Others may want to wait and watch for higher real yields.

Jan. 23 update: New 10-year TIPS gets real yield of 2.243%, highest for this term in 16 years

By David Enna, Tipswatch.com

I picked up the December issue of Kiplinger Personal Finance from my nightstand last week and began paging through. And chuckling. Why? Because nearly the entire issue was devoted to investing in a new era of declining interest rates.

Some sample headlines and topics:

- How lower interest rates affect your finances.

- Dividend payers are poised to benefit from falling rates.

- At long last, rates are dropping.

- Rate-cut winners and losers.

- Columnist: “I am wary of long-term Treasurys.”

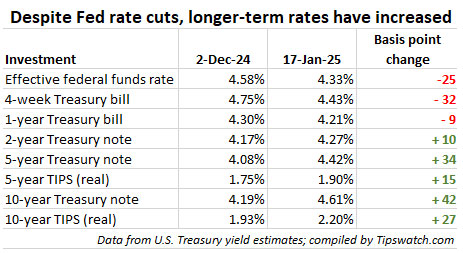

As it turns out, Kiplinger got it wrong. Even though the Federal Reserve continued to cut its federal funds rate by 25 basis points in November and again in December, these cuts had no effect on medium- and longer-term Treasurys. In fact, both nominal and real yields have increased strongly since December 1, 2024.

Let’s give Kiplinger a break, however. I was right with them in expecting to see at least slightly lower medium-term Treasury rates going into 2025. Instead, because of positive economic news and uncertainty about policies of the incoming president, medium- and longer-term rates have been rising.

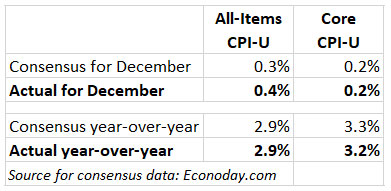

And this all leads up to Thursday’s auction of a new 10-year Treasury Inflation-Protected Security, CUSIP 91282CML2. This will be the first TIPS in history to mature in 2035, and because of that I have long been targeting a purchase at this auction. I need to fill year 2035 in my TIPS ladder. I am pleased to see the potential real yield hovering around 2.20%, despite slipping a bit last week because of a so-called “soft” December inflation report.

Definition: The “real yield” of a TIPS is its yield above official future U.S. inflation, over the term of the TIPS. So a real yield of 2.20% means an investment in this TIPS would provide a return that exceeds U.S. inflation by 2.20% for 10 years.

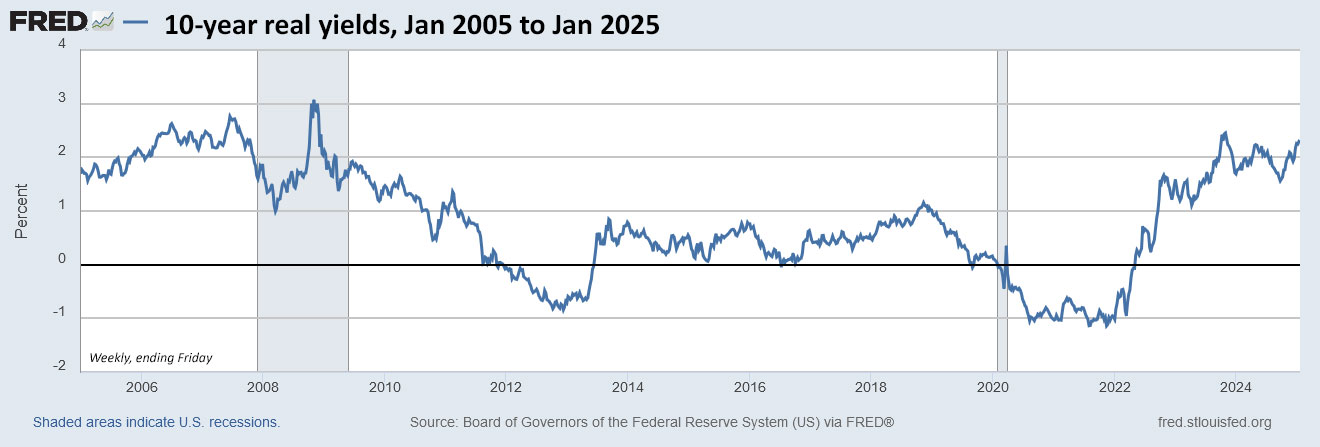

By historical standards, a real yield of 2.20% is attractive. It is actually quite a bit above the historical real return (1.80%) of 10-year Treasurys from 1928 to 2024. Take a look at this chart of the 10-year real yield over the last 20 years:

The lower yields from 2011 to early 2022 were caused by aggressive bond-buying programs of the Federal Reserve, which kept longer-term interest rates suppressed. Now we are in an era of moderate quantitative tightening and yields have returned to more normal levels.

So for me– if rates hold this week — I am going to jump at Thursday’s chance to lock in a 10-year TIPS with a real yield of around 2.20%. A few more things to consider:

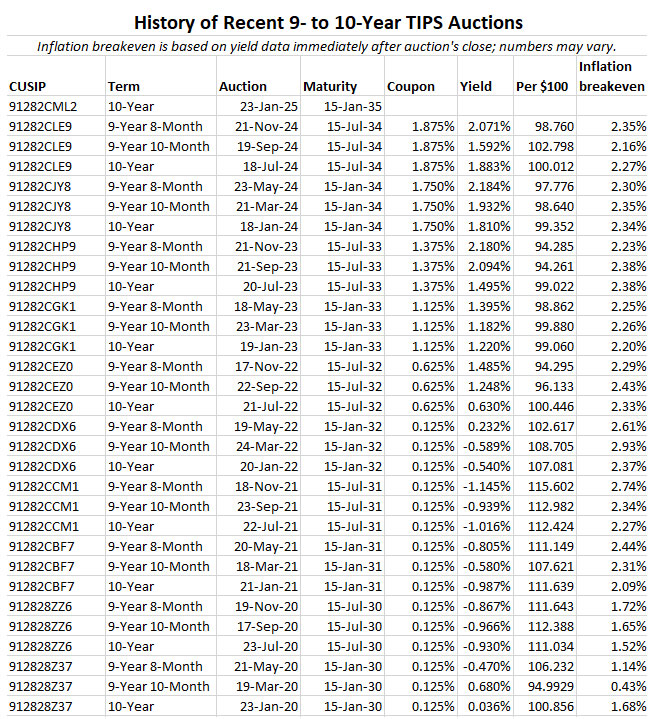

- The Treasury is offering $20 billion of this TIPS, the highest ever for an auction of this term. Last year’s January auction was for $18 billion.

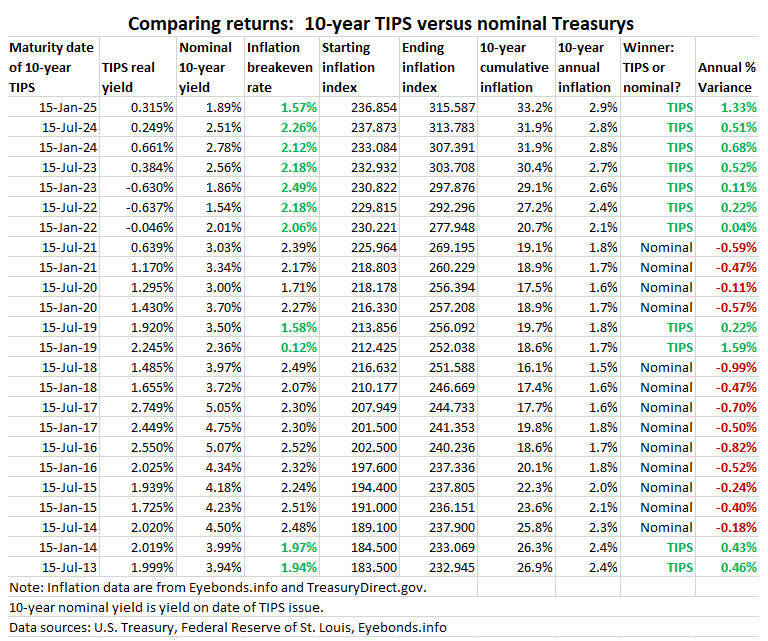

- If the real yield to maturity ends up above 2.20%, it would be the highest real yield for any 9- to 10-year TIPS at auction since January 2009.

- If the coupon rate is 2.125% or higher, it would be the highest for this term since January 2009.

Pricing

This is a new TIPS, so its coupon rate will be set at the 1/8th percentage point level below the auctioned real yield (most likely 2.125% or 2.250%). Because of that, this TIPS is going to auction at a slightly discounted price. Plus, its inflation index on the settlement date of Jan. 31 will be 0.99972, providing another very slight discount.

In other words, a purchase of $10,000 par of this TIPS is probably going to cost just a little less than $10,000 or maybe right at $10,000 after you add in a small amount of accrued interest, maybe $10 or so.

Inflation breakeven rate

With the 10-year nominal Treasury note closing Friday at 4.61%, this TIPS currently would have an inflation breakeven rate of 2.41%, higher than any auction of this term since September 2022. However, U.S. inflation has averaged 3.0% over the last 10 years, so the number isn’t unreasonable. (In my opinion, a 10-year nominal Treasury at 5% would start to get interesting.)

Here is the trend in the 10-year inflation breakeven rate over the last 20 years:

That’s a crazy chart, isn’t it? The shaded areas show the strong effect recessions have on inflation expectations. And yet, over the 20 years, the 10-year inflation breakeven rate never quite reached the 3.0% level of the 2014-to-2024 period. Remember: the inflation breakeven rate is a measure of sentiment, not at all an accurate predictor of future inflation.

Buy now … or wait?

Several readers have asked me why I am going to buy CUSIP 91282CML2 at Thursday’s auction (if yields hold reasonably steady). Why not just wait and buy it later on the secondary market? Waiting could definitely work. … Or not.

Waiting is a bet that real yields will continue to rise, and that definitely could happen. … Or not. My philosophy of TIPS investing is buy a yield you like and don’t look back.

Buying at auction assures me of getting the same high yield as the big-money investors, with no bid-ask spread. Also, because this is a new TIPS, you may not see many small-lot sale offers on the secondary market for several weeks.

The negative of an auction is the uncertainty about the actual yield you will receive. The advantage of the secondary market is that you can see exactly the price and real yield you will get. The negative is that you may face a small bid-ask spread. Most of the time, it doesn’t make a huge difference.

So either way is probably fine, auction or secondary market. I am choosing to go with the auction because this is a new TIPS with a good yield and good pricing. Over this week, you can track the Treasury estimate of the 10-year real yield on this page. Financial markets will be closed Monday in honor of Martin Luther King Jr.

This TIPS auction closes Thursday at 1 p.m. EST. Non-competitive bids at TreasuryDirect must be placed by noon Thursday. If you are putting an order in through a brokerage, make sure to place your order Wednesday or very early Thursday, because brokers cut off auction orders before the noon deadline.

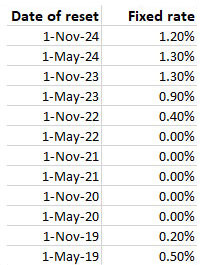

I will be posting the auction results soon after the close on Thursday. Here is a history of auction results for this term over the last 5 years:

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

[…] I also used to believe that the government would not tamper or attempt to politically influence these BLS CPI…