positive, but in this case 10 basis points doesn’t make a huge difference, especially since buying in May gets you a higher starting variable rate. I consider this decision a toss-up, as I wrote in my ‘I Bond Buying Season‘ article.

To purchase an April 2025 I Bond, I highly recommend placing your order on Monday, April 28, to give it time to clear the Treasury process. Purchases on April 29 will also likely be successful, but a purchase on April 30 will be getting the May issue with new rates.

Update: To demonstrate this, on the morning of April 30 I entered a test I Bond order for purchase on April 30 and this is the result:

Purchasing in April results in the most certain result for the investor: A permanent fixed rate of 1.20% and a composite rate of 3.11% for six months and then 4.08% for six months.

If you decide to wait until May, I suggest waiting until late in the month, like around May 28, to make the purchase, since you will earn a full month of interest no matter the date you purchase.

Wait until October?

Once you enter the May to October buying period, you are assured of getting that rate for a full six months, so delaying a purchase until October is fine. Why do that? Because we are seeing high volatility in Treasury yields and could potentially experience a combination of higher inflation, higher budget deficits, a looming debt-limit crisis … and on and on.

- Interest rates could fall by October, but that won’t affect your I Bond purchase. The new composite rate will stay in effect until October 30.

- Or interest rates could soar higher, and then a November purchase may look more appealing, because the fixed rate could rise.

- Or … nothing much will happen to interest rates and you could simply buy in October.

The risks of waiting

The Treasury this week could decide on an oddball, below-expectations fixed rate of 0.50%, with nothing to say about why. (It never explains these decisions.) That is very unlikely to happen, but it could happen.

Or, Treasury could eliminate new purchases of savings bonds entirely, as it did last year with paper I Bonds and payroll-deduction purchases. Again, this is very unlikely.

If things happen as we expect, with the fixed rate set at 1.10%, waiting is a fine move. But there is an air of uncertainty … which will be cleared away on April 30 — or possibly May 1 if Treasury reverts to its old announcement policy.

Of course, I plan to post the rate news on Wednesday (or possibly Thursday) as soon as I get it. The Treasury doesn’t follow a specific schedule for this. It may post the new rates Wednesday morning (because purchases on Wednesday will get the new May rate) but it may not update informational pages until Thursday.

FYI: I focused this article on future rates and didn’t attempt to explain the investing purposes of I Bonds or their intricacies. You can find a lot of that information in these links:

• April 11: Welcome to the I Bond ‘buying season’

• April 3: My I Bond fixed-rate projection just fell to 1.10%

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

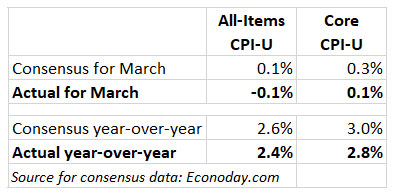

It definitely caused at least a small reduction in six-month inflation. What's amazing is if the United States didn't attack…