The U.S. Treasury just posted the result of today’s auction of CUSIP 912828VM9, a 9-year, 10-month reissue of a TIPS first auctioned on July 18, 2013. It auctioned with a yield to maturity of 0.5% (plus inflation), the highest yield for any 9- or 10-year TIPS auction since July 2011.

The U.S. Treasury just posted the result of today’s auction of CUSIP 912828VM9, a 9-year, 10-month reissue of a TIPS first auctioned on July 18, 2013. It auctioned with a yield to maturity of 0.5% (plus inflation), the highest yield for any 9- or 10-year TIPS auction since July 2011.

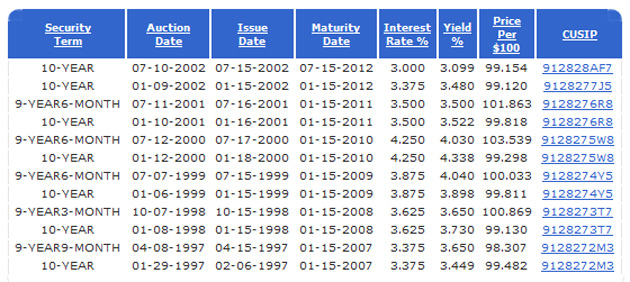

Here is the auction results announcement.

This Treasury Inflation-Protected Security has a coupon rate of 0.3.75%, so that means today’s buyers will get it at a slight discount, about $99.18 per $100 of value, which includes about 78 cents of inflation adjustment accrued since July.

Although the yield of 0.5% was the highest in more than two years, it was lower than the 0.8% that looked likely as recently as last Friday. The Federal Reserve announced Wednesday that it would hold off on tapering its bond-buying stimulus. That sent TIPS yields plummeting, following a weak jobs report last week and a mild inflation report this week.

The yield was slightly higher than the 0.488% projected this morning in a Bloomberg survey of dealers. The initial reaction, indicated by trading in the TIP ETF, looks negative:

Inflation breakeven rate

The 10-year nominal Treasury is trading this afternoon at 2.73%, creating a 10-year inflation breakeven rate of 2.23% for this TIPS. That is up about 10 basis points from the July auction, indicating that TIPS have gotten slightly more expensive versus a traditional Treasury.

Dr Matt....Sell and buy options