Plus, a few other thoughts on a changing Treasury market.

By David Enna, Tipswatch.com

Long-time readers of this site know what that headline signals: I am on the move. Over the next 3+ weeks I will be traveling in Argentina and Chile, including Rapa Nui, also known as Easter Island.

For me, this trip breaks a long stretch of home life — my last overseas trip (the Alps) ended August 2 and I have enjoyed this break from travel. But now … onward!

Much of the time I will be in remote island and mountain areas, and may not have strong Internet connections. I will attempt to keep up with financial news and reading & answering your comments, but no promises. Expect delays. My article updates will be spotty and ill-timed, I expect. Don’t look for posts every Sunday morning.

What’s ahead

Wednesday, February 12. The Bureau of Labor Statistics will release the January inflation report at 8:30 a.m. ET. I will be in Santiago, Chile, on that day and the time will be 10:30 a.m. This will be a “light activity” day so I hope to get an article posted.

The January inflation report is interesting because it turns the corner on non-seasonally adjusted inflation, which is used to adjust principal balances of Treasury Inflation-Protected Securities and set future interest rates for Series I Savings Bonds. At this point, economists are predicting an increase of 0.3% in seasonally adjusted inflation. The non-seasonal number will be higher.

In January 2024, seasonally adjusted inflation rose 0.3% for the month, but the non-seasonal number was 0.54%. We could see something similar on Wednesday. What to watch: Any upside surprise on inflation would not be good for today’s shaky stock and bond markets.

Sunday, February 16. I will post a preview article (probably brief) on the auction of a new 30-year TIPS set for Feb. 20. I have noticed feedback from readers that this auction is drawing some interest, which is unusual for the 30-year TIPS.

Thursday, February 20. I will be in Buenos Aires on this day, visiting the grave of Eva Perón and then touring the Paraná Delta. The auction closes at 1 p.m. ET (3 p.m. in Argentina). I’ll post a summary of the auction, when I can, probably later in the day.

On Friday, Feb. 21, I will be moving much farther south and beginning my Internet-hunting adventure. Again, please realize that I may not be able to post thoughts or respond to comments.

In other news …

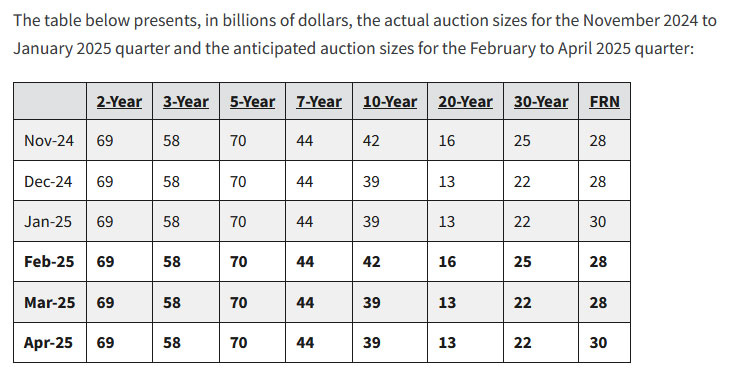

TIPS auction sizes

The Wall Street Journal ran this headline last week: “Treasury Signals No Changes to Bond Auction Sizes.” There had been some speculation the new administration would begin shifting focus from T-bills to longer maturities. It is likely that U.S. borrowing needs will continue to increase in coming months. From the Treasury statement:

But for TIPS, the Treasury is making an exception. It said:

Given the intermediate- to long-term borrowing outlook and the structural balance of supply and demand for TIPS, Treasury believes it would be prudent to continue with incremental increases to TIPS auction sizes in order to maintain a stable share of TIPS as a percentage of total marketable debt outstanding. Over the February to April 2025 quarter, Treasury plans to maintain the February 30-year TIPS new issue auction size at $9 billion, increase the March 10-year TIPS reopening auction size by $1 billion to $18 billion, and increase the April 5-year TIPS new issue auction size to $25 billion.

This follows the trend of recent years, with the 5-year and 10-year TIPS auctions increasing in size for both originating and reopening auctions, but the 30-year remaining at $9 billion, where it has been for four years.

I view this Treasury announcement as an endorsement of TIPS, a valuable and unique inflation-linked investment.

Speaking of Treasury borrowing …

White House Press Secretary Karoline Leavitt on Friday laid out the tax priorities of the Trump administration:

- No tax on tips.

- No tax on seniors’ Social Security.

- No tax on overtime pay.

- Renew Trump’s 2017 tax cuts, set to expire in 2026.

- Increase the deduction for state-and-local taxes, now limited at $10,000.

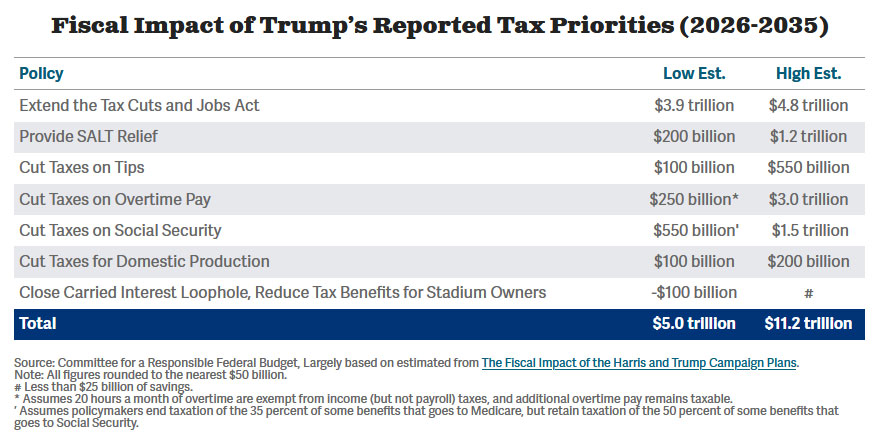

While I would benefit from many of these tax cuts, I have to ask: What is the actual cost and what additional taxes or spending cuts would be needed to ensure that the federal deficit will not increase dramatically in coming years?

Plus, eliminating the tax on Social Security benefits (for higher-income seniors) would speed up the draw-down of its trust fund, which will eventually lead to benefits being slashed by around 23% (now likely to happen in 2033). It could also reduce potential Medicare surcharges, known as IRMAA. While retirees hate IRMAA, those surcharges help keep Medicare afloat.

From a Bloomberg article last week:

President Donald Trump’s tax cut wish list would cost would the federal government between $5 trillion and $11.2 trillion in lost revenue over the next decade, according to a new analysis from … the Committee for a Responsible Federal Budget.

… Without more tax increases or new spending cuts, the proposed tax cuts would drive up the federal government’s debt to between 132% and 149% of gross domestic product by 2035, compared to nearly 100% of GDP currently and 118% in a decade without changes to tax law, the committee forecast. …

Trump proposed a few tax increases, including eliminating the carried interest deduction and ending tax breaks for sports team owners, but those only have a small impact on the deficit, the group estimated.

From the committee’s study:

All along, I have been assuming that the 2017 tax cuts will be extended, with some changes (like the potential SALT deduction increases). OK, that is a given. I realize I cannot foresee the administration’s entire budget-cutting plan, but I suspect taxes will not be increasing enough, and spending won’t be decreasing enough, to cover the potentially giant shortfall.

As investors in Treasurys, we are lending money to the federal government. We should be able to expect some financial discipline.

Reminder: This should not be a political issue. Most Republicans and moderate Democrats agree that the federal deficit should, at least, not be increasing in future years. And in fact, efforts should be made to get the number lower.

Inflation fears are rising

Last week, the real yield of a 10-year TIPS briefly dipped below 2.0%, down about 23 basis points in two weeks, before bouncing back up to 2.07% at Friday’s close. That continues a recent trend, with TIPS real yields declining more than nominal yields, which translates to an increase in the inflation breakeven rate:

Interesting fact to note: Across the board, inflation expectations are well above the Federal Reserve’s target of 2.0% (using a different index), going all the way to 30 years. Investors don’t have confidence that the Federal Reserve, combined with U.S. government policies, can get the job done.

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

[…] I also used to believe that the government would not tamper or attempt to politically influence these BLS CPI…