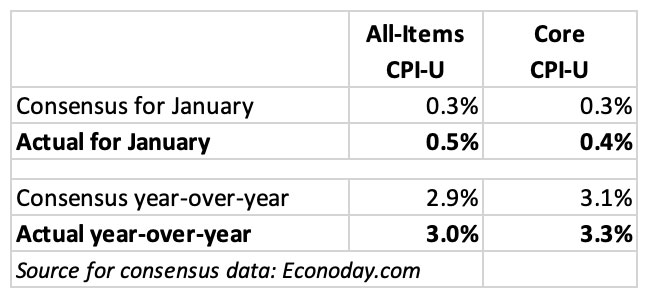

Annual rates for both all-items and core inflation fell from January levels and came in under expectations.

By David Enna, Tipswatch.com

Finally, some good news on inflation. The February inflation report just released by the Bureau of Labor Statistics shows inflation moderating, with annual rates for both all-item and core inflation declining.

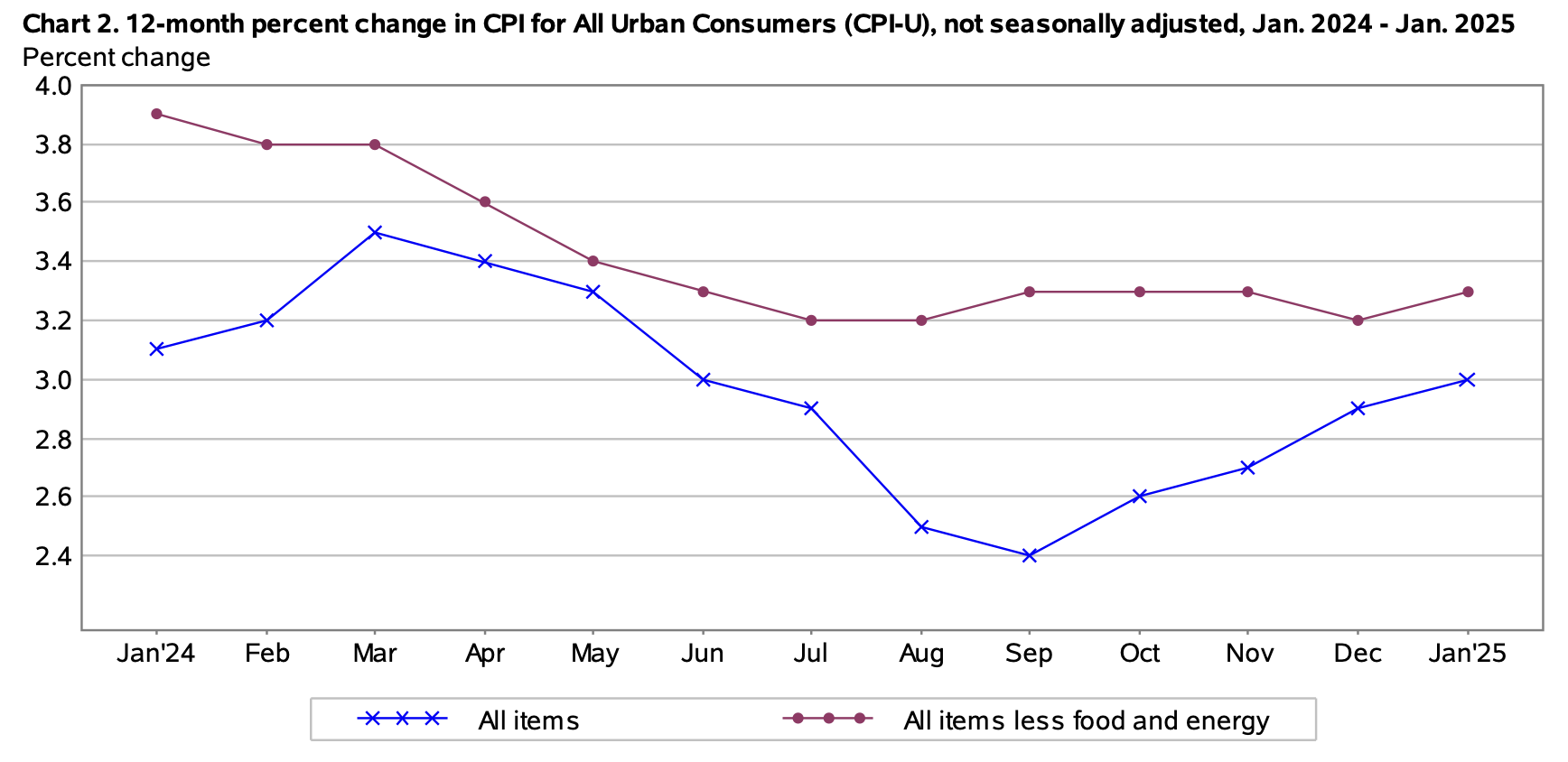

All-items inflation, measured on a seasonally adjusted basis, came in at 0.2% for the month and 2.8% for the year. Core inflation, which removes food and energy, was 0.2% for the month and 3.1% for the year. This was below expectations, and also below January’s annual numbers of 3.0% for all-items and 3.3% for core.

The BLS noted that shelter costs rose 0.3% in February, accounting for nearly half the February all-items increase. Shelter costs were up 4.2% for the year, but the BLS noted that was the smallest 12-month increase since December 2021. Also from the report:

- Food at home prices were unchanged for the month and up 1.9% for the year.

- The price of eggs was up 10.4% for the month and a frightening 58.8% for the year.

- Gasoline prices fell 0.9% and are now down 3.2% annually.

- Electricity costs, however, were up 1.0% for the month and 2.5% for the year.

- Costs of used cars and trucks rose 0.9% for the month but are up only 0.8% over 12 months.

- New vehicle prices fell 0.1% for the month and are down 0.3% for the year.

- Airline fares fell a sharp 4.0% for the month and are down 0.7% for the year.

- Costs of motor vehicle insurance rose 0.3% for the month and are up 11.1% for the year.

Here is the 12-month trend in annual all-items and core inflation, showing how both all-items and core inflation broke lower in February, with core reaching its lowest annual level since April 2021:

What this means for TIPS and I Bonds

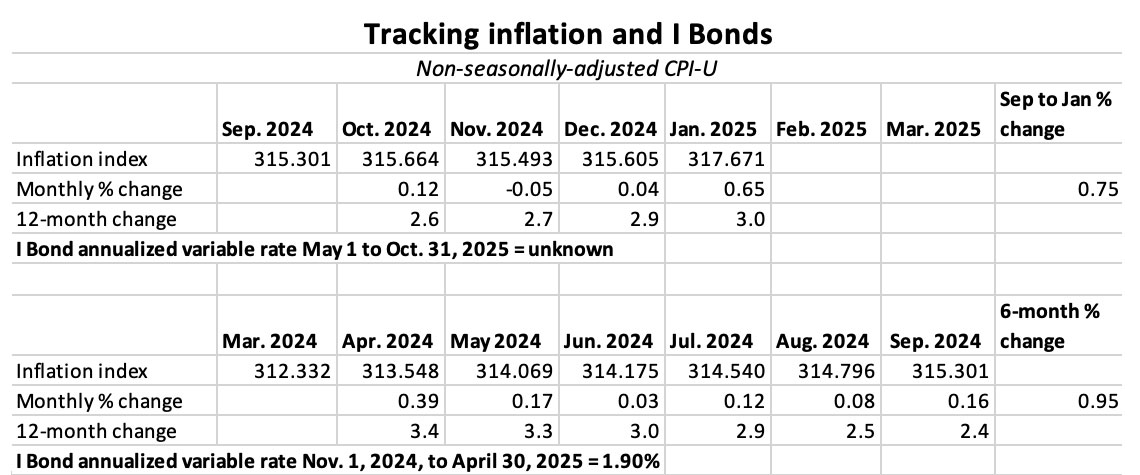

Investors in Treasury Inflation-Protected Securities and U.S. Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances on TIPS and set future interest rates for I Bonds. For February, the BLS set the inflation index at 319.082, an increase of 0.44% over the January number.

For TIPS. The February inflation index means that principal balances for all TIPS will increase by 0.44% in April, after rising 0.65% in January. Keep in mind it is normal for early-year non-adjusted inflation to run higher than the adjusted CPI. That will reverse later in the year. Here are the April Inflation Indexes for all TIPS.

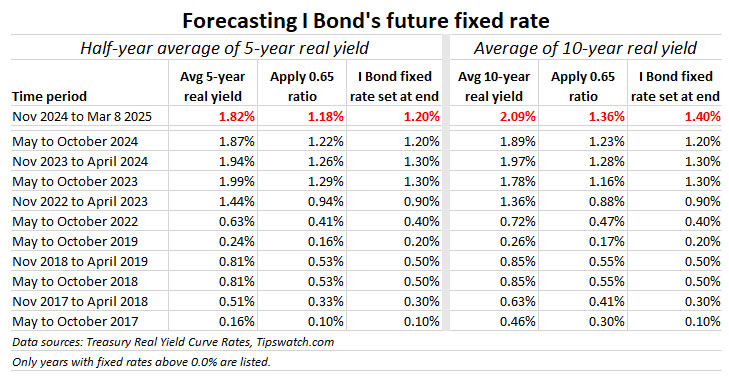

For I Bonds. February marks the fifth of a six-month string that will determine the I Bond’s new variable rate, which will be reset on May 1 and eventually roll into effect for all I Bonds. As of February, with one month remaining, inflation has increased 1.20%, which would translate to a variable rate of 2.4%. The March number seems likely to push that up to about 3.0%, much higher than the current 1.90%.

This trend is going to make I Bonds an interesting investment in 2025, potentially offering a composite rate of about 4.1% or 4.2% for six months, at a time when short-term rates could be declining. I’ll have more on that after the March inflation report is issued on April 10. Here are the data so far:

What this means for future interest rates

The February inflation report provides good news for the Federal Reserve, with annual inflation finally moderating after increasing from 2.4% in September 2024 to 3.0% in January. As it stands, 2.8% for all-items and 3.1% for core remains too high. But the upward creep has ended.

There are still a lot of unknowns, with the effects of tariffs, federal layoffs, deportations and a potentially weakening economy lingering out there in our future. On balance, I’d say the possibility of short-term rate cuts in 2025 has been increasing. But the key question is: Can inflation continue moderating?

From this morning’s Bloomberg report:

While Wednesday’s report offers some relief, several measures still indicate that inflation is rearing back up again. And with President Donald Trump rolling out a series of tariffs, prices are expected to rise on a variety of goods from food to clothing, testing the resilience of consumers and the broader economy. …

“The combination of easing inflationary pressures and rising downside risks to growth suggest that the Fed is moving closer to continuing its easing cycle,” Kay Haigh, global co-head of fixed income and liquidity solutions in Goldman Sachs Asset Management, said in a note.

And the Wall Street Journal:

Wednesday’s report largely predates President Trump’s recent tariff actions, which means the full effect of the new tariffs aren’t captured.

My reaction is: This February inflation report takes a positive (but small) step toward lower inflation. A lot of uncertainty remains. The Fed will be on hold for the near term.

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I wavered a bit when I heard that the fixed rate is likely to remain 0.9% at the May reset,…